Galaxy: The Impact of Large-Scale Wealth Transfer on the Cryptocurrency Market

TechFlow Selected TechFlow Selected

Galaxy: The Impact of Large-Scale Wealth Transfer on the Cryptocurrency Market

Large-scale wealth transfer represents a substantive demographic transformation that will fuel stronger crypto adoption among the digital-native population.

Author: Charles Yu

Translation: Luccy, BlockBeats

Editor's Note: Over the next two decades, millennials will become the primary beneficiaries of a massive wealth transfer. By 2030, their adoption or acceptance rate of cryptocurrency could be at least three times higher than older generations.

Charles Yu, researcher at Galaxy Digital, provides an in-depth analysis of wealth transfer trends in the United States, focusing on the large-scale intergenerational transfer of wealth from Baby Boomers to millennials. The shift from traditional financial systems to cryptocurrencies reflects not only differences in investment behaviors and values between younger and older generations but also presents new opportunities and challenges for the crypto market. This article explores young people’s preference for cryptocurrencies and examines how this trend may profoundly impact the market.

Charles Yu also notes that while the "Great Wealth Transfer" cannot solve all financial problems faced by younger generations, it marks a transition of power and wealth, granting greater autonomy to the digitally native generation.

In the coming decades, older generations will pass trillions of dollars in money and assets to their children, significantly reshaping the landscape of American wealth. These young “digital natives” exhibit markedly different investment preferences compared to their parents’ generation, including a much stronger inclination toward Bitcoin and cryptocurrencies.

Key Takeaways

Millennials are poised to receive the largest intergenerational wealth transfer in history. Although Baby Boomers and older generations make up less than one-third of the U.S. adult population, they collectively hold two-thirds of American household wealth ($96 trillion), more than 11 times the wealth held by millennials and younger generations. Over the next two decades, Cerulli Associates estimates that $84.4 trillion in wealth will transfer from Baby Boomers and older generations to younger ones, with millennials as the primary beneficiaries. Coldwell Banker projects that millennials’ wealth will increase fivefold by 2030 compared to the beginning of this decade, primarily due to inheritance.

Millennials and Gen Z differ significantly from older generations in their attitudes toward cryptocurrency, showing a clear preference for digital assets. As the first generation of digital natives, millennials and Gen Z are more racially diverse, better educated, and more socially conscious than their parents and grandparents. Having experienced multiple economic downturns, high housing costs, and heavy debt burdens, these younger generations are more open to alternative financial systems and investments, including cryptocurrencies. Numerous surveys measuring generational adoption of crypto consistently find that younger generations adopt or accept cryptocurrencies at rates at least three times higher than Baby Boomers.

The transfer of wealth into the hands of crypto-friendly individuals could lead to a significant increase in demand for Bitcoin and other crypto assets. If the Great Wealth Transfer occurred today, we estimate an additional $160 billion to $225 billion would flow into the crypto market based on younger generations’ higher adoption rates relative to Baby Boomers. Given that most of the wealth held by Baby Boomers and older generations is expected to pass to younger generations before 2045, our estimates suggest this wealth transfer could add $20 million to $28 million per day in buying pressure to the crypto market over the next 20 years.

Despite its potential, the wealth transfer may not resolve all financial challenges facing millennials and the next generation. Only a small portion of the population is expected to receive any inheritance. Wealth transfers are unlikely to reach lower-income groups who might benefit most from them. For those expecting inheritances, actual amounts received may fall short due to longer lifespans, rising healthcare costs, poor financial planning, shifting spending priorities, and reduced benefits.

Nevertheless, the demographic shift of wealth and power toward younger generations is inevitable—and this bodes well for cryptocurrencies. Even if the Great Wealth Transfer does not substantially alleviate millennials’ financial burdens, the generational handover from Baby Boomers to younger cohorts will have far-reaching social and political implications—all of which positively influence further adoption and long-term development of cryptocurrencies in the United States.

The Great Wealth Transfer

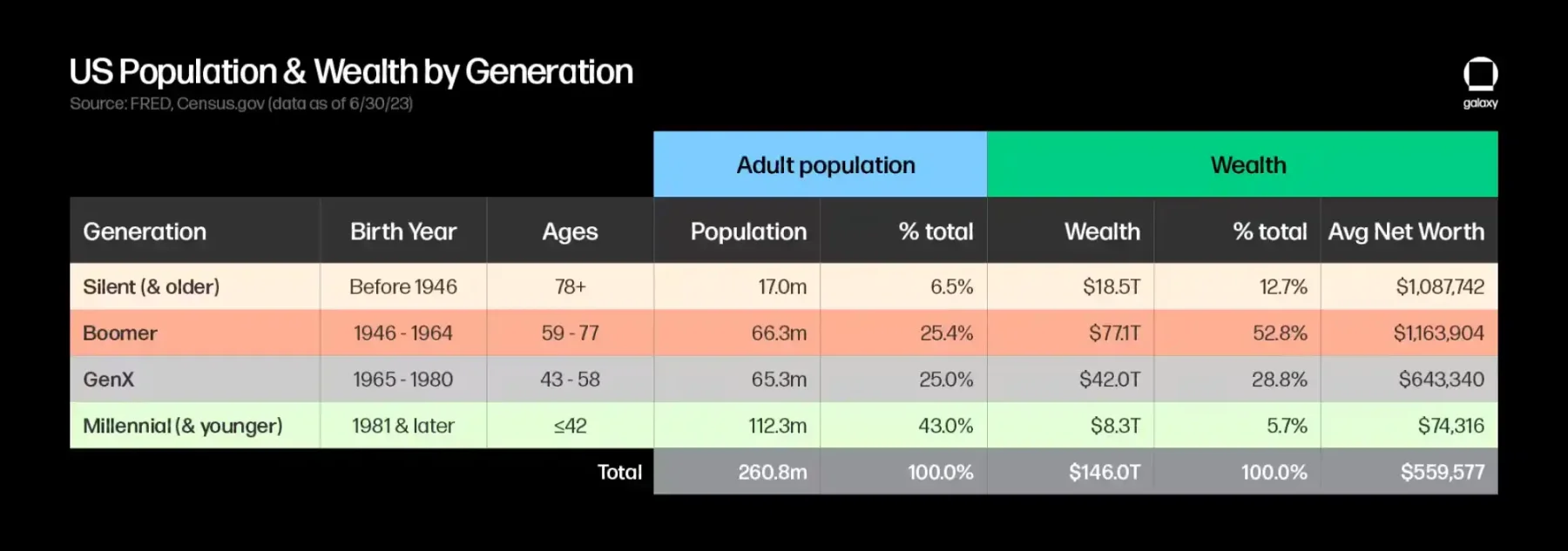

According to the Federal Reserve’s Survey of Consumer Finances, total U.S. household wealth reached $146 trillion as of Q2 2023. Of this amount, Baby Boomers and older generations (born in 1964 or earlier) collectively hold $95.6 trillion—approximately two-thirds of total U.S. wealth—despite comprising less than one-third of the adult population.

In recent years, millennials have surpassed Baby Boomers as the largest generation in the U.S. Despite their numerical advantage, millennials and younger generations (including Gen Z) together hold only $8.3 trillion (about 5.7% of total wealth), roughly 1/11.5th of what Baby Boomers and older generations hold—or about 15.5 times less per capita.

Over the next two decades, millennials are set to be the main beneficiaries of what many call the "Great Wealth Transfer," where older generations pass down trillions of dollars in wealth to their children.

Cerulli Associates predicts that by 2045, transferred wealth will total $84.4 trillion, with $73.6 trillion (87%) going to heirs and $11.9 trillion (13%) donated to charities. Baby Boomers (ages 59–77) are expected to transfer $53 trillion (63% of total), while the Silent Generation (currently aged 78+) is projected to transfer around $16 trillion (19%) over the next decade. Coldwell Banker estimates that by 2030, millennials will hold five times more wealth than at the start of this decade, largely due to inheritance.

Generational Divides

Understanding key differences among these demographic groups and identifying intergenerational trends offers valuable insights for individuals, investors, businesses, and policymakers seeking to understand user behavior, capitalize on market opportunities, or assess policy impacts.

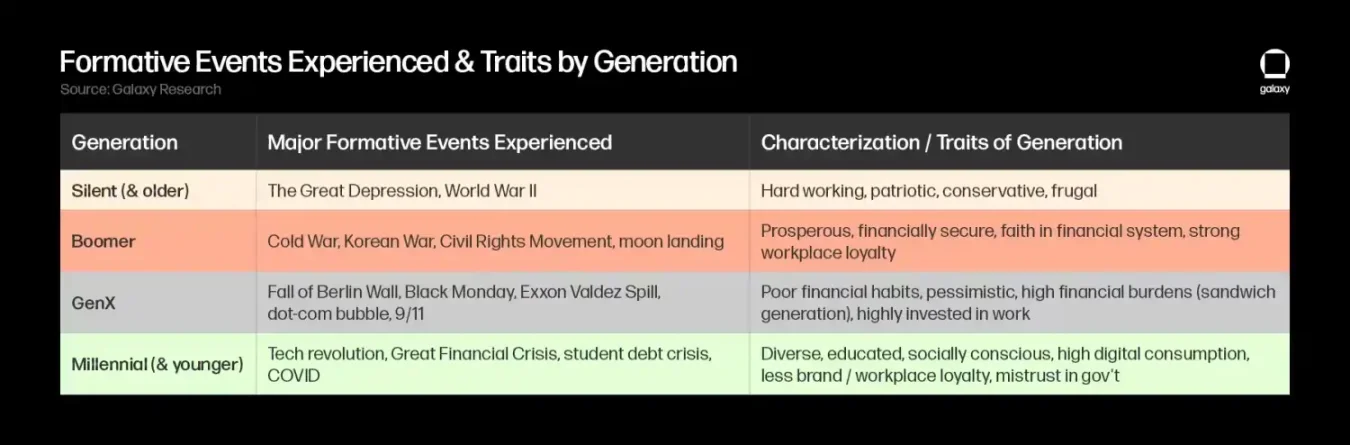

Each generation has experienced formative events and challenges during their upbringing that shaped their core principles and priorities. The Silent Generation came of age during WWII; Baby Boomers lived through post-war global conflicts and civil rights and counterculture movements; Gen X witnessed the fall of the Berlin Wall, inflation spikes in the 70s and 80s, and the dot-com bubble; millennials experienced the Great Recession and launched the Occupy Wall Street movement; Gen Z entered the workforce amid the COVID-19 pandemic. These pivotal life experiences shape how we interact with the world—including our views on work and investment preferences.

In the table above, we outline several key developments during each generation’s formative years, along with certain traits and values associated with each group. Most of these generational characteristics relate to the global political and socioeconomic conditions (e.g., wars, capital markets, labor markets, housing) under which each cohort grew up, while others stem from technological advances or broader trends beyond central banks’ or policymakers’ control (e.g., increased access to information, availability of technology and media, globalization).

Millennials and Gen Z stand out as the first generation raised alongside the internet—the original “digital natives.” Compared to older generations, they are more racially diverse, better educated, and more socially aware. There is also a noticeable generational gap in perceptions: older adults often view younger generations as lazy, arrogant, materialistic, and overly sensitive, while younger people may see elders as out of touch, stubborn, and narrow-minded.

While such stereotypes are debatable, it is undeniable that millennials and younger generations face unique financial difficulties and challenges that earlier generations did not encounter at similar ages—they’ve endured two major economic recessions early in adulthood, alongside rising education and housing costs, all of which affect their ability to save and build wealth:

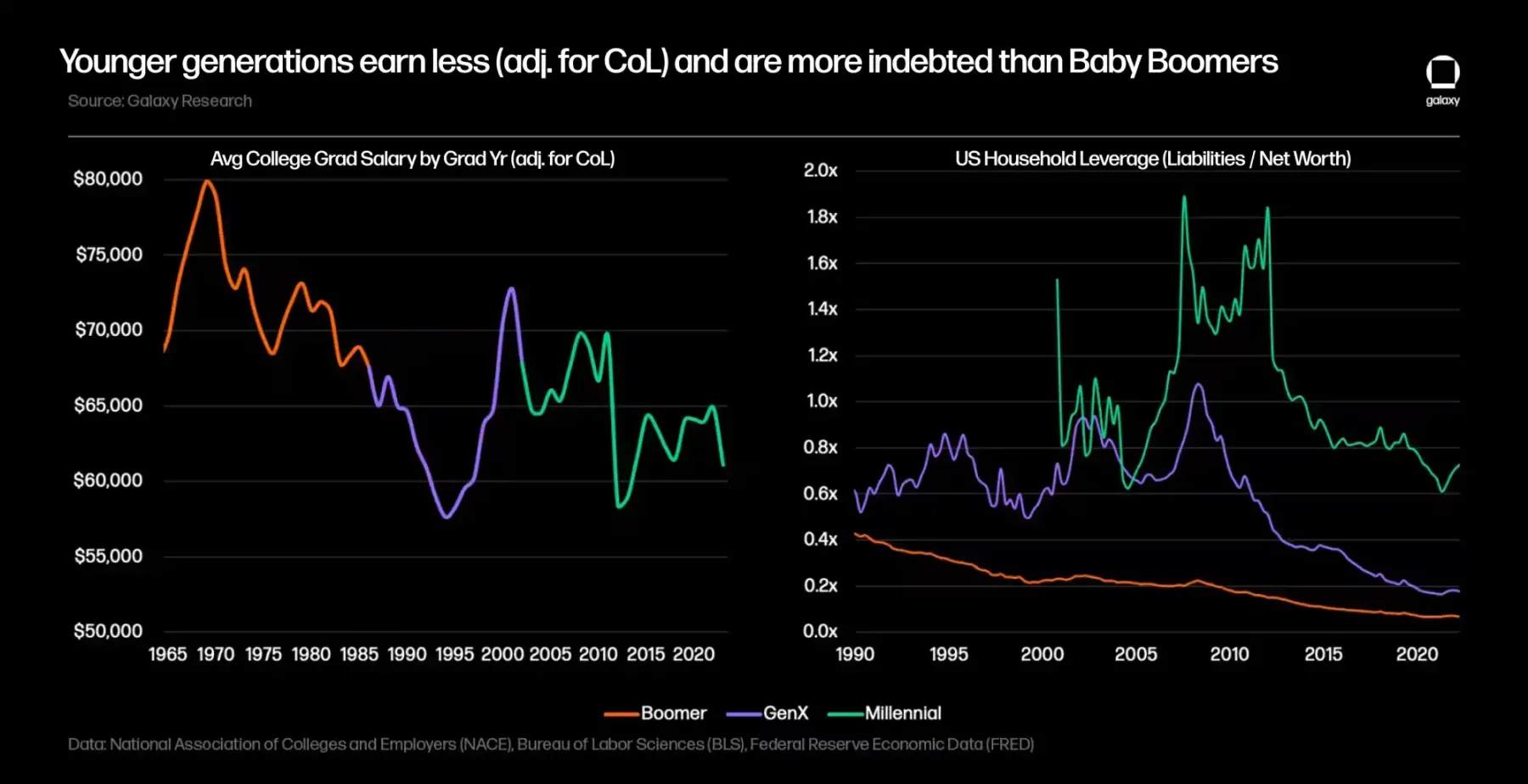

Student loans pose a far greater burden for millennials and Gen Z than for Gen X or Baby Boomers. Not only has the cost of college risen sharply, but tuition increases have outpaced income growth, leading to ballooning student loan balances. From 1982 to 2022, the average cost of attending a four-year university rose from $11,840 to $30,031 (a 153% increase over 40 years). Between 2008 and 2022, student loan debt surged 163% to $1.74 trillion. As of Q3 2023, the number of federal student loan borrowers increased by 45% to 43.5 million Americans, and the average graduate’s student loan debt rose 33% to $37,650. Compared to Baby Boomers at age 30, millennials at the same age are twice as likely to carry student debt (~40% vs ~20%), and their debt-to-income ratio is four times higher (40% vs 10%).

Housing costs have also become relatively more expensive for younger generations (benefiting Baby Boomers whose real estate assets have appreciated). Over the past 40 years, homes have become less affordable as median new home prices have outstripped median household incomes, increasing outstanding mortgage debt and slowing homeownership rates among millennials compared to previous generations (recent interest rate hikes have further worsened affordability). Millennials lag behind older generations in homeownership: in 2022, only 43% of millennials owned a home by age 30, compared to 52% of Baby Boomers at the same age.

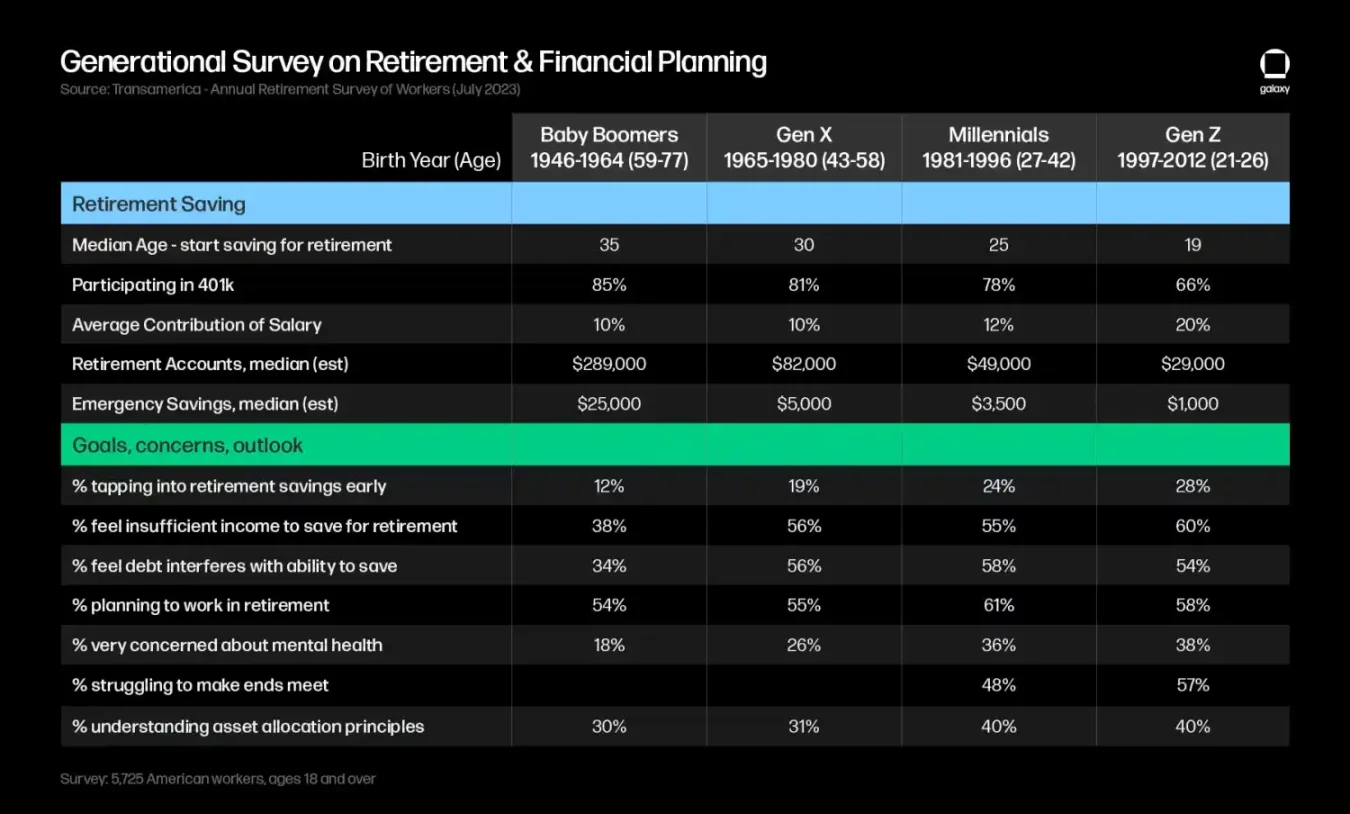

These economic challenges negatively impact millennials’ net worth-to-income ratios, reducing their capacity and willingness to invest or save compared to Baby Boomers at the same age. Higher debt levels delay the onset of investing and reduce savings amounts, potentially affecting risk-taking behaviors. Moreover, traditional retirement income sources have shifted from Social Security and defined-benefit pensions to defined-contribution plans (like 401(k)s), shifting the burden of saving and investment management onto employees. Millennials will be the first generation to retire without widespread access to defined-benefit pension plans, and Social Security may no longer be a reliable retirement income source. According to Transamerica Institute, early withdrawals from retirement savings—such as loans, premature distributions, or hardship withdrawals—are becoming more common among younger generations. The survey also finds that younger individuals are more concerned about their mental health and ability to save for retirement.

Attitudes Toward and Adoption of Cryptocurrency Across Generations

The traditional financial system worked well for Baby Boomers—they enjoyed relatively high incomes, low living costs, and many years of economic prosperity, unlike millennials and younger generations. Consequently, studies show they are more likely to trust the financial system and prefer the status quo.

In contrast, many millennials and younger individuals feel disillusioned with the financial system, believing it fails to meet their needs as it did for their parents and grandparents. Especially after the 2008 financial crisis—which sparked inflation concerns and eroded institutional trust—these digitally native groups are naturally more receptive to alternative financial systems and investments. Compared to older generations, they are more likely to use non-traditional digital brokerage apps and robo-advisors, and show stronger interest in tech, ESG, social impact, and alternative investments.

Therefore, the idea of an alternative financial system—one that enables the use of digital-native currencies outside the control of banks and governments—resonates strongly with this demographic. Bitcoin and cryptocurrencies align with younger generations’ values: a digital-first, accessible, permissionless, privacy-focused, always-on approach to personal finance.

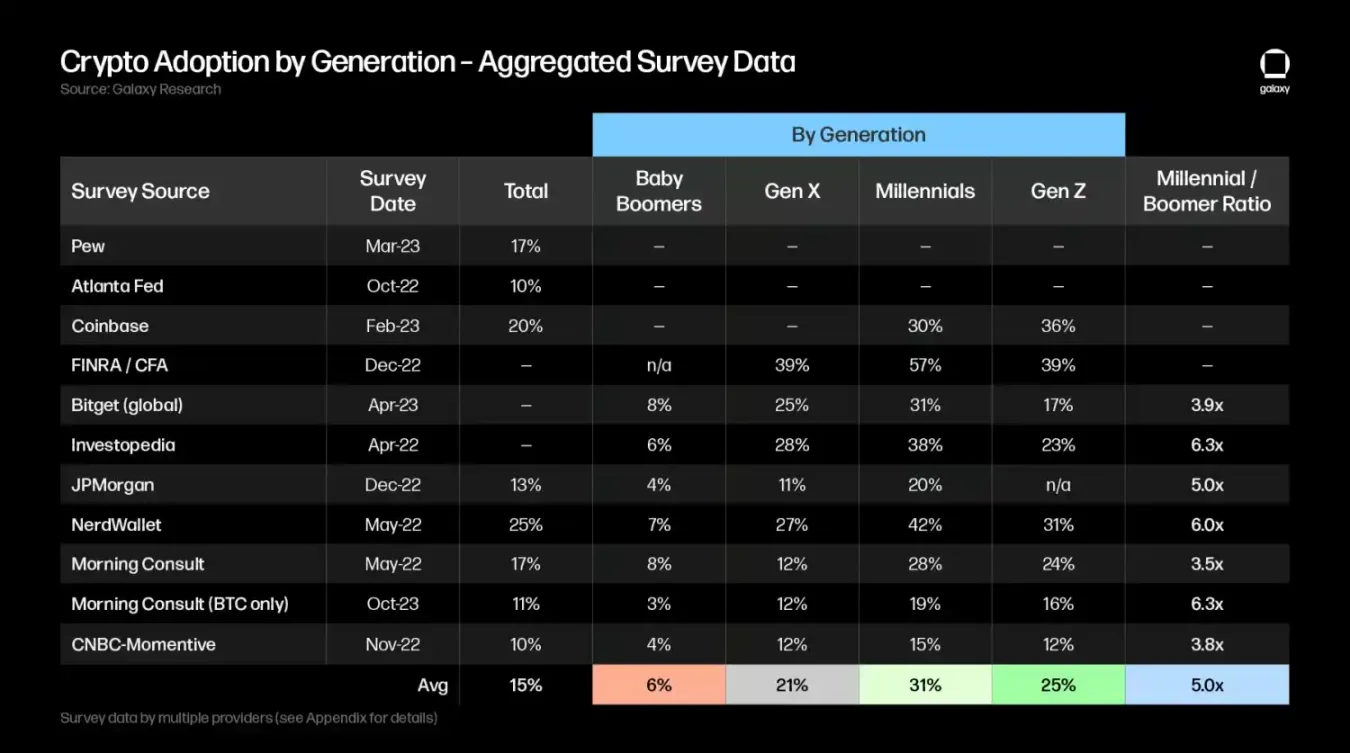

Cryptocurrency Adoption Rates by Generation

Coinbase estimates that 52 million Americans own cryptocurrency (about one-fifth of adults), with millennials having the highest ownership rate (45%), followed by Gen Z (39%). These findings are similar to Pew Research data, which found that 8% of adults over 50 had ever invested in, traded, or used cryptocurrency, compared to 25% of those aged 30–49 and 28% of those aged 18–29—indicating adoption levels among younger adults are three times higher than among those over 50.

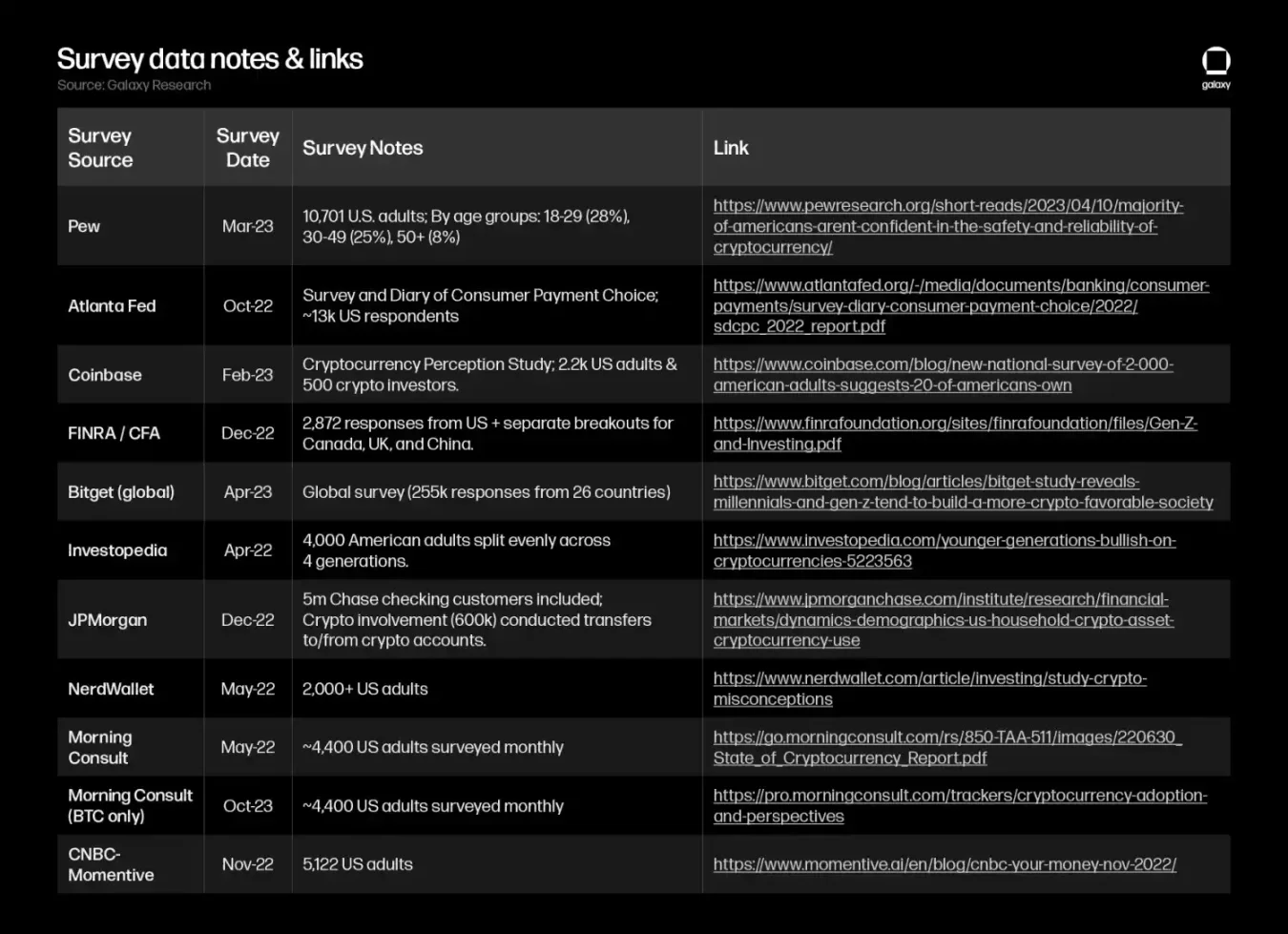

Other surveys tracking generational adoption of cryptocurrency offer slightly different estimates, but all arrive at a similar conclusion: millennials’ crypto adoption rate is several times higher than that of Baby Boomers, averaging 5.0 times higher across the surveys included in the table below (see appendix for detailed survey links and methodology):

Other Notable Survey Findings

Crypto adopters tend to be more highly educated and financially literate. One empirical study on crypto adoption found that “individuals with higher subjective financial literacy are more likely to perceive the benefits of using cryptocurrencies and exhibit greater willingness to adopt them.” An Investopedia survey revealed that 69% of millennials report intermediate to advanced understanding of digital currencies, compared to just 23% of Baby Boomers.

Younger generations favor cryptocurrencies as much as stocks and allocate more to the asset class. The same Investopedia survey found millennials are slightly more likely to invest in cryptocurrency (38%) than stocks (37%). A FINRA/CFA survey found Gen Z investors are most likely to first invest in cryptocurrency (44%), followed by individual stocks (32%) and mutual funds (21%). The study also found Gen Z reports a median investment of $1,000 in crypto—about a quarter of their total median portfolio value of $4,000. A BNY Mellon survey separately found that “next-generation” investors allocate 5% of their average portfolio to crypto—five times the 1% average allocation among North American family offices.

Stances on cryptocurrency could become key issues influencing voter decisions. Millennials and Gen Z currently make up about 40% of the voting-age population and will become the majority of U.S. voters by 2028. A Coinbase survey found that 44% of millennials believe politicians and policymakers should support crypto/blockchain. Among the 52 million crypto owners, 55% said they might vote for a pro-crypto candidate in 2024, with millennials showing the highest support at 78%, surpassing Gen X (71%), Gen Z (69%), and Baby Boomers (51%).

Across all these generational surveys, regardless of phrasing, millennials and Gen Z are consistently more likely than Baby Boomers to support cryptocurrencies. Therefore, transferring wealth to this crypto-friendly demographic could drive substantial capital inflows into Bitcoin and broader crypto assets.

Impact of the Great Wealth Transfer on Bitcoin / Cryptocurrency

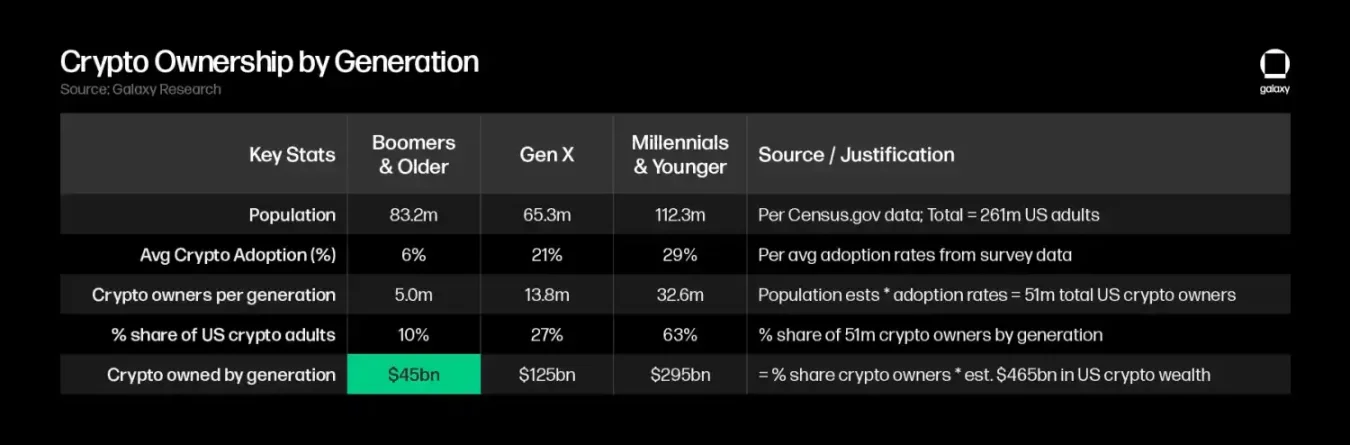

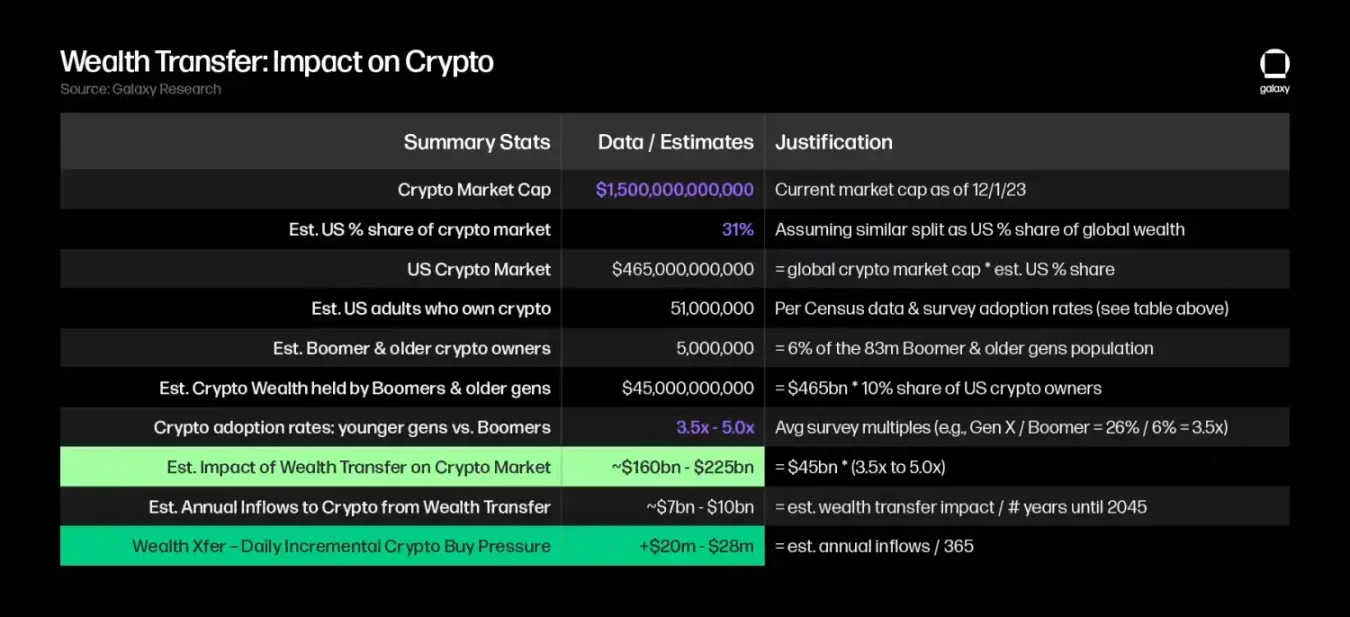

As of November 27, 2023, the crypto market was valued at approximately $1.5 trillion. Assuming a distribution proportional to the U.S. share of global wealth (31%), we estimate the U.S. crypto market value at around $465 billion.

Applying average generational adoption rates from surveys to U.S. Census population data, we estimate 51 million Americans own cryptocurrency (consistent with Coinbase’s estimate of 52 million), with Baby Boomers and older generations accounting for about 10% of U.S. crypto owners (Gen X: 27%, millennials and younger: 63%). Assuming even distribution of the estimated $465 billion in U.S. crypto wealth, we estimate Baby Boomers and older generations currently hold about $45 billion in crypto assets.

If the Great Wealth Transfer happened today, we estimate an additional $160 billion to $225 billion would flow into the crypto market as wealth moves to younger, more crypto-enthusiastic generations. This projection assumes younger generations have 3.5 to 5 times higher crypto adoption rates than Baby Boomers (based on survey averages, using 3.5x for Gen X vs Boomers as the lower bound and 5x for millennials as the upper bound), implying younger generations would hold 3.5 to 5 times more crypto wealth than Baby Boomers currently do.

Since most wealth held by Baby Boomers and older generations is expected to transfer to younger generations before 2045, our estimates suggest this wealth transfer could generate $20 million to $28 million in daily buying pressure for the crypto market over the next 20 years.

Note that this methodology may underestimate the wealth transfer’s impact on crypto markets, as it uses a rough estimate of current crypto holdings by Baby Boomers as a baseline—implying that while adoption rates rise, the propensity to invest in crypto remains unchanged. More likely, however, is that a multiplier effect occurs, as millennials and younger generations typically allocate a larger share of investable wealth to crypto than to traditional assets like stocks and bonds.

This approach is also conservative, as it assumes static preferences and wealth potential today, without factoring in millennials’ higher future earning potential or compounding returns over time. As infrastructure and application layers evolve and the technology proves its potential benefits, crypto adoption and acceptance should continue to grow.

Moderating Expectations About Financial Impacts of the Great Wealth Transfer

While some economists estimate the wealth transfer could increase millennials’ overall wealth by 5–10 times—potentially easing financial strain and triggering an (crypto) economic boom—several factors suggest the actual impact may be much smaller:

Most of the wealth to be transferred is concentrated among a few wealthy families. If the total wealth held by Baby Boomers and older generations were evenly distributed among the remaining ~250 million Americans, each person would receive about $380,000—enough to easily clear existing debts for younger generations. However, wealth transfer will not be uniform: Cerulli estimates 42% ($35.8 trillion) of total transferred wealth will come from high-net-worth and ultra-high-net-worth households, which represent only 1.5% of all families. University of Pennsylvania research on historical inheritances found top 5% income households receive 4 to 12 times more inheritance than bottom 80%. Additionally, the probability of receiving an inheritance within any five-year period is only 7.4%, rising only slightly among higher-income groups.

For those expecting inheritances, actual amounts received may fall short of expectations. A Federal Reserve study found people who inherited in the past three years expected an average of $72,200 but actually received $46,200—a significant gap. For the bottom 50% of wealth holders, the discrepancy is even starker: they expected $29,400 on average but received only $9,700. Regarding the "Great Wealth Transfer," an Allianz survey found 52% of millennials expecting inheritances anticipate receiving at least $350,000, while 55% of Baby Boomers planning to leave inheritances intend to pass less than $250,000.

With longer lifespans and shrinking pensions/benefits, Baby Boomers are spending more on themselves. Fidelity research shows a 65-year-old retired couple can expect to spend $300,000 on healthcare during retirement—an 88% increase since 2002. A Coventry study found 85% of retirees prioritize their own financial security and health, with over 75% planning to leave no inheritance.

Historical intergenerational wealth transfers have led to greater wealth inequality. A Bureau of Labor Statistics (BLS) study on prior wealth transfer events (tracking inheritances from 1989 to 2007) found little evidence of an inheritance surge—inherited wealth accounted for only 19% of net worth on average, continuing a declining trend, suggesting inheritances play a diminishing role in household wealth accumulation over time.

Therefore, millennials hoping the wealth transfer will immediately bring economic prosperity and erase all debts should temper their expectations and prepare accordingly. Most transferred wealth is unlikely to reach lower-income groups who need it most. Nevertheless, any inheritance received can still improve personal financial situations and enhance investment capacity—with Bitcoin and other crypto assets likely to be major beneficiaries.

Outlook

Baby Boomers experienced post-WWII economic prosperity, profoundly shaping American society. Yet they differ sharply from millennials and younger generations, who face greater economic pressures than their predecessors. Beyond vast wealth disparities, digital natives hold distinct social values—particularly regarding technology adoption, social consciousness, and institutional trust—making them more receptive to alternative financial systems like Bitcoin and cryptocurrencies.

As the last of the Baby Boomers enter retirement, millennials will become the primary beneficiaries of the "Great Wealth Transfer," a process through which older generations pass nearly $100 trillion in wealth. While the Great Wealth Transfer may not resolve all mounting debt challenges faced by younger generations, it represents a meaningful demographic shift that amplifies the crypto-friendly inclinations of the digitally native population. Over time, as people age and wealth flows downward, cryptocurrencies may see sustained capital inflows and gain broader support on the path to wider adoption.

Appendix: Survey Data

[Disclaimer] Markets involve risk. Investment should be approached with caution. This article does not constitute investment advice. Readers should consider whether any opinions, viewpoints, or conclusions presented herein are suitable for their specific circumstances. Use at your own risk.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News