How to legally establish a cryptocurrency fund?

TechFlow Selected TechFlow Selected

How to legally establish a cryptocurrency fund?

A Comprehensive Guide to Establishing a Compliant Cryptocurrency Fund

Authors: Tiger, Attorney Jin Jianzhi

Basic Concepts of Crypto Funds

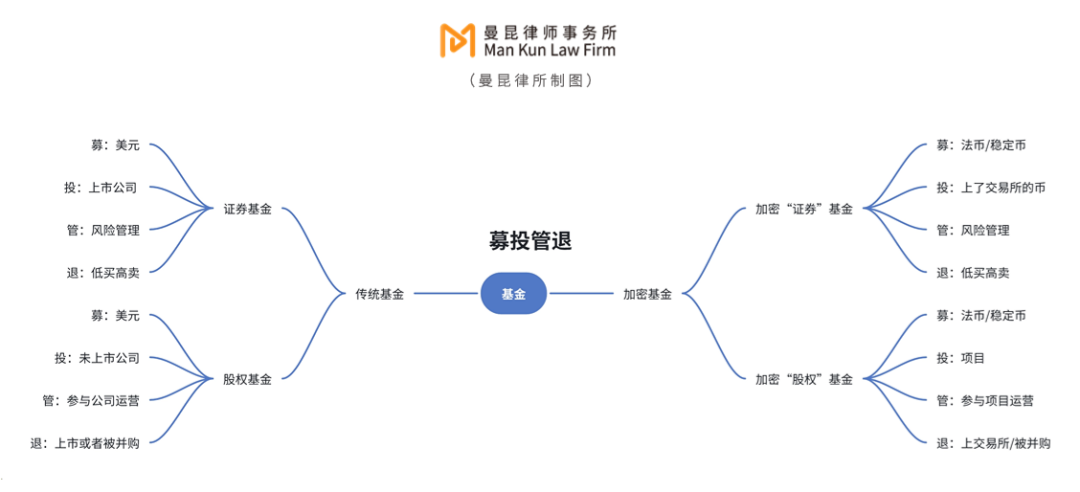

Whether traditional or crypto-focused, every fund goes through a full lifecycle consisting of fundraising, investment, post-investment management, and exit—commonly abbreviated as "raising, investing, managing, exiting" (RISE). In the traditional fund space, funds are categorized into securities funds and equity funds based on the asset classes in their portfolios. Similarly, crypto funds can be understood and structured using this same classification.

If a fund’s portfolio primarily consists of various cryptocurrencies, for clarity we may refer to it as a crypto “securities” fund. Likewise, if the portfolio invests in blockchain projects, we call it a crypto “equity” fund.

RISE: Traditional Funds vs. Crypto Funds

The main differences between crypto “securities” funds and crypto “equity” funds can be identified through their key characteristics. Since crypto “securities” funds invest in highly liquid tokens, they allow continuous subscription and redemption based on market conditions and investor demand. As a result, such funds have variable sizes and no fixed duration. In contrast, crypto “equity” funds invest in specific projects and determine their total size during the fundraising stage, typically with an initial term of 3 years, extendable by up to 2 additional years.

Key Elements of a Fund

Steps to Establish a Crypto Fund

Generally, setting up a crypto fund involves the following steps: first, determining the fund structure; second, selecting an appropriate jurisdiction and fund type; third, appointing intermediaries; and finally, preparing documents and completing closing. It should be noted that unless dealing with very experienced large-scale institutional investors who might have internal compliance teams capable of deferring legal involvement, in most cases legal counsel is engaged from the outset and remains involved throughout the entire process of establishing a crypto fund.

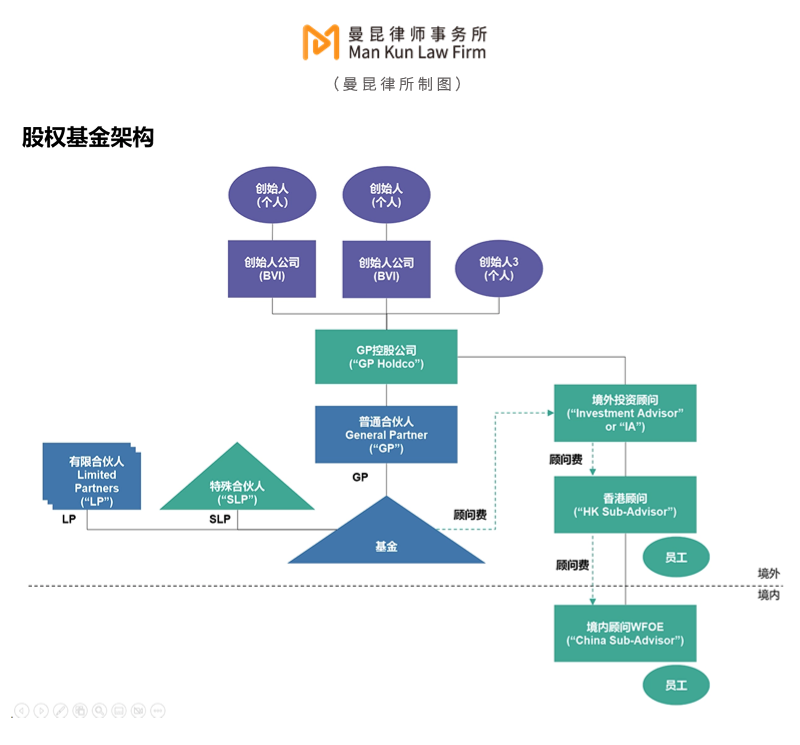

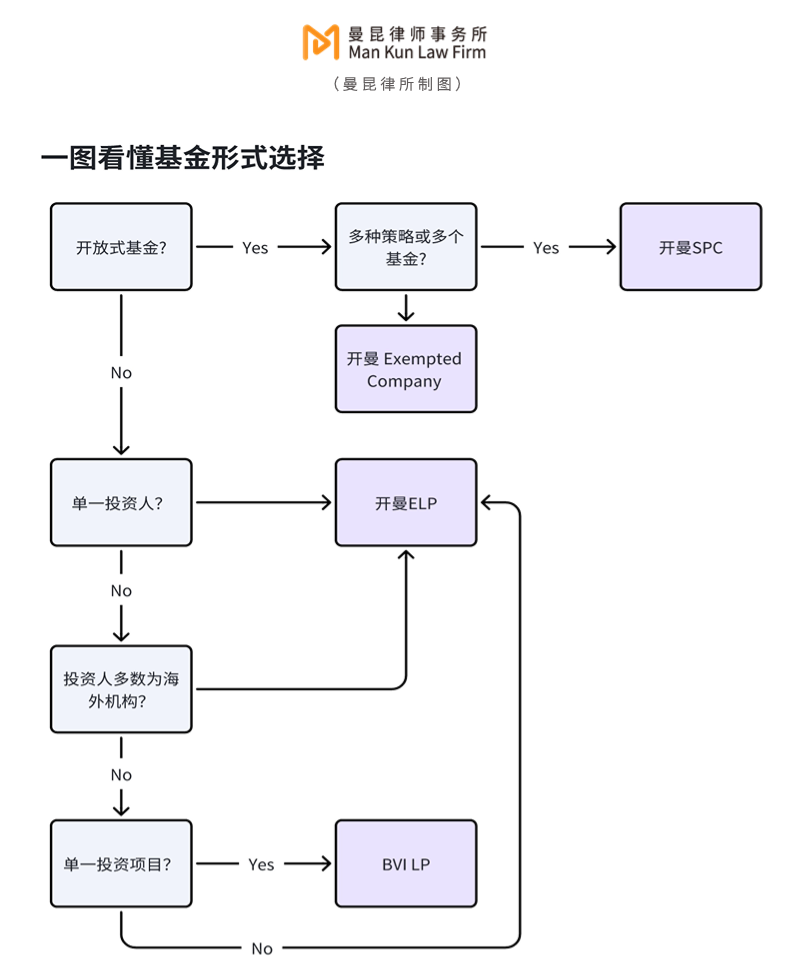

2.1 Determine the Fund Structure

Classic Equity Fund Structure

Without further ado, the classic equity fund structure is illustrated below.

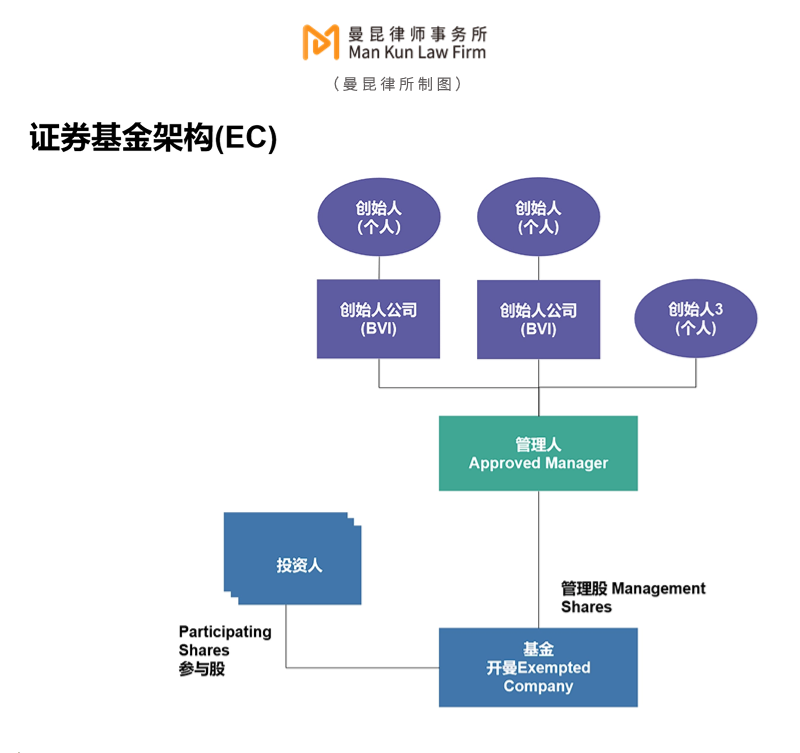

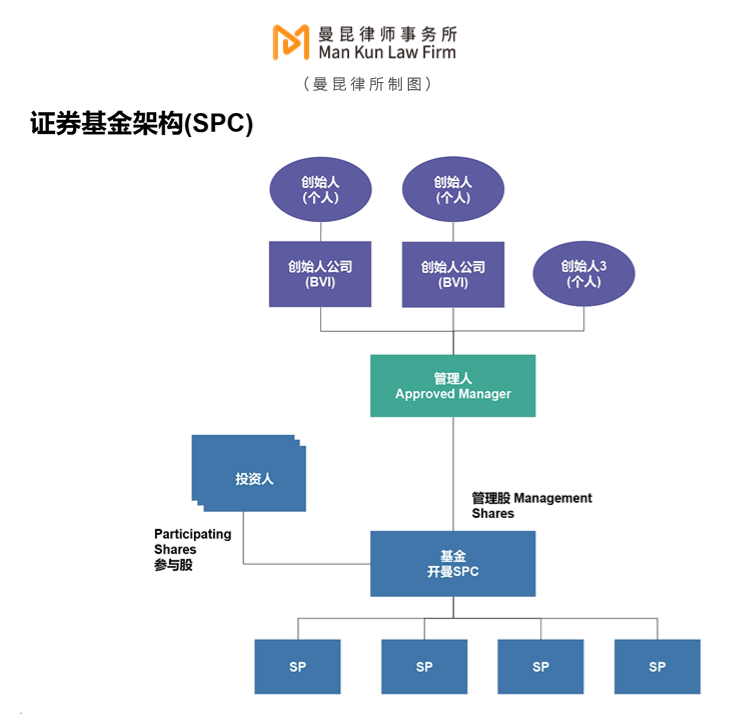

Securities Fund Structure

The structure of a securities fund is simpler than that of an equity fund, mainly comprising two types: standalone fund structure and umbrella fund structure.

1. Standalone Fund Structure: This is one of the simplest forms for a securities fund, where each fund operates as a separate legal entity with its own investment portfolio and shares. Each fund has independent investment objectives, strategies, and shareholders. The standalone structure is generally easier to manage and regulate. An example using a Cayman Islands exempted company is shown below.

2. Umbrella Fund Structure: Refers to a single overarching legal entity that contains multiple sub-funds. Each sub-fund functions as an independent investment pool with its own portfolio and share class. These sub-funds share the same legal and administrative framework but maintain segregated assets and liabilities, isolated from one another. The umbrella structure offers greater flexibility, allowing managers to operate multiple strategy-specific funds under one legal vehicle. An example using a Cayman Segregated Portfolio Company (SPC) is shown below.

2.2 Selecting the Appropriate Jurisdiction / Fund Type

Offshore jurisdictions offer flexible regulations for fund establishment, often requiring no specific financial license or featuring minimal licensing hurdles. Additionally, these jurisdictions provide tax neutrality—such as the Cayman Islands and BVI, which impose no income tax, capital gains tax, stamp duty, or taxes on transactions related to other tax jurisdictions. Establishing a crypto fund in such offshore locations is clearly a more cost-effective option.

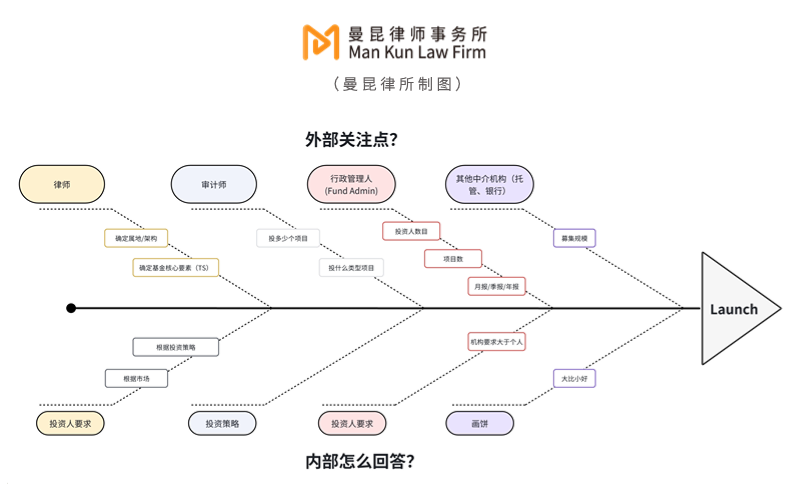

2.3 Appointing Intermediaries

Establishing a fund requires multifaceted support from external intermediaries.

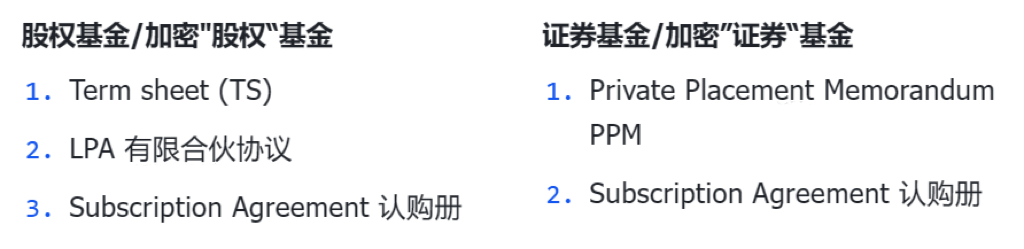

2.4 Preparing Required and Compliance Documents

The main documents required are listed below. Additional documents may be needed depending on the project structure and commercial needs:

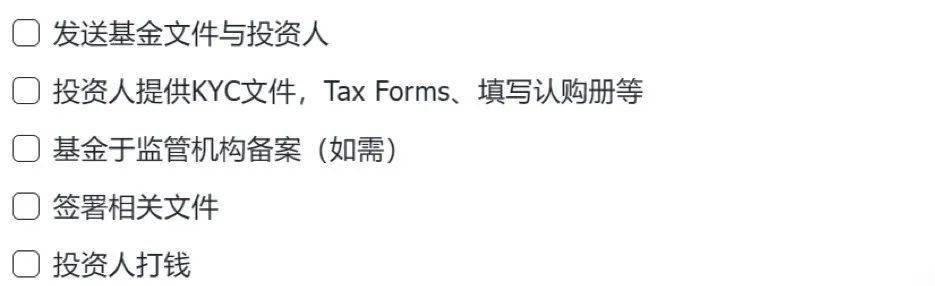

2.5 Closing

Overview of the Regulatory Framework

3.1 Relevant Laws in the Cayman Islands and BVI

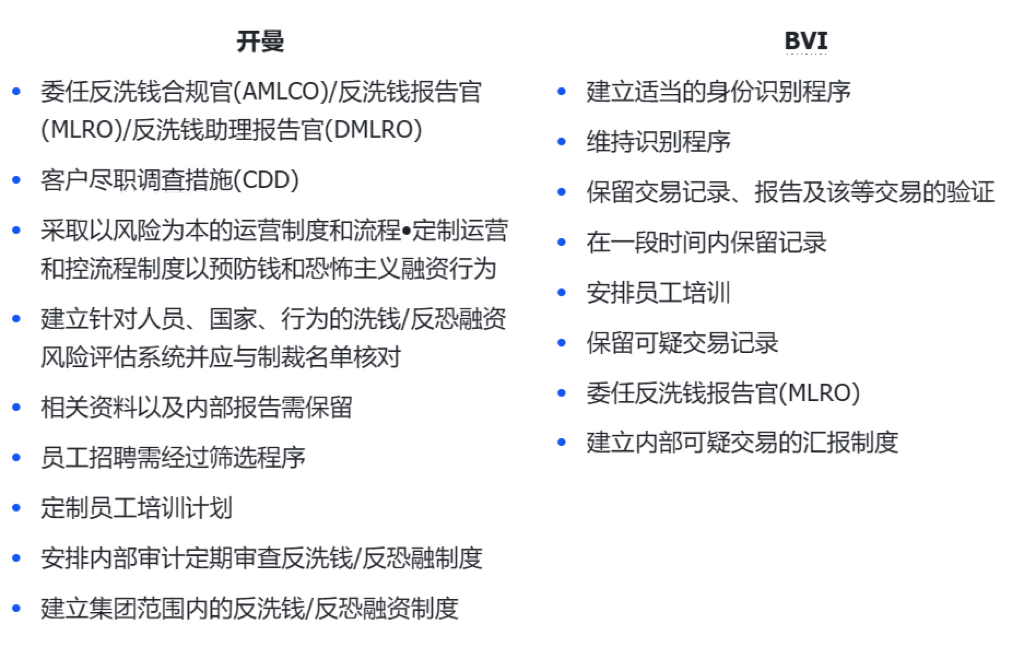

3.2 International Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) Regulations

International AML and CFT regulations are a set of global rules and measures designed to combat money laundering and prevent terrorist financing within the financial system. As financial institutions, crypto funds involve significant capital flows and transactions. To guard against money laundering and terrorist financing, investors must undergo KYC procedures, including providing identity and address verification, and disclosing sources of wealth and funds.

Details include:

3.3 International Tax Compliance: AEOI(CRS)/FATCA

To enable cross-border sharing of financial account information and ensure proper tax treatment of individuals’ assets held in different countries, international tax compliance frameworks have been established. Among them, AEOI/CRS (Automatic Exchange of Financial Account Information) and FATCA (Foreign Account Tax Compliance Act) are key components:

1. AEOI(CRS): A global framework for international tax cooperation aimed at combating cross-border tax evasion through automatic exchange of financial account information. It requires financial institutions to identify and report cross-border accounts to their local tax authorities, who then exchange this data with the tax authorities of the account holders’ residence countries.

2. FATCA: A U.S. law requiring global financial institutions to identify and report information about accounts held by U.S. persons to the Internal Revenue Service (IRS), preventing U.S. taxpayers from evading tax obligations via offshore accounts.

Therefore, investors subscribing to the fund must complete Form W-8 and a self-certification form.

Tax Considerations

Tax exemption at the fund level: The tax regimes of the Cayman Islands and British Virgin Islands (BVI) are characterized by low or zero taxation. In both jurisdictions, entities and individuals generally do not pay income tax, capital gains tax, inheritance tax, or gift tax.

-

Tax exemption at the fund level: The Cayman Islands and British Virgin Islands (BVI) feature notably low or zero-tax regimes. In both jurisdictions, businesses and individuals typically do not pay income tax, capital gains tax, estate tax, or gift tax.

-

Investors file taxes according to their personal circumstances.

-

CARF: At present, cryptocurrency is not a primary focus of AEOI/CRS (Automatic Exchange of Financial Account Information), leaving tax authorities across countries unable to fully capture tax-related information on this decentralized new transaction model, creating tax reporting gaps. However, the OECD has finalized the Crypto-Asset Reporting Framework (CRS for digital assets), scheduled for implementation in 2027.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News