Rising star Mirro: From losing 30 ETH in FT to becoming a top-tier Chinese FT player

TechFlow Selected TechFlow Selected

Rising star Mirro: From losing 30 ETH in FT to becoming a top-tier Chinese FT player

In the Web3 space, there are significant differences between China and North America in Web3 development—not just geographically, but also culturally and symbolically.

Written by: Web3 Figures

Could you briefly introduce yourself?

Hi everyone, I'm Mirro, the curator of a shrine. I graduated from the London School of Economics (LSE) with a degree in finance and previously worked in investment banking within traditional finance. Later, I spent some time at Huobi Exchange during Li Lin's tenure, and since then, I've primarily worked as an independent consultant collaborating with various institutions.

Can you share your entry point into the crypto space?

From Finance to Web3

Early in my career, I entered the financial sector, mainly focusing on investment banking and asset management in traditional finance. However, through serendipitous encounters and the influence of mentors and friends, I gradually shifted toward the Web3 field. These mentors provided invaluable guidance, helping me deeply understand the unique characteristics of Web3's financial markets. In this domain, I discovered its appeal—not only did it offer more direct and reliable market information, but it also deepened my understanding of market transparency and asymmetric games. Here, I could better leverage my strengths, including comprehension of market models and expertise in liquidity and trade execution.

Over time, I dedicated substantial effort to working in this industry. Initially, I focused on industry analysis before gradually moving toward collaborating with major project teams and friends to explore joint opportunities. I often invested significant time researching liquidity issues, analyzing and seeking solutions for liquidity and asset issuance challenges. Looking ahead, I believe solving the problems of liquidity and inconsistent asset quality across the blockchain market is crucial. Although the market has recently performed well, with BTC prices surging, I think the more critical issue is how we can identify high-quality assets, issue them in fairer and more efficient ways, and enable them to accommodate large-scale capital. This remains a challenge carried over from the last bull market—an area we continue to explore.

Friend Tech Brings New Insights

Friend Tech is a great example—they used a bonding curve mechanism to release liquidity. Of course, this method comes with considerable friction and losses, but it offers us many insights. They attempted to treat each Twitter account as an asset for issuance, which sparked new thoughts about asset issuance for me.

In other aspects, I’m not particularly a fervent coin trader, although I have dabbled in trading. Early NFTs and DeFi were areas I paid close attention to. However, whether one can profit from these is another matter—I'm not well-suited for secondary market trading. As for projects I’ve participated in, there have indeed been many, including those I played around with and explored, as well as collaborations with project teams and large institutions. I was an early observer of projects like "Milady," especially their planning and liquidity strategies. Out of interest, I once provided liquidity for such projects for a period without formal agreements. Additionally, I spent a lot of time studying and learning about other projects. I had the privilege of communicating with founders of some projects for a period—though I didn’t actively participate, I gained deep insights into their mechanics and designs.

Key Takeaway: Early in my career, I worked in investment banking and asset management within traditional finance. Influenced by mentors and friends, I transitioned into the Web3 space, diving deep into market dynamics. I began with industry analysis and later collaborated with major project teams to address liquidity and asset issuance challenges. Solving liquidity and asset quality issues in the blockchain market is vital—this remains a key area of exploration. Friend Tech’s approach offered valuable insights, using a bonding curve to release liquidity and prompting fresh thinking about asset issuance.

What has been your deepest insight in Web3?

People Often Focus on Surface-Level, Ignoring the Essence

First, I’ve observed that most people in the market often have conflicting mindsets, motivations, and expectations. This manifests as laziness—even if they work hard, their diligence stems from a desire to eventually become lazy. This leads to widespread unethical behaviors such as rug pulls, PVP battles, scams, and sudden project exits. In my view, courage is required in this market, especially for Chinese participants, due to legal constraints and the highly polarized public perception of projects. People tend to judge a project solely based on price increases, ignoring critical factors like valuation and liquidity.

Second, I’ve noticed that some projects have experienced massive gains—rising tens of thousands or even hundreds of thousands of times. While some may label them as money laundering or problematic, the fact remains that many people genuinely profited from them. Yet, many remain overly optimistic, hoping these projects will surge again, disregarding valuation and liquidity concerns. Eventually, when prices drop, they complain—revealing that many still don’t truly understand risk or the nature of the market.

In reality, I believe many successful project founders aren’t cases of “slayers becoming dragons,” but rather entrepreneurs who deeply understand the true nature of players and users in the market. They realize it’s impossible to make everyone profitable—or even the majority—because even if most do profit, it holds little significance. That’s why top-tier projects ultimately attract different groups of people at different stages—whether at launch, peak, or decline. This phenomenon taught me a lesson: judging what’s good or bad in the Web3 market isn’t always fair.

In my opinion, when evaluating this market and industry, we should focus more on what contributions individuals or entities have made to the ecosystem. This goes beyond just money—it’s about tangible impact and contribution. There are many outstanding developers in this space who have open-sourced excellent tools and projects and conducted extensive open data analysis—all of which contribute meaningfully to the industry. Yet, they don’t directly engage in resource or production allocation; their contributions are largely indirect.

Viewing the Market with Rational Thinking

Conversely, those directly involved in resource and production distribution are often emotionally driven rather than truly rational participants. Even if they don’t directly contribute to the industry, bringing capital into the market counts as a form of contribution. However, I don’t believe capital inflows necessarily represent rationality—in fact, I think the vast majority of participants in this market, including project teams and institutions, are irrational. True rationality is lacking.

This market often follows the “dark forest” principle—the larger your visibility, the more likely a bigger predator will come after you. This is typical for BTC: someone might profit from daily BTC trades, others from weekly charts, but there will always be whales holding tens of thousands of BTC waiting to confront you on the monthly chart, ready to forcefully liquidate your position. Therefore, no one is permanently right in this market—everyone makes mistakes. Hence, we should adopt an inclusive and rational attitude when analyzing others’ actions.

We should consider the backgrounds of project teams and founders—even if they launched questionable projects or faced issues before, they may have learned valuable lessons and thus have the potential to create breakout products. Similarly, so-called “meme coins” might evolve into “dragons.” Despite past negative experiences, they could ultimately build remarkable products. This is precisely the essence of the Web3 market—full of uncertainty, yet rich with opportunity.

The market directly reveals the truth of financial markets. In traditional finance, we often see poorly run listed companies. I once asked my mentor: the chairman used to be a scammer, even involved in online gambling, yet now he runs a big data and AI company that went public. It felt against my conscience—as if I were enabling wrongdoing. But my mentor told me analyzing past history is meaningless. Just like in childhood, you might have mocked others, insulted teachers, or fought with friends—but that doesn’t prevent you from becoming president someday. Take Alexander Hamilton, one of America’s founding fathers—he did many questionable things in his youth, yet became a heroic figure in people’s eyes. This story gave me a profound insight—one I took a long time to fully grasp. Yet, I believe over 95% of people still haven’t understood this truth: how you should perceive people and projects in this market, and the fundamental logic driving it.

Core Insight: In the Web3 market, I observe that most people’s mindsets and expectations are often contradictory, marked by laziness and fantasy. Unethical behaviors and sudden project failures are common, and many judge projects solely by price movements while ignoring key factors like valuation and liquidity. Successful entrepreneurs usually understand the real nature of market participants—they know not everyone can profit. When evaluating the market, we should prioritize actual contributions and impacts over monetary returns. Capital inflows don’t equate to market rationality—true rationality is scarce. Uncertainty and opportunity coexist; we must analyze behaviors with inclusiveness and rationality. Past experiences don’t dictate future outcomes—both projects and individuals carry inherent unpredictability. These views apply equally to traditional finance—we need to rationally assess people, projects, and the market’s core logic.

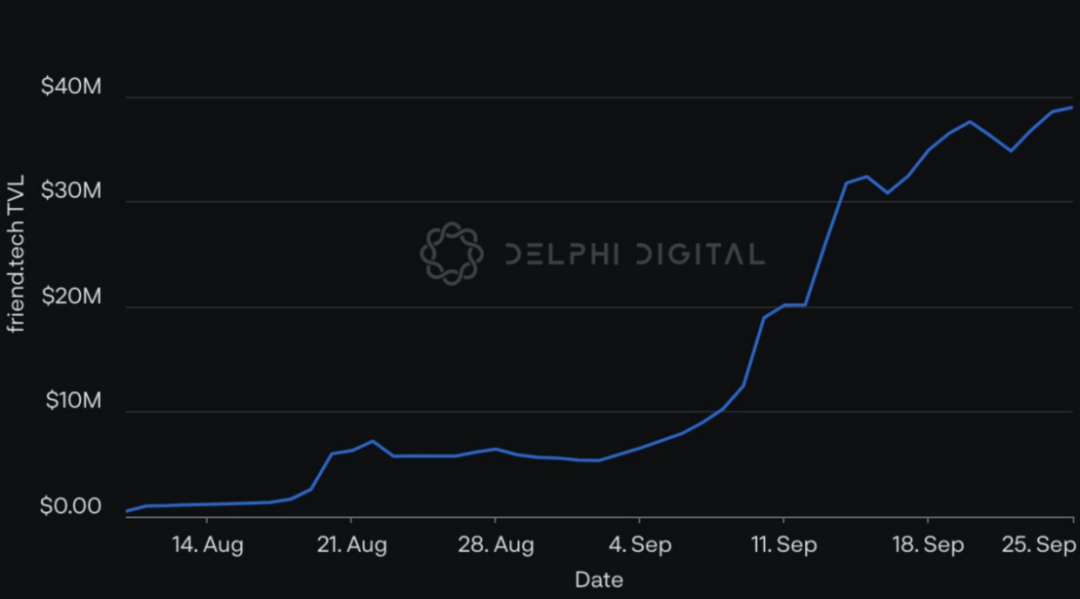

When did you first start paying attention to Friend Tech (FT)?

I first heard about FT at the end of August. Many friends told me it was an impressive product, and one of my mentors strongly recommended it, saying it excellently solved the liquidity issues we’d been researching. At the time, I considered getting involved, but there were mixed opinions in the market. Some called it a “three-no product” (no team, no roadmap, no value), while others worried that deeper involvement might harm personal reputation or legal safety—given that crypto-related activities inherently carry high risks. So during that period, I didn’t actively participate but instead made some backup investments.

Later, I realized FT wasn’t as negative as some described—it had its own unique features and potential. Although I really wanted to join the PD team, I communicated with them and even attended an interview, but unfortunately, our philosophies didn’t align well, and they weren’t particularly impressed with me, so we didn’t reach an agreement. Nevertheless, I’ll keep watching products backed by companies I admire. Just like in the previous market cycle, when I spent a lot of time writing about Blur, sharing knowledge on arbitrage and miner博弈, FT follows similar underlying logic.

Core Insight: I first learned about FT at the end of August, strongly recommended by friends and a mentor. Despite initial skepticism, I chose not to actively engage but made backup investments. Later, I recognized FT’s potential. Though I considered joining the PD team, misaligned philosophies prevented collaboration.

How do you view Friend Tech (FT)?

I think the most crucial aspect is that FT solves the problem of asset issuance—it clearly defines the concept of issuing assets. Previously, creating an asset pool on platforms like Uniswap was considered difficult, requiring technical knowledge, smart contract coding skills, and understanding of pool calculations and pricing mechanisms. FT elegantly addresses this with a clever bonding curve, making asset issuance far more accessible and effective. However, there is a cost—similar to BRC20 in the BTC ecosystem, which also simplifies asset issuance by allowing users to set parameters like total supply, number of shares per user, and total fees for quick deployment.

FT presents itself in a more aggressive manner, but its bonding curve determines its limitations. If you calculate the curve, you'll see that in the first 100 trades, price fluctuations per buy/sell can reach 60%–70%, whereas later inflows only cause 1%–2% changes, sometimes even less. This could deter large capital inflows. I often discuss this in Spaces—I say that if FT wants to attract big money, it may need new measures. I’m unsure if the team has considered this. If they do intend to, perhaps they could introduce mechanisms in the contract or elsewhere to allow large investors easier access to open-market participation. But currently, it seems FT hasn’t prioritized attracting institutional or large-scale capital. So rather than calling it a social finance product, I personally dislike the term “socialfi.” I don’t think FT is a social finance product. Projects like NBC may offer various functions, but fundamentally, they resemble exchanges. Compared to centralized exchanges like Binance, they lack customer support, BD teams, or large operational staff—but this doesn’t stop them from functioning as free, open markets. Currently, FT emphasizes liquidity mining and carries higher risks. It leans more toward being an on-chain exchange with liquidity mining—and so far, it’s the only project of this type still operating. That’s my understanding of FT.

Core Insight: FT solves the asset issuance problem and streamlines the process. However, the shape of its bonding curve limits volatility, potentially hindering large capital inflows. Currently, FT doesn't seem focused on attracting big investors. Rather than labeling it “socialfi,” I see it more accurately as a free, open market—not a social finance product.

Is there anything you'd like to proactively share?

I feel I don’t have strong biases in the Web3 space. I believe Web3 is tied to ideology and geography. Chinese Web3 and North American Web3 are entirely different worlds—so divergent that anyone who’s been to Silicon Valley would immediately recognize the gap. The market conditions, users, and infrastructure developers in mainland China operate on a completely different level compared to North America. I’m not saying one is superior—their ecosystems simply don’t belong to the same circle, making mutual consensus extremely difficult.

But this doesn’t mean we should blindly imitate the North American model. Instead, we should digest and absorb their approaches, reassemble and repackage them into forms suited to our own national context. This phenomenon has existed for a long time—starting from the US era, through last year’s free mint trend, up to today’s FT wave—you can clearly see the structural differences.

Therefore, I feel that when we talk about this industry, we’re often not discussing the industry itself, but rather exploring differences between two cultures, two sets of symbols. Communicating with North Americans involves fundamentally different dynamics. That’s why I hope myself and my friends can interact more with foreigners, understand their ways, and uncover the meaning and purpose behind their actions. Why are they able to create breakout products while we struggle? We need to reflect on these questions.

Core Insight: In Web3, there’s a significant divergence between Chinese and North American developments—not just geographically, but culturally and symbolically. This makes consensus difficult. However, mimicking the North American model isn’t the answer. We should learn from their experience and rebuild our own Web3 ecosystem based on local realities. This pattern has persisted across eras—from the US phase to free mints and now FT. Thus, discussions about the industry are often actually about cultural and symbolic differences. I encourage myself and others to engage with foreigners, understand their methods and intentions, and ask why they succeed where we don’t—these are questions worth pondering.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News