"Unearthing" the Future: Canaan Creative's Mining Business Differentiation and Financial Analysis Report

TechFlow Selected TechFlow Selected

"Unearthing" the Future: Canaan Creative's Mining Business Differentiation and Financial Analysis Report

This report provides a comprehensive analysis of Canaan Technology's financial status since its expansion into mining operations in 2021.

Author: TaxDAO

Canaan Inc., founded in 2013 and listed on November 21, 2019, is a technology company specializing in high-performance ASIC computing chip design, chip development, computing equipment manufacturing, and software services. Guided by the vision "Supercomputing is what we do; enriching society is why we do it," Canaan has accumulated extensive experience in ASIC chip design and streamlined production. In 2013, under the leadership of founder and CEO Zhang Nangeng, Canaan’s founding team delivered the world’s first batch of Bitcoin mining machines based on ASIC technology to customers, branded as Avalon. In 2019, Canaan completed its initial public offering on the Nasdaq Global Market. Beyond providing comprehensive artificial intelligence (AI) solutions globally—including AI chips, algorithm development and optimization, hardware modules, end products, and software services—Canaan also delivers supercomputing solutions through its proprietary high-performance ASICs (Application-Specific Integrated Circuits). As of 2022, Canaan employed 541 people and operated across markets including Indonesia, Malaysia, the United States, Australia, and Kazakhstan, with core businesses in Bitcoin mining machines, mining operations, and AI products.

This report provides a comprehensive analysis of Canaan's financial status since its expansion into mining operations in 2021, aiming to assess the impact of this business decision on the company’s financial health. By reviewing financial data from the inception of its mining activities and comparing recent quarterly performance, this report examines Canaan’s profitability and cost control within the mining sector, and explores how mining operations affect the company’s overall financial stability and strategic direction. This analysis not only reflects Canaan’s competitive position in the mining hardware market but also considers industry trends, shifts in market demand, and the influence of relevant policy environments on its business expansion decisions.

2 Strategic Analysis of Canaan’s Mining Business Expansion

2.1 Canaan’s Mining Activity Revenue Report

2.1.1 Mining Activity Revenue

According to Canaan’s Q2 2023 earnings report, mining revenue for the second quarter of 2023 reached $15.9 million, representing a 43.3% increase from $11.1 million in Q1 2023 and a 105.1% year-on-year rise from $7.8 million in the same period of 2022. The sequential growth was primarily driven by the rebound in Bitcoin prices and an increase in Bitcoin rewards on the network during the quarter. The year-on-year increase was mainly due to enhanced computing power deployed for mining activities.

According to Canaan’s Q3 2023 earnings report, mining revenue for the third quarter of 2023 was $3.3 million, down 79.5% from $15.9 million in Q2 2023 and 64.6% lower than $9.2 million in the same period of 2022. This decline both sequentially and year-on-year was primarily due to reduced mining computing power. A decrease in Bitcoin hashrate leads to longer transaction confirmation times and lower mining costs. The drop in hashrate stemmed from the enforcement in July 2023 of Kazakhstan’s “Rules on Licensing Digital Mining Activities,” which require individuals engaged in cryptocurrency mining to obtain professional licenses. Consequently, the company decided to temporarily suspend approximately 2.0 Exahash/s of mining capacity in Kazakhstan to ensure regulatory compliance. Since early July, Canaan has been actively working to secure Class II licenses for its mining hardware owners, and its mining operations in Kazakhstan remained suspended throughout Q3 2023.

2.1.2 Sales Activity Revenue

According to Canaan’s Q2 2023 earnings report, product revenue for the second quarter of 2023 was $57.9 million, with mining machine sales increasing from $43.7 million in Q1 to $57.8 million. In comparison, product revenue was $44.1 million in Q1 2023 and $238.1 million in the same period of 2022. The sequential increase was primarily driven by higher total computing power sold, despite weaker overall purchasing power in the market leading to lower average selling prices. The year-on-year decrease was mainly due to lower selling prices caused by the decline in Bitcoin prices. AI product revenue in Q2 2023 was $1 million, compared to $4 million in Q1 2023 and $2 million in the same period of 2022.

According to Canaan’s Q3 2023 earnings report, product revenue for the third quarter of 2023 was $29.9 million, with mining machine sales amounting to $29.755 million. In contrast, product revenue was $57.9 million in Q2 2023 and $136.3 million in the same period of 2022. The sequential decline was primarily due to reduced total computing power sold and lower selling prices, reflecting an overall slowdown in market demand. The year-on-year decrease was mainly due to lower selling prices, even though Bitcoin prices gradually recovered and total computing power sold increased, market demand remained sluggish. AI product revenue in Q3 2023 was $2 million, compared to $1 million in Q2 2023 and $4 million in the same period of 2022.

2.1.3 Proportion of Mining Revenue

-

Canaan’s total revenue in Q2 2023 was $73.85 million, with mining revenue accounting for approximately 21.5%;

-

Canaan’s total revenue in Q3 2023 was $33.32 million, with mining revenue accounting for approximately 9.8%.

Currently, Canaan’s mining revenue constitutes a relatively small portion of total income. Regulatory compliance requirements have led to a reduction in hashrate, resulting in higher mining costs and lower mining revenue. However, the company will continue implementing a de-stocking strategy over the medium term to reduce risks and improve operational efficiency. The balance between mining operations and mining machine sales will require further adjustments based on future market conditions and corporate strategy.

2.2 Mining Costs and Profits in Q2–Q3 2023

2.2.1 Direct Costs of Mining Activities

Canaan’s mining costs in Q2 2023 were $30.6 million, up from $27.3 million in Q1 2023 and $11.5 million in the same period of 2022. These costs include direct production expenses such as electricity and hosting fees, as well as depreciation and amortization. Depreciation of deployed mining machines in the quarter amounted to $16.2 million, compared to $16.3 million in Q1 2023 and $10.1 million in the same period of 2022. The year-on-year increase was primarily due to expanded mining capacity. Therefore, direct mining costs in Q2 2023 were $14.4 million, accounting for 47.1% of total mining costs.

Canaan’s mining costs in Q3 2023 were $18.7 million, down from $30.6 million in Q2 2023 and $15.8 million in the same period of 2022. These costs include direct production expenses like electricity and hosting fees, as well as depreciation. Depreciation of deployed mining machines in the quarter was $15.8 million, compared to $16.2 million in Q2 2023 and $7.7 million in the same period of 2022. The year-on-year increase was due to expanded computing power deployment in the company’s mining operations. Thus, direct mining costs in Q3 2023 were $2.9 million, accounting for 15.5% of total mining costs—a significantly reduced proportion.

Canaan’s product costs in Q3 2023 were $83.7 million, down from $113.3 million in Q2 2023 and $97.1 million in the same period of 2022. The sequential and year-on-year declines align with reduced computing power sold. Accrued inventory write-downs, prepayment write-downs, and provisions for inventory purchase commitments in the quarter totaled $53.9 million, up from $45.9 million in Q2 2023 and $33.1 million in the same period of 2022. Product costs include direct and indirect production costs for mining machines and AI products, as well as inventory write-downs, prepayment write-downs, and provisions for purchase commitments.

Based on the above data related to mining and mining machine sales, the gross margin for mining operations was -0.92% in Q2 2023 and -68.47% in Q3 2023. At present, Canaan’s mining operations are not generating significant profits for the company.

2.2.2 Profit Analysis

Net loss in Q2 2023 was $110.7 million, compared to a net profit of $6.3 million in the same period of 2022. Net loss in Q3 narrowed to $80.1 million, which includes $53.9 million in inventory write-downs, prepayment write-downs, and provisions for inventory purchase commitments accrued in the quarter. These actions align with the company’s proactive de-stocking strategy to navigate a challenging market environment and should be considered non-cash items. To improve its financial condition, Canaan has implemented strict cost controls, including workforce reductions to enhance operational efficiency. For the foreseeable future, Canaan will remain committed to maintaining cash reserves through diversified sales efforts and prudent expense management, ensuring operational continuity and positioning itself to seize future opportunities.

2.3 Impact of Mining Expansion on Canaan’s Asset-Liability Ratio

2.3.1 Current Number and Value of Canaan’s Mining Machines

In Q2 2023, Canaan’s inventory stood at $272 million, with fixed assets including software equipment totaling $50.48 million and right-of-use assets at $289,600. In Q3 2023, inventory decreased to $217 million, fixed assets including software equipment dropped to $34.002 million, and right-of-use assets were $230,000. This indicates that Canaan continues to focus on the more profitable mining machine sales segment. Based on a median selling price of approximately RMB 14,000 (about $1,946), the number of mining machines (for both sale and self-mining) remains stable at around 140,000 units.

2.3.2 Impact of Previous Mining Expansion

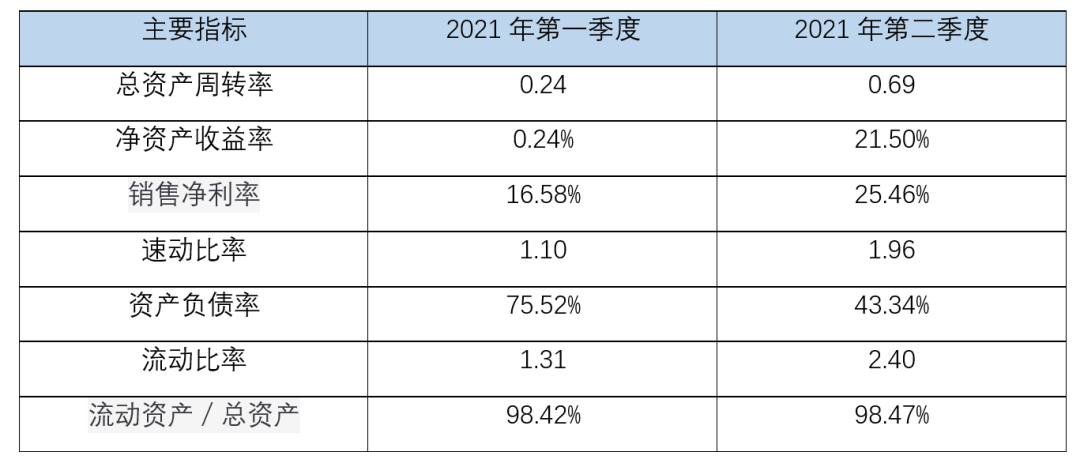

Canaan had previously operated mining activities, but beginning in Q2 2021, it expanded globally, evolving customer relationships from simple mining machine sales to joint mining partnerships, thereby strengthening mutual interests. Simultaneously, mining was established as a separate line item in financial statements. Therefore, key metrics from Q1 and Q2 2021 are compared below to analyze the impact of mining activities on Canaan’s asset ratios, presented in the following table for clear visualization of financial performance differences before and after the launch of this business.

The data show that after expanding its mining operations, Canaan saw significant improvements in financial indicators such as total asset turnover and return on equity (ROE), indicating strong financial performance as a company extending downstream along the traditional upstream industrial chain. Increased current and quick ratios, along with a reduced debt-to-asset ratio, reflect improved financial health. Meanwhile, the rising ROE demonstrates enhanced profitability and efficient capital utilization. Specific analyses are as follows:

(1) Increased current and quick ratios: The current ratio measures the proportion of current assets to current liabilities, while the quick ratio excludes inventory, a less liquid asset. Higher values indicate stronger ability to meet short-term obligations and handle unexpected liabilities. The introduction of mining operations likely boosted cash inflows and reduced capital tied up in inventory, improving these ratios.

(2) Reduced debt-to-asset ratio: This ratio reflects the proportion of liabilities to total assets. A declining ratio suggests healthier asset-liability structure, possibly due to mining-generated funds used to pay down debt or invest in higher-return projects, or improved asset management reducing liabilities.

(3) Increased return on equity (ROE): ROE measures net profit relative to shareholders’ equity. A higher ROE indicates greater profit per unit of equity, potentially driven by additional mining revenue, optimized cost management, or more efficient capital use, all enhancing profitability.

In summary, improvements in these financial metrics suggest that Canaan’s introduction of mining operations has enhanced its financial health, optimized its balance sheet, strengthened profitability, and better met investor expectations.

Historically, mining machine business performance closely tracks cryptocurrency prices—high prices lead to strong results, low prices to weak ones. In 2021, Bitcoin prices fluctuated widely, dipping near $30,000 and peaking above $60,000. Despite numerous challenges, Canaan’s performance rose consecutively for four quarters, ending the year with over a tenfold year-on-year increase—far outpacing Bitcoin’s price movement. This demonstrates the effectiveness of Canaan’s innovative and flexible business strategy, stable supply chain capacity, mining expansion, growing R&D investment, team development, and increasingly refined management practices at the time.

In Q4 2021, despite significant volatility in crypto prices, Canaan further expanded into overseas markets such as Southeast Asia and South America, establishing partnerships with customers in emerging markets including Malaysia, the UAE, Argentina, and Peru. New customers accounted for 41% of purchased computing power. Meanwhile, demand remained strong in traditional overseas markets such as Central Asia, North America, and Europe, where repeat customers contributed 59% of computing power purchases. Strong market demand enabled the company to sell 7.74 million terahashes of computing power in Q4, a 15% increase from Q3, setting another record for best single-quarter sales in company history.

2.4 Impact of Mining Expansion on Canaan’s Inventory

In Q1 2021, Canaan’s inventory was $376 million, rising to $587 million in Q2 2021—a year-on-year increase of 56.12%. The following table visually illustrates the impact of this business decision on inventory ratios.

After implementing this business decision, shortened operating cycles and increased inventory turnover reflect several developments: First, the addition of mining operations may have brought new revenue streams, increasing total income. Second, because mining typically converts faster into cash or other liquid assets, the company’s cash flow improved, shortening the operating cycle. Additionally, higher inventory turnover means the company can convert inventory into sales more quickly, reducing inventory overhang and improving capital efficiency.

Overall, these metric improvements indicate enhanced operational efficiency, stronger profitability, and better responsiveness to market demand.

In summary, building upon its core business of mining machine production and sales, Canaan has extended downstream into self-operated mining to raise competitive barriers, diversify revenue sources, and gradually reduce reliance on a single business model. Although mining operations have grown rapidly, they still represent a small share of total revenue. According to company plans, a certain percentage of monthly production capacity will be allocated to self-mining, with specific volumes flexibly adjusted based on partner mining farms and market demand. These farms are primarily located overseas, such as in Kazakhstan, where ongoing regulatory adjustments may increase Canaan’s mining costs.

While self-operated mining may superficially reduce risk, its high correlation with the core business and exposure to significant regulatory risks could amplify overall risk. If mining becomes a major asset investment, adverse market conditions or tightening regulations could severely challenge Canaan’s revenue and cash flow. Although mining provides an additional revenue stream, its associated risks must be carefully managed to ensure stable operations across varying market environments.

3 Overall Conclusion

Since expanding its mining operations in 2021, Canaan’s strategic decisions and financial performance reflect its efforts to achieve growth and competitive advantage in the global mining hardware market. Through vertical integration across upstream and downstream产业链 segments, Canaan has not only strengthened its control within the Bitcoin ecosystem but also diversified some market risks, further solidifying its market position. However, because both mining machine sales and mining operations are highly dependent on Bitcoin’s cyclical and volatile nature, the risk diversification effect of this strategy is limited.

Although mining operations reported negative gross margins in Q2 and Q3 2023, short-term financial challenges do not fully negate the long-term value of this strategic move. Considering Bitcoin’s potential as a long-term investment asset, Canaan’s held Bitcoin may appreciate in value in the future, offsetting short-term operational losses. Therefore, mining operations serve not only as an immediate revenue source but also lay the groundwork for long-term asset appreciation. Hence, despite current negative margins, Canaan’s mining expansion remains strategic and forward-looking, offering potential for sustained growth and profit maximization amid the evolving digital currency landscape.

In conclusion, Canaan’s mining expansion strategy represents a comprehensive decision informed by market trends, technological strengths, and long-term investment value. By continuously optimizing its business model, strengthening cost control and risk management, and adapting flexibly to market changes, Canaan is well-positioned to turn challenges into opportunities and achieve long-term success and growth in both mining hardware and mining operations.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News