Viewpoint: Bullish on the halving, but betting on BTC may no longer be "worth it"

TechFlow Selected TechFlow Selected

Viewpoint: Bullish on the halving, but betting on BTC may no longer be "worth it"

If history repeats itself, then this time Bitcoin's peak gain will be less than 170%, and it has already achieved most of those gains.

By David Canellis

Translated by Mary Liu, Bitpush News

Bitcoin's current rally coincides with the convergence of two bullish narratives: in less than eight weeks, the halving will cut new supply issuance in half, while spot ETFs are already accumulating Bitcoin faster than it is being mined.

Beyond the new demand from spot ETFs, the halving has historically served as a catalyst for significant price increases in Bitcoin.

However, in the past two cycles, the biggest beneficiaries have been cryptocurrencies other than Bitcoin. Looking back at the peak gains one year after each previous halving:

-

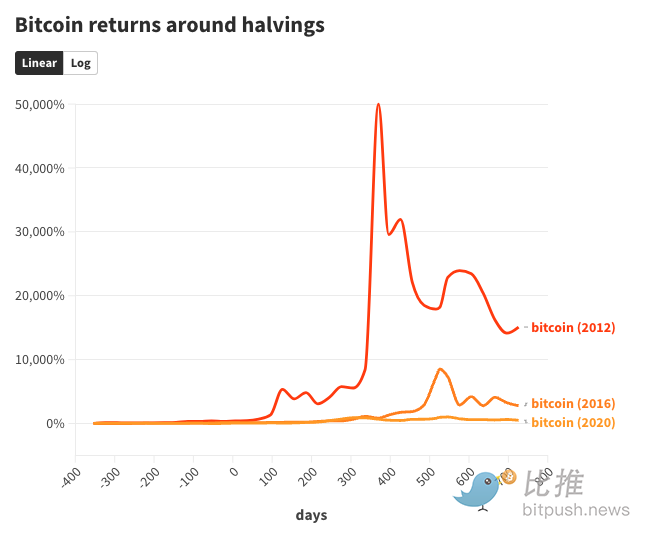

50,000% gain one year after the 2012 halving.

-

8,500% gain within roughly one and a half years following the 2016 halving.

-

1,000% gain one and a half years after the 2020 halving.

For those with a mathematical bent, an interesting observation is that each successive Bitcoin halving cycle’s peak return has been roughly the prior cycle’s figure divided by 6 to 8 (50,000% / 8,500%; 8,500% / 1,000%). If history repeats, this cycle’s peak Bitcoin gain would be under 170%—and currently, much of that gain has already been realized.

This makes sense considering Bitcoin now has a market capitalization exceeding $1 trillion. Its price can no longer increase 500-fold over two years as it did in 2012, when its market cap was under $200 million.

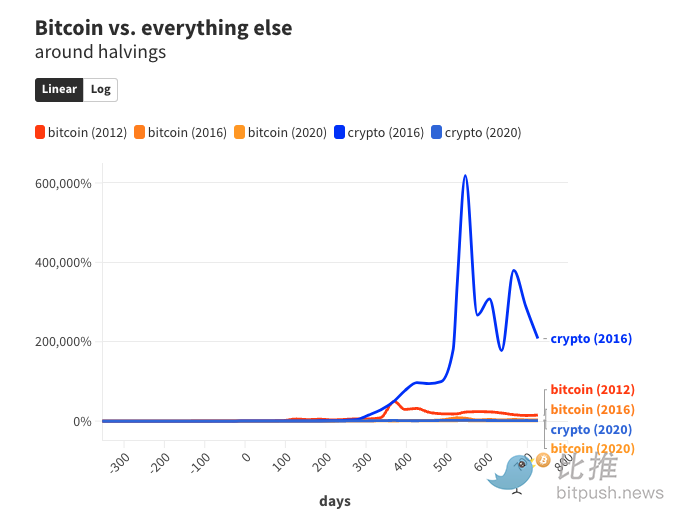

Bitcoin (BTC) currently accounts for about half of the entire cryptocurrency market, but there are tens of thousands of other cryptocurrencies that, collectively, tend to "ride the wave" during Bitcoin’s strongest rallies.

In fact, tokens other than Bitcoin consistently deliver higher returns during Bitcoin bull markets. One year before the 2016 halving, the total value of all non-Bitcoin cryptocurrencies stood at $64.9 million.

One year after the halving, at the peak of the 2017–2018 bull market, this figure had surged over 6,000-fold to $421 billion, driven largely by the rise of XRP, Ethereum, and Bitcoin Cash.

Likewise, in the previous crypto cycle (2019 to 2021), the valuation of cryptocurrencies excluding Bitcoin was $71.6 billion one year before the 2020 halving.

One and a half years later, as Bitcoin neared its all-time high, the combined value of all other cryptos reached $1.7 trillion—representing growth of over 2,000%, outpacing Bitcoin’s own 1,000% rise.

The four-year cycle isn't unique to Bitcoin

It bears repeating: with only three halvings on record, the sample size is too small to draw any meaningful conclusions.

Such a small dataset means factors beyond the halving may also play a role in shaping what appears to be Bitcoin’s regular four-year market cycle.

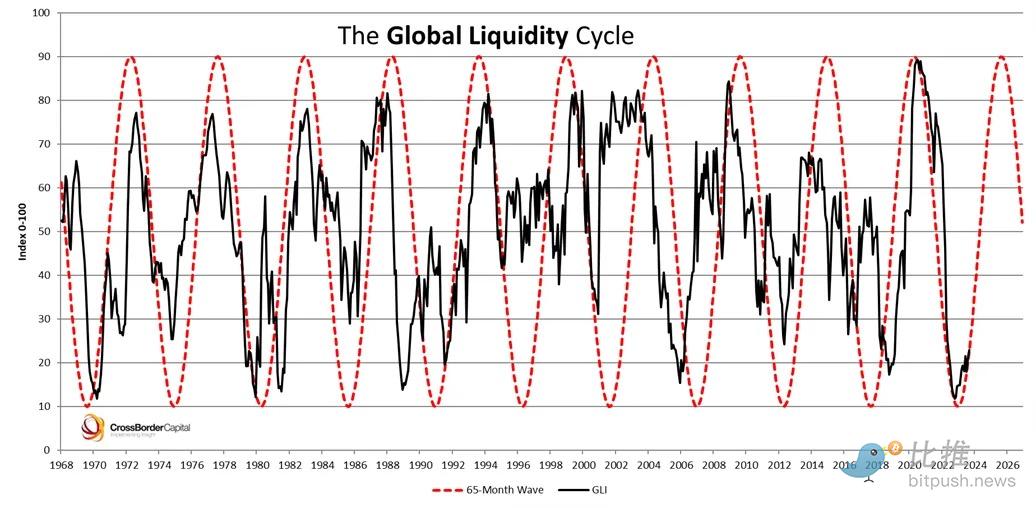

Global liquidity cycles, which track the amount of cash flowing through the global economy, may correlate even more closely with Bitcoin’s rallies than the halving does.

In fact, global liquidity itself operates on a roughly four-year cycle.

Like the halving, proving definitively that global liquidity waves cause explosive Bitcoin growth remains unscientific; it is likely a combination of both effects: as global liquidity expands and supply contracts, capital spills into speculative asset classes like crypto, thereby increasing demand.

Excluding one day of net outflows last week, U.S.-based physically backed Bitcoin funds have purchased nearly 6,350 BTC ($362 million) on average per trading day.

Bitcoin miners mine an average of 147 blocks per day, each rewarded with 6.25 BTC ($356,600), the mechanism by which the network issues new coins.

Thus, miners extract fewer than 920 BTC ($52.5 million) from the blockchain daily. Bitcoin funds led by BlackRock, Fidelity, and Ark/21Shares are purchasing nearly six times that amount on behalf of shareholders.

Many aspects of the Bitcoin market already exceed Bitcoin’s new supply. On average, around 35,000 BTC ($2 billion) flows into cryptocurrency exchanges daily this year, suggesting potential Bitcoin sell-side volume exceeds daily mining output by 37 times.

Even accounting for Bitcoin’s recent price surge, if only a small fraction of the Bitcoin sent to exchanges is ultimately sold, there appears to be sufficient supply to meet demand without prices immediately entering parabolic territory.

Still, with the halving approaching—expected on April 19 or 20—it’s easy to see how it captures the imagination of the entire market. Native crypto firms like Bitwise, Bitfinex, and CoinShares have attempted to demystify it, as have traditional financial institutions such as JPMorgan and Standard Chartered.

On a practical level, the Bitcoin halving will fundamentally reshape the economics of Bitcoin mining. CoinShares estimates that several major operators could face difficulties if Bitcoin fails to remain above $40,000—a threshold so far maintained.

Standard Chartered, known in recent years for bold crypto price forecasts, continues to project a $100,000 Bitcoin target by year-end, partly due to how significantly the halving could tilt supply and demand dynamics in Bitcoin’s favor.

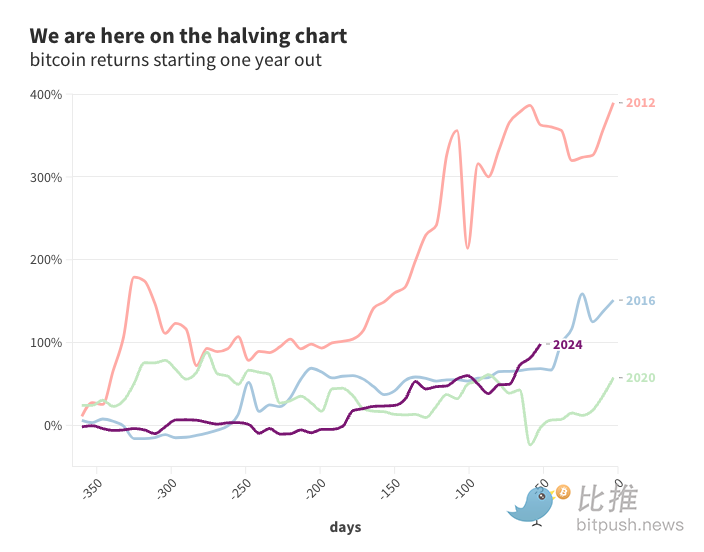

It’s tempting to overlay Bitcoin’s price path following previous halvings—the only three occurred in 2012, 2016, and 2020. After all, Bitcoin’s largest bull runs peaked between one and one and a half years after each halving.

Beyond confirming that “past performance is not indicative of future results,” everyone is speculating on why this time might be different.

Regardless of whether the halving has (or hasn’t) any direct impact on price, historical data suggests that while massive capital injections occur every four years, Bitcoin’s cyclical patterns are weakening over time.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News