A Brief Analysis of THORchain's New Product Model, Flywheel, and Risks

TechFlow Selected TechFlow Selected

A Brief Analysis of THORchain's New Product Model, Flywheel, and Risks

What would your choice be? The red pill or the blue pill?

Author: Sleeping Wildly in the Rain

$RUNE is a recently popular token that surged due to two positive developments from THORChain, only to later become a magnet for short sellers after these catalysts were realized.

Today, I’d like to analyze these two protocol upgrades from both bullish and bearish perspectives—covering mechanics, flywheels, and risks.

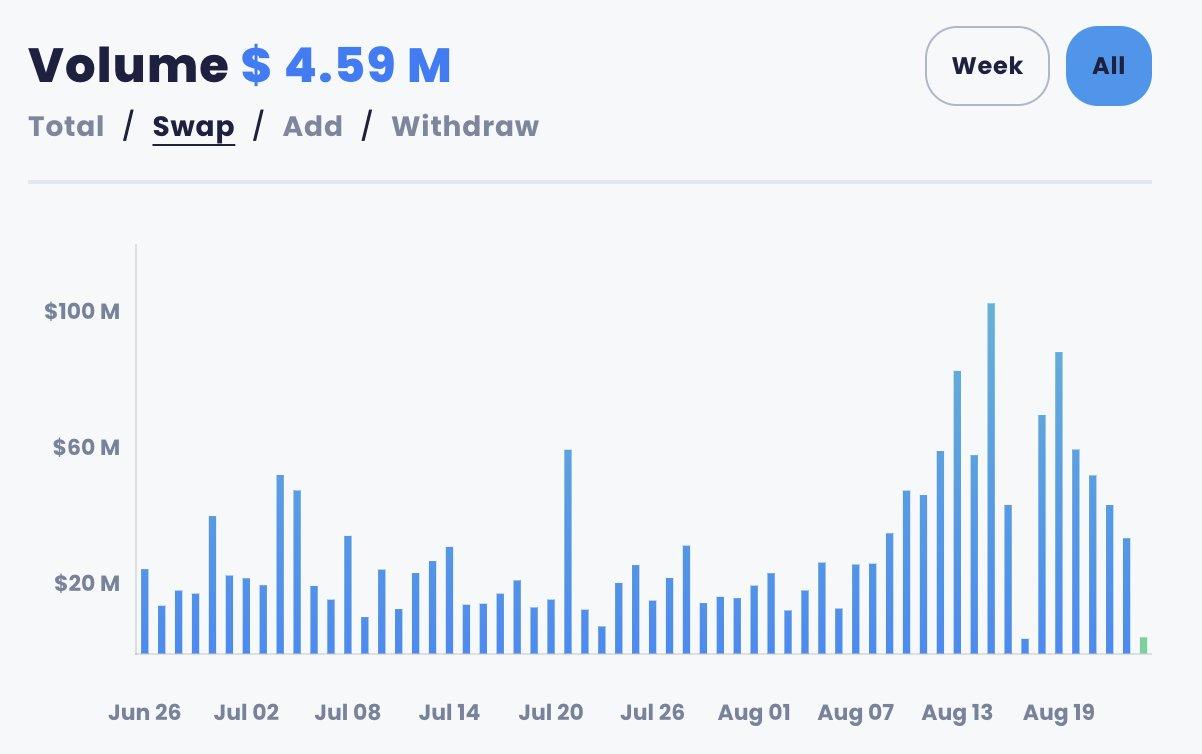

The first bullish update is "Streaming Swap," which essentially breaks large cross-chain orders into smaller ones to reduce slippage and improve user experience. This feature doesn’t directly impact the token price but indirectly drives value through increased on-chain activity.

Looking at the data below makes it clearer—after Streaming Swap launched, Thorswap saw a noticeable spike in volume, but this was followed by a sharp decline. Whether Streaming Swap’s impact is sustainable remains to be seen.

The other major feature is Lending. Given its complexity, I’ll break it down as simply as possible (this is my personal understanding—if there are inaccuracies, please correct me). Simplifying the lending model:

Suppose you deposit $10 worth of $BTC as collateral. Thor converts it into torBTC via the following path: BTC → RUNE → burn RUNE to mint torBTC. With an LTV (Loan-to-Value) ratio of 30%, you can borrow 3 TOR (a unit of account where 1 TOR = $1). If you want to borrow $3 worth of ETH, the protocol mints $3 worth of $RUNE, swaps it for $ETH, and disburses it to you. Repayment is calculated in USD value at borrowing time, not in crypto terms.

Next comes one of its most critical concepts: no liquidations, no interest, and no maturity date. Why can Thor afford this? Because your collateral is effectively converted into $RUNE. The protocol has little incentive for you to repay—the moment you deposited, your core asset was already transformed into $RUNE.

When you withdraw your collateral, if the $BTC/$RUNE rate stays constant, no additional action is needed. But if $BTC appreciates relative to $RUNE, Thor must mint extra $RUNE to cover the difference. For example, if $10 of $BTC doubles to $20 while $RUNE holds steady, the protocol must mint an additional $10 worth of $RUNE (inflation).

Therefore, the protocol actually prefers you *not* to withdraw your collateral. As long as you don’t repay, it continues burning $RUNE—this is the small flywheel Thor is building. (Note: loans must remain open for at least 30 days before repayment.)

That said, torBTC isn’t fully backed by $RUNE alone—it's backed 50% by $RUNE and 50% by $BTC. This reduces the protocol’s risk exposure—in simpler terms, if the collateral appreciates, Thor only needs to mint half as much $RUNE to settle the withdrawal.

This explains the fundamental rationale behind no liquidations, no interest, and no maturity dates: converting users’ core assets into the protocol’s native token. From a bullish perspective, both new products—Streaming Swap increasing trading volume, and Lending involving multiple token swaps that also boost volume—will increase activity on ThorSwap and burn $RUNE. Clearly, this is bullish.

Currently, lending supports only $BTC and $ETH, but support for more Layer 1 assets will follow. Lending is also a DeFi Lego piece within the Tor.Asset ecosystem—Thor may launch further products leveraging Tor.Asset to enhance capital efficiency for ThorSwap LPs.

Bearish On the flip side, if the bullish case hinges on deflation, the bearish argument centers on the potential risks introduced by the lending product. Although the protocol uses circuit breakers to cap debt size, during strong market rallies—especially when $RUNE underperforms the collateral assets—it could trigger excessive $RUNE inflation (current buffer: 15 million RUNE, hard cap: 500 million).

If the cap is reached and collateral assets continue rising (particularly the Asset/$RUNE ratio), things get ugly—bad debt emerges, and the protocol must use treasury funds to cover losses. Ultimately, Thor’s Lending module shifts risk onto the protocol itself and $RUNE holders. Moreover, due to multiple swap steps required by the product, lending incurs high friction costs, resulting in poor user experience.

Additionally, the protocol caps loan capacity at 500,000 $RUNE (currently ~$7–8 million). Only as more $RUNE gets burned will this limit increase. As lending scales, the 15 million $RUNE inflation buffer will likely prove insufficient to handle mass withdrawals.

While Thor has a positive flywheel, it also risks triggering a death spiral—if the 15 million newly minted $RUNE and treasury reserves cannot meet redemption demands, Thor enters a downward spiral.

Hence, we can understand why Thor sets collateral ratios between 200%-500%—to prevent users from taking excessive leverage—and why it reduces LTV as total collateral grows. However, lower LTV ratios discourage adoption, potentially stalling the upward flywheel.

As a result, Lending becomes somewhat of a gimmick—offering limited benefit to the protocol, neither compelling nor easily discarded. If it’s not clearly bullish, what else could it be but bearish?

After reading this analysis, what’s your choice? The red pill, or the blue pill?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News