95% of ChatGPT’s users pay nothing—but they may be its most valuable users

TechFlow Selected TechFlow Selected

95% of ChatGPT’s users pay nothing—but they may be its most valuable users

Is Consumer AI merely experiencing high usage volume, or is it truly evolving into a legitimate business?

Author: Apoorv Agrawal

Translated by: TechFlow

TechFlow Introduction: This is the third installment in the author’s series on ChatGPT’s business model. The first two pieces established usage scale (900M weekly active users, 70% market share) and engagement stickiness (retention “smile curve,” usage depth comparable to Slack). This piece tackles the most critical question: What is this attention actually worth? The core conclusion is counterintuitive— for leading consumer AI applications, the ceiling for advertising revenue may exceed that of subscription revenue. Currently, ChatGPT’s 95% free user base contributes virtually zero revenue—a vast, untapped monetization opportunity across the entire industry.

Full Text Below:

The first two articles in this series demonstrated ChatGPT’s user scale and genuine engagement. Those pieces addressed the “quantity” component in the revenue equation: Revenue = Price × Quantity—how many users, how often they return, and whether habits are real. This article addresses “price”: How much can you actually charge?

Time spent is the bridge connecting the two. In consumer tech, time is the raw material for monetization. Subscription businesses convert time into perceived value and willingness to pay; advertising businesses convert time into ad inventory. Both start from the same point: How much time does your product occupy for users?

Let’s state the conclusion upfront: I believe the advertising revenue opportunity for top-tier consumer AI applications may exceed the subscription revenue opportunity. The reason is simple: Consumer AI is accumulating the same raw materials as the largest internet companies—time and attention. The advertising revenue formula is straightforward: Advertising Revenue = Total Time Spent × Ad Density × Cost Per Mille (CPM). Looking at these three variables, the data shows:

Total time spent on AI applications is exploding. AI’s share of attention follows the same power-law distribution as user count—even after adjusting for per-user time spent.

Per-user time spent is rising, meaning larger and more sustained growth in ad inventory. AI applications currently lag behind consumer benchmarks but are beginning to approach enterprise application levels. ChatGPT’s behavioral patterns resemble work and productivity tools more than social feeds—an encouraging signal for future ad density increases.

ChatGPT’s query intent signals are stronger than search, implying higher CPMs. See Section 3 below for details.

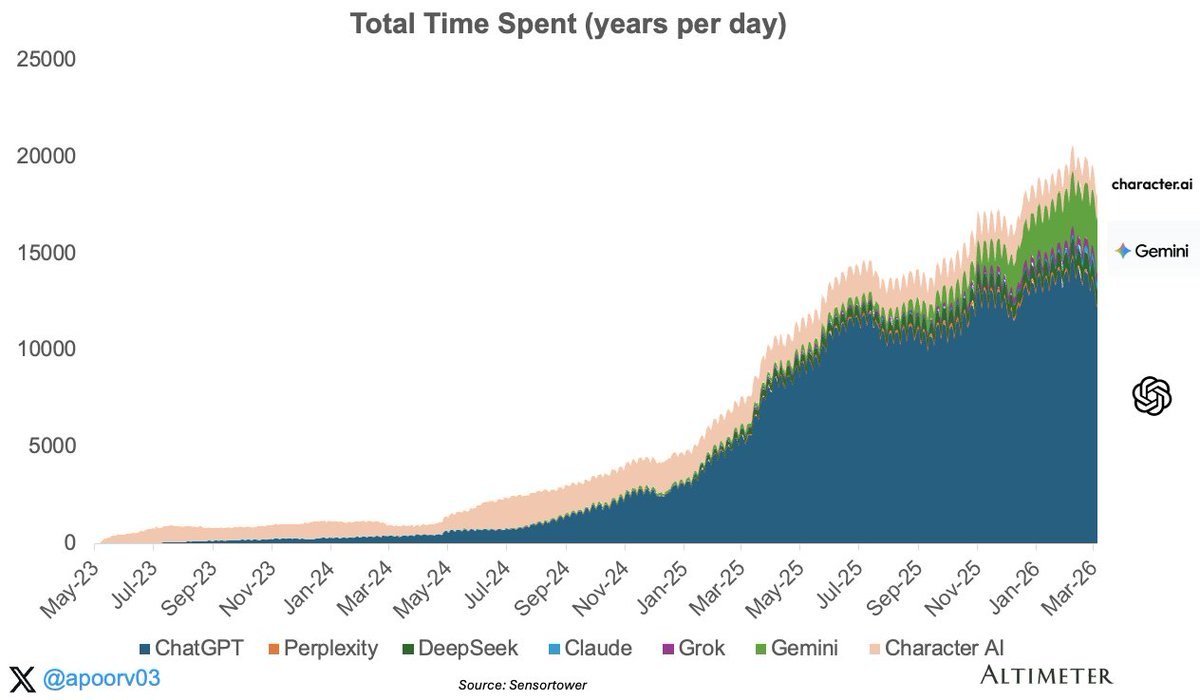

1. Total Time Spent: ChatGPT Captures 68% of Consumer AI Attention

Total time spent on generative AI applications has grown roughly tenfold over the past two years—and increased 3.6x alone in 2025. No other app category has expanded at such speed.

A few points stand out. First, the inflection point around January 2025 is highly visible. Driven by ChatGPT’s expansion into voice, image generation, and search features, total time spent doubled during the first half of 2025. Second, Gemini emerged meaningfully in mid-2024 and achieved notable growth—but remains far behind the leader.

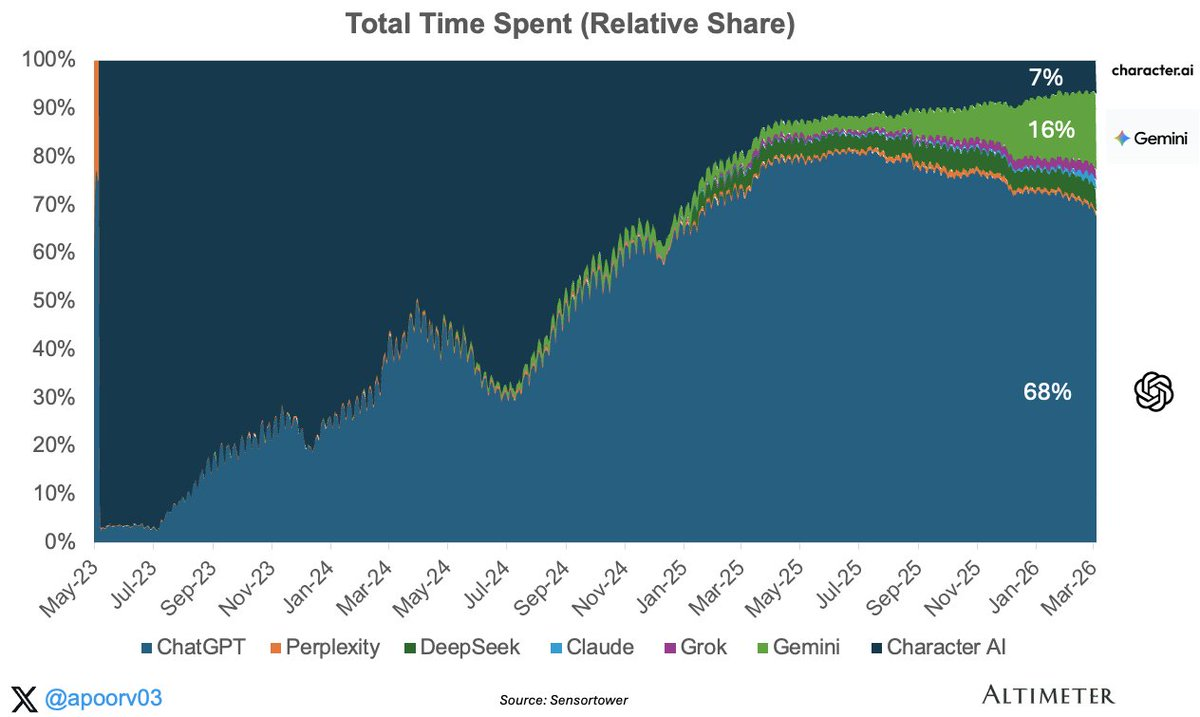

ChatGPT accounts for 68% of total AI time spent; Gemini, 16%; all others combined, ~16%. This concentration makes ChatGPT the most likely place for the first scaled AI-native advertising business to emerge. It also helps explain why OpenAI has experimented with monetization earlier and more aggressively than peers with smaller attention shares—a crucial point, because you cannot run ads on a platform lacking scale.

Where users spend time is where advertisers have available ad space—and 68% of that inventory resides in a single product: ChatGPT. For advertisers evaluating AI-native ad placements, the fact that attention is so heavily concentrated in one product is hard to ignore.

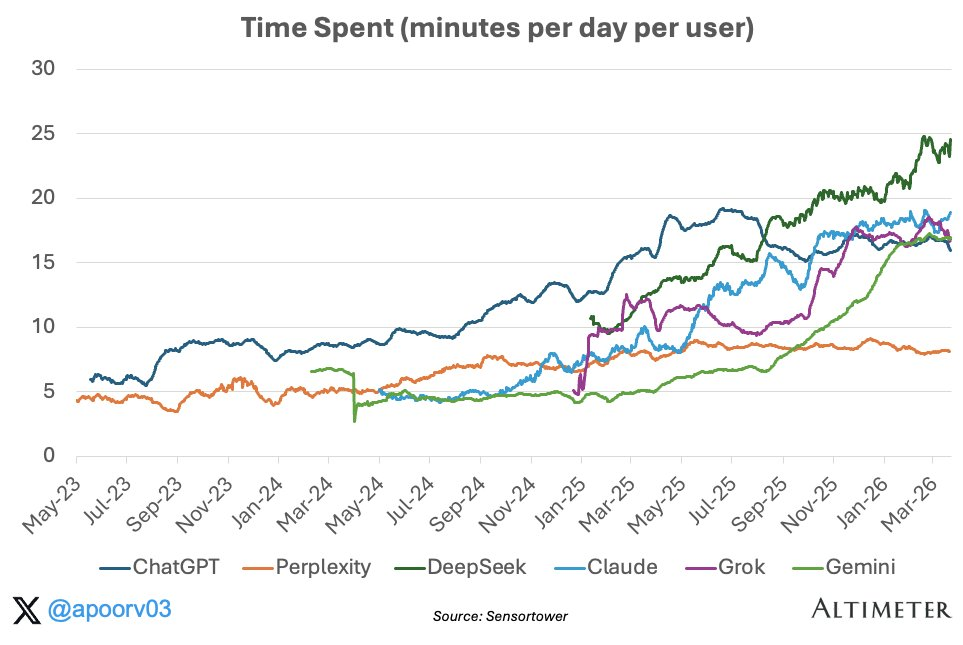

2. Per-User Time Spent Is Rising—Meaning More Ad Space

Every AI application shown in this chart is trending upward. ChatGPT’s per-user time spent has roughly tripled since early 2023. Claude, Gemini, and Grok have all surged sharply over the past year. The trend is clear: Users are spending more time on AI apps—not just downloading and abandoning them.

But how does this compare to known benchmarks for consumer and enterprise applications?

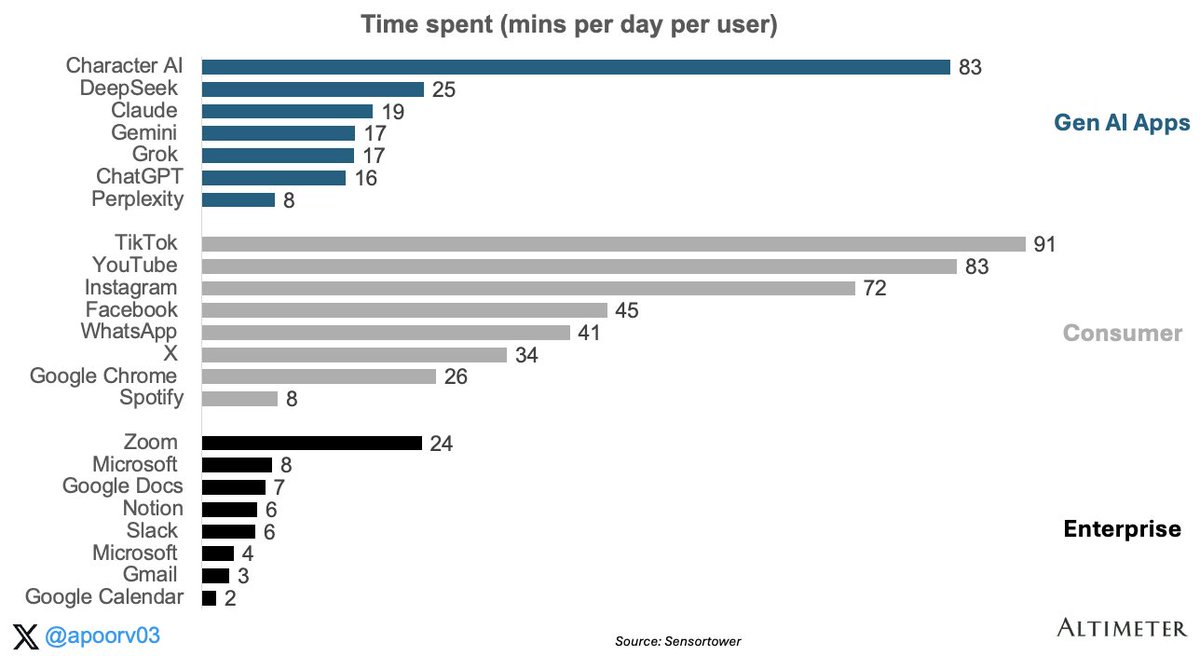

Compared to consumer apps: Still much lower. At 16 minutes per day, ChatGPT falls far short of TikTok, YouTube, and Instagram. But this gap isn’t a fair comparison—ChatGPT lacks two key drivers of massive time spent on consumer apps.

First, it lacks network effects. TikTok and Instagram are sticky partly because your friends, creators, and communities live there. Content is personalized and generated by people you follow—creating a pull to keep returning and refreshing. ChatGPT has none of this: no feed, no followers, no social graph.

Second, it lacks dopamine loops. You don’t open ChatGPT to scroll cat videos or check an ex’s profile. Consumer social apps are engineered for variable-reward interactions—you never know if the next swipe will be boring or delightful, and that unpredictability keeps you glued to the screen. AI assistants are the opposite: You arrive with a specific task, get an answer, and leave.

Compared to enterprise apps: Higher than most. Comparisons with enterprise apps are more relevant—but with an important caveat: This SensorTower data reflects mobile-only usage, so desktop-dominant products like Slack, Gmail, and Google Docs are underestimated. Even so, the signal is noteworthy. On mobile alone, ChatGPT already resembles a high-frequency productivity tool. This matters because productivity products can achieve strong monetization even with significantly less time spent than entertainment apps.

Slack charges $7–$12 per user per month. If AI assistants, operating at consumer scale, already capture daily usage time at this level, the monetization potential is substantial.

Rising per-user time spent implies two things in the revenue equation: greater perceived value to support subscription willingness-to-pay, and more ad inventory. Both point in the right direction.

3. Revenue Opportunities

3a. Why Advertising Can Outpace Subscriptions

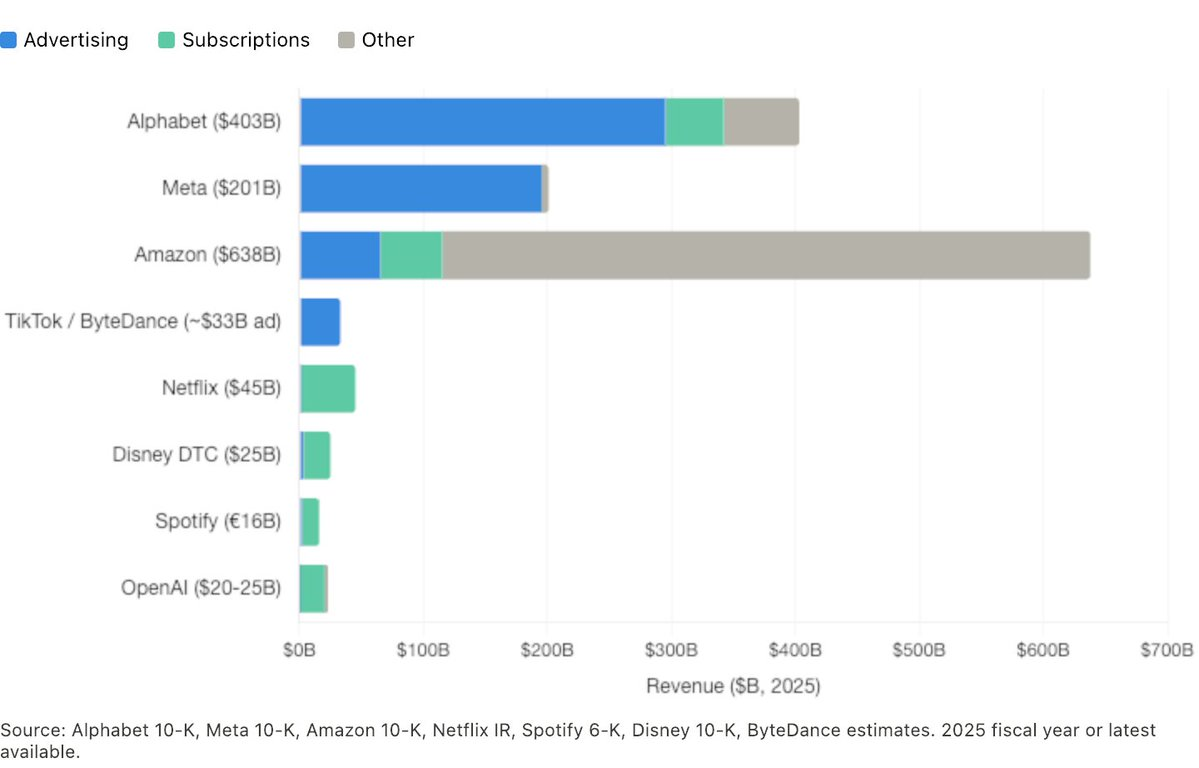

Now let’s examine the price side: What is this attention actually worth? At consumer scale, the two dominant monetization models are subscriptions and advertising. The key point isn’t that subscriptions are weak—it’s that historically, the largest consumer internet companies have generated far more revenue via advertising than subscriptions.

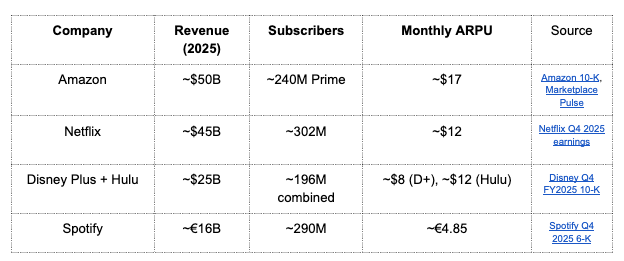

Largest consumer subscription businesses:

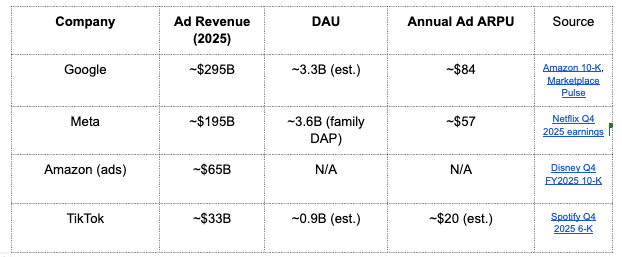

Largest consumer advertising businesses:

The magnitude gap is central. Google’s advertising business alone generates about five times Netflix’s revenue; Meta’s advertising business is about four times Netflix’s. Even Amazon’s advertising business—which barely existed a decade ago—now exceeds Netflix’s. A natural question arises: Can higher subscription ARPU compensate for a smaller paying user base? For some businesses, yes. But at scale, advertising’s broader monetization base tends to prevail.

Alphabet and Amazon are especially interesting because they operate both models. In both cases, their advertising businesses are larger and growing faster than their subscription businesses. Netflix, Disney, and Spotify rely almost entirely on subscriptions; Meta and TikTok, almost entirely on advertising. OpenAI currently relies almost entirely on subscription revenue, plus a small amount of ad revenue recently launched for ~5% of its free users in the U.S. This represents a massive attention pool contributing virtually zero revenue today. OpenAI is the pioneer here—but the same free-user monetization challenge applies to every AI application with a large unpaid user base.

3b. How AI Attention Is Priced

Advertising Revenue = Total Time Spent × Ad Density × CPM

Total Time Spent: We’ve covered this in Sections 1 and 2. ChatGPT has ~900M weekly active users, a DAU:MAU ratio of 45%, and ~16 minutes of daily mobile usage.

Ad Density (or “ad load”) is a product decision: How many ads per session? Google displays 3–4 ads per search results page; Meta inserts one ad every 3–5 posts in its feed. ChatGPT currently shows at most one ad per conversation—and only to ~5% of its mobile users. This restraint is wise for maintaining trust, but it means ad density is currently very low.

CPM—the price advertisers pay per thousand impressions—is fundamentally a function of one question: Will this user buy something? That breaks down into three elements: Intent (Is the user actively making a decision?), Attribution (Can the advertiser trace the ad to a purchase?), and Audience Quality (Does this user have purchasing power?)

Different major advertising businesses leverage distinct advantages. Google Search boasts strong intent signals: When someone types “best mortgage rates 2026,” they’re expressing commercial intent in real time. CPMs range from $15–$200+, varying by category, generating ~$84 annual revenue per user globally. Meta’s intent signals are weaker but it commands massive time spent—users scroll 30–90 minutes daily—and compensates with extraordinary targeting precision, inferring intent through behavior and social graphs, generating ~$57 annual revenue per user. YouTube sits between the two: moderate CPMs, long sessions, video creatives.

In summary: Google sells intent; Meta sells attention; YouTube sells watch time.

3c. Positioning of AI Assistants—Using ChatGPT as a Case Study

We use ChatGPT as our test case because it has the largest free user base and the most ad data. ChatGPT’s ad pricing is likely closer to Google’s than Meta’s—and potentially superior in categories where conversational context enhances commercial intent.

When someone opens ChatGPT to ask for laptop recommendations, compare insurance plans, or plan a family trip, the interaction resembles search—but with richer context. Users often provide budget, preferences, constraints, and intent in a single prompt. This makes commercial signals easier for advertisers to interpret—even if it doesn’t automatically make every AI query more valuable than every search query.

I expect ChatGPT’s actual CPM to be at least on par with Google Search—and possibly higher in certain categories. Early data supports this view. OpenAI’s premium ad placements are priced at ~$60 CPM—far above display ads and squarely within the high-intent search ad range.

ChatGPT currently has ~800–900M free users (95% of its weekly active users). If ChatGPT could generate $30 in annual ad revenue per free user, that would translate to $25B in ad revenue at current scale. For context, Meta generates $57 per user, Google $84—so $30 per user for a high-intent, login-required product is not aggressive.

Early data shows no impact on trust metrics—but testing remains in early stages. The real execution challenge is scaling ads 20x without damaging the experience that builds user habits. The primary reason this opportunity remains unproven is that not all AI time spent has commercial value. A significant portion of ChatGPT usage involves informational queries, creative generation, or productivity tasks—not transaction-oriented ones. And unlike feeds or search result pages, the conversational interface offers fewer obvious places to insert ads without harming trust. So upside is real—but execution constraints are equally real: OpenAI must monetize without compromising the habit-forming product experience.

There’s also a more optimistic possibility. AI isn’t just creating new ad inventory—it’s enabling entirely new ad formats. Conversational ads—where product recommendations are woven into dialogue rather than tacked onto sidebars—could actually improve, rather than degrade, user experience. Imagine asking ChatGPT to plan a weekend getaway, and it recommends a relevant hotel deal based on your unique preferences and memory—within the flow of conversation. That’s not an interruption; it’s a feature. If AI delivers hyper-personalization, agent-like behavior, and truly conversational brand moments, the advertising opportunity may not only be massive—but fundamentally different from any ad experience that exists today.

3d. Why Google Can Wait

Google’s strategy differs markedly from OpenAI’s. Google has repeatedly stated it has no plans to run ads in Gemini. At Davos in January, DeepMind CEO Demis Hassabis expressed surprise at OpenAI’s “rush” to introduce ads in ChatGPT. In December 2025, Google Ads VP Dan Taylor wrote: “There are no ads in the Gemini app, and no plans to change that.”

This is a strategic luxury unique to Google. Its search business is already a $295B-per-year advertising cash machine. Google can subsidize Gemini as a loss-leading acquisition vehicle—growing users and deepening engagement with an ad-free experience—while monetizing AI through its existing search infrastructure (AI Overview and AI Mode already run ads). OpenAI lacks this luxury. With no independent cash cow to lean on, it must monetize directly from the chat interface.

Currently, Gemini monetizes solely via subscriptions—a much smaller per-user revenue opportunity compared to OpenAI’s emerging ad-plus-subscription model. But Google is playing a different game—protecting its assistant to retain users while aggressively monetizing search result pages. Whether this strategy remains viable as free-user inference costs rise and Gemini surpasses 750M monthly active users is an open question. At some point, the economics of operating a large-scale free AI assistant may force even Google to act.

In Summary

This series asks a simple question: Is consumer AI merely a high-volume phenomenon—or is it becoming a real business? The first article showed reach; the second, user habits; and this third article suggests the monetization opportunity may be larger than many assume.

An underappreciated point: Top AI assistants—especially ChatGPT—already possess the best monetization traits of the largest consumer internet companies: scalable, recurring attention. Roughly 95% of its weekly active users remain free—meaning most of this attention is monetized at nearly zero today.

This doesn’t guarantee advertising will reach Google or Meta’s scale. The conversational interface is harder to monetize cleanly, and trust is the product’s most valuable asset. But if OpenAI can prove ads can exist in high-intent assistants without degrading user experience, the long-term advertising opportunity may ultimately surpass subscription revenue. And if that happens, Google’s real strategic question won’t be whether Gemini should stay ad-free—but how long it can afford to.

Thanks to Sarah Friar and Fidji Simo for reviewing drafts of this article and the series.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News