2023 Ethereum On-Chain Data Review: On-Chain Activity Concentrated in DeFi, Liquid Staking Leading New Use Cases

TechFlow Selected TechFlow Selected

2023 Ethereum On-Chain Data Review: On-Chain Activity Concentrated in DeFi, Liquid Staking Leading New Use Cases

The adoption of L2s expands, DeFi dominates most of Ethereum's activity, and ETH staking increases.

Author: J Hackworth

Translation: TechFlow

At the end of 2022, the cryptocurrency industry faced the collapse of FTX, and market sentiment was extremely low. Today, the industry is filled with excitement and positive sentiment from crypto users and developers.

So, what did on-chain data reveal about 2023? This article explores Ethereum's on-chain metrics to identify the key activities and trends that shaped Ethereum in 2023.

Facing the Bear Market

Given that we spent most of the year in a severe bear market, it's no surprise that various metrics declined across the board. But not all news was bad.

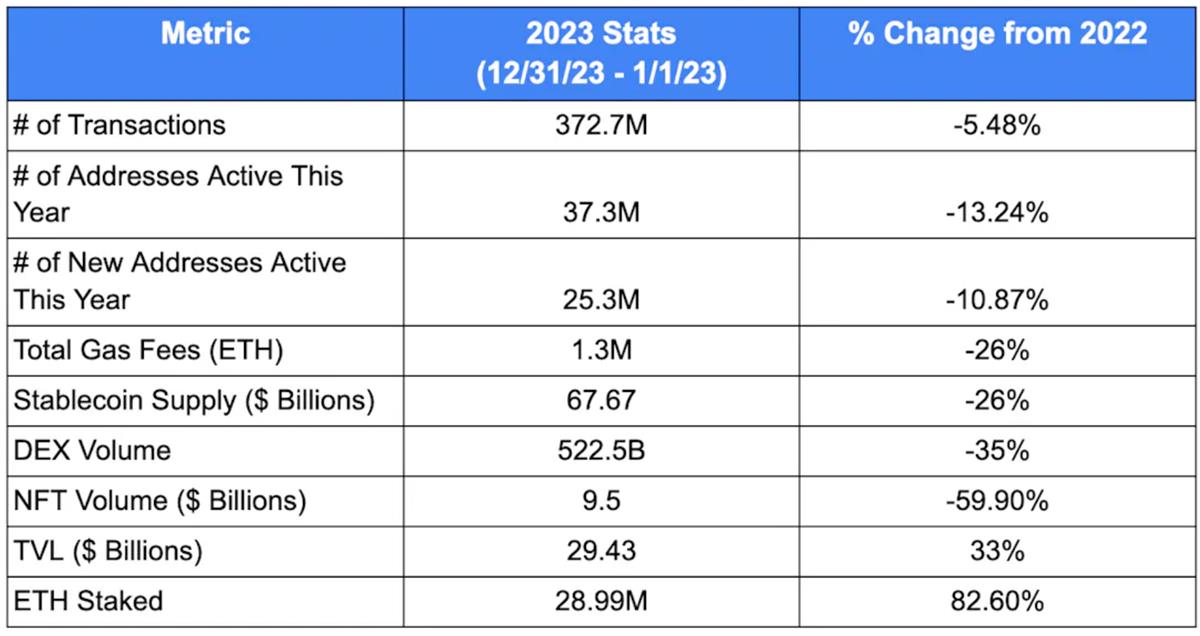

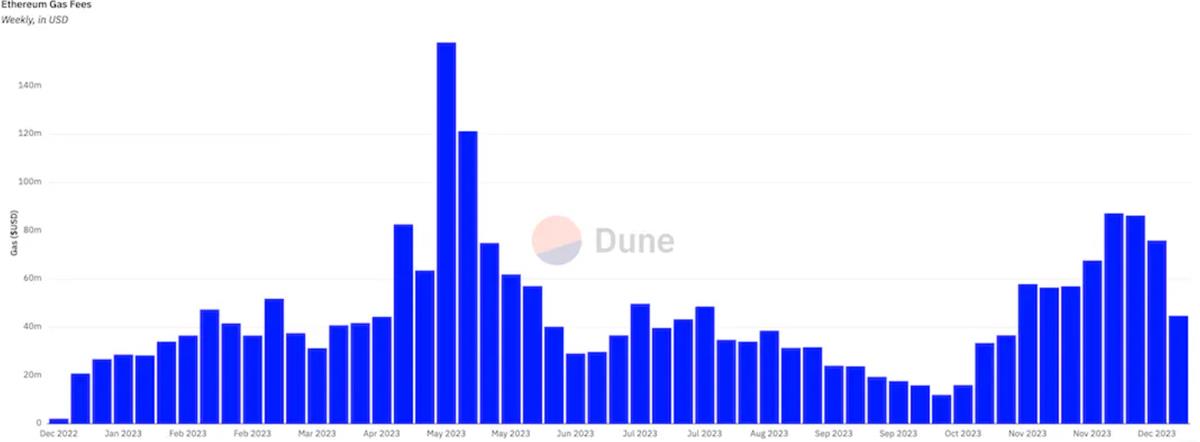

The downside: In 2023, all major indicators declined. Notable drops include total gas fees (-26%), NFT trading volume (-59.9%), and DEX trading volume (-35%).

The upside: By the end of 2023, data began to rebound. Year-to-date TVL has increased by 33%, likely driven by rising prices of ETH and other tokens. Additionally, despite some underperforming metrics, conditions are now improving—including over $20 billion in stablecoin inflows since October (source) and a strong upward trend in gas usage.

Looking deeper into on-chain activity, we can identify three major trends that shaped the Ethereum ecosystem in 2023:

-

L2 Growth

-

DeFi Driving Gas Demand, While NFT Interest Declines

-

Increase in ETH Staking

Embracing L2s

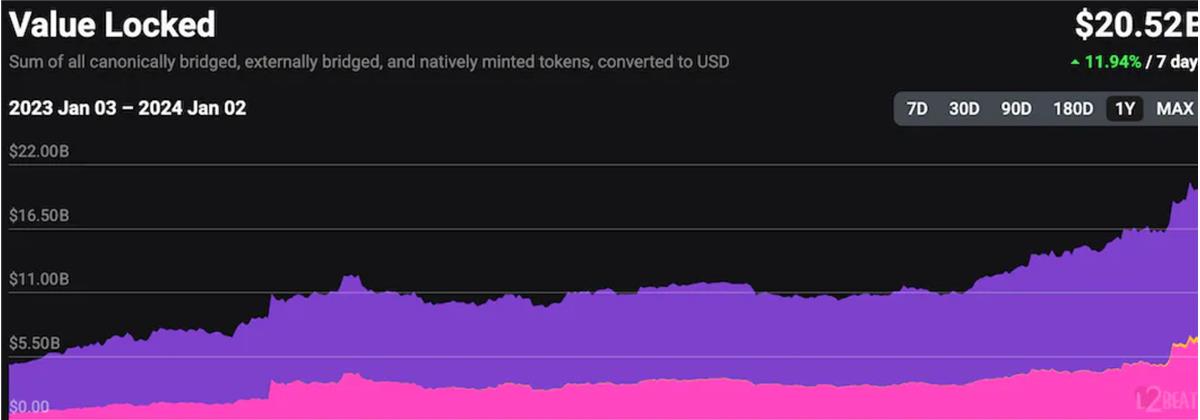

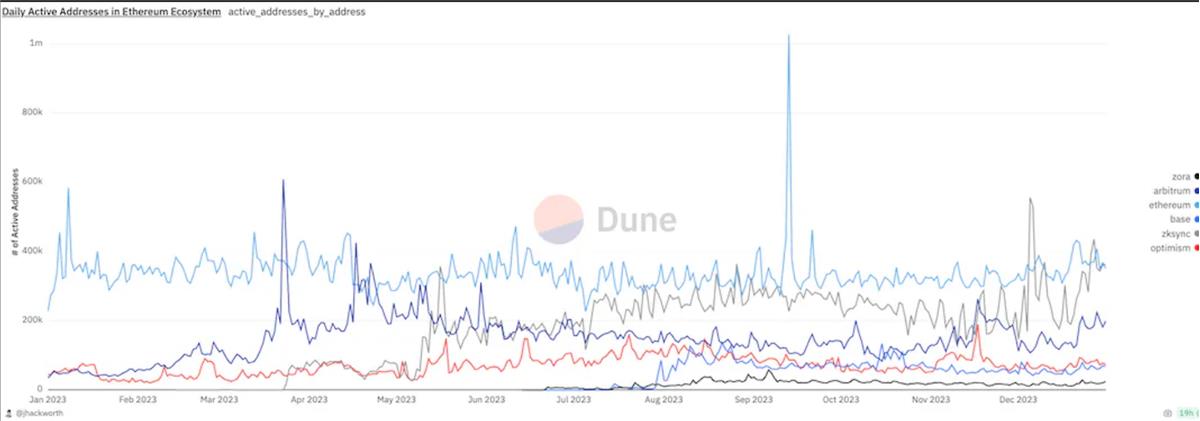

Despite reduced activity on Ethereum mainnet, L2 adoption continued to grow. At the beginning of 2023, there were 16 active L2s with $4.95 billion in TVL. By year-end, the market had over 34 L2s and $20.74 billion in TVL.

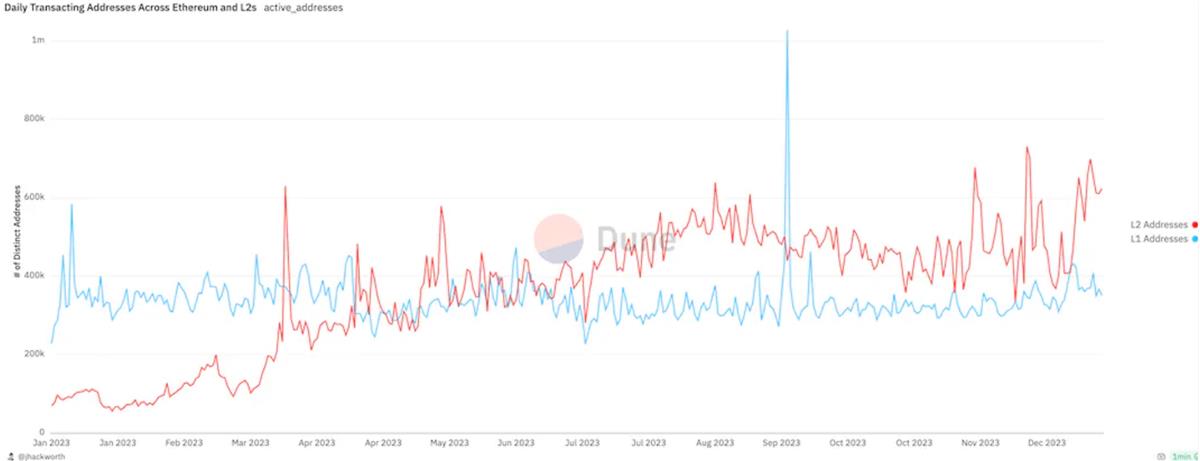

Increased L2 adoption led to a surge in activity. Active addresses on L2s grew from fewer than 70,000 to over 400,000—surpassing the number of active addresses on Ethereum mainnet.

While total L2 active addresses exceeded those on Ethereum, no single L2 could match Ethereum’s level: during 2023, only nine days saw an individual L2 (zkSync, Arbitrum) surpass Ethereum in active addresses. The conclusion: L2s still need to further develop their ecosystems and infrastructure to rival Ethereum's activity levels.

In 2023, L2s made significant progress by attracting new capital and users, offering cost-efficient features for protocols, and enabling unique applications not feasible on Ethereum.

Deep Dive into DeFi Data

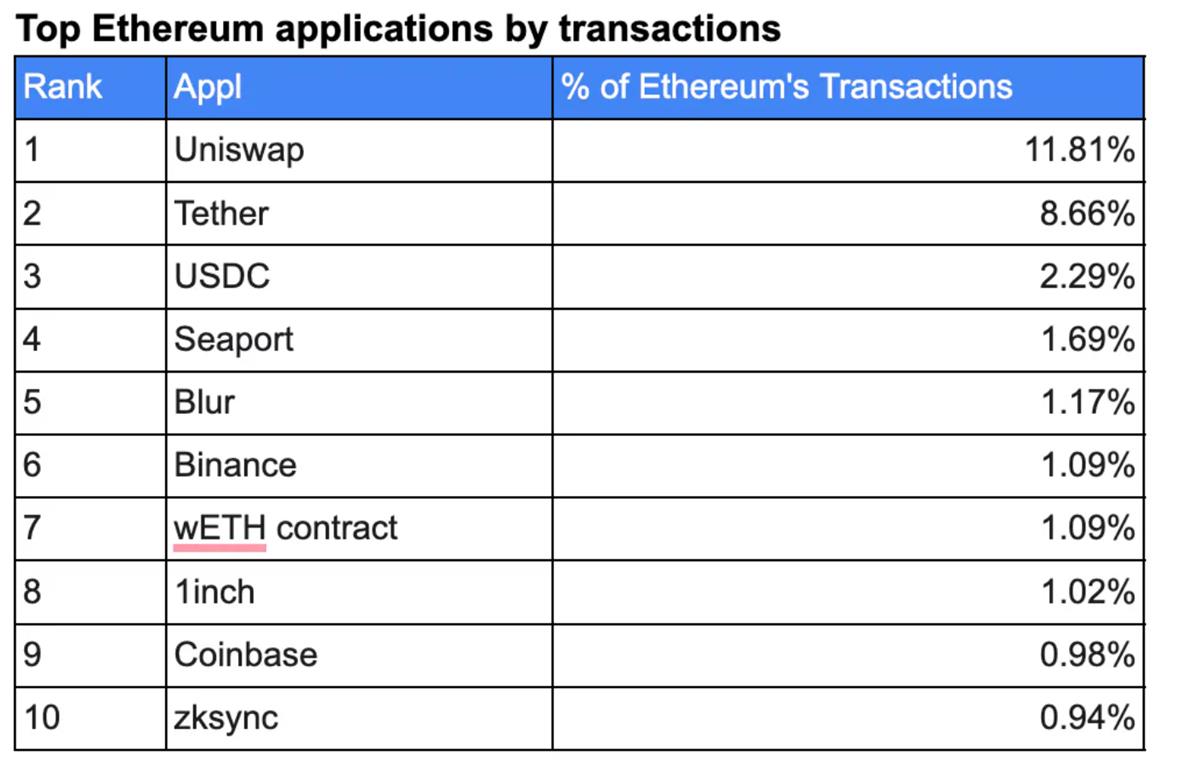

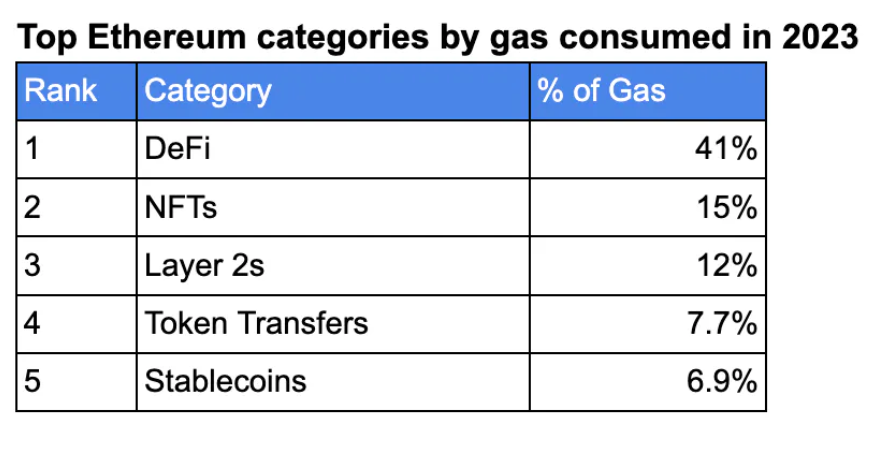

From the charts below, you can see the top ten applications by trading volume and categories by gas consumption. One clear conclusion emerges: Ethereum mainnet activity in 2023 was heavily concentrated in DeFi.

Two things stand out immediately:

-

USDC and Tether ranked as the two highest-volume applications, accounting for 7% of gas usage—highlighting strong demand for stablecoins on Ethereum

-

DeFi, led by Uniswap, accounted for 41% of Ethereum’s gas usage, underscoring the critical role of DeFi and DEXs in Ethereum use cases

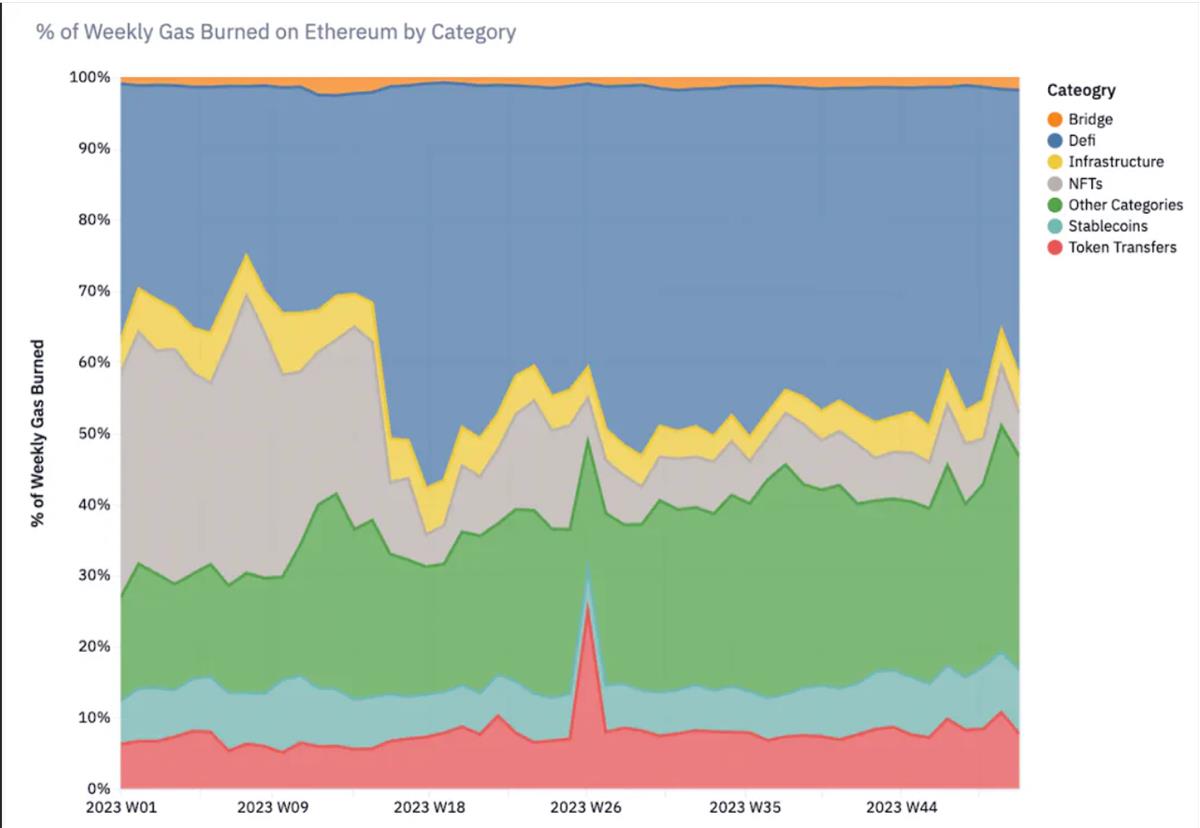

DeFi indeed had a solid year. In January, DeFi accounted for about 31% of Ethereum’s total gas; by year-end, it consumed nearly half.

Although most gas usage came from DEXs, other use cases also performed strongly:

-

Maker achieved an all-time high in total fees, exceeding $105 million, and reached record daily revenue this year

-

Curve and Aave launched new stablecoins, growing by over $103 million and $34 million respectively

-

Tokenized treasuries were part of the real-world asset surge, growing to over $450 million on Ethereum within a year

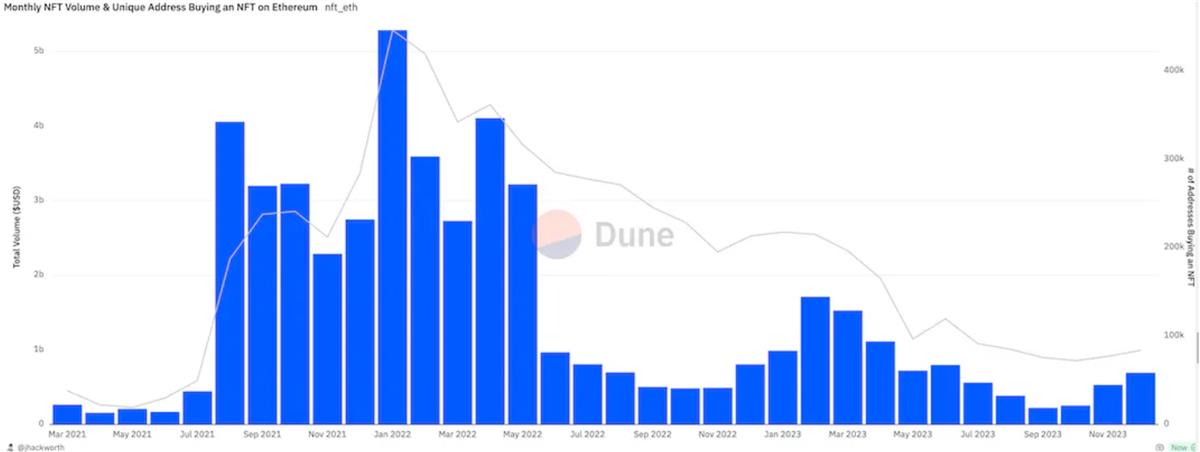

NFT Trading Cools Down

As DeFi took up more Ethereum activity, NFT trading declined. Data shows that NFT gas usage on Ethereum dropped from 32% in January to 7% in December, indicating waning interest in NFTs.

Additionally, in September 2023, NFT trading volume hit a two-year low. However, recent L2 growth and emerging NFT use cases suggest it's too early to write off NFTs' future.

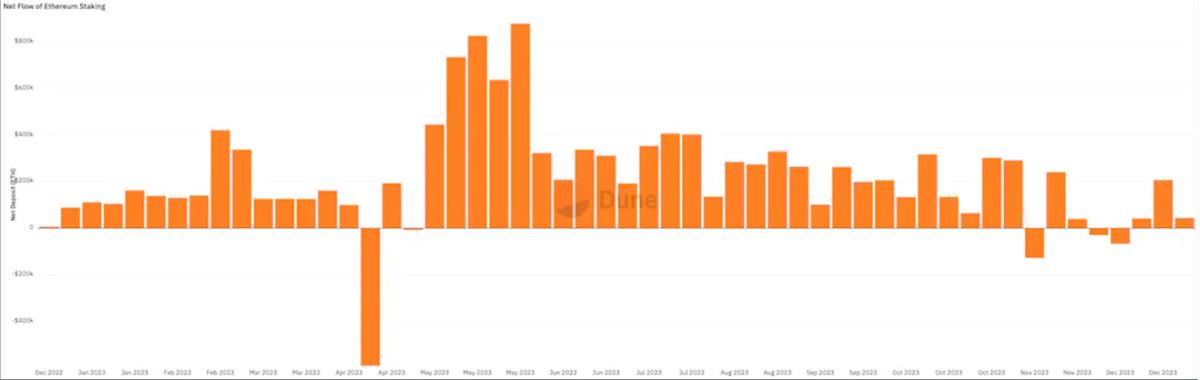

Staking Data

It's hard to believe from the data that Ethereum's proof-of-stake system has been live for just over a year.

2023 marked the first year ETH could be withdrawn from the Beacon Chain, triggering massive inflows into staking. During 2023, the amount of staked ETH supply grew by 82.6%, with around 24% of ETH supply now staked. This was the largest annual increase in ETH staking to date.

As more ETH gets staked, it's becoming a foundational component for the next phase of Ethereum applications and use cases:

-

Using liquid staking tokens (LSTs) as collateral in DeFi apps, even earning yield on L2s like Blast

-

Supporting new stablecoins like Lybra, Prisma, and Ethena, which together have a market cap exceeding $345 million

-

Restaking ETH via Eigenlayer to provide Ethereum’s security to other applications

As staking and LSTs become increasingly common, ETH will be used in diverse ways, and its range of use cases will continue to expand.

Summary

Despite numerous challenges, Ethereum made substantial progress in 2023. L2 adoption expanded, DeFi dominated mainnet activity, and ETH staking surged. With these trends, Ethereum is laying the foundation for significant growth in 2024.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News