Eternal inflation with only upward price trends? Unveiling the mystery behind YES and its team Baseline

TechFlow Selected TechFlow Selected

Eternal inflation with only upward price trends? Unveiling the mystery behind YES and its team Baseline

How is "only rising, never falling" achieved?

Author: Peng SUN, Foresight News

Recently, YES on Blast has attracted significant attention. Between its meme status, claims of being "up-only," lack of liquidation mechanisms, and multipliers enabling leveraged positions, it already resembles a Ponzi scheme—fueling widespread community FOMO. Even Adam Cochran (AC), partner at Cinneamhain Ventures, joined the discussion in Discord and reviewed all of Baseline’s code. Moreover, key opinion leaders (KOLs) are aggressively buying in. On-chain data shows that Brother Maji established a position of $1.5 million worth of YES yesterday, with an average cost of $4.47 per token.

Yet many are asking: Why does YES only go up? Why is its total supply constantly inflating? Today, Foresight News will unveil the mystery behind YES and its underlying team, Baseline—how it achieves its so-called “Wudang Ti Yun Zong” maneuver, and why it continuously mints new tokens. Let’s start by understanding what YES actually is!

What Is YES?

YES is the first ERC420 token on Blast leveraging Baseline's automated tokenomics, soon to be launched on Blast. However, there remains no clear definition or explanation for BRC-420—the standard supposedly defined by Baseline. Unsurprisingly, this appears to be a new concept invented by the Baseline team.

YES initially opened its Initial Baseline Value (IBLV) presale on March 2 at 10:00, completing 87% of the sale by 03:55 on March 3. The team set a minimum price (IBV) for YES, allowing qualified community members to deposit ETH and purchase YES at this IBV price, capped at 340 tokens per participant:

-

The top 100 users who participated in the Base Invaders game and earned the “Jeet Slayer” role on Discord, along with 400 users who earned the “Based” role, were allocated 228 ETH (67%);

-

Members of the Jimmy Stimmy community received an allocation of 112 ETH (33%).

According to DexScreener data, YES opened trading at 1.92 USDT on the morning of March 3. Within about two hours of launch, YES accounted for half of all trading volume on Blast. By 04:00 on March 4, YES reached a high of 7.07 USDT—an increase of over 3x—and currently trades at 5.83 USDT.

YES brands itself as an “up-only token,” with team members repeatedly hyping the community with FOMO-inducing statements.

YES’s Twitter account even proclaims that YES is “today’s peak, tomorrow’s floor.” However, the official Yes Twitter account was suspended yesterday.

At this point, you might wonder: What exactly is IBLV? Isn’t “only going up” inherently Ponzi-like? So what’s really going on here? Don’t rush—we’ll begin by examining Baseline, the team behind YES, and gradually uncover the truth behind YES.

The Origins of Baseline

If you’ve been following developments on Blast recently, you likely know that Baseline is one of the 47 winning projects selected in Blast’s BIG BANG initiative. Going further back, Baseline was previously known as Jimbos Protocol—a project that suffered a $7.5 million flash loan attack last year. As mentioned earlier, Baseline also allocated a portion of YES tokens to victims of the Jimbos protocol incident (members of the Jimmy Stimmy community).

On July 28 last year, Jimbos rebranded to Baseline Protocol, announcing plans to build a permissionless algorithmic market maker protocol. This protocol expands upon Olympus’ concept of Protocol-Owned Liquidity (POL), using smart contracts to manage token liquidity within concentrated liquidity pools. At first glance, this seems similar to Trader Joe’s liquidity order book or Uniswap v3’s concentrated liquidity model. However, Baseline differentiates itself by aiming to automate market making and optimize liquidity deployment via code—arguing that humans are unreliable and operationally expensive.

Regarding POL, many assume Baseline has close ties to the Olympus team. However, Berachain founder Smokey The Bera has deliberately distanced OHM from Baseline, suggesting that projects borrowing POL concepts should focus on execution rather than riding OHM’s reputation.

Baseline officially launched on February 15 this year. Its mechanism is simple: initial liquidity is fully deployed on Thruster, Blast’s native DEX (a fork of Uniswap v3). Users can deposit ETH to purchase protocol tokens like YES; the deposited ETH forms the protocol’s liquidity position and fuels Baseline’s permissionless market-making and native lending mechanisms. Baseline aims to accumulate sufficient liquidity reserves through various means to maintain a minimum price (BLV) for tokens like YES—even if everyone decides to sell. In practice, assuming no smart contract exploits and continued growth in user and capital base, BLV would never decrease—it would only rise over time.

How Is “Up Only” Achieved? Baseline’s “Wudang Ti Yun Zong”

Within the Baseline protocol, “Up Only” is both a critical technical feature and a narrative element, deeply embedded in meme culture.

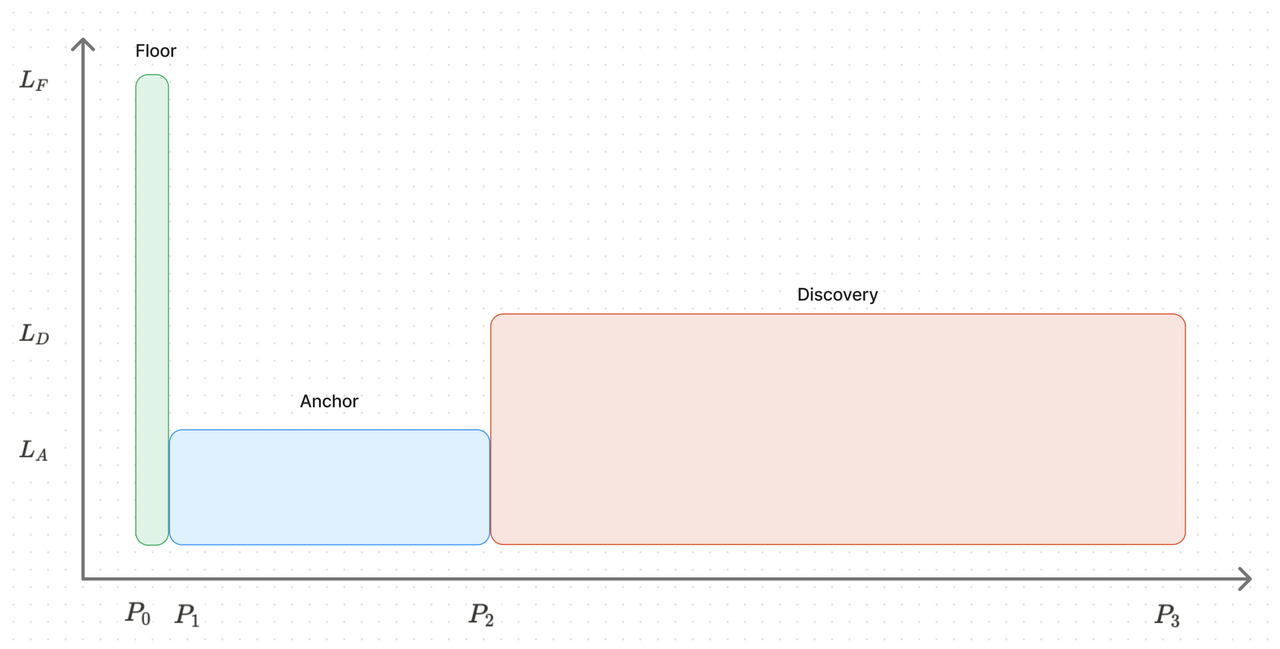

Let’s return to Baseline’s algorithmic market-making mechanism. When users buy tokens like YES and provide ETH liquidity, the resulting liquidity position is allocated across three price ranges: Floor, Anchor, and Discovery:

-

The Floor range has the narrowest spread but the highest concentration of liquidity. When users collectively dump circulating tokens, ample liquidity within this tight range ensures the BLV price remains stable and does not fall;

-

The Anchor range is slightly wider but contains much less liquidity, serving primarily as a transitional zone facilitating movement into the Discovery range;

-

Once liquidity breaks through the Floor and Anchor zones, it enters the broader Discovery range, where normal trading occurs. Liquidity here is more dispersed, allowing greater price volatility and upward momentum.

* Currently, YES’s market price is 0.001601 ETH (~5.77 USDT), BLV floor price is 0.00116 ETH (~4.18 USDT), Anchor price range spans 0.0012 to 0.0016 ETH (~4.32–5.77 USDT), and Discovery ranges from 0.0016 to 0.3679 ETH (~5.77–1327 USDT).

Typically, when whales enter, large capital pushes past the Anchor range, minting new tokens within the Discovery range and selling them at profits above both BLV and Anchor levels. Once sufficient profit accumulates, the algorithmic market maker triggers the shift() function, raising the upper bound of the Floor range and proportionally increasing the lower bound of the next Discovery range. Simultaneously, the protocol transfers some ETH from the Anchor position into the Floor to strengthen its liquidity. With enough profit, the protocol may even repurchase all circulating tokens at higher prices, boosting the floor value and redeploying additional ETH liquidity into a new Anchor position. Project teams can also manually adjust price ranges into the Anchor zone. Additionally, during price declines, the liquidity rebalancing strategy uses slide() to move the Discovery position toward the current market price while compressing the Anchor range—without affecting the Floor price. If this still feels abstract, you can simulate Baseline token liquidity allocations yourself at: https://baseline-simulations.streamlit.app/.

By now, do you detect strong Ponzi undertones? Baseline generates profits precisely by selling tokens at a premium, ensuring protocol revenues consistently exceed the value of circulating tokens.

Next, let’s examine Baseline’s lending mechanism, which employs over-collateralized loans with a Loan-to-Value (LTV) ratio of 100%. Furthermore, since Baseline extends POL principles, the security of protocol-owned liquidity eliminates concerns about capital withdrawal risks. Notably, Baseline’s lending carries zero liquidation risk—each token is backed by Floor price reserves. The protocol never seizes borrower assets. Instead, if a borrower defaults upon loan maturity, the collateral is simply burned, reducing both circulating supply and reserves in proportion to the intrinsic value.

In Baseline’s design, users can deposit purchased tokens to borrow ETH, then use that borrowed ETH to buy more tokens—creating leveraged positions. In other words, without liquidation risk, purchasing a Baseline token enables 2x leverage via collateralized borrowing. A single user’s actions thus help propel the token price upward in a self-reinforcing loop—akin to mastering the Wudang Ti Yun Zong technique. Note, however, that each user can only open one loan at a time, paying a one-time fee of 0.01095% when initiating the loan.

Now, let’s break down how Baseline generates protocol profits to increase BLV, through three main channels:

-

LP Revenue: Baseline’s LP income is primarily generated within the Discovery range, where approximately 78% of liquidity is currently deployed (though not yet active). This pool charges a 1% fee on swaps, directly contributing to BLV floor price increases.

-

Liquidity Rebalancing Fees: During shift() operations, part of the proceeds are funneled into the Floor range to boost liquidity. When BLV rises, the protocol calculates surplus tokens and sends a portion to the team (since all liquidity resides within the protocol, the team receives no direct token allocation);

-

Lending Fees: One-time daily fees paid when opening or extending loans are directly used to increase BLV.

The Protocol Mystery: Is YES Forever Inflating?

Many are confused: Why does the total supply of YES keep rising on the Blast explorer? Community members refer to this as the “Mystery of the Protocol,” with no one fully understanding what’s happening. Meanwhile, existing materials about YES and Baseline tend to avoid discussing inflation altogether—unsurprising, given that even Baseline’s documentation offers no explanation.

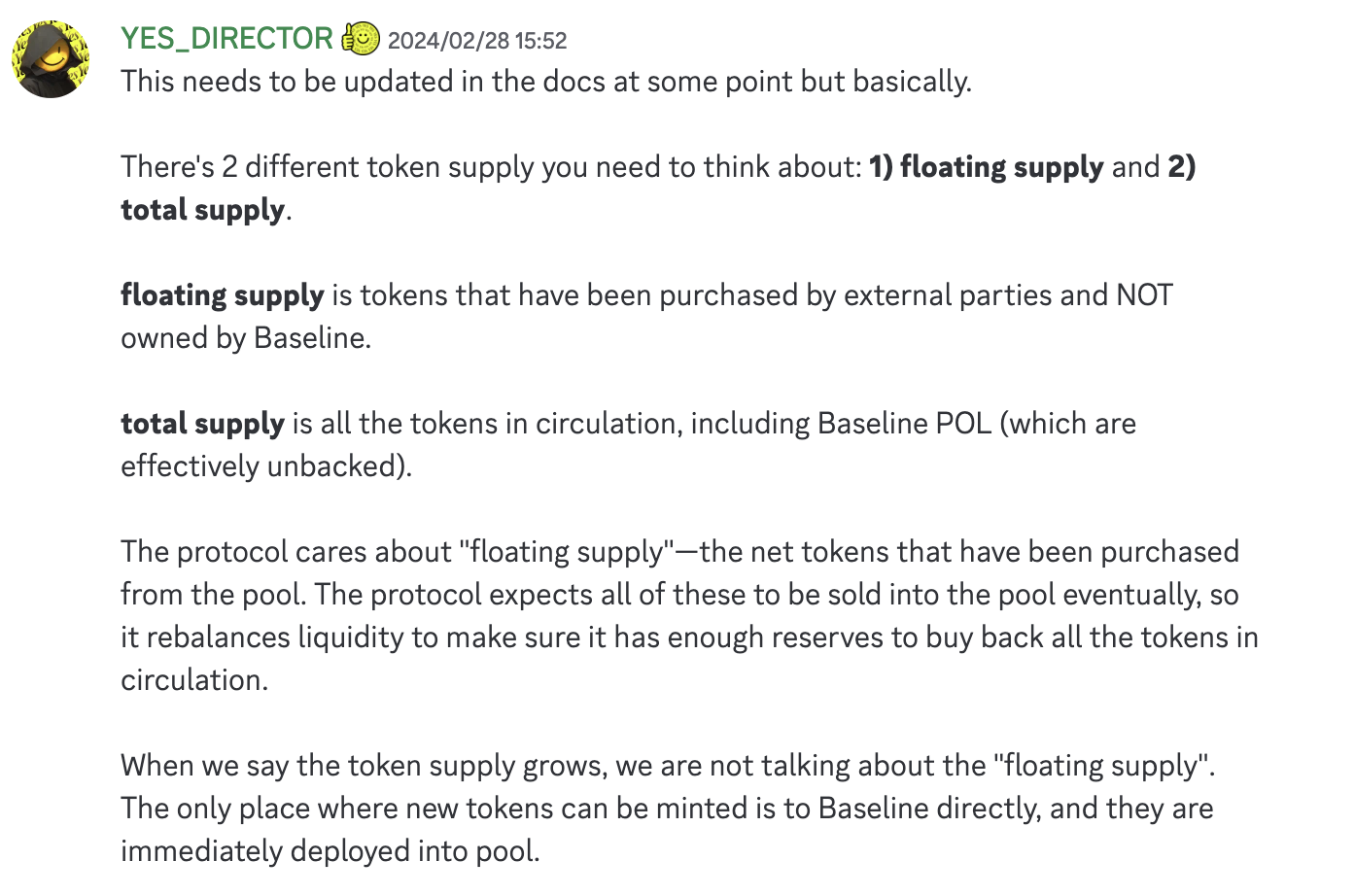

However, after digging through Discord, I found some clues. In reality, Baseline’s automated tokenomics operates on two levels: floating supply and total supply.

Floating supply refers to all tokens outside Baseline’s liquidity positions—essentially, tokens that have been purchased by users and are no longer owned by Baseline. Holding tokens means they belong to the floating supply. If tokens are burned, they’re excluded from floating supply. Think of this as equivalent to conventional circulating supply.

Baseline’s total supply includes all tokens in circulation, including Baseline POL positions not backed by reserves. However, POL is not counted toward the circulating supply of tokens like YES. For example, only when ETH liquidity is matched with newly minted YES tokens does it form a protocol-owned liquidity position capable of being added to the liquidity pool.

The protocol focuses on “floating supply”—the net number of tokens purchased from the pool. As previously analyzed, Baseline aims to maintain sufficient reserves to repurchase all circulating tokens, ensuring BLV never drops below the Floor price range. But this depends on having adequate liquidity in the Recovery pool to generate profits for the Floor and reinforce BLV pricing.

Therefore, the continuous growth in YES supply observed on explorers does not reflect growing floating supply. Rather, it reflects newly minted YES tokens issued to deploy POL positions into liquidity pools. In short, unbacked token supply keeps growing, while reserve-backed supply does not.

Another important point: Newly minted tokens have no fixed issuance rate. When users add ETH liquidity to the pool, the protocol calculates how much liquidity is needed for the corresponding position and mints the required amount of YES to match it. This leads to a common misconception—that YES is perpetually inflating. But that’s not entirely accurate. During liquidity rebalancing, there are built-in token burn mechanisms. If YES or other Baseline tokens become excessive, they are directly burned—offsetting any newly minted supply.

How Should We Calculate YES’s Market Cap?

Now that we understand the mechanics of token minting and burning, we can calculate YES’s true market cap. Current data from the Blast explorer shows a total supply of 69.23 million YES tokens. However, 55.05 million of these are still deployed as liquidity within the Discovery range, and the market price has only just entered this zone. Thus, the actual floating supply stands at around 14.18 million YES. At the current price of $5.71, YES’s real market cap should be approximately $80.96 million.

Could Baseline Enter a Death Spiral?

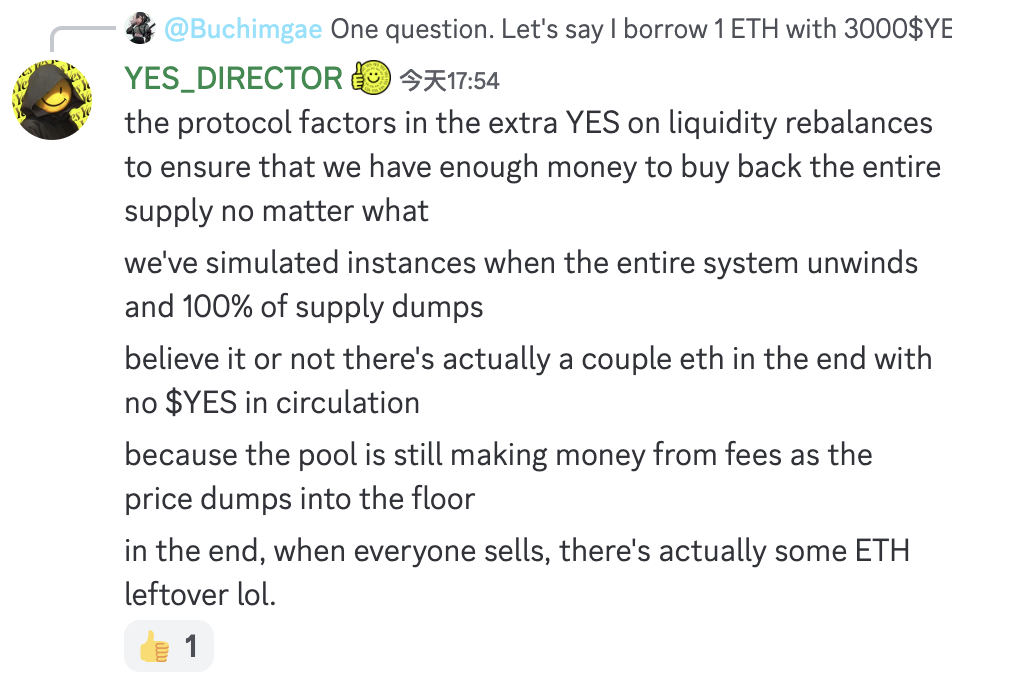

If everyone dumps YES simultaneously—like a bank run—would the liquidity within the Floor range truly be sufficient? The Baseline team claims to have simulated such scenarios and confirmed that even if all YES tokens were dumped, several ETH would remain in the Floor, meaning the protocol holds enough reserves to repurchase all circulating tokens.

Adam Cochran of Cinneamhain Ventures stated he has read through all the code—there may still be issues, but the existence of the Floor price range alone makes it superior to most other projects.

Of course, under Baseline’s BLV mechanism, can the Floor price of tokens like YES truly never fall? Can it avoid a death spiral? Could the tragedy that befell Jimbos Protocol happen again? Honestly, I don’t fully grasp the code—my IQ clearly can’t keep up. Participation would ultimately come down to trusting the team. But in the end, only the market can decide. After all, Ponzis often feel great—right up until they collapse.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News