L2 Remains Hot: Data Reveals Mantle's Unique Value and Holding Strategies

TechFlow Selected TechFlow Selected

L2 Remains Hot: Data Reveals Mantle's Unique Value and Holding Strategies

Mantle (MNT) stands at a strategic crossroads, poised to benefit from the upcoming Ethereum Cancun upgrade and the introduction of EIP-4844.

Author: Revelo Intel

Translation: TechFlow

Introduction: Going Long on MNT Before EIP-4844

This article outlines a strategic opportunity to go long on Mantle (MNT) ahead of the Ethereum Dencun upgrade and the introduction of EIP-4844, also known as Proto-Danksharding.

Despite having a less prominent technical team compared to peers such as Polygon or Arbitrum, Mantle’s user-centric approach—combined with innovative yield and airdrop strategies—positions MNT for potential appreciation in Q1 2024.

Overview

Mantle is an Ethereum-compatible optimistic L2 rollup. It leverages Ethereum mainnet (L1) for consensus and settlement, while utilizing its proprietary Mantle DA—powered by EigenDA technology—for data availability services.

Currently, Mantle is using a simplified solution of EigenDA developed in collaboration with the EigenLayer team, awaiting the release of a more comprehensive, standardized version. The plan is to transition fully to EigenDA following its mainnet launch.

Catalysts

Although its technical team may not match competitors like Polygon or Arbitrum, Mantle adopts a user-first strategy. This allows them to leverage top-tier technical solutions while focusing on delivering superior end-user products. Ultimately, these efforts are key to growing on-chain economies and increasing adoption.

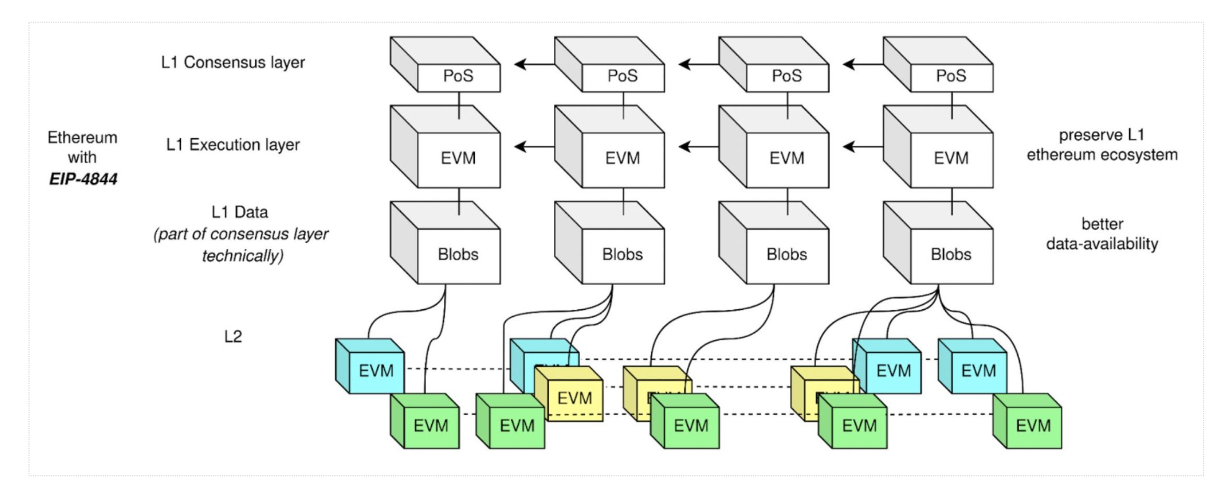

Ethereum's Dencun Upgrade and EIP-4844

The introduction of Proto-Danksharding and EIP-4844 serves as a major catalyst for Ethereum L2s. This upgrade is expected to significantly reduce rollup costs, benefiting L2 tokens such as $MNT. Markets may rebound in anticipation, offering a favorable window to establish positions in L2 tokens—with further catalysts on the horizon. At the core of EIP-4844 lies the concept of "blobs," short for binary large objects. Essentially, blobs are data chunks associated with transactions but distinct from regular transaction data. These blob-carrying blocks are stored specifically on the Beacon Chain and incur minimal gas fees. Blobs allow Ethereum blocks to carry significantly more data without increasing block size. Simply put, leveraging blobs can increase data capacity nearly tenfold compared to average block sizes.

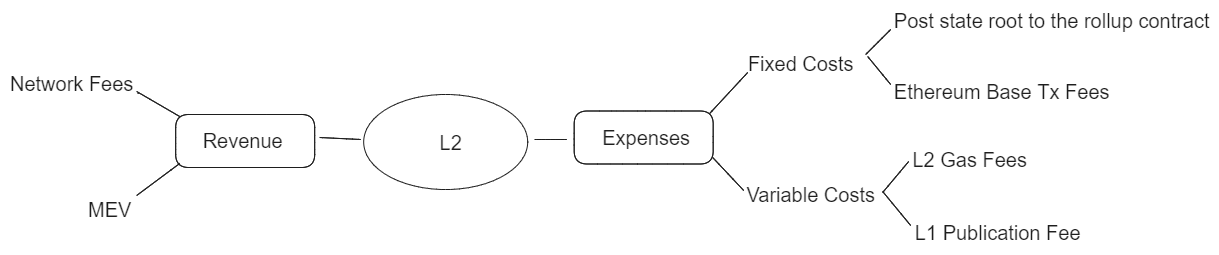

Blobs are introduced primarily to drastically reduce rollup data availability (DA) costs. Currently, publishing data onto Ethereum accounts for over 90% of total rollup fees.

EIP-4844 introduces a dynamic fee system, differing from traditional fee models seen today on L2s. With dynamic blob fees, operating costs on Ethereum will be influenced by two separate markets: the regular transaction market and the blob market.

This shift means rollups must adapt to a fee environment where part of their operations is governed by traditional fee structures, while another part becomes more fluid, adjusting based on specific demand for blob capacity.

Specifically, decoupling the cost of posting L2 data to Ethereum from standard gas prices enables L2s to achieve substantial cost reductions when submitting data to Ethereum—potentially lowering costs by up to 16x, or around 90% below current gas fees.

Sustainable Yield

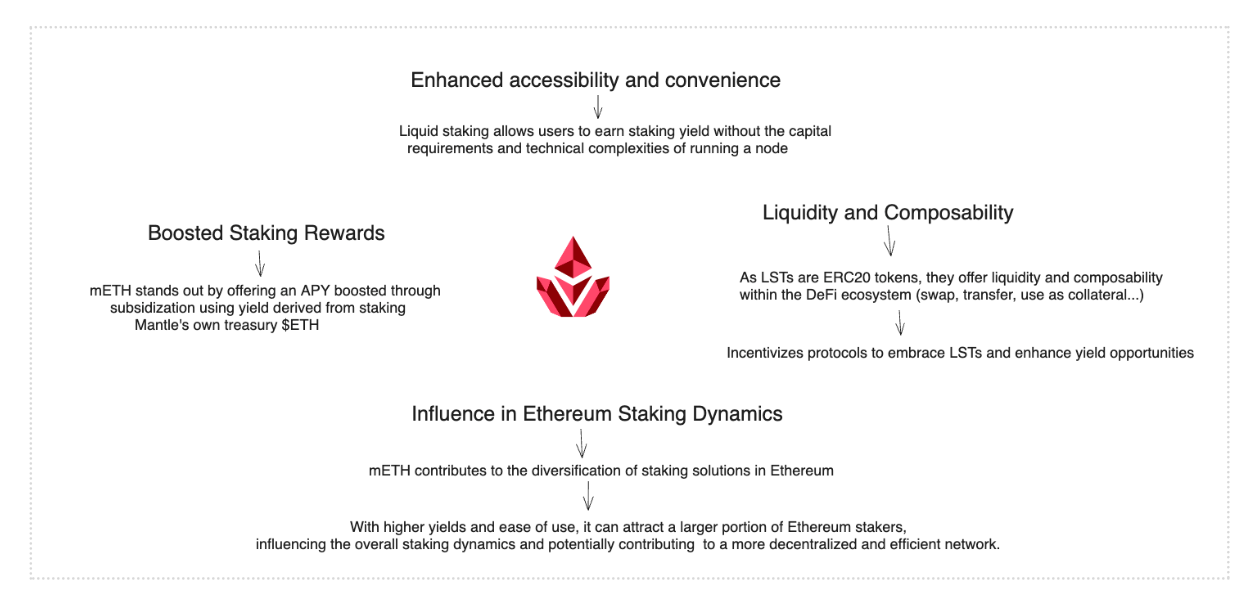

Mantle emphasizes long-term sustainability and real yield opportunities, offering two unique real yield options and one additional speculative opportunity: First, $mETH offers double the staking yield on ETH deposits. This is possible because additional subsidies come from Mantle’s own treasury, which stakes its ETH holdings and passes staking rewards directly to $mETH holders.

Second, $mUSD generates yield from short-term U.S. Treasuries and bank money market funds, enabling users to earn interest on their stablecoin holdings. It is a rebranded version of USDY, designed to maintain a 1:1 peg to the U.S. dollar, with interest distributed via new token units issued through Ondo Finance.

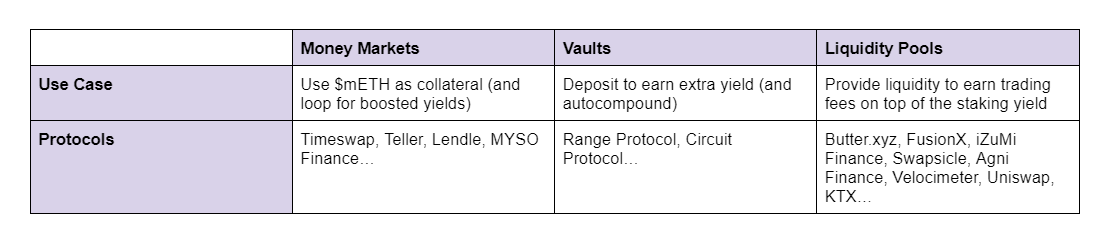

Similar to $mETH, users can employ yield strategies, with platforms like MYSO being among the most popular money markets.

Third, Mantle has been a long-term partner of Eigenlayer. By adopting EigenDA for data availability (DA), it holds a strong hand when future airdrop opportunities arise.

Additionally, we cannot overlook the momentum rollups may gain post-Dencun, as increased sequencer revenue could provide additional fuel for real yield initiatives. Unlike Optimism and Arbitrum, Mantle has already set a precedent for sharing revenue with token holders—by staking ETH in its treasury and distributing staking rewards to ETH stakers.

Enhanced Token Utility

Mantle is one of the few rollups that chose not to use ETH as gas, thereby enhancing the utility of its native token, MNT. Looking ahead, MNT’s utility will extend beyond its role as a gas token. It will be used for staking and may reward holders who participate in such activities. This would not only remove tokens from circulation but also make holding MNT more attractive, potentially increasing buying pressure.

Supply and Demand Dynamics

On the supply side, the absence of token unlocks and inflation provides MNT with a stable and predictable supply, reducing the risk of market dilution. This sets it apart from other L2s, as MNT originated from a token migration of BIT, and the majority of its supply has already been released over time.

On the demand side, it's worth noting that Mantle’s previous association with BitDAO (formerly Mantle) and Bybit may have prevented the token from listing on major exchanges such as Binance, Coinbase, Kraken, or Upbit. Given the successful rebranding and the deployment of the L2 rollup into production, this now represents a potential opportunity. Future listings could serve as a price appreciation catalyst.

Risks and Failure Cases

We should not underestimate how increasingly competitive the L2 landscape has become. Liquidity might flow into other networks such as zkSync, Starknet, Scroll, or Linea in pursuit of their respective airdrops. In such a scenario, we may not see the anticipated growth in TVL and trading volume on Mantle.

However, it's important to recognize the opportunity cost involved, as those funds are generating returns elsewhere instead of within the Mantle ecosystem. While other chains have raised capital at high valuations and their airdrops may be substantial, we do not know when their tokens will actually launch or whether snapshots have already been taken.

Therefore, considering the opportunity cost of liquidity (such as being staked in Blast with no withdrawal option), we believe the risk-reward profile does not favor those alternatives when it comes to capitalizing on a clear L2 catalyst like the Dencun upgrade and EIP-4844.

It's also worth noting that we are seeing power-law dynamics emerge in the L2 space. Despite the expected proliferation of L2s, activity may concentrate around one or two dominant players—such as Arbitrum or Base—while Mantle may not fall into this category.

Hence, it's crucial to remember that betting on Mantle hinges on the belief that MNT will dilute its holders less than its competitors and has additional catalysts beyond EIP-4844—such as MNT staking for airdrops, real yield opportunities, incentives, and ecosystem grants.

Tokenomics

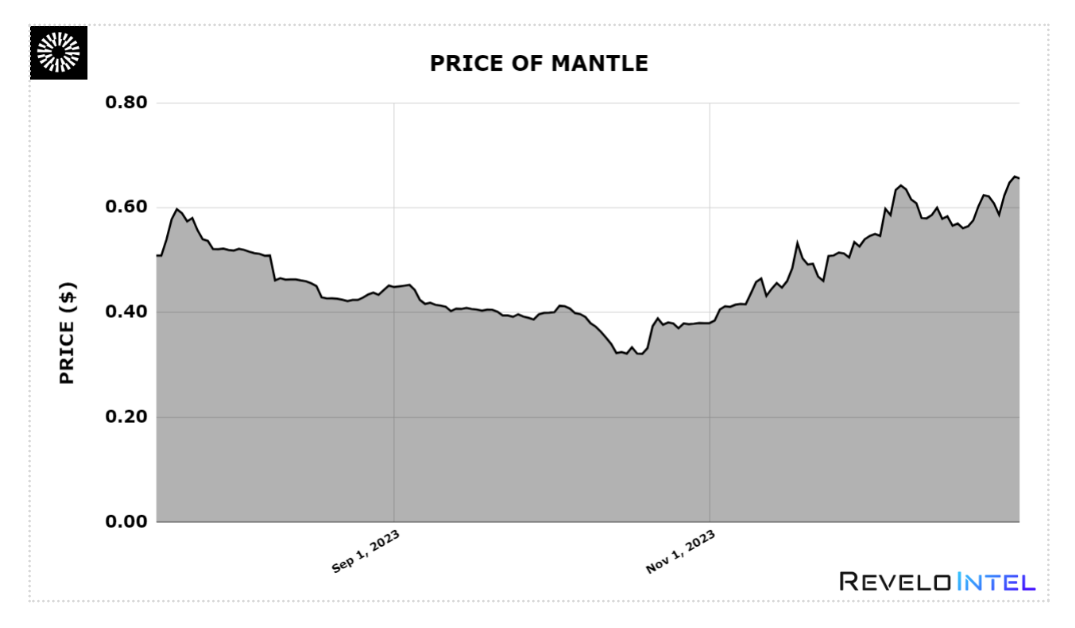

Token Price

October marked a local bottom, with MNT rising 60% over the past 90 days.

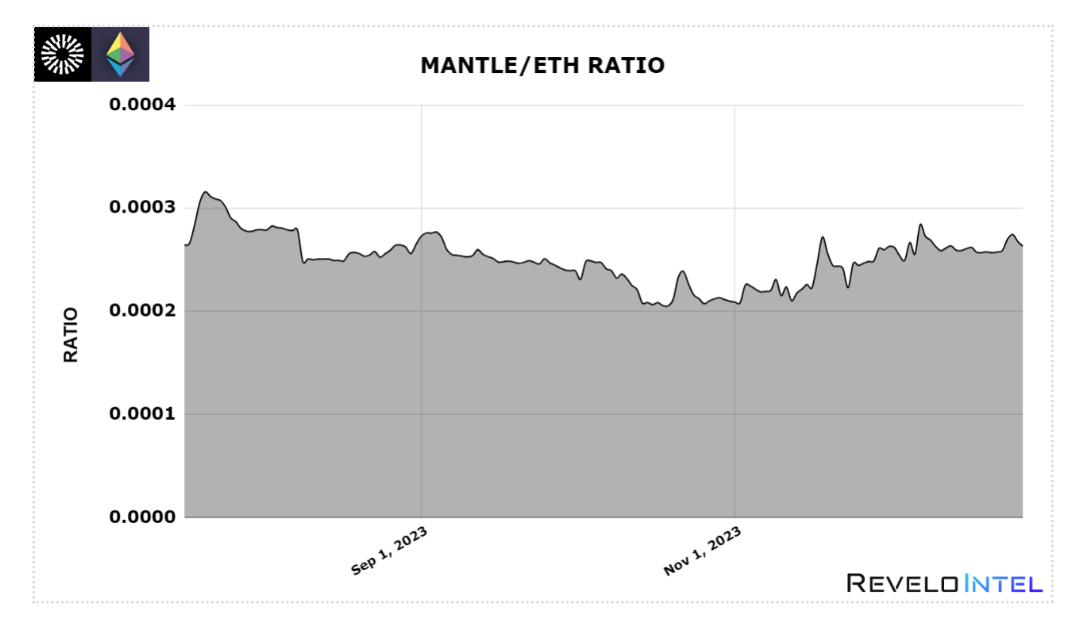

We observe similar trends when comparing MNT and ETH.

Looking at the two charts below, the left axis is denominated in USD, the right axis in ETH.

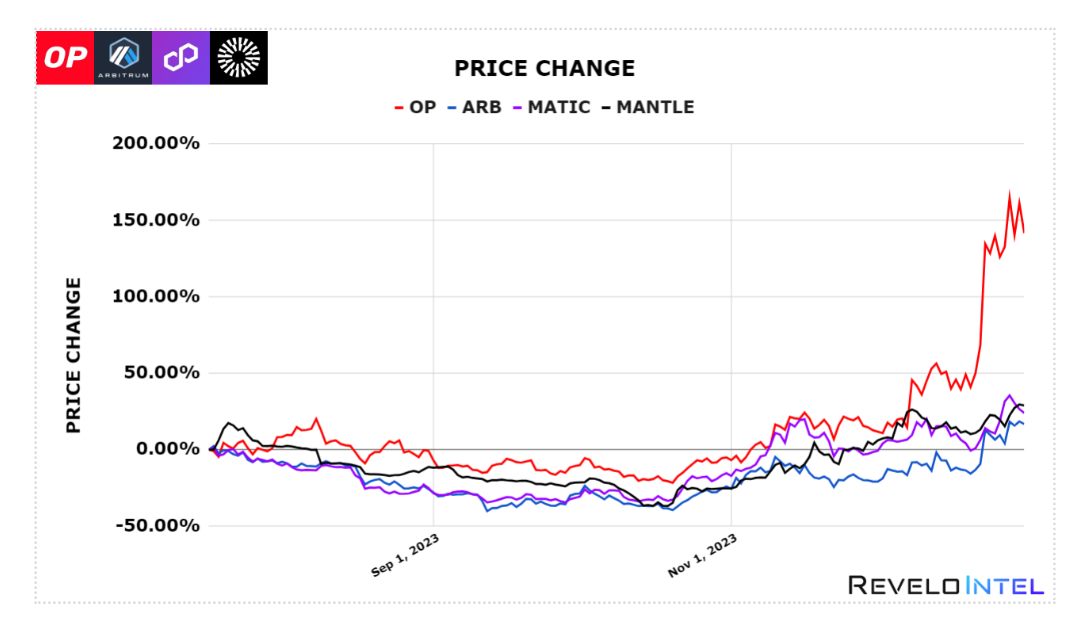

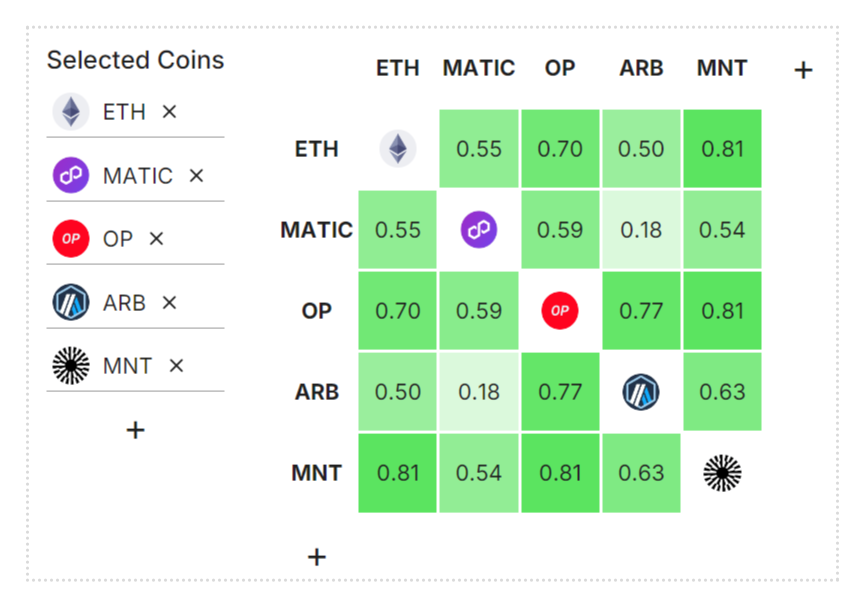

MNT is highly correlated with other L2s, except OP, which performed exceptionally well in December.

Compared to ARB, MNT also shows lower correlation with OP, suggesting the market may hold higher expectations for ARB and OP as the two leading optimistic rollups. This further reinforces our view that developments within the Mantle ecosystem may be underappreciated by the market.

MATIC is not an optimistic rollup, so the market views it differently—especially when considering its transition from a PoS L1 to zkEVM and the gradual rollout of the Polygon 2.0 roadmap.

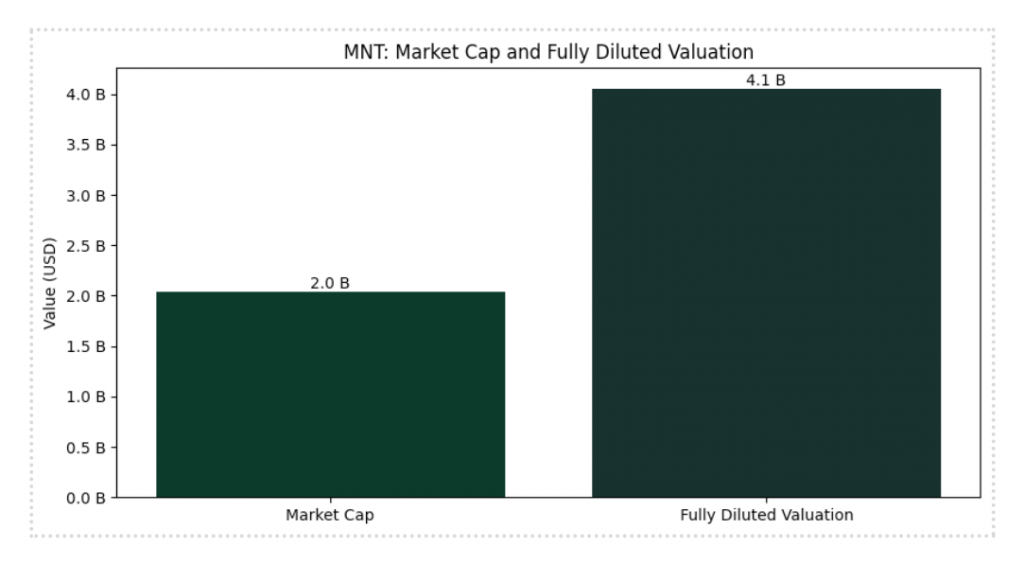

Market Cap and Fully Diluted Valuation

Mantle has consistently ranked within the top 50 by market cap, with a market cap/FDV ratio of 0.50—indicating it is among the L2 tokens with the lowest future dilution and inflation over the next year.

Market Cap / FDV

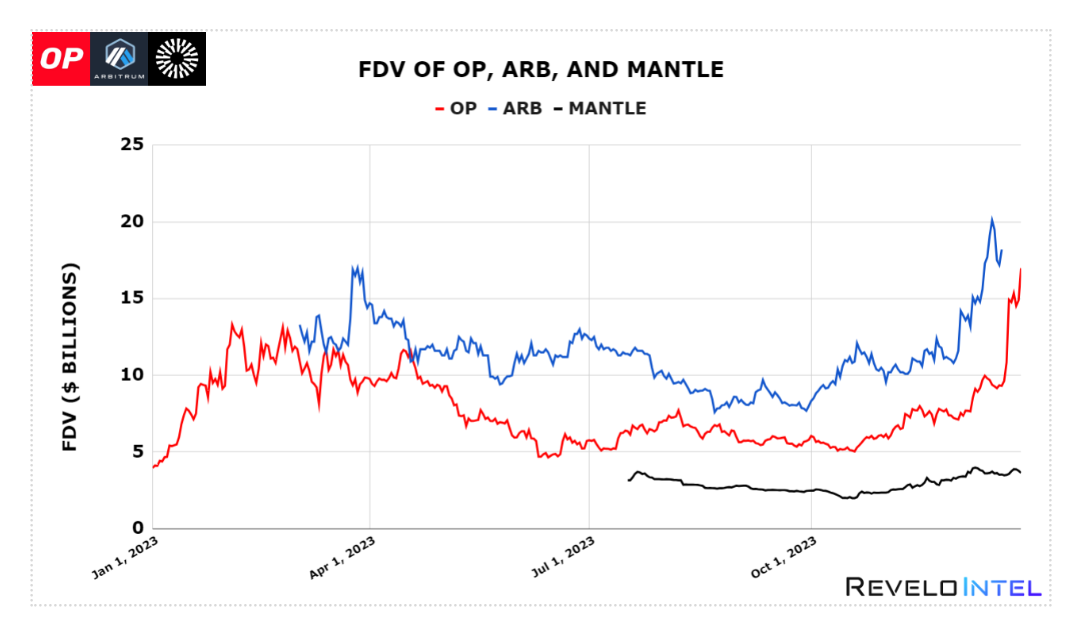

The table below compares the market cap/FDV ratios across various L2 tokens—a proxy for future dilution.

We can also observe significant deviations in FDV for OP and ARB as prices rise. Unlike MNT, neither has yet undergone relatively large supply unlocks.

Arbitrum:

-

March 22: 673 million ARB tokens (worth $1.084 billion) will unlock from Offchain Labs and advisors

-

March 22: 438 million ARB tokens (worth $705.58 million) will unlock from investors

Optimism:

-

January 29: 17 million OP tokens (worth $64.09 million) will unlock from the team

-

January 29: 15.21 million OP tokens (worth $57.35 million) will unlock from investors

It should be noted that we do not expect the supply increases of ARB and OP to create massive sell-side pressure. Instead, our goal is to highlight the low volatility and expected variance in MNT’s FDV.

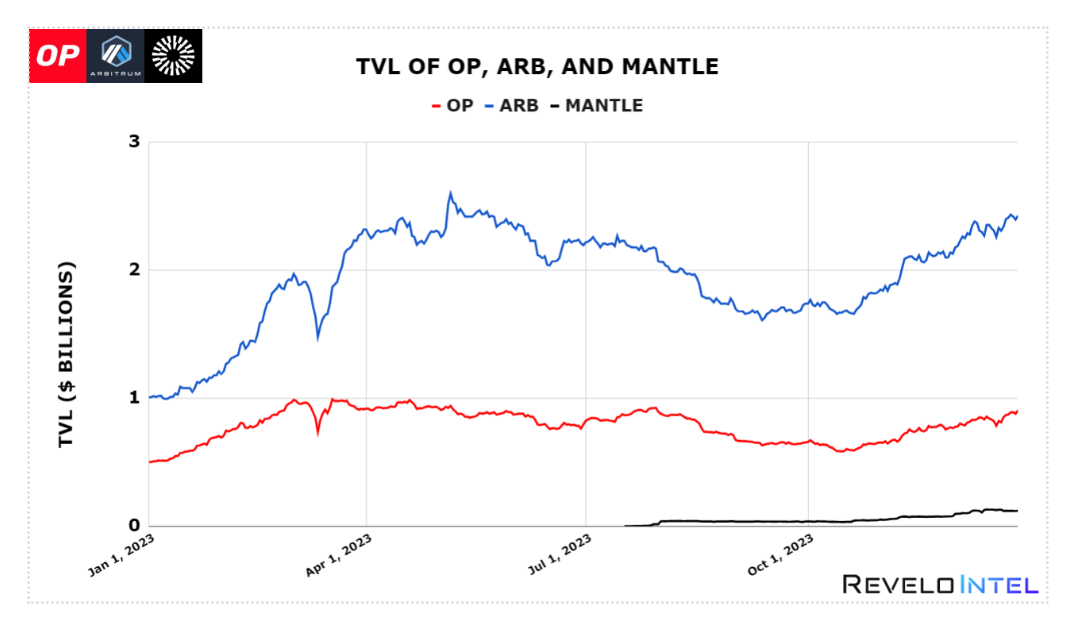

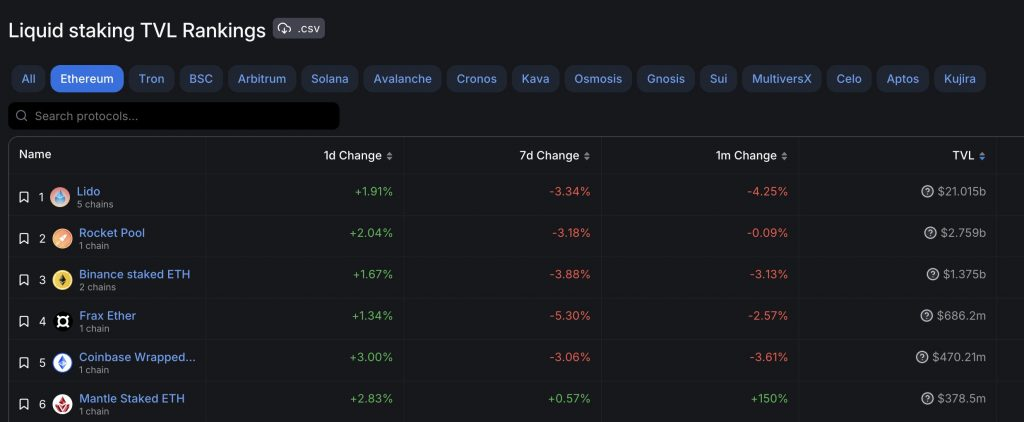

Total Value Locked (TVL)

TVL has been rising, driven by sustainable initiatives that allow investors to earn real yields in both ETH and USD—via $mETH and $mUSD respectively. As a result, we expect these deposits to remain within the ecosystem for the foreseeable future. We can also see from the chart that Eigenlayer raising its cap in December did not significantly disrupt TVL, indicating community confidence that Mantle delivers strong returns on staked ETH.

However, stablecoin market cap remains very low, just over $10 million.

Likewise, compared to Arbitrum ($2.505 billion) and Optimism ($882.39 million), Mantle’s TVL remains minimal. However, as TVL begins to grow, it signals improving liquidity conditions to the market—potentially foreshadowing increased on-chain activity and network fees (which must be paid in MNT).

Nevertheless, entering 2024, we are beginning to see stablecoin inflows exceed outflows.

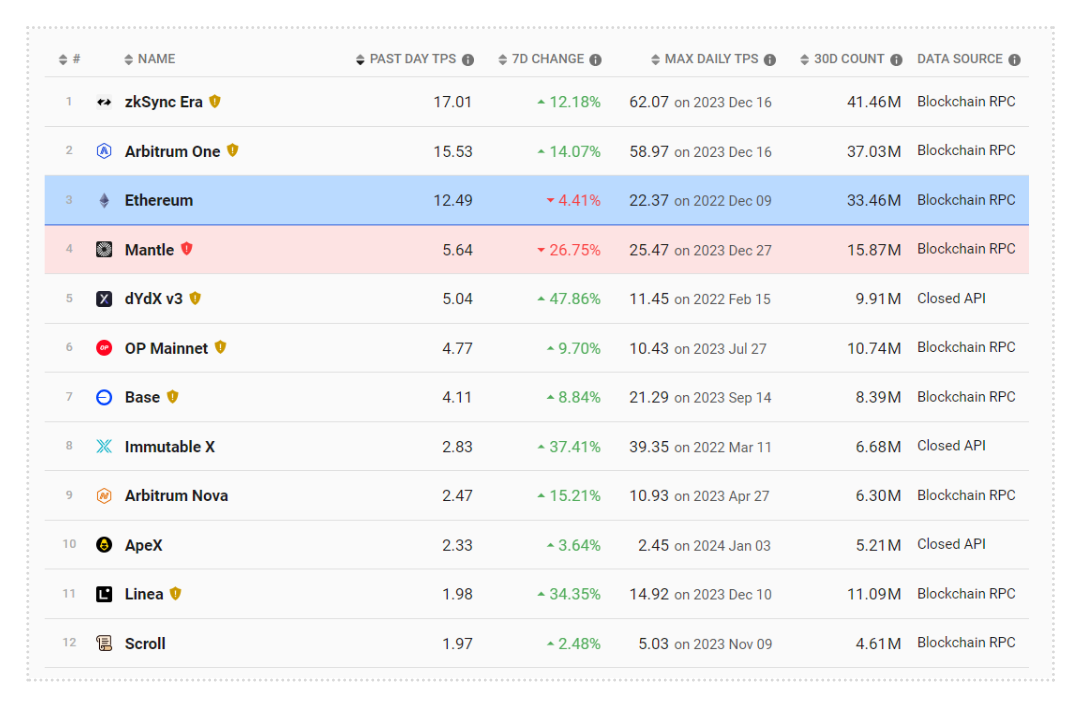

Mantle’s TVL/market cap ratio remains low, but it’s worth noting that the chain launched in mid-2023, new projects are still incubating, and launches are expected throughout 2024. On-chain activity has also increased recently, with 30-day transaction counts surpassing those of Optimism.

Since its soft launch in Q4 2022, mETH has also seen impressive growth over the past month.

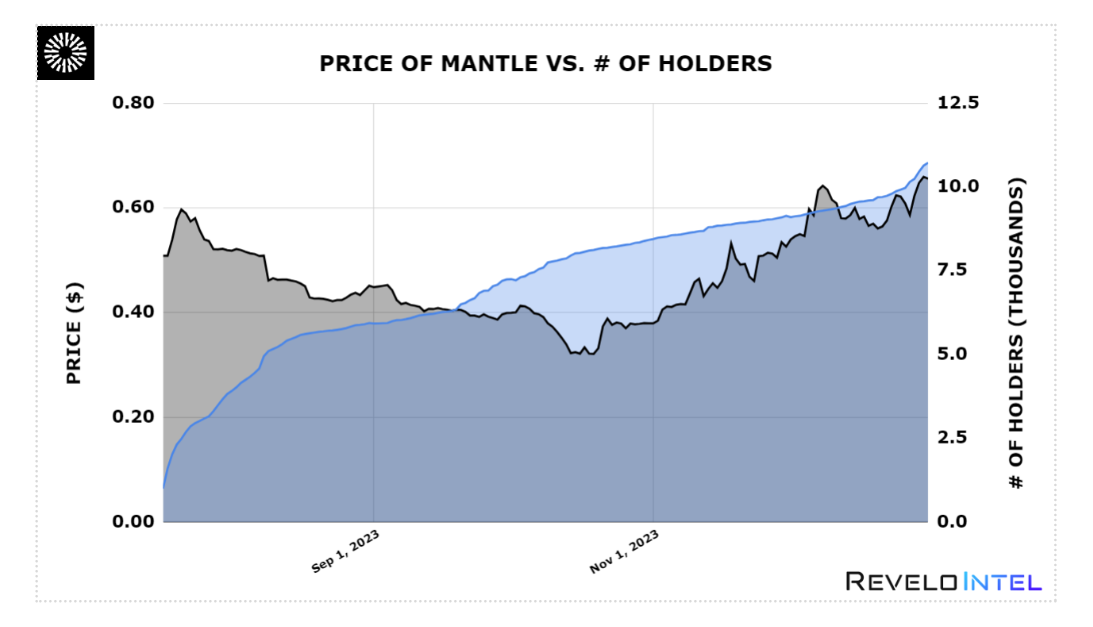

Token Holders

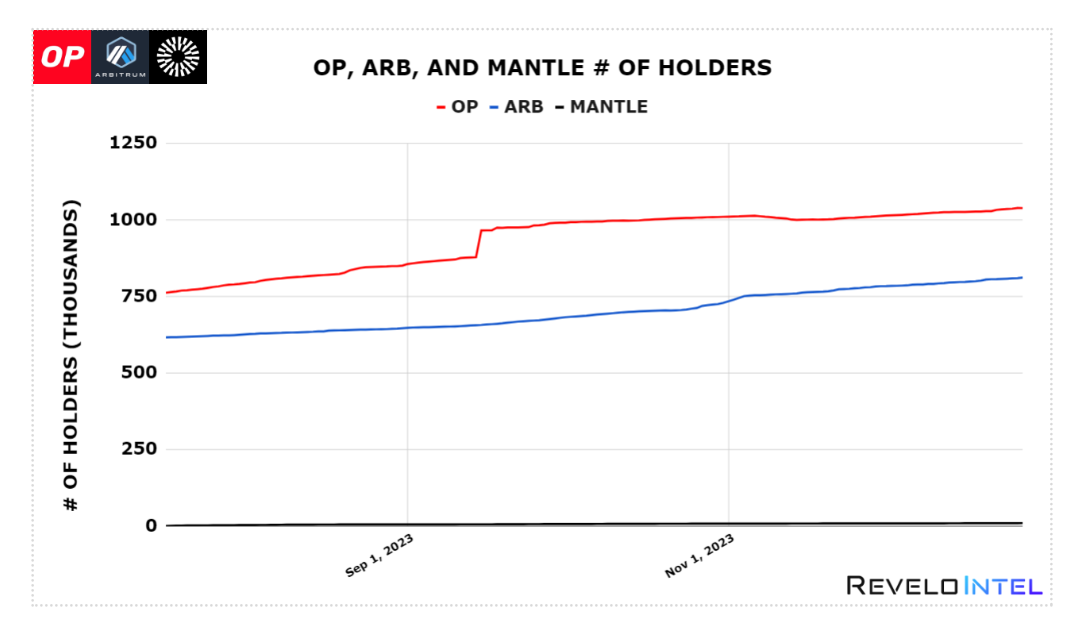

The number of MNT token holders continues to grow, and we expect this trend to accelerate rather than slow down.

Nonetheless, the total number of token holders remains very small—approximately 100 times fewer than OP and 80 times fewer than ARB.

We anticipate this number will rise as more users engage with Mantle Journey and seek to benefit from airdrop allocations across ecosystem projects.

The duration of the incentive program will depend on user feedback and on-chain activity, but it continuously drives new user acquisition through NFTs and exclusive whitelists for new drops. Additionally, Mantle Journey Miles can be redeemed for rewards at the end of each season, with the current campaign offering $20 million in MNT rewards.

Treasury

Mantle still holds one of the largest crypto treasuries outside of the Ethereum Foundation. Notably, it holds over $100 million in stablecoins and more than $250 million in BTC and ETH.

Excluding native tokens, this totals $635 million—over six times larger than Lido and more than eleven times larger than Maker.

Moreover, the presence of native tokens in the treasury is not necessarily negative, as they can be used to incentivize further ecosystem development—and much of it will not enter the market in large quantities for a long time.

Ecosystem

In terms of ecosystem, notable projects include Merchant Moe (a spin-off of Trader Joe), Eigenlayer, Ethena, Ondo, and others such as INIT Capital (money market), Butter XYZ (integrated exchange), Range Protocol (on-chain asset management), Tsunami X (spot and margin trading), and Mintle (an NFT marketplace backed by Rarible).

Equally important, established teams with strong track records such as Byte Masons are launching two projects on Mantle: Cleopatra and Aurelius.

As a DEX, Agni Finance currently dominates with $40 million in TVL—over 30% of the total—followed by Ondo ($30 million), FusionX, iZiSwap, and Range Protocol.

Conclusion

Mantle (MNT) stands at a strategic crossroads, poised to benefit from the upcoming Ethereum Dencun upgrade and the introduction of EIP-4844. Its unique focus on user experience, combined with compelling yield offerings and a robust partner ecosystem, positions it favorably for potential growth.

The absence of token unlocks and inflation further strengthens its investment thesis. Therefore, we recommend holding Mantle (MNT) as a strategic long-term investment ahead of these key developments. Unlike its competitors, MNT has additional catalysts beyond EIP-4844—including MNT staking, enhanced growth prospects through incentives, and lower dilution rates.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News