HODL on, and merry crypto Christmas to you!

TechFlow Selected TechFlow Selected

HODL on, and merry crypto Christmas to you!

For this wonderful life, hold strong!

Source: Bloomberg

Translated by: Yanan, BitpushNews

Cryptocurrencies have not only survived the collapse of FTX but have become one of this year’s hottest investment themes. It turns out decentralized finance doesn't need exchanges.

Merry Crypto Christmas! Bitcoin is up 167% this year, and Ethereum has risen 91%. If you predicted these gains a year ago, I salute you. In terms of return on investment, crypto assets have significantly outperformed other asset classes. The Nasdaq Index rose 36%, the S&P 500 gained 19%, and gold increased by 10.7%. If you bet on oil or commodities, your returns might be down 10% to 12%.

A year ago, many of us—including myself—believed the game was over for cryptocurrencies, and that skeptics would be proven right.

Sam Bankman-Fried’s fall wasn’t shocking news. He has now been sentenced to prison on seven counts of financial fraud, and his exchange, FTX, no longer exists. The fate of rival Binance hung in the balance after an investigation by the U.S. Department of Justice. Binance’s founder, Changpeng Zhao, admitted to anti-money laundering violations, stepped down as CEO, agreed to pay a $50 million fine, and Binance itself was fined $4.3 billion.

At that time last year, the scandal storm surrounding crypto exchanges convinced me that blockchain-based finance was fundamentally flawed, and that I should immediately sell most of the Bitcoin, Ethereum, and other tokens I had accumulated since becoming a crypto believer in 2017.

I was a fool. I forgot the first rule of crypto investing: Once you buy, you should always HODL—Hold On for Dear Life!

How wrong my decision to sell at the bottom (SATB) was can be seen in the transformation of Nouriel Roubini—the well-known economist who predicted the 2008 financial crisis and has long criticized cryptocurrencies and blockchain technology, frequently questioning the sustainability, security, and value of Bitcoin and other digital currencies. Just a year ago, he was gloating over the demise of all “shitcoins,” but now he is launching his own blockchain-based “flatcoin.”

The past 12 months have made it clearer than ever that crypto exchanges or other custodial intermediaries are not, and never were, central to the future of blockchain fintech.

Let’s not forget: the original vision was peer-to-peer transactions without banks or other intermediaries, and without state surveillance. Looking back, the era when crypto was dominated by exchanges never should have existed, because such centralized platforms contradict the core idea of decentralized finance.

Exchanges emerged simply because the technical difficulty of directly exchanging cryptocurrencies between participants without intermediary platforms was extremely high. Early adopters used a site called LocalBitcoins, which functioned like Craigslist. Users posted ads to buy or sell Bitcoin and then chose their preferred payment method. Although crypto transactions still involve some complexity—I’ve had my frustrations using Ledger and MetaMask—the process is gradually becoming easier.

However, the critical steps of depositing and withdrawing funds are now almost entirely controlled by regulated exchanges. Coinbase appears to be both a survivor and a winner amid the wave of scandals. Because the link between traditional finance and decentralized finance remains monopolized by a few major platforms, the crypto industry remains risky.

The sustained rally in BTC and ETH over the past year teaches us three things:

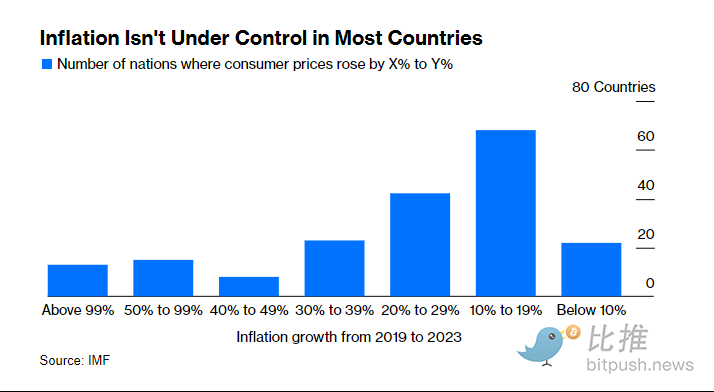

First, after two decades of historically low inflation, the world is now suffering from the consequences of poorly managed fiat currencies, and interest in cryptocurrencies will inevitably grow. According to the International Monetary Fund, among 191 countries with available data, only 22 have seen consumer prices rise less than 10% since 2019. Another 68 countries saw inflation between 10% and 19%; 42 between 20% and 29%; 46 between 30% and 99%; and sadly, 13 countries experienced price increases exceeding 100%. That number would be higher if we had reliable data for Lebanon and Syria this year.

In Argentina, consumer prices have risen eightfold in four years; in Sudan, 103-fold; in Zimbabwe, 159-fold; and in Venezuela, more than 5,000-fold.

The worse the inflation, the greater the appeal of cryptocurrencies. The mood in Argentina speaks volumes. Last Sunday, libertarian economist Javier Milei was sworn in as president. Unlike my crypto investments, this was something I got right this year: I spent the entire year telling my Argentine friends that when inflation hits 100%, voters will choose radical solutions over mainstream ones.

Milei’s radicalism borders on obsession. He sports a rock-star hairstyle reminiscent of 1960s icons—almost as if he stepped off a Yardbirds album cover. His presidential staff is silver-embossed with engravings of his five English mastiffs and their names: Conan (named after his previous dog, from whom all five were cloned), Milton (after Chicago free-market economist Milton Friedman), Murray (after Austrian-influenced libertarian Murray Rothbard), and Robert and Lucas (after another giant of the Chicago School, Robert Lucas).

Some English-language media mistakenly equate Milei with right-wing populists like Brazil’s Jair Bolsonaro. Milei belongs to a completely different category. Amid rising global antisemitism, he announced plans to convert to Judaism and chose a modest Hasidic rabbi’s gravesite in Queens as the destination of his first overseas visit as president.

In his inaugural address, Milei told the crowd: “We have no choice but massive fiscal adjustment,” warning them of an impending recession. The crowd responded: “Motosierra! Motosierra!” (“Chainsaw! Chainsaw!”)—a nod to his promise to cut public spending. Milei told them: “There is no money.” And the crowd cheered. His proposed budget-balancing plan is the boldest shock therapy the world has seen since Margaret Thatcher became Prime Minister of the UK.

Yet someone explained to Milei that his cherished goal—replacing Argentina’s currency with the U.S. dollar—is unfeasible. The Central Bank lacks sufficient dollars, and any talk of dollarization could plunge the already collapsing peso into hyperinflation. As a result, Argentines paid and saving in pesos would inevitably see further devaluation—indeed, depreciation has already begun since last week.

At such a moment, wouldn’t every Argentine want to hold some Bitcoin?

The second lesson is that cryptocurrencies have evolved.

The first crypto bull run was driven almost entirely by faith in Bitcoin’s technology—the belief that Bitcoin could become censorship-resistant digital cash. That cycle was interrupted in 2011 by the first major hack of the Mt. Gox exchange, which lost about 25,000 bitcoins. Although Bitcoin quickly recovered, the era ended in 2013 and 2014 as the FBI shut down the Silk Road darknet market and Mt. Gox—handling 70% of Bitcoin transactions at the time—collapsed.

The second bull market began around 2016, fueled primarily by the Initial Coin Offering (ICO) frenzy on the Ethereum network. ICOs were speculative sales of tokens by crypto teams to retail investors, promising to build smart contract blockchains superior to Ethereum. But when it became clear that these blockchain projects had almost no “useful” activity, the industry plunged into another winter.

The 2020 bull market seemed to answer criticisms about crypto’s lack of utility. Starting with “DeFi Summer,” waves of decentralized autonomous organizations (DAOs) and non-fungible tokens (NFTs) followed. Now, crypto networks appear to be attracting real users—both retail and institutional—though much of the activity remains highly speculative, risky, and often leveraged. It was precisely this excessive risk and poor financial engineering that led to the failures of projects like Terra and the collapse of funds like Three Arrows Capital.

Today, the total value locked (TVL) in DeFi smart contract protocols is roughly where it was in 2022. But according to analysis by Manny Rincon-Cruz, a researcher at the Hoover Institution, this figure actually reveals a shift—from high-risk tools toward safer, bond-like assets.

During the 2020 bull market, the most-used DeFi protocols were margin lending platforms and decentralized exchanges. Today, DeFi is dominated by yield-generating assets—not just interest-bearing lending positions, but also tokenized real-world assets like Treasury bills.

But today’s most important yield-generating assets are liquid staking protocols—essentially ways for users to delegate their tokens to validate and secure blockchain networks. For example, users can deposit their Ethereum into the Lido protocol, which delegates block-building work on the network to Ethereum validators, earns transaction fees, and redistributes them to users. (Liquid staking is roughly analogous to Bitcoin users participating in Bitcoin mining.) Today, the largest liquid staking protocols account for 56% of DeFi TVL—up from just 0.1% in early 2021.

It's unclear what consequences this focus on yield may bring, but in 2024 and 2025, the crypto industry is likely to continue developing more useful, less speculative peer-to-peer protocols.

The third lesson of 2023 is that despite efforts by regulators and lawmakers to stop it, traditional finance continues to adopt cryptocurrencies.

This year, asset managers including Franklin Templeton and BlackRock, along with Grayscale—one of the earliest players in the space, having launched the first OTC Bitcoin fund in 2013—filed applications with the U.S. Securities and Exchange Commission (SEC) for Bitcoin and Ethereum exchange-traded funds (ETFs). Grayscale applied in 2017 to convert its Bitcoin Trust into an ETF but withdrew the application after negative feedback from the SEC. Now, the SEC keeps extending its response deadlines, suggesting it cannot find strong enough grounds to reject these ETF applications.

Meanwhile, the Financial Accounting Standards Board (FASB) recently issued new cryptocurrency accounting rules requiring U.S. companies holding crypto assets to record their tokens at current market prices—or “fair value.”

One major reason crypto was prematurely declared dead was the so-called “lack of adoption.” In the 2018 revised edition of *The Ascent of Money*, I made this argument—and should have stuck to it:

Bitcoin is portable, liquid, anonymous, and scarce. By design, it is “digital gold.” A moment’s reflection shows that $6,000 is still cheap for this new store of value. So far, about 17 million Bitcoins have been mined. According to Credit Suisse, there are 36 million millionaires globally, with combined wealth of $128.7 trillion. If they collectively decided to allocate just 1% of their wealth to Bitcoin, the price would exceed $75,000—higher still when considering lost or hoarded coins. Even if they allocated only 0.2%, Bitcoin would trade around $15,000.

That range prediction was almost exactly right. In November 2021, Bitcoin peaked at $63,621. A year later, it bottomed at $15,460. Today’s price of around $40,000 is roughly the midpoint.

If you believe, as I do, that law-abiding citizens should not be presumed to surrender their transactional activities to government scrutiny, then you should welcome Bitcoin’s growing adoption.

These days, we hear a lot about the First Amendment—the constitutional feature Harvard students recently discovered while studying anti-Israel slogans—not to mention the Second Amendment, frequently invoked at Republican primaries. But freedom of speech and the right to bear arms weren’t the only liberties the Founders cared about.

The Fourth Amendment states:

“The right of the people to be secure in their persons, houses, papers, and effects, against unreasonable searches and seizures, shall not be violated, and no Warrants shall issue, but upon probable cause, supported by Oath or affirmation, and particularly describing the place to be searched, and the persons or things to be seized.”

One of the most compelling papers I read this year was “Electronic Cash, Decentralized Exchange, and the Fourth Amendment” by Peter van Valkenburgh of Coin Center.

Valkenburgh argues that the erosion of our Fourth Amendment rights began with the Currency and Foreign Transactions Reporting Act of 1970. This law, along with its amendments and related regulations, collectively known as the Bank Secrecy Act (BSA), requires banks to keep records of large cash purchases, file reports on cash transactions exceeding $10,000 per day, and report suspicious activities believed to involve money laundering. U.S. financial institutions must submit Currency Transaction Reports and Suspicious Activity Reports (SARs). Banks are compensated for compliance.

To some, this legislation clearly violates the Fourth Amendment. Justice William O. Douglas wrote in dissent: “I am not yet prepared to agree that the United States has been so far led astray by evil forces that it must embark on a course designed to remove all constitutional obstacles to the detection and punishment of crime.”

But Douglas—a progressive deeply committed to civil liberties—was in the minority. The BSA was upheld by the Supreme Court in *California Bankers v. Shultz* (1974) and *United States v. Miller* (1974), establishing the principle that financial information handed to third parties like banks is no longer private.

Today, this third-party doctrine is being challenged, as our electronic data now resides with another kind of third party: Big Tech companies. Since *Carpenter v. United States* (2018), for instance, the government needs a warrant to access individuals’ mobile location history.

Nevertheless, as cash transactions decline and post-9/11 governments intensified financial surveillance, the scope of the BSA has expanded. SAR filings surged from 60,000 in the 1990s to 3.6 million in 2022.

Blockchain technology poses a fundamental challenge to this financial surveillance regime by enabling truly peer-to-peer transactions. As Valkenburgh acknowledges, Bitcoin isn’t truly “crypto” currency because user identities can still be inferred from immutable ledger records.

However, innovations like Tornado Cash are making genuinely anonymous peer-to-peer transactions possible. Unless software developers themselves act as third parties collecting user data, no third party is involved in the transaction process.

Valkenburgh concludes: “As the world increasingly shifts toward fully intermediated and surveilled payment technologies like Alipay, WeChat Pay, or so-called central bank digital currencies (CBDCs), truly decentralized finance is essential for preserving human dignity and autonomy. Anonymous electronic cash and decentralized exchange software are the ultimate goals of all cryptocurrency networks.”

You don’t need to personally know Senator Elizabeth Warren or SEC Chair Gary Gensler to guess they would strongly oppose this view. They and others will inevitably call for imposing BSA compliance obligations on crypto software developers and individual users. Yet under the Fourth Amendment, such actions would clearly be unconstitutional—equivalent to warrantless search and seizure of private information.

The reason government might win this battle is obvious: as long as people like SBF exist, and terrorists can benefit from reckless crypto operators, authorities will continue claiming that while the Fourth Amendment deserves respect, it can be overridden when necessary.

But what the government cannot do—even if JPMorgan CEO Jamie Dimon wishes otherwise—is completely ban cryptocurrencies and restore dwindling U.S. banks’ monopoly over financial transactions.

Once again, happy Crypto Christmas! HODL for this beautiful life—but don’t count on the Fourth Amendment to protect you.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News