BlackRock's Latest Proposal: Differences Between SEC-Preferred Cash Redemption Model and In-Kind Redemption Model for Spot Bitcoin ETF

TechFlow Selected TechFlow Selected

BlackRock's Latest Proposal: Differences Between SEC-Preferred Cash Redemption Model and In-Kind Redemption Model for Spot Bitcoin ETF

Cash Creation Method, which is the redemption method preferred by the U.S. Securities and Exchange Commission (SEC).

By Aiying

BlackRock, ARK Invest, and WisdomTree submitted revised proposals for spot Bitcoin ETFs yesterday, adopting the cash creation method—a redemption approach preferred by the U.S. Securities and Exchange Commission (SEC). This shift marks a significant industry transformation and may signal that discussions around in-kind redemption options will be postponed, serving as a strategic move to streamline operations before the Christmas holiday. Whether using in-kind or cash redemption, spot Bitcoin ETFs hold Bitcoin as their underlying asset; the key difference lies in the redemption process. The SEC favors the cash redemption model because it ensures only the issuer handles Bitcoin, avoiding situations where unregistered broker-dealer subsidiaries would need to transact in Bitcoin.

However, the cash redemption model involves actual cash flows in Bitcoin ETFs, which could trigger tax liabilities such as capital gains taxes, as these are treated as real buying and selling activities. In contrast, the in-kind redemption model directly exchanges Bitcoin for ETF shares without any inflow or outflow of cash, making tax treatment simpler and potentially avoiding tax burdens arising from cash transactions. Below is an explanation of these two redemption models:

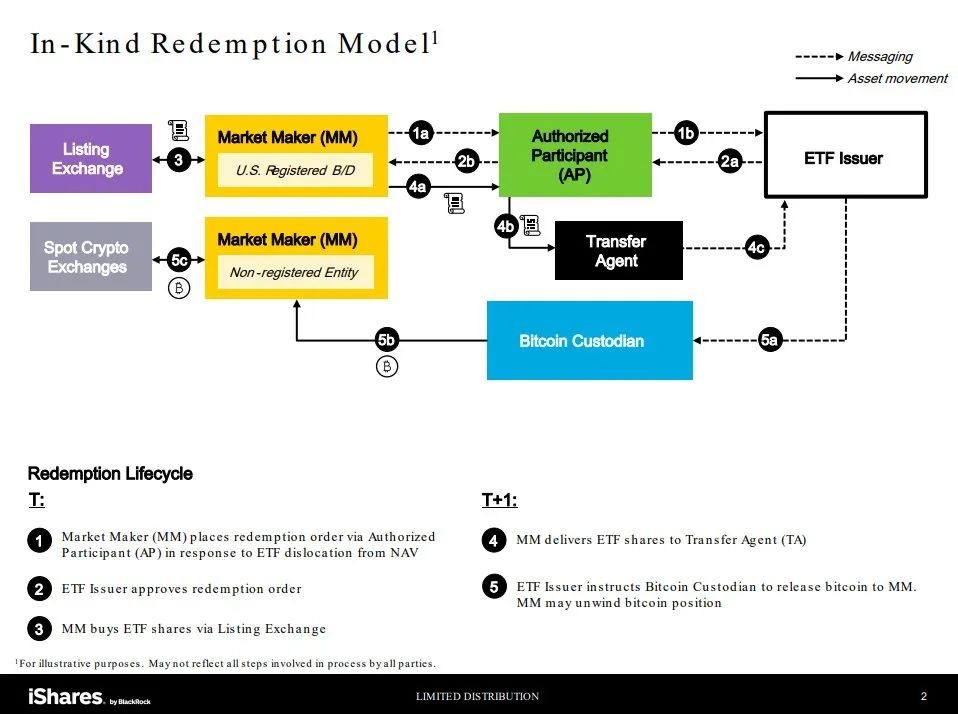

In-Kind Redemption Model

-

Market Maker (MM): Liquidity providers in the market. They are either registered U.S. securities brokers/dealers subject to securities regulations, or unregistered entities not overseen by regulatory authorities.

-

Authorized Participant (AP): Financial institutions authorized to create and redeem ETF shares, typically done in large blocks known as "creation units."

-

Listed Exchange: The platform where ETF shares are traded.

-

ETF Issuer: The company managing the ETF.

-

Transfer Agent: A third party responsible for handling transfers of ETF shares.

-

Bitcoin Custodian (e.g., Coinbase): Entity safeguarding the ETF’s Bitcoin assets.

-

Spot Cryptocurrency Exchange: Where immediate delivery of Bitcoin transactions occurs.

Process on Trading Day (T-Day):

A market maker requests redemption of ETF shares from an authorized participant, especially when the ETF price deviates from its net asset value (NAV). After approval by the ETF issuer, the market maker receives shares eligible for redemption.

On the next business day (T+1), they surrender these shares, and the Bitcoin custodian releases Bitcoin to them, which can then be sold on the spot market. This mechanism helps maintain alignment between the ETF price and Bitcoin's market value.

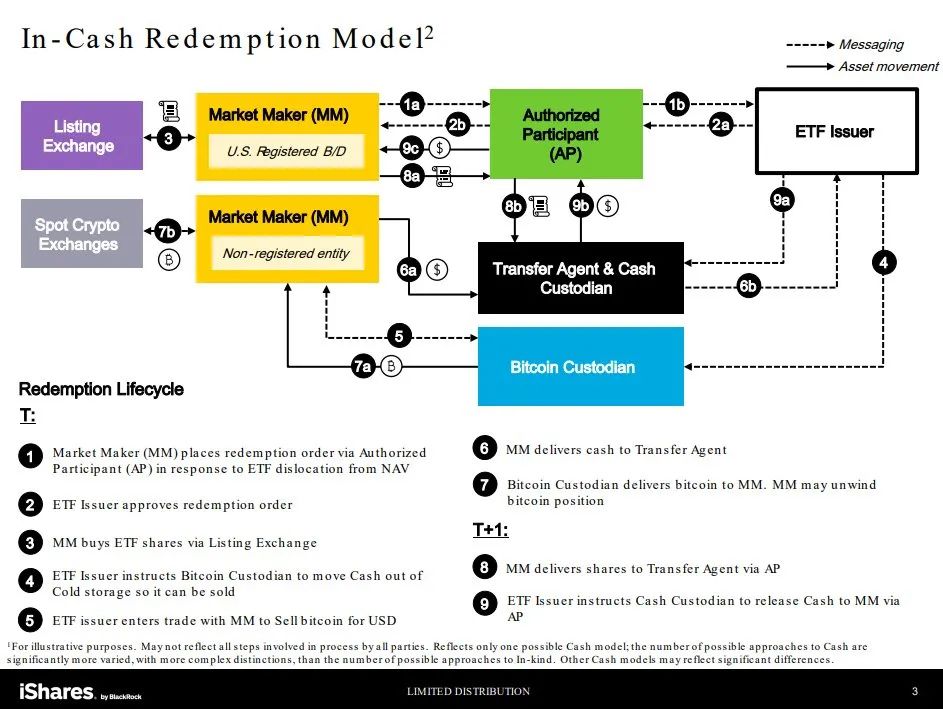

Cash Redemption Model

-

Redemption Order Submission: Market makers, whether registered or not, submit orders to authorized participants to redeem ETF shares at prices below NAV, aiming for arbitrage opportunities.

-

Order Approval: The ETF issuer approves the redemption request.

-

Purchase of ETF Shares: The market maker buys shares through the listed exchange.

-

Cash Movement Instruction: The ETF issuer instructs the Bitcoin custodian to prepare cash from cold reserves for sale.

-

Transaction with ETF Issuer: The issuer directly trades Bitcoin for U.S. dollars with the market maker.

-

Cash Delivery to Transfer Agent: The market maker delivers cash to the transfer agent.

-

Bitcoin Delivery: The custodian sends Bitcoin to the market maker, who may sell it to realize arbitrage profits.

-

Share Delivery and Cash Release (Next Day): The market maker delivers shares to the transfer agent, and the issuer releases cash to complete the process.

The SEC’s preference for the cash redemption model may also stem from several additional considerations. First, the cash redemption model is operationally simpler, making the regulatory process more direct and transparent, thus facilitating effective monitoring and auditing by regulators. Second, this model reduces the risk that large-scale redemptions or purchases could directly impact Bitcoin’s market price, thereby minimizing the potential for market manipulation. Additionally, cash redemption allows for better management of liquidity risk, offering greater flexibility and stability, especially during periods of high market volatility. Finally, with investor protection in mind, the SEC believes the cash redemption model can more effectively shield investors from the direct impacts of price fluctuations in the underlying asset—particularly important in the highly volatile cryptocurrency market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News