The CLARITY Act Released: Is Ethereum the Biggest Winner?

TechFlow Selected TechFlow Selected

The CLARITY Act Released: Is Ethereum the Biggest Winner?

As competitors have all fallen into the second tier of “revenue-based pricing,” Ethereum has become the only asset capable of competing with Bitcoin and gold for store-of-value status.

Original author: Adriano Feria

Translated and edited by Jiahuan, ChainCatcher

On May 12, the Senate Banking Committee released the full 309-page revised version of the Digital Asset Market Structure Clarification Act.

Most coverage will focus on which tokens fail the new decentralization test, which issuers face new disclosure burdens, and which projects must restructure within the four-year transitional certification window. This reporting is not wrong—but it’s incomplete.

The more important story lies in how the bill affects the sole asset that passes every single criterion of the test—and happens to be the only programmable smart contract platform.

Once this framework becomes law, Ethereum will occupy a regulatory category under U.S. law with only one member: itself. Over the past five years, the two dominant bear theses against ETH will simultaneously collapse—and markets have yet to price this in.

Two Bills, One Framework

Before diving into substance, it’s worth briefly reviewing the broader regulatory architecture—because public discourse often conflates two distinct pieces of legislation.

The GENIUS Act (Guidance and Establishment of National Innovation for U.S. Stablecoins Act) was signed into law by the President on July 18, 2025.

It establishes the first federal regulatory framework for payment stablecoins: requiring 1:1 reserves held in liquid assets, monthly reserve disclosures, federal or state licensing for issuers, banning algorithmic stablecoins, and—critically—prohibiting stablecoin issuers from paying interest or yield directly to holders.

The GENIUS Act covers USDC, USDT, and bank-issued stablecoins. It includes nothing else.

The CLARITY Act covers everything else. It addresses SEC/CFTC jurisdictional boundaries, the decentralization test for non-stablecoin tokens, exchange registration, DeFi rules, custody requirements, and the ancillary asset framework.

These two bills are complementary components of a broader regulatory architecture.

Most financial media coverage of the CLARITY Act has centered on stablecoin yield—because Section 4 (“Retention of Stablecoin Holder Rewards”) was the political flashpoint that nearly killed the bill.

Banks pushed to ban indirect yield via exchanges and DeFi protocols because yield-bearing stablecoins compete with bank deposits. Crypto exchanges fiercely advocated retaining it. A bipartisan compromise reached on May 1, 2026 cleared the bill’s path—but after several delays, its passage remains precarious.

This debate matters—but it’s just one piece of a nine-chapter bill. For anyone who actually holds and trades non-stablecoin tokens, the more consequential provisions lie buried in Section 104—and almost no one discusses their second-order impact on asset valuation.

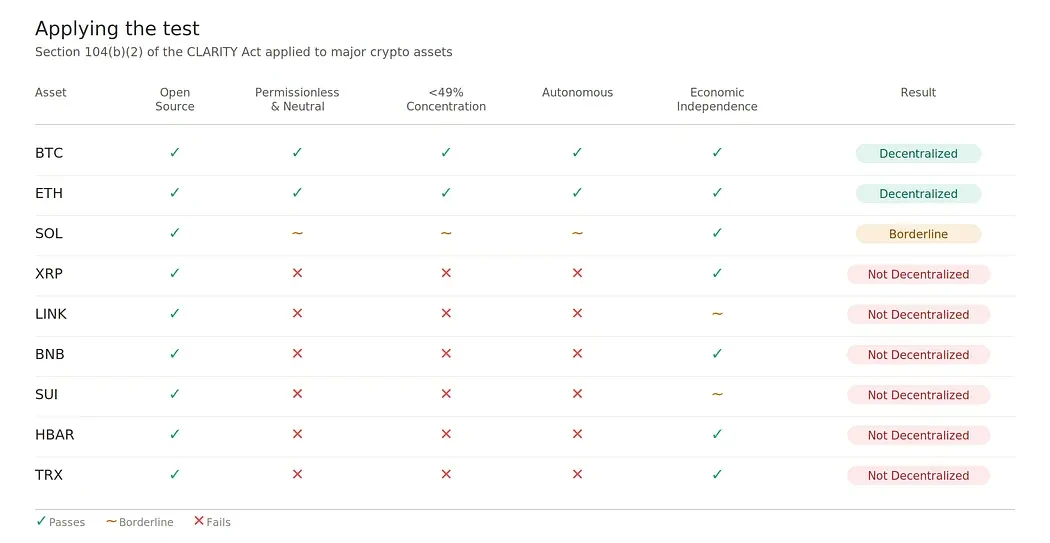

The Five Tests

Section 104(b)(2) directs the SEC to weigh five criteria when determining whether a network and its token are under coordinated control:

Open digital system: Is the protocol publicly available open-source code?

Permissionless and credibly neutral: Does any coordinating group review users—or grant itself hard-coded priority access?

Distributed digital network: Does any coordinating group beneficially own 49% or more of the circulating tokens or voting power?

Autonomous distributed ledger system: Has the network achieved autonomy—or does someone retain unilateral upgrade authority?

Economic independence: Is the primary value capture mechanism functionally operational?

Networks failing this test produce “network tokens,” presumed to be “ancillary assets”—meaning their value depends on the entrepreneurial or managerial efforts of a specific sponsor.

This classification triggers semiannual disclosure obligations, Rule 144–style insider resale restrictions, and registration requirements for initial offerings. Secondary-market trading on exchanges proceeds uninterrupted.

The 49% threshold is the core data point—and far more permissive than the House version’s 20% red line. Networks failing under the 49% threshold do so for genuine structural reasons—not technicalities.

Bitcoin and Ethereum unambiguously pass all criteria. Solana hovers at the edge—its foundation’s influence over upgrades, heavy early insider allocations, and documented history of coordinated network pauses contradict its claims to autonomy and credible neutrality.

All other major smart contract platforms fail for structural reasons difficult to rectify easily. This list includes XRP, BNB Chain, Sui, Hedera, and Tron—and extends to most L1 competitors.

Among assets that pass the test, exactly one possesses a fully functional native smart contract economy.

A Shift in Valuation Frameworks

Tokens trade based on two fundamentally different valuation frameworks.

The first is the commodity/currency premium framework—value derived from scarcity, network effects, store-of-value properties, and reflexive demand—with no fundamental-based valuation ceiling.

The second is the cash flow/equity framework—value derived from income capitalized via standard multiples, subject to strict ceilings imposed by real-world revenue forecasts.

Most non-Bitcoin tokens have occupied a strategic gray zone between these two frameworks—marketing themselves using whichever framework yields higher valuations. The CLARITY Act ends this ambiguity through three mechanisms.

First, disclosure requirements impose a cognitive framework. Section 4B(d) mandates semiannual disclosures—including audited financial statements (for entities >$25M), a CFO’s going-concern statement, summaries of related-party transactions, and forward-looking development costs.

Once a token has SEC filings resembling Form 10-Q, institutional analysts evaluate it like any entity filing Form 10-Q. The document format dictates the valuation framework.

Second, statutory definition itself is qualitative. Ancillary assets are defined as tokens “whose value is dependent upon the entrepreneurial or managerial efforts of the ancillary asset sponsor.” Conceptually, this definition is incompatible with currency premium—which requires value independent of any issuer’s efforts.

A token cannot credibly claim currency premium pricing while satisfying the legal definition of an ancillary asset.

Third, visible scarcity is fragile scarcity. Currency premium is reflexive—and reflexivity requires a scarcity narrative the market can collectively believe.

When a token discloses treasury holdings, named insider unlock schedules, and quarterly reports on related-party transactions to the SEC, its scarcity story becomes visible; once visible, reflexivity vanishes. Investors can precisely see how much supply insiders hold—and when those tokens will sell. This visibility kills buy-side pressure.

The result is a two-tiered market. Tier 1 assets trade on currency premium—with no fundamental-based valuation ceiling. Tier 2 assets trade on income multiples—with reasonable valuation ceilings.

Tokens currently priced on Tier 1 logic but classified as Tier 2 face structural re-rating. For fundamentals-weak, narrative-driven tokens—LINK and SUI being prime examples—this re-rating could be severe.

The Collapse of Two ETH Bear Theses

For five years, bear arguments against ETH rested on two pillars.

The first thesis held that ETH would ultimately be classified not as a commodity—but as a security. Pre-mining, the Foundation’s ongoing influence, Vitalik’s public role, and post-Merge validator economics gave the SEC ample grounds to strike if needed.

Every bull argument for ETH had to discount for tail risk—potential restrictions on institutional capital flows.

The second thesis argued ETH would be displaced by faster, cheaper smart contract platforms. Each cycle birthed new “Ethereum killers”—Solana, Sui, Aptos, Avalanche, Sei, BNB Chain—each touting better UX and lower fees.

This argument claimed ETH’s technical limitations would force economic activity to migrate—diluting its value capture.

The CLARITY Act doesn’t just weaken these bear theses—it structurally dismantles them.

The first collapses because ETH cleanly passes all five Section 104 criteria: no coordinated control, ownership concentration well below 49%, no unilateral upgrade authority post-Merge, fully open-source, and functioning value capture.

The regulatory tail risk long used to justify ETH discounts evaporates.

The second collapses in a more interesting way. “Ethereum killers” only compete with ETH if they operate under the same valuation framework.

If SOL is certified as decentralized, competition continues. If it fails the test—as all other major smart contract competitors currently do—it’s forced into Tier 2 valuation, while ETH remains in Tier 1.

The competitive landscape shifts. Tier 2 assets cannot compete with Tier 1 on currency premium—because Tier 1’s defining feature is freedom from fundamental-based valuation ceilings.

Faster, cheaper chains can still win in specific verticals—transaction throughput and developer attention. But they cannot win on the asset valuation framework that determines L1 market cap—the most critical variable.

The Sole Entry Ticket

Among assets passing the Section 104 test, Ethereum is the only one with a fully functional native smart contract economy. Bitcoin passes—but its base layer lacks programmable finance.

Every smart contract platform with meaningful TVL fails one or more substantive criteria. This includes Solana, BNB Chain, Sui, Tron, Avalanche, Near, Aptos, and Cardano.

Thus, the bill creates a new regulatory category: decentralized digital commodities with native smart contract economies—and currently, Ethereum is its sole member.

Every traditional financial institution exploring tokenization, settlement, custody, or onchain finance needs two things: programmability and regulatory clarity.

Pre-CLARITY, these attributes were strictly segregated. Bitcoin offered clear property rights but no programmability. Smart contract platforms offered programmability but legal ambiguity. Post-CLARITY, Ethereum becomes the only asset delivering both within a single statutory category.

Once the framework takes effect, anyone building tokenized Treasuries, tokenized funds, onchain settlement infrastructure, or institutional-grade DeFi gateways has a clear preferred underlying vehicle.

This preference isn’t aesthetic or technical—it’s compliance-driven. Asset managers, custodians, and bank-affiliated funds operate within legal frameworks favoring commodity-class assets and rejecting securities-like treatment.

Institutional capital flows follow asset classification—and current classification narrows to the sole programmable asset.

The Sound Money Question

Once BTC and ETH share Tier 1 classification, a careful comparison of their monetary properties becomes necessary—because conventional wisdom gets causality backwards.

BTC’s appeal has always rested on its nominally fixed 21-million supply schedule and predictable quadrennial halvings. As a scarcity narrative, this is highly valuable—and its simplicity is why BTC secured currency premium first.

But BTC’s supply model carries three structural burdens rarely mentioned in scarcity discussions.

First, mining generates persistent structural sell pressure. Network security relies on miners bearing real-world operating costs: electricity, hardware, hosting, and financing.

These costs are denominated in fiat—meaning miners must continuously dump large portions of newly minted BTC onto the market regardless of price.

This selling is permanent, price-insensitive, and baked into the consensus mechanism itself—the cost of maintaining PoW security.

Second, BTC offers no native yield. Yield-seeking holders must either lend BTC to counterparties (introducing credit risk) or move it to non-BTC platforms (introducing custody and cross-chain bridge risk).

Holding non-yielding BTC incurs opportunity cost that compounds over time relative to yield-bearing assets. For institutional holders measuring performance against yield-inclusive benchmarks, this is a real and persistent drag.

Third, the cliff-like decline in mining subsidies poses a long-tail risk to decentralization—the very quality qualifying BTC for Tier 1.

Block rewards halve every four years and approach zero by 2140—but actual pressure arrives much earlier. By the 2030s, subsidy income will be a fraction of today’s level, forcing the network to rely on fee income to maintain security.

If the fee market fails to develop sufficiently, lowest-cost miners will consolidate, miner concentration will rise, and the credible neutrality and decentralization prized in Section 104 will erode. Not imminent—but an unresolved structural risk in BTC’s model.

Ethereum reverses each of these attributes.

ETH has variable issuance with no fixed cap—the core argument of sound money purists against it. This critique is superficial.

What matters to holders is the rate of change in their share of total supply—not whether the supply schedule has a fixed endpoint.

Under Ethereum’s post-Merge design, all newly issued tokens are distributed as staking rewards to validators. Validator yields have historically exceeded inflation—meaning any participant in staking maintains or increases their share of total supply over time.

The “infinite supply” argument rings rhetorically true—but mathematically false—for anyone running a validator node or holding liquid staking tokens.

The structural sell pressure burdening BTC doesn’t exist at comparable scale for ETH. Validators’ operating costs are negligible relative to their rewards. Solo staking requires one-time hardware purchase and minimal ongoing electricity. Liquid and pooled staking abstract even these costs away.

Newly issued tokens accrue to the validator set and are largely retained—not sold to cover costs. This same security model that pays holders avoids the price-insensitive selling required by PoW.

The subsidy cliff problem doesn’t exist. Ethereum’s security budget scales with the value of staked ETH—and is funded by continuous issuance and fee income. No predetermined date exists for sudden security funding collapse.

This model is self-sustaining—while BTC’s increasingly depends on fee market development, whose success remains uncertain.

None of this argues ETH will replace BTC. They serve distinct roles in institutional portfolios.

BTC is a simpler, clearer, politically more defensible scarce asset. ETH is productive monetary collateral—delivering value by paying holders for securing its network.

The key point: the conventional view that BTC’s fixed supply makes it “harder money” than ETH collapses under scrutiny.

ETH’s variable issuance combined with native yield delivers superior real economic properties for holders versus BTC’s fixed supply plus zero yield—without structural sell pressure or long-term security funding risk.

This matters immensely for institutional allocators building Tier 1 crypto exposure. The case for ETH alongside BTC isn’t just “the programmable one”—but “the one that pays you to hold it, without forcing structural selling to maintain its security.”

Treasury Companies Tell the Same Story

The structural differences between BTC and ETH aren’t abstract. They’re concretely reflected in the balance sheets of the two largest corporate treasury vehicles built around these assets.

Strategy (formerly MicroStrategy) holds the world’s largest corporate Bitcoin position. BitMine Immersion Technologies (BMNR) holds the world’s largest corporate Ethereum position.

Observing how they fund operations and behave reveals the underlying supply-side dynamics playing out in real corporate finance.

As of May 2026, depending on reporting cycles, Strategy holds ~780,000–818,000 BTC.

It funds these purchases using $8.2B in convertible notes (maturing 2027–2032) and ~$10.3B in preferred stock (covering STRF, STRK, STRD, and STRC series).

Convertible notes must convert to equity at maturity (diluting existing shareholders) or be refinanced (requiring market access on acceptable terms).

Preferred stock carries ongoing dividend obligations—STRC alone requires ~$80M–$90M per quarter.

Strategy’s core software business is dwarfed by its treasury position—and its cash flow pales next to debt obligations. With BTC’s price decline, it reported losses for three consecutive quarters—including a $12.5B net loss in Q1 2026.

On May 5, 2026, Executive Chairman Michael Saylor explicitly broke his five-year “never sell Bitcoin” pledge on the Q1 earnings call—telling analysts Strategy may sell some BTC to pay dividends.

Within days, he revised wording to “never be a net seller” and “sell one BTC to buy 10–20”—but the directional shift was real.

Polymarket odds of Strategy selling any BTC by year-end jumped from 13% pre-call to 87% post-call.

The structural reality is simple: Strategy’s ability to continue accumulating BTC depends on its capacity to issue new debt or preferred stock on repayable terms.

On the Q1 earnings call, Saylor explicitly laid out the model’s breakeven: BTC must appreciate ~2.3% annually for Strategy’s existing holdings to indefinitely cover STRC’s dividend obligations—without selling common stock.

This figure was widely reported—and reflects Saylor’s own published calculation—but it’s only one of three conditions that must simultaneously hold.

The mNAV (market-to-net-asset-value) premium must remain above ~1.22x to justify continued issuance; market demand for STRC preferred must stay strong; and BTC must clear the 2.3% threshold.

Individually, none are catastrophic—and 2.3% is far below BTC’s historical average. But it’s a moving target. STRC’s effective dividend rate has risen from 9% at issuance to 11.5% after seven monthly hikes—pushing up the breakeven over time.

The underlying asset provides no organic income stream to fund operations. Strategy must successfully refinance, reissue, or convert to maintain its position.

BitMine Immersion Technologies operates on a fundamentally different footing. Per latest disclosures, BMNR holds ~3.6M–5.2M ETH (depending on reporting period) and carries essentially zero debt. It holds $400M–$1B in unsecured cash.

~69% of its ETH is actively staked—generating ~$400M in estimated annual staking revenue via its proprietary MAVAN (Made-in-America Validator Network) infrastructure.

The structural difference is BMNR generates native yield from its underlying asset. Staking rewards compound regardless of ETH’s spot price.

The company needs no debt rollovers, preferred stock refinancing, or mNAV premium maintenance to fund operations. It can be a passive, perpetually cash-flowing holder—or actively deploy capital.

Its $200M January 2026 investment in MrBeast’s Beast Industries—and planned “MrBeast Financial” DeFi platform on Ethereum—represents the latter. BMNR leverages its treasury position to participate in and accelerate Ethereum’s economic ecosystem—not just hold the asset.

This distinction matters for long-term trajectories. Chairman Tom Lee recently commented at the 2026 Miami Consensus that BMNR may slow ETH accumulation because “there’s other stuff happening in crypto now”—indicating expansion paths beyond simple accumulation.

Bitcoin treasury companies lack such paths. No native yield to compound, no protocol-level ecosystem to participate in, no equivalent to ETH’s validator infrastructure or DeFi integration.

Both companies suffered during this cycle’s downturn. BMNR fell ~80% from its July 2025 peak. MSTR posted losses for three consecutive quarters. As digital asset treasuries broadly face pressure, both saw NAV premiums compress.

This analysis isn’t about one company winning and another losing. It’s about structural mechanics producing divergent outcomes—mapped directly to the underlying assets’ properties.

Strategy’s flexibility comes from continuous capital market access. BMNR’s flexibility comes from continuous staking yield.

Strategy must roll debt to maintain position. BMNR must keep validators online. Strategy’s operational needs embed structural sell pressure. BMNR has structural buy pressure from reinvesting staking rewards into holdings.

These aren’t narrative preferences—they’re mechanical consequences of underlying asset supply-side properties.

Where industry narratives go next likely depends on evolution over the next 12–24 months.

If BTC surges, Strategy’s model performs brilliantly—and leveraged BTC logic remains mainstream institutional crypto narrative.

If BTC stagnates or falls, Strategy’s debt rollover demands grow heavier—and lack of native yield becomes an increasingly obvious structural disadvantage.

The Ethereum treasury model has a wider viability range—because staking yield provides a floor absent in pure BTC accumulation.

For an industry about to receive its first comprehensive regulatory framework under CLARITY—and for an institutional audience about to make decade-long capital allocation decisions based on that framework—treasury company comparisons offer a useful forward-looking lens: how abstract supply-side arguments translate into real corporate behavior.

Treasury companies are leading indicators of underlying asset trajectories.

The Boundary Between Network Philosophy and Legal Classification

One subtle but important point requires direct discussion. Even if Solana eventually achieves decentralization certification under Section 104, that legal classification alone wouldn’t place SOL on equal valuation footing with ETH.

Legal classification is necessary—but insufficient—for Tier 1 currency premium treatment. The deeper question is what each network consciously optimizes for—and what its own founders and ecosystem participants believe it should be valued for.

On these questions, ETH and SOL made conscious, divergent choices.

From inception, Ethereum prioritized credible neutrality, reliability, and longevity over raw performance. The network achieved ten years of 100% uptime—no major disruptions since launch.

Following the May 2025 Pectra upgrade, active validators exceed one million—globally distributed, with largest concentrations in the U.S. and Europe—but substantial presence across multiple continents. Average validator uptime is ~99.2%.

Its consensus mechanism prioritizes finality and security over speed—using carefully designed constraints ensuring no single entity (including the Ethereum Foundation) can unilaterally alter the protocol.

Solana prioritizes throughput and transaction speed. Its architecture optimizes for processing maximum TPS at minimum cost. These are real engineering achievements—enabling use cases Ethereum’s base layer can’t satisfy. But they come at a cost—one Solana’s ecosystem increasingly acknowledges.

Since 2021, the network has endured at least seven major outages—including multi-hour downtimes in Jan, May, and June 2022; 18 hours in Sept 2022; >18 hours in Feb 2023; and 5 hours in Feb 2024. Each required coordinated validator restarts.

Solana Foundation reports 16 months without downtime as of mid-2025—a real improvement—but contrasts sharply with Ethereum’s never-downtime record—reflecting fundamental design priority differences—not temporary engineering capability gaps.

Validator metrics tell a similar story. Solana’s active validator count fell from ~2,560 in early 2023 to ~795 in early 2026—a 68% decline.

The Nakamoto coefficient—the minimum number of entities controlling a critical network share—dropped from 31 to 20. Solana Foundation characterizes this as healthy pruning of subsidized Sybil nodes that never meaningfully contributed to decentralization—a defensible interpretation.

An alternative interpretation is that Solana validator economics became uneconomical for small operators—whose annual vote fees now exceed $49,000—supported by data.

Both interpretations contain partial truth—but neither produces the geographically and operator-diverse network Ethereum maintains.

Client diversity is the clearest contrast—and most revealing—because it directly relates to structural resilience required for monetary collateral.

On Ethereum, the consensus layer enjoys healthy diversity: Lighthouse (~43% validators), Prysm (31%), Teku (14%), with Nimbus, Grandine, and Lodestar sharing the rest—no single client dominates.

The execution layer is more concentrated but improving: Geth (~50%, down from historic 85%), Nethermind (25%), Besu (10%), Reth (8%), Erigon (7%).

This diversity isn’t theoretical. In September 2025, a critical Reth client bug stalled 5.4% of Ethereum nodes—but the network stayed online because other clients independently implemented the protocol.

Ethereum’s design philosophy explicitly anticipates any single implementation failing—and network continuity doesn’t depend on any team’s code being flawless.

On Solana, client diversity has historically been virtually nonexistent. For most of mainnet’s life, every validator ran some variant of the original Agave codebase.

The February 2024 outage brought the entire network down—because no independent implementation existed to keep it running during bug fixes.

Today, Jito-Solana—an Agave fork optimized for MEV—controls ~72%–88% of stake. Original Agave holds another 9%. Both share identical code ancestry—meaning a core Agave logic flaw could impact ~80% of the network simultaneously.

Firedancer—the first truly independent Solana client, developed by Jump Crypto—launched on mainnet in December 2025—holding ~7%–8% of stake.

Frankendancer—a hybrid combining Firedancer’s networking with Agave’s execution—holds another 20%–26%.

The Solana ecosystem targets 50% Firedancer stake in Q2–Q3 2026—a major step toward real client diversity—but until crossing that threshold, the network remains structurally vulnerable to single-implementation failure.

These differences aren’t accidental engineering outcomes. They reflect deliberate philosophical choices.

Ethereum consistently chooses slower, more conservative paths—prioritizing network operation regardless of any single team’s code—or any single participant’s intent.

Solana consistently chooses faster, more performant paths—accepting higher coupling and operational dependency for speed.

Both are valid engineering approaches—producing assets with different properties.

Asset impacts follow. Solana’s ecosystem itself—including major analyst frameworks from VanEck and 21Shares—increasingly values SOL on cash flow as a capital asset.

SOL holders earn returns from network revenue, token burns, and staking yield—the asset priced on its capacity to generate these cash flows.

This aligns internally with Solana positioning as financial infrastructure for high-throughput applications. It’s also a Tier 2 valuation framework.

Co-founder Anatoly Yakovenko publicly defines Solana as a “global financial atomic state machine”—emphasizing execution-layer value capture over currency premium. Solana’s community largely embraces this framework.

By contrast, Ethereum consistently positions ETH as productive monetary collateral. Staking yield, ultrasonic money discourse, deflationary mechanisms, and validator distribution all serve Tier 1 framing—where ETH is held as a monetary asset and pays holders for securing network security.

While this framework is more contested within ETH’s community than SOL’s, underlying network design supports it.

Practically, this means—even if Solana achieves decentralization digital commodity certification under CLARITY—its own ecosystem positions it as a Tier 2 asset.

Certification unlocks institutional access and eliminates regulatory tail risk—both price-positive—but doesn’t place SOL in the reference frame driving currency premium pricing. Markets won’t assign currency premium to an asset its own creators and ecosystem treat as a cash-flow-generating capital asset.

This is the deeper reason ETH’s unique status endures beyond what legal frameworks alone imply.

Legal classification, network design philosophy, ecosystem positioning, and observed market preferences all point in the same direction. For any competitor to credibly challenge ETH’s Tier 1 status, it must pass the legal test, maintain comparable reliability and decentralization—and get its own ecosystem to position the asset as currency premium—not cash flow.

Among existing networks, no candidate satisfies all three—and the philosophical commitment required can’t be remedied short-term.

The Real Meaning of DeFi Dominance

ETH’s enduring DeFi dominance has long been viewed as a legacy effect. Conventional wisdom holds Ethereum won DeFi early via first-mover advantage—but dominance will erode as faster chains compete for developer attention and user activity.

Each TVL migration to Solana, each DeFi summer on competing chains, each “market rotating out of ETH” article reinforces this view.

Actual results don’t match this narrative.

Despite well-funded competitors over years—and technically superior execution layers—despite L2 fragmentation and high L1 fees, Ethereum and its Rollup ecosystem still dominate stablecoin settlement, DeFi TVL, RWA tokenization, and institutional onchain activity.

BlackRock’s BUIDL Fund launched on Ethereum. Franklin Templeton’s tokenized money market fund launched on Ethereum. Stablecoin supply on Ethereum mainnet plus major L2s dwarfs all competing chains combined. Tokenization of real-world assets occurs overwhelmingly on Ethereum.

This persistence—against technically superior alternatives—isn’t just legacy. Markets have priced something not yet legally explicit: builders and institutions value credible neutrality and regulatory defensibility far more than performance.

Their bets are exactly what CLARITY now formally codifies.

The very traits making Ethereum slow—strict decentralization, no unilateral upgrade authority, conservative consensus change mechanisms, and deliberately planned validator decentralization—are precisely what Section 104 rewards.

Every article over the past three years claiming “ETH is losing to faster chains” measured the wrong variable. The real critical variable has always been credible neutrality—and once regulatory direction clarifies, credible neutrality inevitably becomes the qualifying attribute.

Market preference is correct. It just lacked a self-defending legal framework—now being codified in the Senate bill under consideration.

A Shift in Reference Frames

Historically, ETH’s natural comparables were other smart contract platforms: SOL, BNB, SUI, AVAX. Within that frame, ETH was “the slow, expensive one”—facing constant narrative pressure as competitors rolled out faster execution layers.

Valuation multiples anchored to revenue, TVL share, and developer activity—all with natural valuation ceilings.

Post-CLARITY, this reference frame breaks. Tier 2 chains compete on cash flow multiples and value capture. ETH’s relevant reference frame becomes Tier 1 monetary base assets with utility premium: primarily BTC, conceptually gold, and in extreme cases sovereign reserve assets.

None of these frameworks produce revenue-anchored market caps. All produce market caps anchored to monetary roles within larger economic systems.

This is a multi-trillion-dollar repricing. In the last cycle, competitive pressure dragged ETH down to Tier 2 valuation logic. CLARITY lifts ETH up to Tier 1 valuation logic—by establishing competitors no longer belong in that reference frame.

It also resolves a contradiction plaguing ETH for years. Since L2 rollups feeding value capture back to L1 ETH was considered theoretical and contentious, the base layer L1’s value remained undervalued relative to active L2 ecosystems.

In the new framework, this matters less. ETH’s value isn’t anchored to L2 fee capture. It’s anchored to its role as the sole programmable digital commodity.

L2 ecosystems extend ETH’s economic reach without diluting its currency premium—because currency premium derives from regulatory classification—not fee income.

Measuring the Currency Premium Capital Pool Size

The phrase “multi-trillion-dollar repricing” warrants deep unpacking—because the difference between Tier 1 and Tier 2 valuation frameworks isn’t about multiple size. It’s about the underlying market size the asset competes for.

Cash flow valuation anchors to network fee revenue—currently low single-digit billions annually for ETH. Applying any reasonable multiple implies market caps in the hundreds of billions.

Currency premium valuation anchors to a completely different—and vastly larger—dimension.

Gold is the clearest benchmark. Global above-ground gold supply totals ~244,000 metric tons—valued at ~$32.8T at current prices. Industrial demand accounts for only a tiny fraction.

The overwhelming portion is pure currency premium: its value exists because gold preserves purchasing power across centuries—something fiat, sovereign bonds, and most other financial instruments cannot do.

Gold pays no yield. It generates no cash flow. Yet it sustains a $32T valuation—because markets assign currency premium to assets that credibly preserve wealth regardless of utility.

Gold’s currency premium function carries operation friction costs often underestimated. Physical gold requires assay at each transaction. Gold bars need purity and weight testing. Coins require authentication. LBMA Good Delivery standards exist precisely because counterparty trust in gold quality can’t be assumed without institutional-grade infrastructure.

Retail gold trades typically command 2%–5% premiums over spot to compensate for assay and distribution costs. Cross-border transfers require customs declarations, security, and transport insurance.

Paper gold (ETFs, futures, allocated/unallocated accounts) solves authentication—but reintroduces counterparty risk—and breaks the bearer-asset property motivating initial gold holding. The gap between paper and physical gold is the gap between trusting institutions—and not trusting them—a point critical in the next section.

Real estate is where more interesting analysis begins. As of early 2026, global real estate is valued at ~$393T—the world’s largest asset class. Residential property accounts for $287T, agricultural land another $48T, remainder commercial.

Real estate has three distinct value layers that must be separated. Use value is what you pay for housing or productive land. Cash flow value is what you pay for rental income or agricultural output. Currency premium is what you pay on top—because the asset preserves wealth and resists inflation erosion.

Real estate’s currency premium portion explains why premium properties in Manhattan, London, Hong Kong, and Tokyo trade at 2%–3% cap rates. Rental income alone can’t support these prices. Implicit wealth storage function is the logical underpinning.

A reasonable estimate is 30%–50% of global real estate value ($120T–$200T) represents currency premium—absorbed into real estate by default—not because it’s the optimal vehicle—but because no large-scale alternative existed.

This absorption occurred because no scalable alternatives existed. Wealth needed a home—and for most of modern history, the only options absorbing global liquidity were gold, equities, sovereign bonds, and real estate.

Equities are cash flow assets. Bonds carry sovereign credit risk. Gold’s market is too small to absorb all overflow. Real estate absorbed the remainder by default.

Asymmetric holding costs make this capital sedimentation increasingly fragile. In the U.S., property tax runs 1%–2% annually—higher in some jurisdictions. Maintenance adds another 1%–2% annually. Insurance costs surge amid climate-related repricing.

Total holding cost sits at ~2%–4% annually—before accounting for vacancy, repair shocks, or management fees.

Transaction friction exacerbates holding cost issues. U.S. residential transactions incur 7%–10% bidirectional friction—factoring in broker commissions, transfer taxes, title insurance, and closing fees.

International friction is often higher—UK stamp duty on high-value or second homes hits 12%–17%; Singapore’s additional buyer stamp duty for foreigners reaches 60%.

Liquidity windows run 30–90 days in good markets—and much longer in bad ones. Price discovery is opaque. Lots are large and indivisible.

For decades, real estate’s currency premium function was subsidized by enduring these operational frictions. When no alternatives existed, this didn’t matter. But once alternatives emerge, everything changes.

Wealth Migration in Progress

The currency premium capital pool isn’t static. Wealth is actively migrating between pools in response to two interrelated dynamics becoming visibly apparent over the past decade: declining institutional trust and rising geopolitical tensions.

Institutional trust has declined across multiple dimensions. Edelman Trust Barometer consistently shows institutional trust in most developed economies at or near historic lows.

Geopolitical tensions accelerated this trend. The 2022 freezing of Russia’s central bank reserves was a watershed moment for sovereign asset managers. Recognizing dollar-denominated reserves held in Western financial infrastructure depend on political alignment shifted risk preferences for every non-aligned central bank.

This response manifests measurably across three asset classes.

Central banks’ gold buying is the most visible response. In 2025, global central banks net purchased over 700 tonnes—highest annual increment since 1967.

As of end-2025, the People’s Bank of China had been a net buyer for 14 consecutive months—reportedly holding 2,308 tonnes in foreign reserves. India followed suit.

Beyond buying, multiple central banks moved to repatriate physical gold held in overseas vaults. Germany repatriated half its gold reserves from New York and Paris between 2013–2020. Poland, Hungary, the Netherlands, and Austria took similar actions.

This pattern signals responding to declining institutional trust isn’t just about holding more gold—but explicitly holding gold outside institutions that could fail or be weaponized.

Bond market movements are larger—but less discussed. For nearly 80 years, U.S. Treasuries effectively served as a currency premium asset.

The global financial system’s designation of “risk-free rate” effectively declared U.S. Treasuries the ultimate store-of-value for dollar wealth. Governments, large corporations, and HNWIs allocate trillions to Treasuries—not for yield—but because they represent the deepest, most liquid, and most institutionally trusted store-of-value channel globally.

U.S. Treasury market outstanding stands at ~$39T—with overseas holdings ranging $8.5T–$9.5T depending on methodology.

Within this overseas pool, asset rotation trends are evident. China’s U.S. Treasury holdings peaked at $1.32T in November 2013—but fell to ~$760B by early 2026—a 42% decline.

The People’s Bank of China and major state-owned banks’ moves are interpreted as “orderly liquidation” of U.S. Treasury positions—accelerated in early 2026 by explicit policy guidance. Similar patterns occurred among other major sovereign holders—though less overtly directed.

The PBOC’s simultaneous reduction of U.S. Treasuries and increase in physical gold is the clearest cross-asset rotation example: reducing U.S. Treasury exposure while buying gold for 15 consecutive months.

The dollar’s share of global foreign exchange reserves tells the same macro story. By Q3 2025, the dollar’s share of disclosed global FX reserves fell to 56.92%—down from a 2001 peak of 72%.

This decline is gradual but persistent. A 2025 Fed analysis noted dollar market share losses were absorbed primarily by smaller currencies (AUD, CAD, CNY)—not gold (except China, Russia, Turkey).

This is a crucial insight: de-dollarization is real—but its impact is often overstated. Current trends reflect diversification—not wholesale abandonment—with the dollar retaining absolute dominance.

Yet 20-year data shows a consistent trajectory—and underlying drivers (fiscal deficits, monetary weaponization risk, structural deficits) remain unaddressed.

The third response is the rise of digital currency premium assets as the fourth major wealth reservoir. Bitcoin has already absorbed this overflow.

Since 2017, Bitcoin’s core thesis has been: BTC offers a gold-alternative for digital-age currency premium—and markets are progressively validating this. BTC’s market cap now stands at ~$2T—achieved in just fifteen years from zero.

The rise of Bitcoin treasury companies, spot ETF inflows, and recent corporate adoption reports all map to the same underlying logic: currency premium is seeking a digital-age home—one solving real estate’s high holding costs, gold’s assay friction, and traditional finance’s heavy institutional dependence.

This asset migration isn’t theoretical. It’s an ongoing, multi-decade, multi-asset reallocation already visible in central bank gold flows, Treasury holdings, and FX reserve composition data.

The core question now isn’t whether pools are shifting—but where the next destination opens.

ETH’s Positioning and Potential Market Size Estimation

Until now, Ethereum was excluded from this category due to regulatory uncertainty and competitive narrative pressure. CLARITY’s implementation removes the regulatory barrier.

As previously noted, once regulatory classification reduces competitor count, competition-based narratives collapse. The remaining core question is: what unique advantages does ETH offer versus traditional currency premium assets?

The answer is ETH is the first candidate currency premium asset combining negative net holding cost (earning yield while held) with institutional independence.

Gold’s holding cost is positive—no yield—and assay friction persists even with institutional packaging.

Real estate offers some rental yield—but high holding costs offset it; faces 7%–17% transaction friction depending on jurisdiction; and is entirely subject to local government property rights enforcement.

Treasuries offer positive yield—but as the 2022 reserve freeze showed, they’re highly dependent on specific issuers.

ETH, by contrast, has near-zero custody cost—and delivers ~3%–4% annualized staking yield—outpacing protocol inflation; transaction costs are in basis points; global instant liquidity exists; cryptographic identity verification eliminates dependence on any institutional infrastructure—or any government’s property regime.

Holding ETH and participating in consensus maintenance delivers positive net yield before asset appreciation—and critically, this asset’s properties remain intact even if individual institutions or nations face crisis.

This combination of advantages is unprecedented. Every prior currency premium asset compromised on solving certain problems.

Gold achieved independence from financial institutions—but carried assay friction and zero yield. Real estate delivered yield—but was jurisdiction-bound and faced high transaction friction. Treasuries offered excellent liquidity and yield—but depended heavily on issuer credit.

ETH is the first asset successfully overcoming all these limitations—and CLARITY’s enactment ensures institutional capital allocators recognize these properties.

The implied potential market size isn’t a prediction—it’s a measurement.

Assuming ETH captures 10% of gold’s current market cap—that’s ~$3T, or 7–10x its current market cap. Capturing 2% of real estate’s currency premium portion (conservatively) yields ~$2.4T. Capturing 5% (optimistically) implies $10T.

Even capturing 1% of foreign Treasury holdings would bring $85B in incremental capital.

All scenarios don’t require ETH replacing gold, real estate, or Treasuries outright. They merely require a small fraction of the massive global currency premium pool—already in motion—to flow over the next decade from slightly clunky traditional vehicles to a superior new destination.

Cash flow valuation frameworks cannot produce numbers of this magnitude. Under traditional logic, Ethereum’s annual fee revenue would need explosive growth—even then, stock-market valuation multiples imply market cap ceilings far below currency premium framework ranges.

This is the fundamental chasm between Tier 1 and Tier 2. Their foundational measurement scales differ entirely. These valuation frameworks don’t bleed into or convert to each other. Any asset’s valuation logic is binary—either/or.

Two key risks warrant special mention.

First, currency premium is reflexive. Markets assign it because they believe it will persist—but that belief can vanish anytime. ETH’s current currency premium status isn’t guaranteed forever; maintaining it requires continuously safeguarding network stability, upholding decentralization, and preserving credible neutrality.

Second, capital migration is slow. Even if a large share of the existing currency premium pool ultimately flows to digital alternatives, this evolution spans decades—not quarters. This profound valuation impact is real—but the path there is absolutely not linear.

This analysis has revealed the target pool’s massive scale—and identified the established direction of capital flow.

In the last market cycle, ETH’s valuation benchmark was fee revenue and total value locked (TVL)—both often capping its market cap at a few hundred billion dollars.

CLARITY liberates Ethereum from this constraint—elevating its benchmark pool size by two full orders of magnitude. This pool is currently undergoing a multi-decade reallocation—previously benefiting gold, Bitcoin (BTC), and—to some extent—certain global reserve currencies.

This is the core significance of this valuation framework reshaping.

Risk Factors

Three scenarios could weaken—or even invalidate—the above framework.

The bill may fail to pass. Polymarket odds of passage in 2026 stand at ~75%, with hearings scheduled for Thursday—but political obstacles remain around missing ethics provisions.

Since mid-2025, the decentralization framework has maintained broad consistency across House and Senate versions. The 49% threshold may adjust—but the five-element structure’s substantive change is highly unlikely.

If the bill is fully rejected, this analysis’s structural arguments weaken severely. But as long as it passes in any recognizable form, the framework holds.

Solana may achieve certification. If the Solana Foundation undertakes aggressive reforms during the four-year transition—foundation restructuring, validator decentralization, treasury reallocation—ETH could lose absolute dominance in the “decentralized programmable platform” category.

But as explored above, certification alone wouldn’t elevate SOL to Tier 1 valuation—because Solana’s ecosystem positions it on cash flow, and its network design prioritizes throughput over the high reliability currency premium depends on.

Nonetheless, successful certification would significantly narrow its gap with ETH—especially in institutional investment access and ETF inflow competition. Solana’s governance decisions over the next 24 months will be critical for approval likelihood—and any ecosystem shift in asset valuation framework stance.

Even if a category permits currency premium, markets may not blindly follow. Regulation merely creates space for valuation frameworks—it doesn’t force market adoption.

If institutional analysts cling to traditional valuation models, ETH—even passing all tests perfectly—may still trade on cash flow logic.

While gold, BTC, and select reserve currencies have proven currency premium acceptance—and ETFs, custody, and prime brokerage infrastructure stand ready to provide Tier 1 treatment for qualified assets—this isn’t an automatic transition.

ETH still faces structural challenges: L2 fragmentation, staking economics some argue undervalue L1 ETH, conservative development pace frustrating developers, and underwhelming deflationary mechanisms.

None are solved by CLARITY. Its role is removing two largest structural mountains—and eliminating competitors dragging ETH’s valuation framework downward. It doesn’t make Ethereum perfect.

Where Next?

Its immediate impact is limited. No tokens auto-delist. No overnight reshuffling. No forced capital movement. The SEC has 360 days to finalize rules defining “common control” in practice. The four-year transition gives projects ample time for structural adjustments.

The first wave of certifications and rejections won’t begin until 2027.

Framework shift may accelerate far faster than regulatory implementation. Within months, asset managers, ETF issuers, custodians, and bank-affiliated funds will begin adjusting internal asset classification and allocation frameworks.

Mainstream sell-side firms are expected to publish first reports declaring “ETH is the only programmable digital commodity” within weeks. Narrative building doesn’t wait for regulatory completion—it needs only a compelling regulatory signal.

Historically, crypto markets react ahead of regulatory clarity. BTC ETFs traded for two years before approval. ETH ETF approval news was priced into spot months ago. Major regulatory tailwinds are often digested early.

For holders and traders, the core question isn’t whether the bill becomes law on July 4—or in 2027. It’s whether markets will front-run—and position ahead of the profound implications this regulation’s finalization brings.

The underlying logic supporting ETH valuation is quietly undergoing a transformation—from “smart contract platform burdened by regulatory compliance risk” to “unique programmable digital commodity with currency premium potential.”

This massive shift hasn’t yet been fully reflected in price.

For five years, holding ETH meant enduring dual structural pressures: regulatory uncertainty and risk of competitors overtaking it.

Thursday’s upcoming bill hearing promises to dispel both clouds—and more critically, zero out ETH’s direct competitors.

Markets will realize this eventually. The only remaining question is timing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News