21 Applicants for Hong Kong Licensed Exchange: Who Will Make It First?

TechFlow Selected TechFlow Selected

21 Applicants for Hong Kong Licensed Exchange: Who Will Make It First?

Behind the "withdrawal" of the virtual asset trading platform license application lies a race to seize the timing opportunity.

Author: Bowen, Bailu Salon

On February 23, 2024, another license application was withdrawn from a licensed exchange in Hong Kong.

After years of navigating compliance challenges, the long-established exchange Huobi finally found an ideal opportunity with Hong Kong's aggressive push into Web3 in 2023. Achieving full compliance and establishing operations in Hong Kong would allow Huobi to successfully come ashore—both an opportunity to reshape its image and revive its business growth.

However, even a minor mistake in the application process forces applicants back to square one. With Hong Kong’s virtual asset exchange licensing process being lengthy and involving extensive back-and-forth communication with the Securities and Futures Commission (SFC), delays easily cause applicants to miss critical first-mover opportunities.

On January 29, BitHarbour withdrew its application; on February 7, Meex followed suit; just days later, on February 23, Huobi HK also pulled its application. Within less than a month, the number of withdrawn applications surpassed previous figures, delivering a harsh reality check for all remaining applicants still waiting in line.

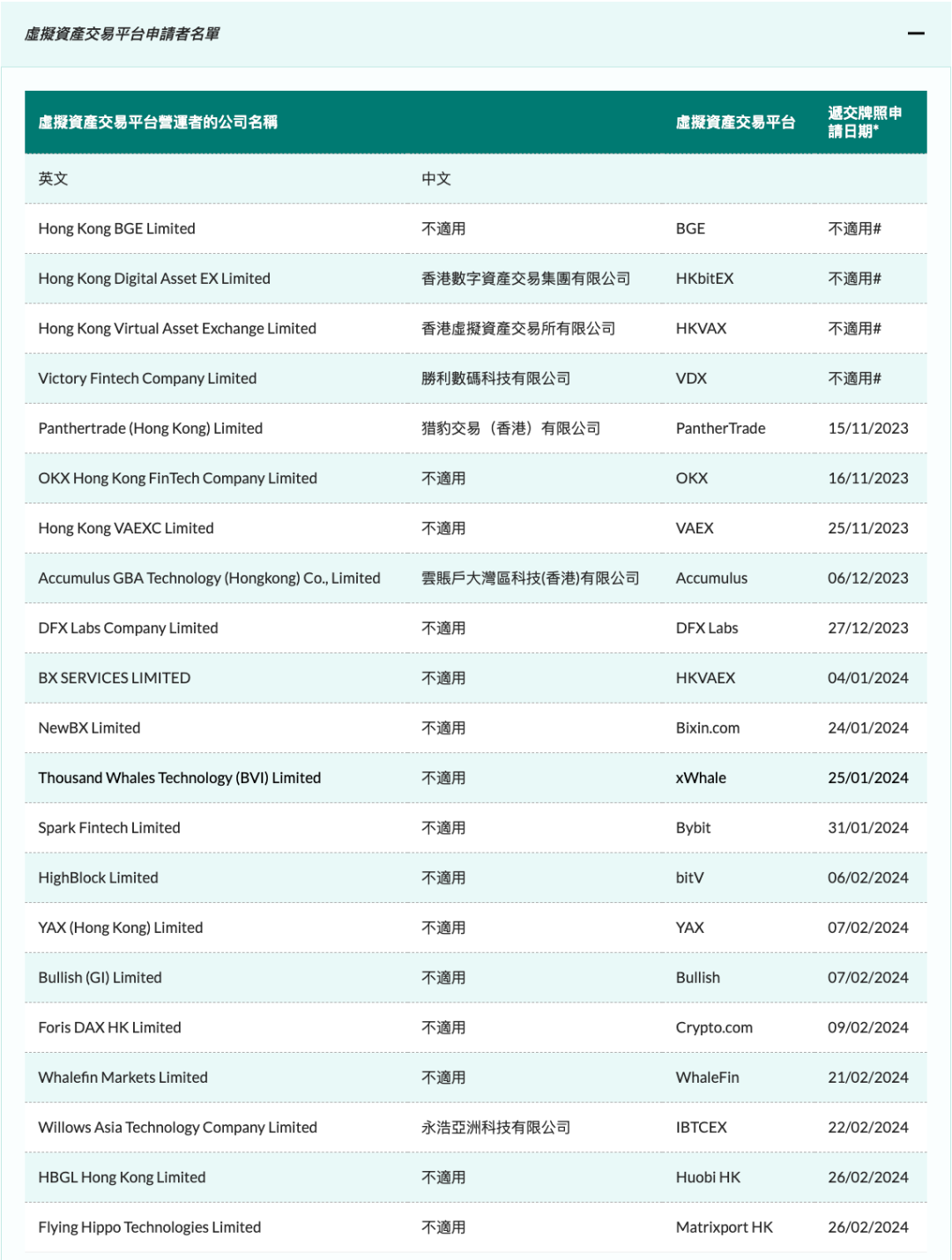

As of February 28, there are still 21 applicants actively undergoing review by the SFC. What makes obtaining a licensed virtual asset exchange in Hong Kong so difficult? And which players will seize the moment and emerge ahead of the pack?

In this article, Bailu Salon explores the operational landscape of licensed virtual asset exchanges in Hong Kong together with our readers.

(1) Three Key Application Requirements: Capital Injection, External Assessments, and Fit-and-Proper Criteria

Throughout 2023, the Hong Kong government made loud proclamations and bold moves, leading market participants and industry professionals alike to believe this could be the cure-all solution to revitalize Hong Kong's financial sector. This wave of enthusiasm created a false impression: that success could be achieved effortlessly.

But reality doesn't favor those who believe “even pigs can fly if they catch the wind.” The 331-page Anti-Money Laundering and Counter-Terrorist Financing (Amendment) Bill 2022, along with the 99-page Guideline for Virtual Asset Trading Platform Operators, establishes an extremely complex regulatory framework for licensed virtual asset trading platforms in Hong Kong. Without thorough preparation across legal, technical, and capital dimensions, no applicant can see this journey through to completion.

Applicants must take seriously three core requirements: capital injection, external assessment mandates, and staffing that meets fit-and-proper criteria.

Capital Injection

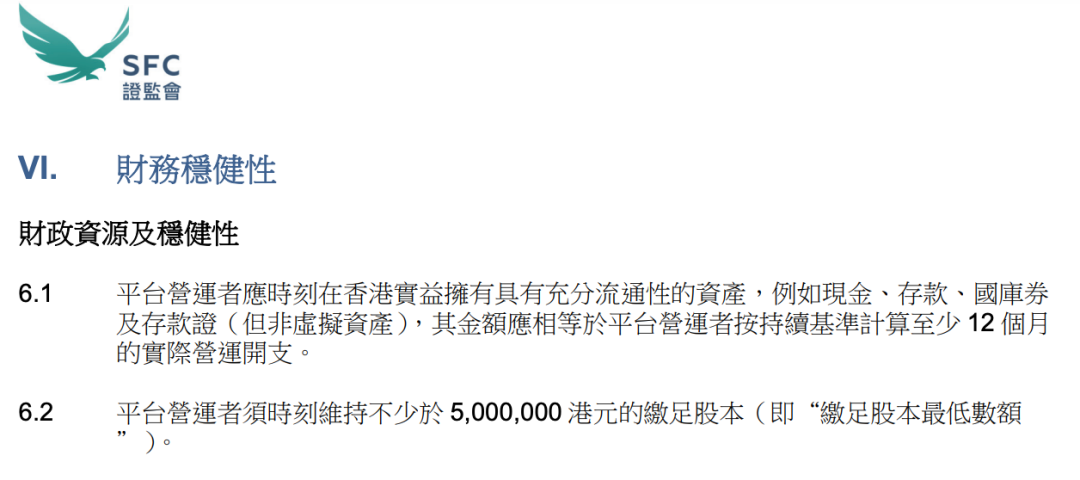

According to the SFC’s Guideline for Virtual Asset Trading Platform Operators, applicants must meet two fundamental capital requirements:

(i) The platform operator must always beneficially own liquid assets in Hong Kong—such as cash, deposits, treasury bills, or certificates of deposit (excluding virtual assets)—equal to at least 12 months of actual operating expenses calculated on a rolling basis.

(ii) The platform operator must maintain a paid-up share capital of no less than HK$5 million at all times.

Pre-application capital preparation is not the hardest hurdle. Anyone daring enough to enter the exchange arena likely already has the financial and logistical readiness required—otherwise, they wouldn’t have considered it in the first place. The real test lies in the ongoing costs of operating an exchange in Hong Kong, which we’ll discuss later.

External Assessment Requirements

Second in importance—and placed here by the author—are various external assessment requirements covering areas such as private key management, investor protection measures, anti-money laundering (AML), surveillance systems, and cybersecurity.

From a solutions standpoint, pathways to meeting these conditions are already well established. Different types of applicants possess different advantages, and leveraging them appropriately enables success. For seasoned major exchanges applying for licenses, robust development capabilities and rich operational experience already exist—the main gap is filling deficiencies in legal and compliance functions. Conversely, traditional financial institutions transitioning into this space typically excel in corporate governance and compliance due to their long-standing presence in Hong Kong’s financial markets but need to reconfigure development teams with sufficient industry expertise and technical strength.

Pure entrepreneurs may face some difficulties. Overall, however, applicants who thoroughly prepare each step upfront can smoothly navigate SFC reviews; should any misstep occur, timely corrections allow restarting the process.

The fit-and-proper criteria, however, present a significant challenge for all applicants.

Fit-and-Proper and Competency Requirements

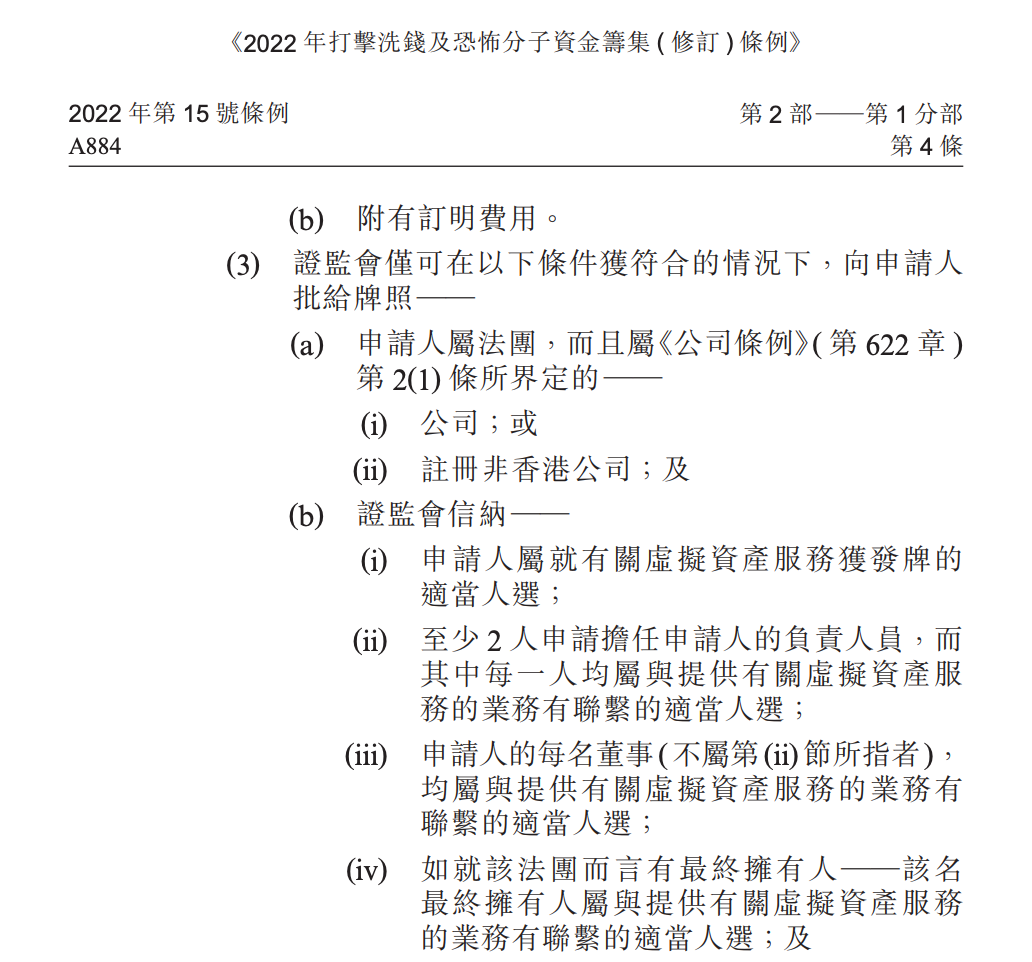

Under the Anti-Money Laundering and Counter-Terrorist Financing (Amendment) Ordinance 2022, the SFC may only approve a license if the applicant satisfies certain conditions. These include:

(i) Being a company incorporated in Hong Kong with a fixed place of business, or incorporated elsewhere but registered in Hong Kong under the Companies Ordinance;

(ii) Passing the SFC’s fit-and-proper test.

Passing the fit-and-proper test is no easy task. Conditions include:

(i) At least two SFC-approved Responsible Officers (ROs) must supervise operations to ensure compliance with AML/CFT regulations and other supervisory requirements; only ROs may serve as executive directors of VASPs.

(ii) The applicant’s ultimate beneficiaries must be individuals capable of providing virtual asset services.

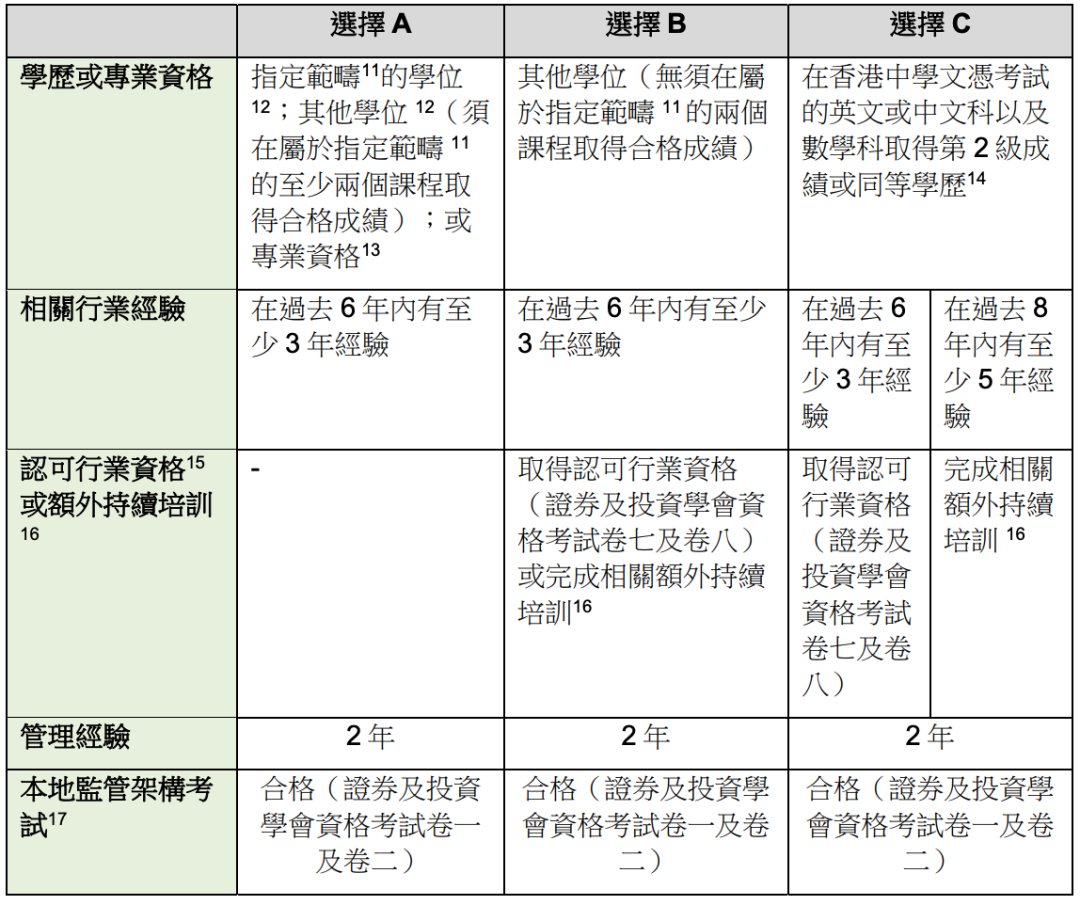

Focusing on individual ROs, each must have both adequate academic qualifications and at least three years of relevant industry experience. Qualified candidates are scarce, driving up the service fees for eligible ROs. Any disagreement during collaboration could derail the entire application process, and the time cost of reconfiguring personnel is even higher.

Beyond executives, all relevant personnel must also meet competency standards and ongoing training requirements. From management to frontline staff, Hong Kong’s strict oversight ensures professional integrity across the board—but simultaneously increases the difficulty and ongoing operational burden for every applicant building a team.

(2) Two Operational Challenges: Burning Cash and Fierce Competition

Even after obtaining a license, the struggle isn’t over. Operating a licensed exchange in Hong Kong faces two major hurdles: “licensed-to-die” and “too many wolves, too little meat.”

The “Licensed-to-Die” Dilemma

The term “licensed-to-die,” coined by Yang Wang, Vice President of the Hong Kong University of Science and Technology, best encapsulates the operational困境 faced by licensed virtual asset exchanges in Hong Kong. The stated HK$5 million registration threshold is just the baseline—real challenges lie in the accumulation of ongoing operational costs.

Legal and compliance teams, investments in security and technology infrastructure, implementation of fund segregation and risk management mechanisms, establishment of audit and reporting systems, employee compliance training, and maintaining local branches in Hong Kong to store recovery phrases and private keys—all incur substantial costs.

Each of these represents a distinct expense category. Beyond these predictable costs, numerous unpredictable ones remain. For example, due to high demand, the two mandatory licensed Responsible Officers (ROs) per institution often charge premium fees. Another case: on January 30, 2024, the SFC mandated that licensed virtual asset exchanges provide insurance covering at least 50% of client assets. On April 12, 2024, public consultation began on the OTC licensing regime, which when implemented will further increase application and maintenance fees. As such provisions multiply, the capital required to maintain compliance will keep rising.

High costs represent one side of the “licensed-to-die” problem. The flip side is limited business scalability—a separate constraint.

First, listing any virtual asset requires prior approval from the SFC, with each exchange submitting individual applications. As a result, the number of tradable tokens on licensed exchanges remains extremely limited, severely hampering user acquisition.

Second, compared to large unregulated global exchanges, Hong Kong-licensed platforms face heavy restrictions on innovation. Without derivatives—the primary revenue driver—and stripped of gambling-like features, compliant exchanges suffer disproportionately during market downturns—far more than today’s leading offshore platforms.

OSL offers a prime example. In 2022, OSL Group reported a loss of HK$300 million; in the first half of 2023, it recorded a net loss of approximately HK$95 million. In June 2021, during the bull market, OSL Group (then BC Technology Group) reached an all-time stock price high. By 2023, its share price had fallen nearly 80%. The virtual asset market remains collectively vulnerable—when winter comes, regulatory burdens and operating costs only deepen the crisis.

Inevitable Industry Saturation

“Licensed-to-die” reflects regulatory stringency. Yet even absent direct pressure from regulators, fierce competition among applicants inevitably shrinks everyone’s room to survive.

To date, including the two already approved licensed exchanges and one granted provisional approval (HKVAX), a total of 26 institutions have submitted applications for virtual asset trading platform licenses in Hong Kong. In just February 2024 alone, six new applicants entered the race.

Hashkey is beginning to show signs of market leadership, aggressively capturing market share. Once more exchanges gain approval, fee wars, marketing battles, insurance competition, and even airdrop giveaways could erupt overnight. In such a crowded field, will stronger players rise based on merit—or will mutual destruction send everyone into a death spiral?

Hong Kong’s licensed exchanges must avoid repeating the bank runs seen at Binance and FTX.

(3) Facing Competition: Only Clear Strategy and Leveraged Strengths Can Secure a Foothold

The Hong Kong government’s intention to raise industry barriers is sound—Web3’s pervasive risks remain the biggest obstacle to sector expansion, leaving no room for inadequate preparation. Under competition, the ultimate winners will be those best suited for the market.

With Hong Kong’s market infrastructure still underdeveloped, institutions of different backgrounds possess varying core competencies. Traditional financial institutions, backed by vast capital pools, should focus on investor education and guidance to channel funds into the market. Meanwhile, mature Web3-native firms should drive innovation and work with regulators to bring diversified products to market. By finding their niches and jointly developing the ecosystem, a healthy, competitive, and thriving market can emerge.

Of course, ecosystem development starts with securing a license. While future outcomes remain uncertain, early movers deserve close attention.

Traditional Finance Background: HKVAX, VDX

HKVAX holds a first-mover advantage. On August 11, 2023, HKVAX received a letter of principle approval from the SFC to conduct Type 1 and Type 7 regulated activities (Virtual Assets 1&7 License), positioning it to become Hong Kong’s third licensed virtual asset trading platform. Its application status is beyond doubt; its head start will significantly accelerate business development.

In January 2024, HKVAX CEO Wu Weiliang attended the "2024 Qingdao·Hong Kong & Macao Financial Night" event, stating: “Domestic ‘exclusive’ blockchains like Wenchang Chain, Wuhan Chain, and Ant Chain differ greatly from international ones like Ethereum. Technologically, Hong Kong is the preferred platform for enterprises venturing into virtual assets—it supports all chains. If we link domestic digital assets via domestic chains (e.g., Ant Chain) to Hong Kong, then convert the underlying layer to Ethereum before selling to overseas companies, we can resolve both technical and legal issues. Hong Kong serves as the bridge connecting domestic businesses to global markets.” This suggests HKVAX has likely identified a strategic niche—bridging domestic operations to overseas markets—and is already collaborating with mainland Chinese enterprises to leverage this advantage.

Turning to VDX, another first-wave applicant, VDX has maintained a clean track record throughout the process. As a subsidiary of Victory Securities, its proven ability to integrate traditional finance into Web3 could become a powerful edge. On November 24, 2023, Victory Securities became the first local Hong Kong brokerage approved to offer retail virtual asset services. Within two months, it achieved an average monthly transaction volume of $10 million, with its virtual asset business turning profitable—demonstrating strong capabilities in investor education and attracting traditional capital. This positions VDX well for future B2B collaborations in Hong Kong.

Reliable sources indicate that VDX’s CEO comes from traditional finance, with over ten years of high-frequency trading experience and seven years in the virtual asset industry; the COO previously worked at Deutsche Bank and Accenture and served as an SFC expert on virtual assets. Multiple team members hail from Tencent, Futu, and Tiger Brokers. While the license outcome remains pending, VDX’s team formation is stabilizing, and capital readiness is supported by its parent company—neither poses a critical barrier. In partnering with traditional financial institutions, VDX stands out as one of the most promising licensed exchanges to watch.

Major Exchange Background: Hashkey, OKX

For the foreseeable future, Hashkey will remain the leader in Hong Kong’s Web3 market. With over 150,000 users, daily trading volume averaging $630 million, support for 18 virtual assets, more than 10 broker-dealer and fund integrated accounts, partnerships with over 20 institutions, and six Hong Kong-listed companies opening accounts—Hashkey’s deep roots in Hong Kong are starting to pay off. The ecosystem needs Hashkey to lead innovation, expand the market, promote stablecoins, and pioneer RWA development.

Most anticipated is the issuance and advancement of a Hong Kong dollar stablecoin. On February 6, 2024, RD Technologies announced a cooperation intent with HashKey Exchange and Allinpay International regarding stablecoin initiatives. The collaboration covers online and offline stablecoin use cases, cryptocurrency trading services, physical merchant acceptance networks, stablecoin R&D technology, and joint research into launching HKDR, a Hong Kong dollar-pegged stablecoin.

The U.S. approval of spot Bitcoin ETFs reflects its intent to extend dollar dominance into the virtual asset realm. The success of a Hong Kong dollar stablecoin is crucial to Hong Kong’s future global standing in the industry.

Another highly watched exchange is OKX, which commands the largest Chinese-speaking user base. Although Bybit, KuCoin, and other major exchanges also have Hong Kong operations, in a city closely tied to mainland China, OKX’s brand reputation and influence within Chinese communities remain its greatest weapon—even allowing it to absorb much of the time cost associated with licensing. Market expectations for major legacy exchanges are largely shared: Will top-tier exchanges pursue compliance merely for legality, or will they drive meaningful innovation? The world awaits answers.

In recent years, OKX has invested heavily in financial products and exchange features—innovations that align perfectly with Hong Kong’s strategy for virtual asset development. Can OKX leverage its influence to achieve regulatory breakthroughs, bringing more products and functionalities into compliance to propel market growth? This isn’t just the market’s hope for OKX—it’s the expectation for all major-exchange-backed applicants.

Conclusion

Ultimately, applying for and operating a licensed exchange in Hong Kong is difficult because of unpredictability.

Evolving regulations, shifting markets, and changing risks—Web3 is fraught with uncertainty. Extreme price volatility, new hacking techniques, or even sudden AI breakthroughs disrupting the entire industry—no one can predict what’s coming.

Precisely for this reason, every step must be taken with care. Maintain rigorous discipline, continuously enhance professional expertise, foster innovation, and seize every critical juncture. Only in this way can one adapt to the ever-evolving landscape of Web3 finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News