Crypto "Pikachu" Revives: Is Grayscale Coming for Altcoins' Good Days?

TechFlow Selected TechFlow Selected

Crypto "Pikachu" Revives: Is Grayscale Coming for Altcoins' Good Days?

Two months after GBTC's conversion to ETF, Grayscale has quietly increased its offerings of altcoin products, revealing some arbitrage opportunities.

Author: Frank, Foresight News

Once hailed as the "Piloting Beast" and "Bull Market Engine" of the crypto world, Grayscale enjoyed unparalleled prominence before 2021—until January 10 this year, when its golden era abruptly ended.

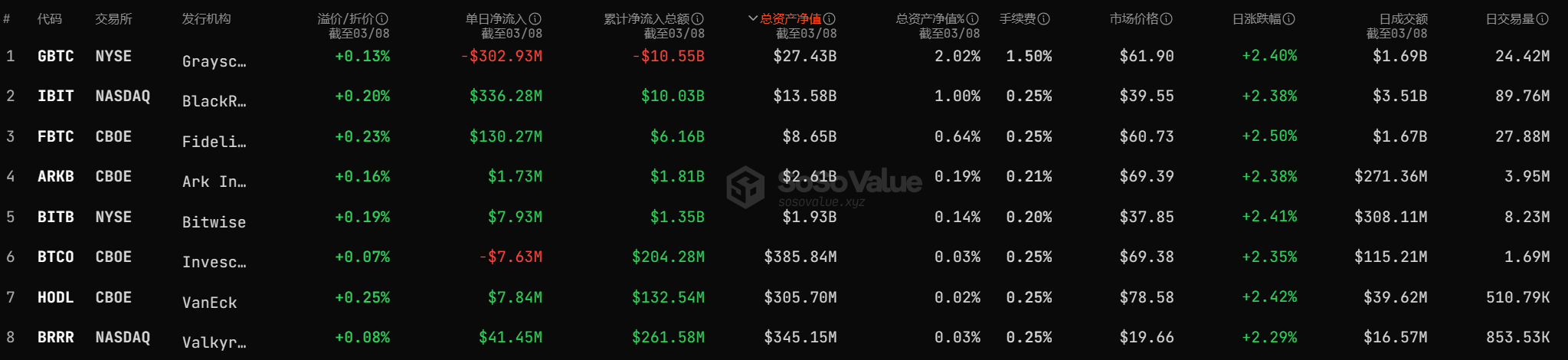

According to SoSoValue statistics, since January 11, GBTC has seen over $10 billion in net outflows, with its total net assets dropping to $27 billion, making it the only one among the 10 spot Bitcoin ETFs experiencing continuous net outflows.

During bull markets, positive factors are amplified; only choices made during downturns are truly representative. Amid this major shift over the past two months, Grayscale has clearly accelerated its pace, rapidly launching new products and expanding its strategic layout. This article aims to provide a concise overview and examine what’s really happening behind the scenes.

Opening Private Placements for Five Altcoin Trusts

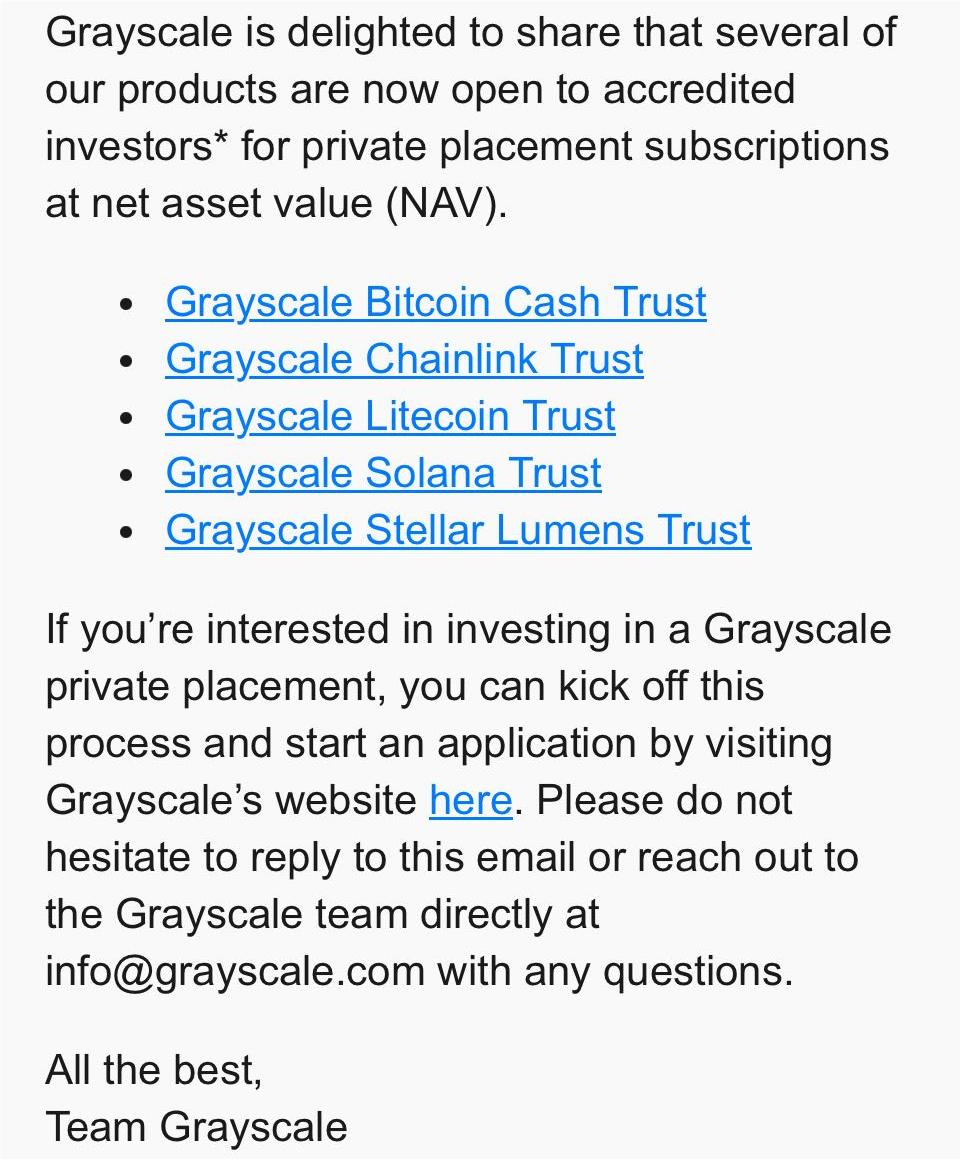

On February 15, Grayscale announced via email that private placements for several cryptocurrency trusts were now open to accredited investors, including the Grayscale Bitcoin Cash Trust, Grayscale Chainlink Trust, Grayscale Litecoin Trust, Grayscale Solana Trust, and Grayscale Stellar Lumens Trust. Subscriptions will be priced at net asset value (NAV).

In short, private placements for BCH, LINK, LTC, SOL, and XLM crypto trusts are now open for qualified investors—according to Grayscale’s official product lifecycle framework, its trust products go through four stages: private placement, public quotation, SEC filing, and eventual conversion into an ETF. Currently, apart from the Bitcoin Trust GBTC, all other crypto trusts remain closed-end funds with no two-way redemption available on the market.

However, Coinglass data shows that within less than a month after opening private placements on February 15, these five altcoin trusts showed clear net inflows compared to other holdings across Grayscale’s fund portfolio:

LTC increased by over 44,300 coins (over $3.5 million), BCH by over 4,062 coins (about $1.6 million), XLM by over 4.92 million coins (about $680,000), and LINK by over 100,000 coins (around $2 million).

Only SOL stands out—netting over 97,500 coins, worth more than $13.5 million.

Given that only GBTC has transitioned into an ETF, why did substantial off-market capital rush into private placements for these five altcoin trusts?

The Arbitrage and Game Theory Behind Subscriptions

The reason lies in the significant premium between primary and secondary markets combined with a unique redemption mechanism creating exclusive arbitrage opportunities.

Premiums Exceeding 130%

As shown in the chart above, it's evident that all five altcoin trusts carry substantial positive premiums—legacy PoW coins like LTC and BCH typically have premiums exceeding 130%, SOL surpasses 870%, and LINK reaches as high as 830% (though the total holding size of the LINK trust is only around $8 million).

This premium specifically refers to the price difference between the underlying cryptocurrency (viewed as the primary market) and its corresponding stock shares traded on the secondary market. Taking LTC as an example, a 161.79% positive premium means the secondary market trading price per share of ETCG is 161.79% of the actual value represented by its underlying ETC holdings.

Under these conditions, combined with Grayscale’s “long-only trust” creation/redemption mechanism, a perfect arbitrage path emerges to exploit and eventually close this positive premium gap.

The "Long-Only Trust" Mechanism

Here we need to briefly explain Grayscale’s nearly “long-only” creation/redemption mechanism for its crypto trusts.

Take GBTC pre-ETF conversion as an example: Grayscale crypto trusts cannot directly redeem their underlying assets—there is no clear exit mechanism, so there is currently no formal “redemption” or “sell-off.”

This implies that these crypto trusts are essentially “long-only trusts”—with inflows but no outflows in the short term (although Grayscale charges a management fee based on a percentage of holdings, deducted in-kind, which explains why holdings gradually decrease over time).

More specifically, using ETCG as an example: investors can acquire ETCG shares either by purchasing them directly on the U.S. secondary market or by depositing the corresponding ETC tokens through private placement, unlocking proportional ETCG shares after the lock-up period (public information indicates a 12-month lock-up).

This creates an arbitrage opportunity: for instance, an investor could participate in the ETCG private placement by contributing ETC in the primary market, receiving equivalent shares based on NAV, while simultaneously opening a short position on the derivative market for the same value of ETCG (if betting that the positive premium will persist after 12 months, even this hedging step could be skipped).

Then, after waiting 12 months, once the ETCG shares unlock, they can be sold on the U.S. secondary market while closing the short position, thereby pocketing the difference between the Grayscale ETCG net asset value and its secondary market price—completing the entire arbitrage cycle.

Put simply, it’s akin to arbitrageurs buying ETC in the crypto spot market while selling ETCG in the U.S. equity market. From a market perspective, the current high premiums on products like ETCG resemble 12-month “call options.”

Yet this highly lucrative call option may represent an asymmetric game—ETCG opens private placements to institutions and qualified investors in the primary market, enabling them to later sell shares on the secondary market, while ordinary U.S. retail investors buying at such steep premiums are clearly at an informational disadvantage.

Indeed, similar situations occurred with Grayscale’s Bitcoin Trust GBTC and Ethereum Trust ETHE from 2020 to 2021, featuring positive premiums and associated arbitrage. However, following cascading shocks like the collapse of Three Arrows Capital and DCG’s crisis in 2022, GBTC’s premium flipped from positive to negative, reaching over 50% at its lowest, effectively shutting down this arbitrage channel.

But starting mid-2023, amid renewed speculation around spot Bitcoin ETF approvals and progress toward GBTC’s ETF conversion, the negatively-priced GBTC created an entirely opposite arbitrage opportunity: buying GBTC at a discount and betting on its future ETF approval, profiting from the expected convergence and premium recovery once converted.

Is Grayscale Accelerating Its Shift Toward Altcoins?

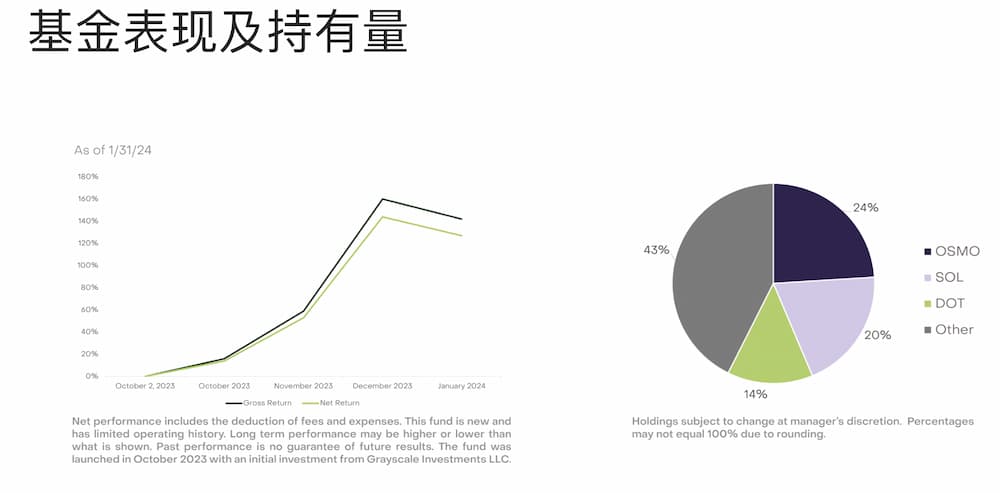

Additionally, on March 5, Grayscale launched its first actively managed fund—the Grayscale Dynamic Income Fund (GDIF).

The fund generates income through staking various cryptocurrencies and initially supports nine blockchain assets: Aptos (APT), Celestia (TIA), Coinbase Staked Ethereum (CBETH), Cosmos (ATOM), Near (NEAR), Osmosis (OSMO), Polkadot (DOT), SEI Network (SEI), and Solana (SOL), with plans to distribute staking rewards quarterly in USD.

Based on the GDIF fund’s disclosed asset allocation, leading positions include OSMO at 24%, SOL at 20%, DOT at 14%, and the remaining portion accounting for 43%, significantly lowering the barrier for external institutional investors to participate in PoS investments.

In many ways, this marks Grayscale’s most significant “product innovation” in recent years—signaling a gradual shift toward active participation in earning native crypto yields, offering institutional investors a simplified way to access PoS staking rewards.

Necessity drives change, and change leads to progress. Since its inception in 2019, Grayscale has stood as a pivotal institutional buyer in the crypto space and one of the largest “transparent whales.” For years, its core narrative has been providing compliant investment channels into cryptocurrencies through trust funds.

However, after the approval of spot Bitcoin ETFs on January 10 this year, Grayscale’s role as an “institutional gateway” began facing sustained outflows due to its relatively high management fees, resulting in significant near-term market selling pressure.

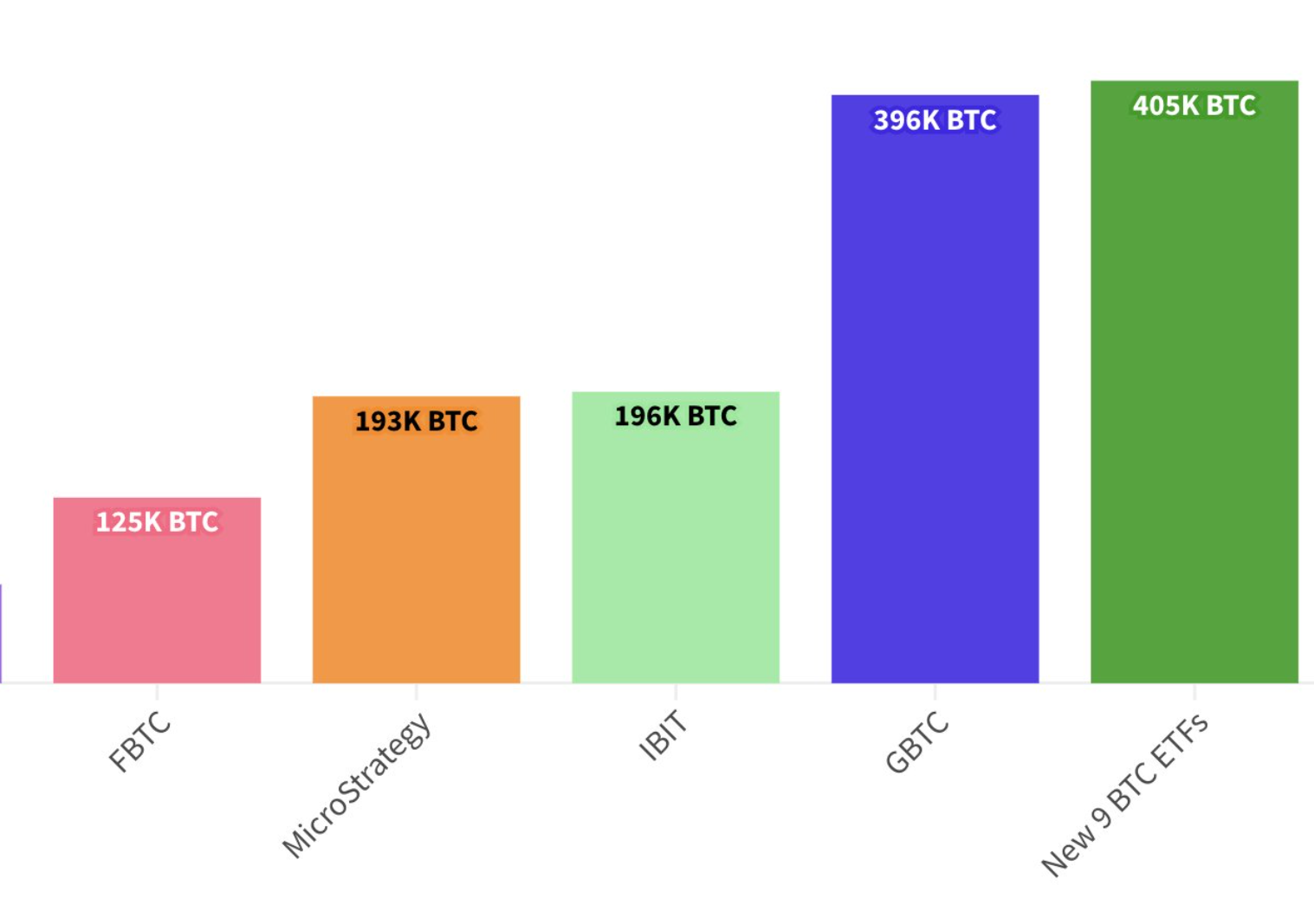

According to monitoring by crypto trader Fred Krueger here, as of the previous trading day, the BTC holdings of the other nine spot Bitcoin ETFs officially surpassed those of Grayscale’s GBTC:

The nine spot Bitcoin ETFs collectively hold 405,000 BTC, exceeding GBTC’s 396,000 BTC—an astonishing surge within just two months, overturning GBTC’s five-year dominance.

Summary

Perhaps for this very reason, Grayscale’s recent moves over the past two months have focused on expanding beyond Bitcoin into altcoins, aiming to diversify revenue streams beyond its now-dethroned Bitcoin Trust by shifting focus toward other crypto trusts to uncover new profit centers.

By replicating its former status as a near-exclusive compliant entry point like GBTC once was, Grayscale hopes to capture the “compliance premium” institutions are willing to pay, continuing to quietly generate profits.

The good old days of tailwinds are always nostalgic, but for Grayscale, whether the easy profits of 2020 can ever return remains uncertain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News