Venture Capital and Free Lunch

TechFlow Selected TechFlow Selected

Venture Capital and Free Lunch

Venture capital is the cradle of innovation and the engine of world-changing breakthroughs.

Written by: Packy McCormick

Translated by: Block unicorn

Venture capital gets a bad rap, but let me tell you—venture capital is great. In fact, it's the best asset class. I can feel other asset classes protesting, and sure, some have their advantages:

-

Public equities are the largest

-

U.S. Treasuries are the safest

-

Only real estate can be your home

-

Private equity is an asset class

But no asset class is more beautiful than venture capital—it’s a free lunch machine. I admit, venture capital isn’t perfect. It’s risky, illiquid, and highly volatile. The best venture funds perform spectacularly; the worst are abysmal.

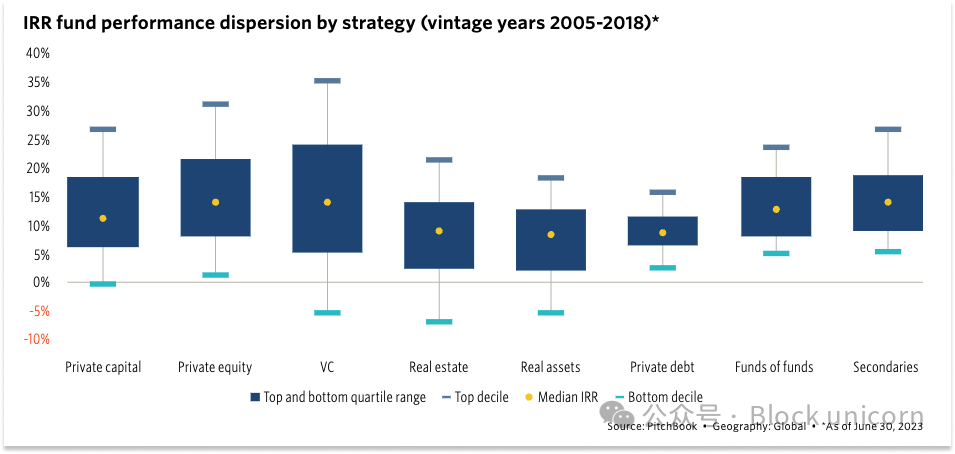

Pitchbook Q2 2023 Global Fund Performance Report

Even the best venture capitalists are wrong far more often than they’re right. Peter Lynch (a board member of Fidelity) once said about public market investing: “In this business, if you're good, you're right six times out of ten. In venture capital, if you're good, you're right three times out of ten, or two times, or maybe even once—but when you're right, you're really right.”

That’s where the beauty lies.

No other asset class has a higher failure rate among its components, yet venture capital delivers returns that match or exceed all others.

Imagine the dumbest investments made by your least favorite venture capitalist. FTX, WeWork, Quibi, Juicero, Theranos—you pick your poison. Feel free to include them all. Add in some Clubhouse, the 9,000th dating app, the 78,000th social network, the 19th-best foundational model company, and the 10,000th PFP NFT project.

All those roaring zeroes are baked into these returns:

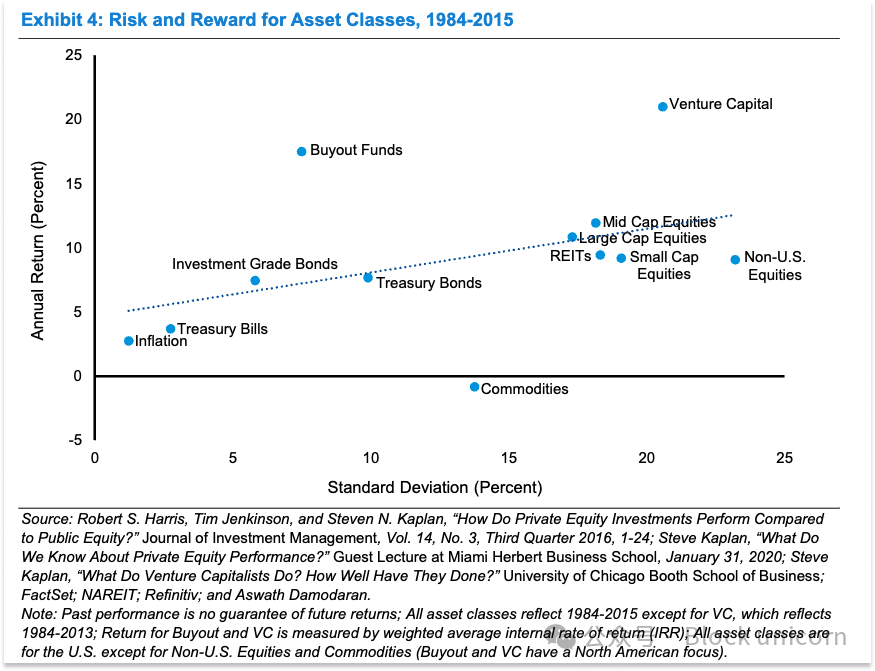

Michael Mauboussin, "From Public to Private Equity in the U.S.: A Long-Term Perspective"

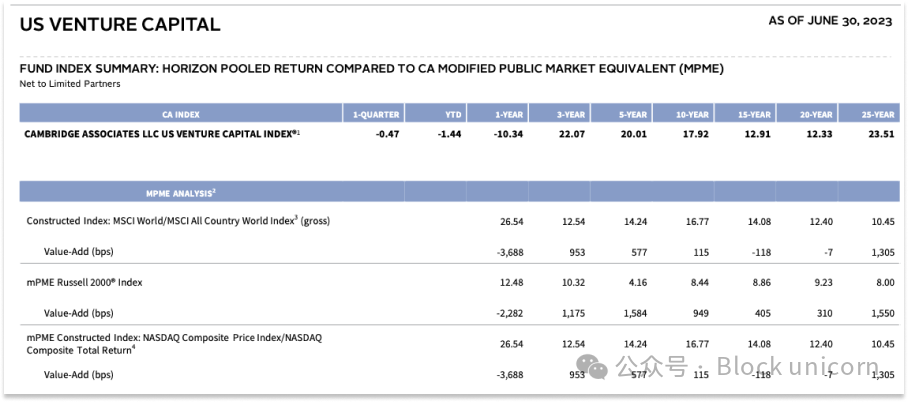

Cambridge Associates, U.S. Venture Capital, as of June 30, 2023

The data isn't perfectly clear—depending on time horizon and whether risk-adjusted returns are considered, venture capital may or may not be the top-performing asset class. And investing in venture capital locks up money for a decade, unlike stocks or bonds which can be sold immediately.

Yet the mere fact that venture capital appears on this list—and wins over certain time horizons—means the world gets access to all this innovation, losers and winners alike, essentially for free.

Outside of venture capital, there are no free lunches—except perhaps, venture capital itself.

The Free Lunch

This doesn’t mean VCs are smarter than everyone else—as I’ve noted, they’re frequently wrong. It means that because of the power law, venture capital is the investment approach best suited to embracing change.

Would returns be better if VCs only funded good companies and skipped the bad ones? Maybe in the short term, perhaps not in the long run—but it’s a moot point, because nobody knows in advance which companies will be great. That’s what makes venture capital beautiful: it embraces uncertainty.

VCs can fund the wildest ideas in the world, most of which won’t work—but a few will succeed spectacularly, and as a whole, the portfolio generates strong returns.

And we get to enjoy the fruits of innovation—venture capital is the only investor willing to back brand-new, unproven innovations.

Take today’s AI boom: VCs are pouring billions into foundational model companies, much of which will be wasted. The problem? It’s hard to know which billions are wasted until after the money is spent and results observed. That’s how venture capital is designed—to place bets and see what unfolds.

If history is any guide, most AI startups will go to zero, while a handful generate enough returns to justify the entire portfolio. Those returns flow back to limited partners (LPs)—charities, foundations, pensions, individuals, and institutions—who then reinvest part into the next generation of VC funds and use the rest to sustain their missions.

Back in 2007, before becoming a VC himself, Marc Andreessen wrote that great VCs improve society in two ways: first, by helping new companies bring transformative technologies and therapies to the world; second, by helping universities and foundations fulfill their educational and humanitarian missions.

In return, the world might just get artificial general intelligence (AGI). We shouldn’t expect charity from VCs—we should expect self-interest.

The Visible Invisible Hand

In venture capital, the invisible hand is more visible than in any other asset class. VC is an ecosystem where participants act in their own self-interest, yet somehow function with collective wisdom over longer time horizons.

If you zoom in on any participant at any given moment, their behavior might seem foolish—and often, it is. Yet the system works well not despite the stupidity, but partly because of it. (Remember that—it helps.)

VCs are willing to fund companies building new technology, even without a viable business model. The best VCs try to back teams combining cutting-edge tech with solid business models—but sometimes the tech is simply too early, economically nonsensical. No matter! There are still VCs willing to fund them.

Maybe they believe the team is smart enough to figure out a model. Maybe they hope the tech gets acquired. Maybe they bet the market will catch up while the company survives. Or maybe they’re just excited, swept up in the hype.

We mock VCs for jumping so quickly on trends. My feed is full of memes about VCs pivoting overnight from Web3 investors to AI investors to Gundo investors.

I think being drawn to hype is one of VCs’ most endearing qualities.

Hype usually means something real is brewing, even if realization is years away. As I wrote in *Liberated Capital*: “Any technology valuable enough in its ideal state will eventually reach that state.” But getting there often requires years—even decades—of grueling experimentation and hundreds of millions, even billions, of dollars to reach a point where the technology can be profitably built and sold.

Who funds those early experiments? Banks? Public markets? No—venture capitalists.

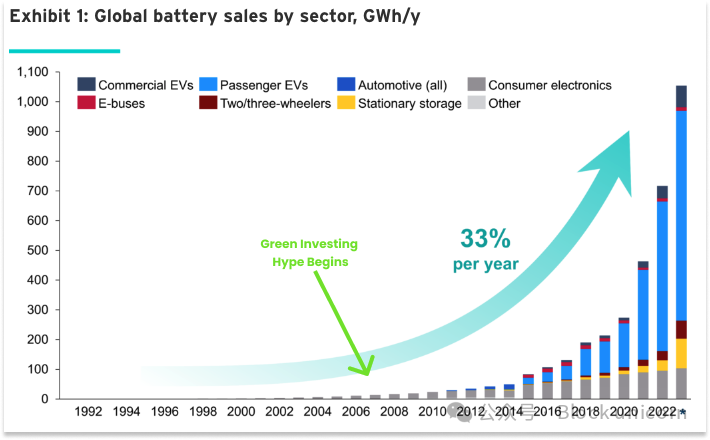

Consider the mid-2000s cleantech bubble led by Kleiner Perkins. In 2007, partner John Doerr declared: “Green is bigger than the internet. It may be the greatest economic opportunity of the 21st century.”

Kleiner and other VCs poured billions into cleantech—and lost most of it. But their investments attracted talent and incentivized improvements in clean tech, laying the foundation for today’s explosion in renewable energy and storage capacity nearly 20 years later. Tesla alone is now worth $626 billion—many times the total capital ever invested in cleantech.

Beyond government-funded basic research, VCs are typically the ones funding technologies that leap too early from lab to market. They provide capital during the flat part of the curve, when losses are common. Then, when the curve turns exponential, the next wave of VCs steps in to capture the upside.

This is what I mean by collective wisdom emerging over time. If no one had absorbed losses decades ago, there would be no returns today. No VC does this out of altruism—they’re driven by the tiny, contrarian chance that an early-stage idea could become the next big thing—but in their mistakes, they create opportunities for others.

“But isn’t losing money a game for VCs since it’s not their own?”

What about pensioners?

Whenever a specific investment fails, someone inevitably cries for poor pensioners, charities, and foundations—the real backers behind the scenes (since many VC funds are backed by sovereign wealth or pension funds).

Let me tell you—those pensioners are doing just fine, thank you very much.

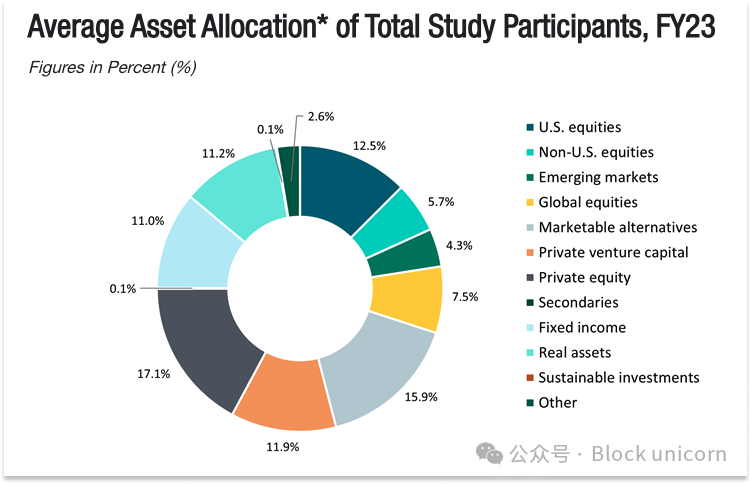

Limited partners (LPs) typically manage large pools of capital diversified across asset classes. Take Yale’s endowment—around $42 billion.

NACUBO (National Association of College and University Business Officers) surveys endowment allocations annually. In 2007, as Marc Andreessen noted in *The Truth About VC*, endowments allocated 3.5% to venture capital. By 2023, that number had risen to 11.9%.

NACUBO 2023 U.S. Higher Education Endowment Report

LPs build diversified portfolios across asset classes, then further diversify within each class. In venture capital, they invest across multiple funds—some early-stage, some late-stage; some generalist, some vertical-focused. They commit capital annually, meaning every year they either launch new funds or re-up existing ones, which then spread investments across dozens of companies over many years.

From an LP’s perspective, venture capital is a small but growing portion of a high-risk, high-return portfolio. Any single investment failing—even spectacularly—is unlikely to materially impact overall performance. What matters more to LPs is that the venture ecosystem continues taking risks capable of generating outsized returns.

If a VC firm makes too many premature bets and loses heavily, it may collapse—but LPs remain, waiting for those early technologies to mature.

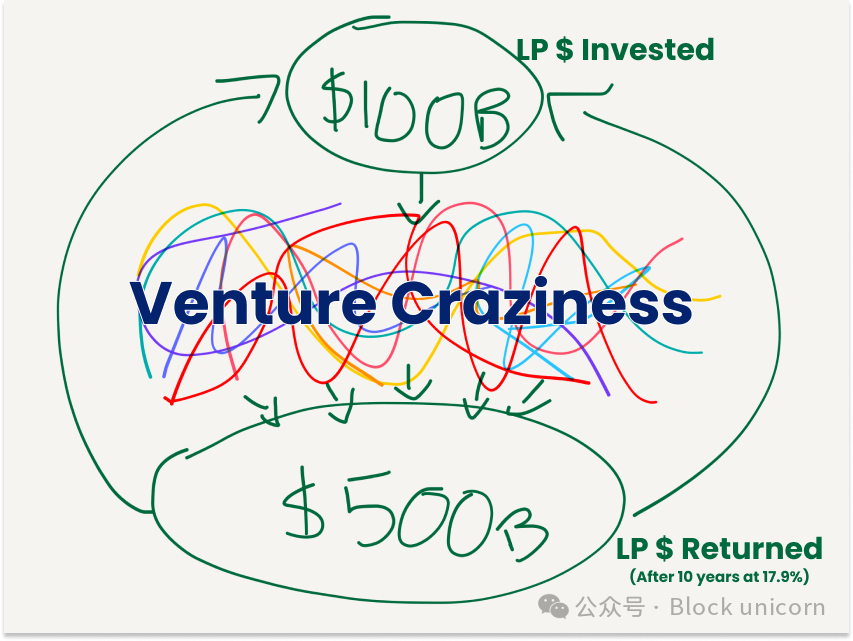

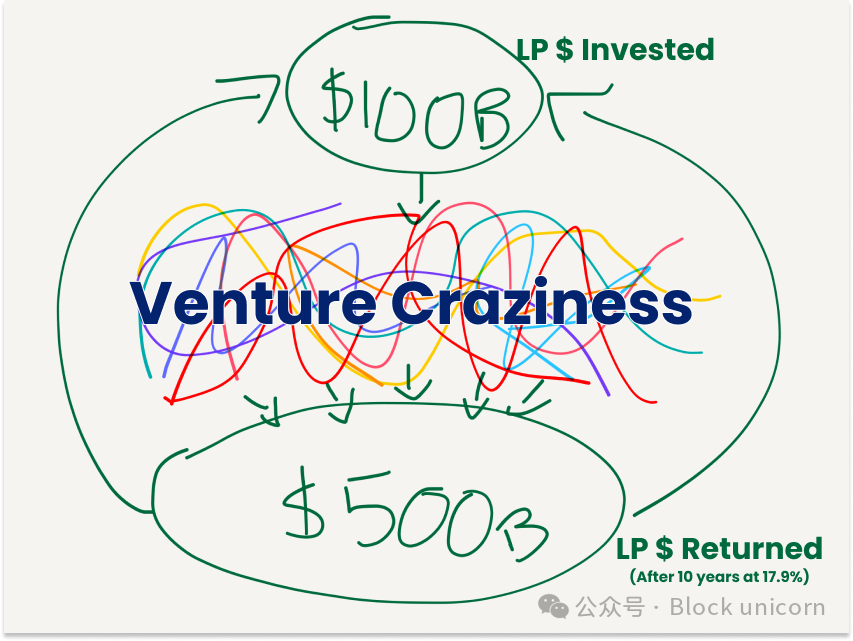

With their long-term view, LPs can invest through the chaos—successes and failures alike—and expect, roughly a decade later, to earn multiples on their capital. Then they reinvest, harvesting seeds planted by yesterday’s losers.

More returns mean more donations to charities, stronger pension payouts, better university funding, and continued investment in venture capital.

The Fund Size Paradox

LPs use these returns to keep backing the funds that made them successful, causing those funds’ assets under management (AUM) to grow over time.

The rise of these mega-funds draws criticism—sometimes even from VCs themselves—who argue large funds are terrible for returns and exist only to generate fees.

VC funds typically follow a “2 and 20” model: 2% management fee and 20% carry. They take 2% annually from fund size to cover salaries and operations for ten years, and keep 20% of profits after returning LPs’ capital.

Critics argue: achieving outsized returns is harder with larger pools. Owning 20% of a company that IPOs at $10B is a 20x return for a $100M fund—but for a $3B fund, it barely breaks even! But they don’t care, critics say, because they still collect 2% annually on a huge number.

So why do LPs keep allocating more capital to these larger funds instead of smaller ones?

Let’s revisit this chart:

Assume a fixed amount of capital flows into venture each year, and a fixed number of breakout companies emerge. If all current capital going to mega-funds were redirected to smaller, early-stage funds, problems arise.

First, those small funds’ extraordinary returns would shrink. Increased competition at the early stage could drive up valuations and reduce the number of deals each fund wins, lowering their odds of owning major companies.

Second, and more importantly, capital available to scale successful companies would decrease. Some companies need hundreds of millions to reach profitability—a reality for pure software firms, and increasingly for capital-intensive foundational model and deep tech companies.

Without mega-funds investing post-Series A, more companies would fail before going public, reducing LPs’ overall returns. This, in turn, would limit small early-stage funds’ ability to take the risks needed for outsized returns and space for wild ideas.

If anything, we need more mega-funds. Recently, I spoke with an LP interested in deep tech in India whose biggest concern wasn’t talent (plentiful) or market (growing), but downstream capital scarcity. If even the most promising companies can’t raise needed funds, why start or back a new company?

Again, the invisible hand reveals itself: self-interested actors dynamically form an ecosystem with robust capital pipelines. Larger funds are rewarded through fees for playing their role, while smaller funds are rewarded through higher upside when they get it right. Neither is better; both are necessary.

Founders win. LPs win. The world wins.

If mega-funds profit handsomely from fees along the way, great! If you think they earn too much relative to value delivered—like Jeff Bezos did—treat their profits as your opportunity: start a larger, lower-fee fund, or something else.

About Management Fees

On the topic of mega-fund management fees, I believe they represent one of the most interesting forms of capital in the world—one we’ll see deployed in increasingly beneficial ways.

The logic is simple: if mega-funds are confident they’ll benefit from the growth of the early tech ecosystem, they can spend fees on things that strengthen that ecosystem. If you believe technology is good (I do), then using management fees to boost tech is like self-sustaining philanthropy.

For example, it’s no surprise that last weekend’s Gundo defense-tech hackathon was co-organized by 8VC and sponsored by many others, including Founders Fund—or that a16z hosted an unofficial St*****d defense-tech club launch party the night before.

These are small examples. At larger scale, a16z recently announced it will “support tech candidates aligned with our vision and values.” It also built a world-class crypto research team based on the belief that “an industrial research lab can bridge academic theory and industry practice.” That team went on to develop and open-source several useful research-based products, including Lasso and Jolt.

I suspect this is just the beginning of a broader trend: VCs using their management fees—which are already netted out in the return figures I shared earlier—to support their industries in increasingly creative ways.

For long-term-oriented firms, there’s economic incentive to support long-horizon, uncertain-benefit initiatives—a rarity outside government and academia, both of which are becoming increasingly rigid and slow. For instance, I wouldn’t be surprised to see more VC-backed basic and applied research labs. Short-term, it’s great marketing (and a way to attract brilliant minds); long-term, it increases the pipeline of investable companies and generates returns (and fees) on ever-larger funds.

In the deal, the world gets accelerated research and knowledge—another free lunch, delicious.

Vive la Venture Capital

Venture capital is in a slump. According to Crunchbase, VCs invested $258B in 2023—the lowest since 2017.

It’s also not especially popular. Sure, VCs promoting pro-Putin views on Twitter doesn’t help, but there are deeper reasons.

VCs make money (and sometimes fame) while others—founders and startup employees—do all the hard work. They frequently tell founders “no, we won’t fund your life’s work,” far more often than they say “yes.” They back bold, risky ventures that occasionally fail spectacularly. They jump from trend to trend, often knowing less about industries than people working in them.

Some VCs are truly bad: poor investors, or worse—revealing predatory behaviors in downturns. They block potentially life-changing acquisitions for founders that make no sense for returns. Sometimes, the most helpful thing a VC can do is write a check and disappear. I’ve worked the other side with bad investors—I know how harmful they can be. The good news? Over time, markets usually punish bad investors.

There are also many truly excellent VCs—but I’m not arguing here that VCs are heroes. At their best, they identify, encourage, and fund entrepreneurs who create real value by building great things.

I’m just saying that as an asset class, venture capital is far better than its reputation suggests. Over the past half-century, no other asset class has been as active, productive, or generous with free lunches.

A founder can walk into a VC’s office with an idea and a dream, and walk out with millions. They hire people, build things that existed only in their imagination. Most fail, but many of those failed founders return to the same offices, raise new capital, and try again. Some succeed—so spectacularly that their success pays for all the failures, and then some. They might even make the world better in the process.

I believe that even if venture capital underperformed other asset classes, or delivered zero returns, having a pool of capital to fund wild experiments would still be a net positive for society. But this is capitalism—the returns are what keep the machine running. So the fact that venture capital delivers such strong returns over long periods is crucial.

The question is: will venture capital continue delivering returns? I believe the answer is unquestionably yes.

Technology will grow larger as its total addressable market expands into massive existing industries previously untouched by tech—industrial, agriculture. As Isaiah Taylor of Valar Atomics puts it, energy, intelligence, and flexibility are getting cheaper, enabling new opportunities to attack old industries with cheaper, better products. Higher margins in large industries will produce extremely valuable companies, and things once impossible are becoming possible at an accelerating pace.

Venture capital was made for such moments—when foundational technologies shift dramatically, giving mad geniuses the chance to build world-changing products.

If the past few decades of pure software investing were a necessary transition period while Bitcoin matured enough to impact the atomic world, the coming decades will be when Bitcoin and atoms combine to make the world magical.

The speed of change, the capital required, and the audacity of founders’ ambitions mean more and larger blowups than ever—but also more and larger winners. Along the way, the world will gain a series of new capabilities—drugs, machines, money, literal moonshots—and get them almost for free.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News