A Brief Analysis of EigenLayer's Restaked Re-staking Model and Returns

TechFlow Selected TechFlow Selected

A Brief Analysis of EigenLayer's Restaked Re-staking Model and Returns

How EigenLayer Transformed the Paradigm of Network Security with Its Innovative "Restaking" and Created New Yield Opportunities for Validators and Investors

Author: Siddharth Rao, IOSG Ventures

Special thanks to Kratik Lodha from Renzo for valuable feedback on this article, and contributions from the IR team.

The "Restaking" Part

Introduction to EigenLayer

Around a year ago, EigenLayer embarked on a journey aimed at enabling new paradigms in network security understanding—the concept of "restaking" emerged. In short, ETH validators can now secure multiple networks, including foundational layers like DA layers, compute networks, and middleware such as shared sequencers. Essentially, any network requiring some form of consensus no longer needs to bootstrap its own security capital. These networks are known on EigenLayer as Actively Validated Services (AVSs).

Without EigenLayer, anyone wanting to become an operator within a system (e.g., DA) would need to invest in relevant hardware and initial staking. This forces projects that require validator sets to issue tokens at extremely high (sometimes unreasonable) valuations to fund high-inflation rewards. This could lead to massive speculative sell-offs, which are detrimental to validator operators.

Admittedly, there is leverage risk from single-operator concentration, but there will always be well-performing validators seeking additional yield opportunities.

EigenLayer enables native Ethereum restaking by creating EigenPods or using liquid staking tokens (LSTs) such as stETH, rETH, and cbETH, thereby securing AVS networks. Anyone holding LSTs is effectively contributing to Ethereum’s security and decentralization and earning rewards from the Ethereum network. Further staking of LSTs provides security for AVS networks in exchange for AVS-generated yields. Thus, LST restakers become eligible for network rewards (after operator fees).

If staking and restaking are beneficial, why make it liquid?

If you believe in liquid staking on Ethereum, then you should also support liquid restaking. Liquid staking on Ethereum involves two parties: Lido and retail participants. Retail participants may say, I don’t have enough ETH, hardware, or even time to run a validator, but I want higher returns on my ETH. Staking providers respond: I can help; I’ll take a portion of the returns as an operational fee and operate transparently.

This eliminates five public costs: hardware cost, hardware maintenance, time, effort, and mental overhead.

For EigenLayer, beyond the above-related costs, there is additional delegation complexity. In Ethereum, every node operated by a provider is “interchangeable”—the network treats each node identically regardless of whether it runs on bare-metal infrastructure, cloud, or elsewhere.

With EigenLayer, however, one network secures other networks, and each operator in the network can choose which specific networks they wish to validate. This essentially means no two operators are identical. Therefore, experienced teams or consortia wisely select operators with strong strategies to address retail participants’ concerns.

The "Liquid" Part

Opportunities exist year-round to earn higher ETH yields than any staking protocol on Ethereum.

If focusing solely on yield, there are approximately 1,748 ways to boost your ETH returns.

The real value lies in nearly “risk-free” yield—the method of earning ETH with minimal risk. For liquid tokens, the lower the risk, the greater the likelihood the LST will be whitelisted across other protocols, enhancing composability and increasing demand for the LST. All of this begins with trust—lowest possible risk.

For LSTs, risk assessment isn't overly difficult. You have operator-based risks (e.g., operator shutting down validators, operator quality, hardware quality) and network-based risks (smart contract risk). The consensus mechanism is uniform, and minimum hardware requirements apply equally to all operators.

In restaking, more factors must be considered, including hardware scalability requirements, security audits of AVSs, battle-testing of novel consensus mechanisms, economic models of individual AVSs, and types of supporters (investors, partners, etc.). Just among the 15 AVSs currently running on EigenLayer, there are 32,767 possible strategies. We cannot expect retail investors to make informed decisions.

Retail participants won’t do this—and if they blindly mimic any operator strategy and suffer slashing, trust will erode, harming network liquidity. If every operator launches their own LST, it will cause excessive fragmentation or over-concentration of stakes early on. Even if multiple operators use the same strategy but issue different Liquid Restaking Tokens (LRTs), unnecessary fragmentation occurs. A common LRT with unified strategy and decentralized operators is crucial for EigenLayer’s success.

This ensures a positive feedback loop of “lowest risk,” which can be visualized as:

Best Risk Management → More Liquidity → Most Whitelisted → Most Used → Most Liquidity → Most Popular → Lowest Risk

It's considered lowest risk because losing 1 ETH from being slashed among 100,000 validators is far less risky than losing 1 ETH from a single validator. This is why people still choose to stake with Lido. Lido recently experienced a slashing event where over 20 validators were each penalized about 1.1 ETH (totaling ~20 ETH). Although their infrastructure partner absorbed the loss, it was negligible relative to Lido’s 8.83 million staked ETH. This highlights the importance of having trustworthy partners.

How Does Liquid Restaking Work?

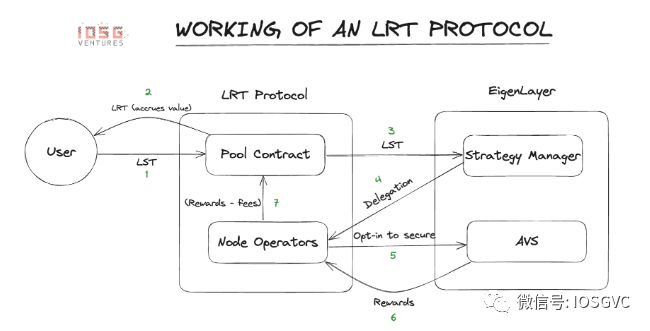

Users send their LSTs/ETH into the liquidity pool contract of a liquid restaking platform. Restakers receive an equivalent amount of LRTs (Liquid Restaking Tokens). The contract then allocates these tokens to a strategy management contract within the EigenLayer protocol. The strategy management contract delegates the tokens to node operators and ensures they adhere to the defined strategy. Governance of the LRT can select specific strategies. Operators validate underlying AVSs and retain a portion of the rewards. The remainder is passed back to the LRT protocol, which takes a cut before distributing the rest to restakers. This process is clearly more extractive than LSTs (Liquid Staking Tokens), but requires significantly more work and resource investment.

How Attractive Are the Yields?

We don’t know how AVS (Actively Validated Services) incentives will be distributed or exactly how each consensus mechanism will function. But based on some basic mathematical modeling, below are several plausible scenarios useful for estimating EigenLayer yields.

Considering FDV (Fully Diluted Valuation), referencing the latest known FDV data of comparable projects, token launches could occur at higher valuations, making yields significantly more attractive. Conservatively, we assume the FDV values of all partners announced on the EigenLayer ecosystem page reflect their last fundraising round valuation. As of October 19, EigenLayer’s TVL (Total Value Locked) was approximately 172k ETH, with Lido’s base yield around 3%. Based on our calculations, emissions total roughly $62 million (both affected by TGE price and emission schedules—conservative estimates assuming 2.5% token supply and FDV), translating to an approximate average 9% APY boosted yield, potentially totaling up to 12%.

In a more aggressive scenario, boosted APY could reach as high as 15%. Of course, these figures are based on assumptions—if you’d like to dive deeper into the calculations, feel free to DM me on Twitter (@Rao_Sidd).

LRT Ecosystem

-

Ion Protocol: A lending protocol allowing users to borrow assets using LSTs and LRTs;

-

Renzo: A dedicated liquid restaking platform accepting all EL LSTs (EigenLayer Liquid Staking Tokens) and ETH in exchange for their LRT ezETH (Liquid Restaking Token ezETH);

-

Rio: A dedicated liquid restaking platform accepting all EL LSTs and ETH in exchange for their LRT reETH;

-

Puffer Finance: A DVT-based LRT protocol;

-

Inception LRT: An LRT protocol focused on securing L2s;

-

Swell: An LST protocol also building its own LRT. Swell’s LST is also on EigenLayer’s JokerAce competition shortlist;

-

Stader Labs: Offers its own LST ETHx and is developing its own LRT;

-

Genesis LRT: Offers customized LRTs, enabling clients to create their own LRTs based on desired risk profiles, primarily targeting large clients and institutions entering this space;

-

Astrid Finance: Uses a rebase model where users receive rstETH, rrETH, or rcbETH based on what they’ve staked and their balance, with balances automatically adjusting as rewards accrue;

-

KelpDAO: Model similar to Renzo and Rio;

-

Ether.Fi: Allows users to deposit only ETH into a pool in exchange for their LRT eETH.

How Might This Space Evolve in the Future?

To become a true winner in this space, one must start by establishing maximum trust. LRTs will follow the same positive feedback loop as LSTs. Risk management is the most critical factor in attracting restakers, liquidity providers, and partners.

At some point in the future (timeline uncertain), yields may slightly exceed native ETH yields—but this depends heavily on the design and adoption of underlying AVS economic models. AVS usage may become the preferred way for users to earn the lowest-risk returns on Ethereum, combining Ethereum’s consensus rewards with AVS yields.

Recently, Mantle staked 40,000 ETH from BitDAO funds into Lido. In the foreseeable future, this means they will hold substantial stETH, likely to be listed on Mantle, with a portion also restaked into EigenLayer (once LST supply caps increase). For example, if Mantle chooses to use EigenDA as its DA layer, they would strongly favor the lowest-risk strategies, as these AVSs protect treasuries while aligning with Mantle’s overall strategy and goals.

Mantle could further encourage use of their platform’s LST: mntETH, and build a corresponding LRT (Liquid Restaking Token). This would help Mantle efficiently utilize their capital while helping secure their committed DA layer. Earned fees could be returned to users as gas rebates.

Due to competitive dynamics, power laws will play a role (market structures tend toward “winner-takes-most” outcomes), with the top 1–2 protocols eventually controlling 80–90% of the market. I believe only those protocols fully dedicated to developing this market stand a chance of emerging successfully, as this space demands highly concentrated effort. It’s also possible that major LST protocols may vertically integrate upstream, as Swell has done, though there are no clear signs yet.

Being available on day one is also critical for LRT protocols. The greatest trust in retail markets comes from TVL (Total Value Locked). Projects that attract strong TVL on EigenLayer’s first or second day may become leaders in the foreseeable future.

There will always be those chasing high yields, especially high-risk investors. As LRT protocols gain broader adoption, more DeFi integrations will emerge, unlocking exponential strategies and potentially creating a positive flywheel effect.

We believe over time, all operators will converge toward similar strategies and settle on minimal spreads. This will largely depend on the novelty and design of underlying AVSs and their economic models. To prevent too many large LST whales and liquid staking protocols from dominating EigenLayer, protocol-level controls exist. If restaking yields become increasingly low-risk, liquid staking protocols could become power centers within the Ethereum ecosystem. This risk could be mitigated through early adoption of a version of Jon Charbonneau’s “Proof of Governance” concept.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News