The Rise and Fall of SBF: The Crypto King's Downfall

TechFlow Selected TechFlow Selected

The Rise and Fall of SBF: The Crypto King's Downfall

Crypto is like the serpent in the Garden of Eden, tempting humanity into original sin, and FTX is merely the tip of the iceberg of that evil breaking the surface.

By Hao Fangzhou

FTX, once a towering giant in the crypto world, crashed into an iceberg in November last year. The impact triggered a tsunami that not only swallowed ships sailing nearby but also dragged down numerous associated businesses, ultimately devastating the entire crypto landscape.

Even today, the ripples from the FTX collapse continue—its scattered wreckage remains like a splinter lodged beneath every crypto enthusiast’s skin, reinforcing regulators’ perception of crypto financial risks, warning investors against complacency toward centralized operational risks, and constantly reminding industry participants who still feel the pain about “the next FTX downfall.”

As one of the largest frauds in financial history, the developments in the FTX case have been dragging on slowly (making it hard to keep up when you’re stuck in the middle of it). Odaily Planet Daily provides a brief recap of the latest developments over the past 10 days, along with key upcoming milestones for the next 10 days:

-

On September 16, SBF (Sam Bankman-Fried, founder/former CEO of FTX) saved an unpublished 15,000-word article on X (formerly Twitter), which included the line: “I might never be able to turn my lifetime impact positive, but the truth is, I did what I thought was right.” The article also revealed details about SBF’s personal relationship with Caroline Ellison, former CEO of Alameda Research, stating that Ellison refused SBF’s request to stop hedging trades at Alameda, prompting him to send her “the harshest message I’ve ever said.”

-

On September 17, FTX under CEO John Ray III announced that all affected accounts had been unfrozen, allowing claimants to reapply via the platform.

-

On September 22, a U.S. judge barred witnesses proposed by SBF from testifying at his October trial. FTX sued SBF’s parents, seeking recovery of “misappropriated funds.”

-

In court filings and social media posts, SBF repeatedly criticized law firm Sullivan & Cromwell for scapegoating him as responsible for FTX's collapse, while downplaying his own ties to the exchange.

-

FTX reminded users: September 29 is the final deadline for customers to submit claims.

-

On September 25, former FTX brand ambassadors including Shaquille O'Neal filed motions to dismiss class-action lawsuits.

-

On September 26, several lawyers interviewed by CoinDesk said that given the severity of the alleged crimes and estimated losses, if convicted, SBF could spend around 10 to 20 years in prison. However, Judge Kaplan holds broad discretion, and the final sentence will depend on his judgment.

-

CoinDesk disclosed the schedule for SBF’s October trial, set to begin on October 3, expected to last six weeks.

Earlier today, BBC released its documentary on FTX founder SBF titled “Panorama · Downfall of the Crypto King.”

Riding High on Success

Sleeping five hours a night, living with 10 roommates in The Bahamas, worth $22 billion at age 29, yet wanting to donate it all to charity, driving a Toyota Corolla because “I don’t really need a Lamborghini”—this was SBF as portrayed by NAS Daily shortly after he rose to fame.

When did people first start noticing SBF?

In 2019, he founded the cryptocurrency exchange FTX and quickly used high-profile marketing strategies to promote his vision and ideals worldwide.

Thanks to endorsements from popular social media influencers, FTX was seen as the most user-friendly crypto “stock exchange,” “as safe as a bank.” Many KOLs and YouTubers promoting FTX taught viewers how to “do nothing and become millionaires.”

Soon after, FTX expanded into collaborations with top-tier sports and entertainment celebrities, flooding mainstream channels with ads.

“If you don’t believe in crypto, you’ll miss out.” This message saturated online spaces frequented by youth (a familiar dose of FOMO).

Offline, FTX hosted lavish parties in the Bahamas featuring famous DJs. Young FTX users said, “It was cool. They were a company changing the world anyway, so they could afford to burn money.”

Amid this optimism and media hype, FTX rapidly attracted users from over 100 countries. For many new users, the “safe” way into crypto was: register → buy some FTT (FTX’s native token) → sell at peak prices → convert back into local fiat currency, reinforcing their wealth dreams during bull markets.

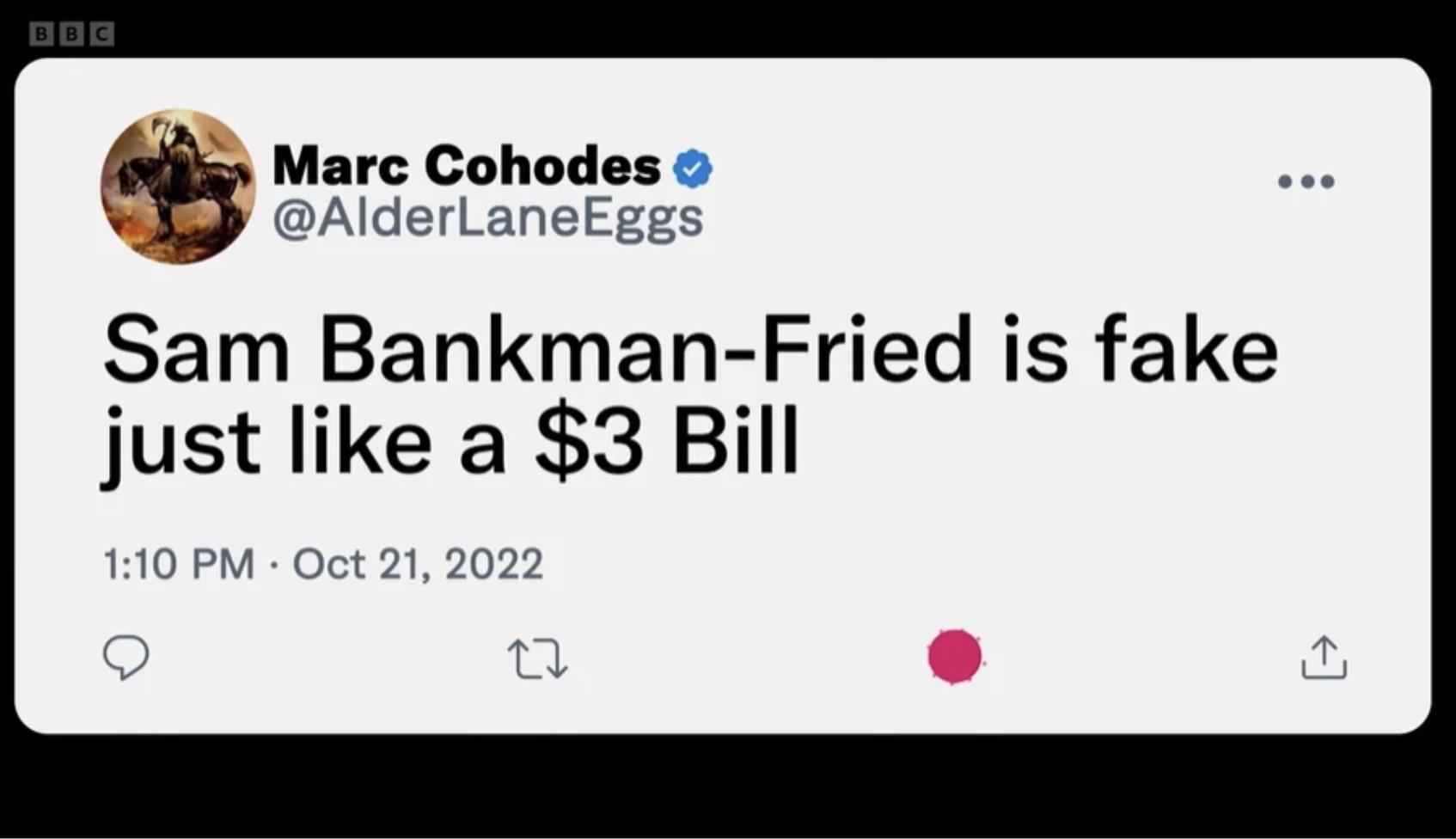

At the height of enthusiasm, whistleblowers tried to sound alarms—“The crypto industry is full of money laundering and fraud.” In the documentary, the horse-riding “Brother M” kept warning others: “Crypto is a wild west filled with snakes, continuously attracting cowboys… My mission is to expose the bad actors.”

But these voices were drowned out by louder ones.

An FTX user called “Brother S” claimed he always did thorough research before investing. Normally, when considering investing in or joining a company, people ask many questions: Who are you? What’s your edge? Who else supports you? Yet no one asked these questions of a genius with Stanford and MIT credentials.

A well-known anecdote recounts SBF playing video games during investor video calls. Instead of raising red flags, this left firms like Sequoia Capital and BlackRock wondering, “Wait—who is this kid? A genius?”

(Odaily Planet Daily note: FTX raised a total of $1.8 billion across multiple funding rounds, with investors including Sequoia Capital, Temasek Holdings, SoftBank Vision Fund, Ontario Teachers’ Pension Plan, Tiger Global Management… In January 2022, FTX announced a $400 million Series C round, valuing the company at $32 billion—the final funding announcement and peak valuation.)

SBF enjoyed a happy childhood; both parents were law professors at Stanford. Gifted in math from an early age, he attended gifted schools and later MIT, studying physics and mathematics. True to the nerd stereotype, he was deeply passionate about video games.

After founding FTX, the company culture revolved around gaming in spare time, shooting TikTok videos, occasionally sleeping in the office—all resonating strongly with younger generations.

Other key team members included:

-

Caroline Ellison, dubbed the “rumored girlfriend,” a Harry Potter fanatic with a “complicated” relationship with SBF. After SBF claimed he wanted to focus fully on public good through FTX, she took over Alameda Research (a crypto market maker/hedge fund/investment firm founded by SBF) as CEO;

-

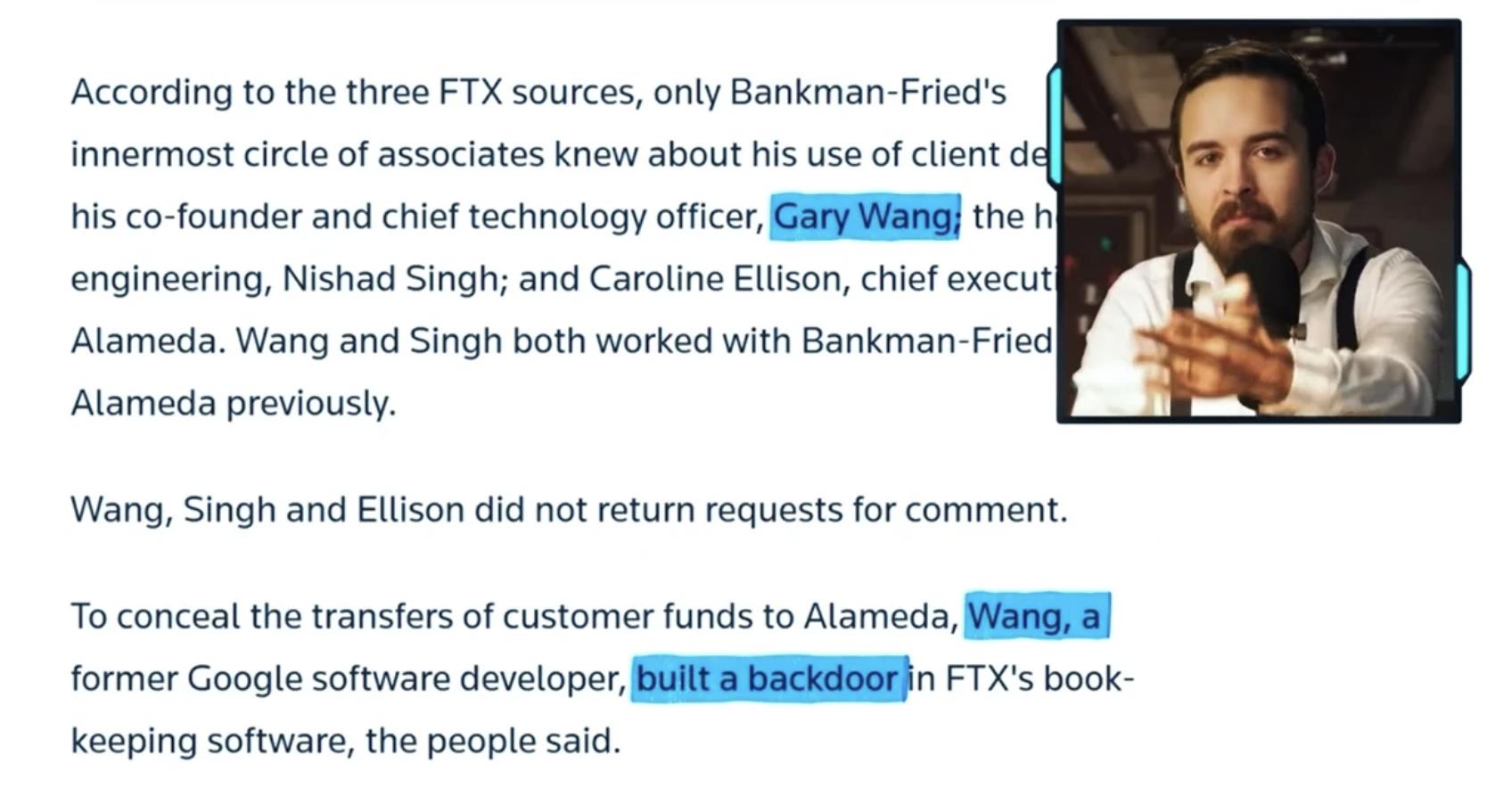

Gary Wang, mysterious Asian co-founder and CTO, see more in “The Mystery of FTX’s Missing Funds: Who Is CTO Gary Wang?”;

-

Anthony Scaramucci, former business partner of FTX (better known as founder of Skybridge Capital), who bought large amounts of FTT (and in early 2022, FTX acquired 30% of SkyBridge Capital). Considered a mentor figure to SBF, he played a significant role in fundraising efforts in the Middle East and North America, and later invested in a new crypto venture launched by Brett Harrison, former president of FTX US…

While appealing to youth, SBF also cultivated a different image to win backing from old-money elites. He graced the cover of Forbes, testified before Congress representing the crypto industry, and became Biden’s second-largest donor during his presidential campaign (donating $40 million to Democrats during the 2022 midterms).

And then, within less than two weeks, this very figure plunged into ruin, accused of being “the worst scammer ever.”

Ten Days of Drama in Crypto History

On November 2, 2022, Alameda Research claimed complete independence from FTT (related financial operations), sparking suspicion.

On November 6, Binance CEO CZ tweeted plans to “dump” FTT, quickly spreading FUD.

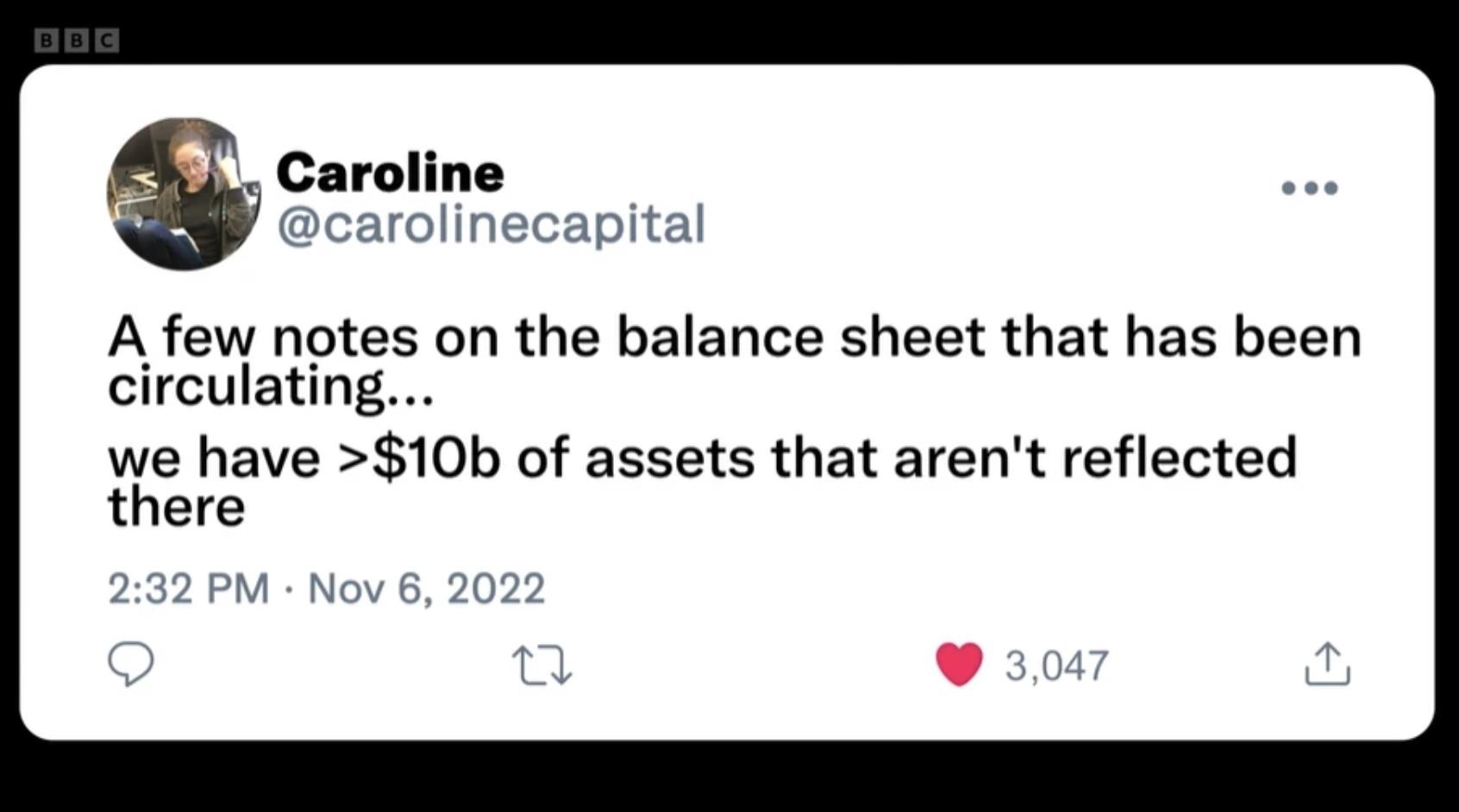

“Everyone was selling, everyone was rushing to withdraw. People told their friends to pull funds immediately.”

Perception matters immensely in financial markets. Caroline and SBF took turns issuing statements, trying to calm nerves and insist “we’re fine.”

On November 7, a deadly spiral of withdrawals → panic → bank run began.

SBF called partners saying it was just a liquidity issue—but within hours, a second call came: “It’s worse than I said earlier.”

Later interviews with former employees revealed they’d heard rumors about FTX risks but dismissed them. When confronted with the “unable to withdraw” screen, they were stunned.

At the time, some insiders still hoped FTX could be sold to Binance. (Odaily Planet Daily note: CZ initially considered acquiring FTX but later withdrew.) Some crypto KOLs argued: “CZ lit the fuse under his biggest competitor and let the market finish the job.”

On November 9, many offered SBF advice on what to do next. Anthony flew to the Bahamas to help, but the cash-strapped FTX empire was merely “plugging holes between subsidiaries.”

On November 10, SBF began apologizing publicly on social media. FTX US moved to impeach SBF.

On November 11, FTX collapsed completely.

“No one has ever lost everything faster.”

The Fall Guy

In front of the camera, one investor said he had placed $2.1 million—intended for housing and children’s education—into FTX.

Other FTX users calmly recounted their initial trust in FTX and the ultimate betrayal they felt.

Victims redirected their anger toward social media platforms and celebrity endorsers, accusing them of “manipulating investor thinking” and influencing their decisions: “Return those millions in endorsement fees—pay back our hard-earned money.”

Yet whenever the conversation turned to “why didn’t anyone notice earlier?”, answers grew vague, with fingers pointing everywhere.

Media reports described FTX’s fraud as classic: “misappropriating customer funds for personal use.”

As investigations progressed, documents revealed Alameda Research had operated without audits, with internal reports casually using phrases like “such is life.” Another piece of evidence showed that three years prior, FTX paid $3.3 million to someone exposing FTX’s fraud and money laundering, effectively bribing silence.

Politicians and celebrities previously backed by FTX swiftly distanced themselves. Republican representatives denied knowledge of certain campaign donations, claiming FTX also donated equal amounts to libertarian causes.

On December 12, 2022, SBF was arrested by Bahamian authorities. A crypto KOL live-streamed: “Two happiest moments in my life: losing my virginity and SBF’s arrest.”

Then followed long, drawn-out processes: investigations, restructuring, legal filings, extradition of executives, disputes among affiliated companies, attempts to seal Caroline Ellison’s diary (“too intimate” to be used in criminal proceedings), temporary releases, apologies, and defiance…

Behind the tangled facts lay complex human nature.

When the camera turned to residents of the Bahamas, different perspectives emerged.

One man who wrote a song about the FTX incident noted that FTX genuinely improved quality of life for local children through philanthropy. Some journalists described SBF, aside from his business failures, as a kind of “modern-day Robin Hood.”

Yet many charitable organizations reported receiving no donations from FTX, speculating that “perhaps disbursement priority was based on reputational benefit to FTX.”

Regardless of opinions, the fact remains: $1.7 billion in user funds remain unaccounted for.

What If I Did Many Good Things But Broke a Few Small Rules?

In post-collapse interviews (BBC notably captured a leg-twitch close-up), SBF repeatedly insisted he wasn’t a fraudster, vowed to repay victims to the best of his ability, and denied any backdoor access between FTX and Alameda. (Odaily Planet Daily note: However, on September 12 this year, court documents confirmed Alameda accounts had special privileges on FTX, including immunity from liquidation.)

By January this year, SBF appeared far less confident in interviews—avoiding eye contact, offering awkward smiles reminiscent of a guilty child, an expression that became a meme across online communities.

Crypto video blogger Tiffany Fong had never interviewed someone of SBF’s stature before the FTX collapse.

During SBF’s brief home confinement, Tiffany visited his parents’ house in California. Surrounded by fences, SBF wore an electronic ankle monitor. He occasionally played chess with visiting journalists, but mostly spent time “feeling loneliness”—solving Sudoku puzzles in jail, watching animated series *Inside Job* on Netflix at home.

After discussing guilt and responsibility, Tiffany even wondered: Could SBF actually be innocent?

In August this year, SBF was barred from contacting witnesses.

As mentioned at the beginning, October will bring the most critical trial phase in the FTX saga.

For the broader crypto industry, regulators are still striving to define compliance frameworks. Countless professionals are fighting for legitimacy, while others believe crypto is akin to the serpent in Eden, tempting humanity into original sin—and FTX may just be the tip of the iceberg.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News