a16z Releases the AI Application Top 100 List: ChatGPT’s Dominance Wanes, Global Market Splits into Three Camps

TechFlow Selected TechFlow Selected

a16z Releases the AI Application Top 100 List: ChatGPT’s Dominance Wanes, Global Market Splits into Three Camps

AI is becoming increasingly embedded in tools people already use.

Author: ethn, a16z

Translation & Compilation: TechFlow

TechFlow Intro: a16z has released the sixth edition of its Generative AI Consumer Applications Ranking. ChatGPT now boasts 900 million weekly active users, while Gemini and Claude are growing faster in paid subscriptions—the race for the “default AI assistant” has officially begun.

The biggest change in this edition is the inclusion of established products like CapCut, Canva, and Notion—where AI features have become core—to the ranking, alongside first-time coverage of Agents, AI browsers, and desktop-native tools.

Olivia Moore, Partner at a16z’s Consumer team, authored this report, which stands among the most systematic publicly available data tracking the generative AI consumer application landscape today.

Full Report Below:

Three years ago, we published the first edition of this ranking, with a simple goal: identify which generative AI products were truly being adopted by mainstream consumers. Back then, the line between “AI-native” companies and others was clear-cut. ChatGPT, Midjourney, and Character.AI were built from the ground up around foundation models; the rest of the software world was still figuring out how to apply the technology.

That boundary no longer holds. CapCut—a video editor with 736 million monthly active mobile users—relies entirely on AI for its most popular features: background removal, AI effects, auto-captions, and text-to-video. Canva’s growth engine runs entirely on its Magic Suite of AI tools. Notion’s paid AI add-on rate surged from 20% to over 50% within a year, and AI features now contribute roughly half of the company’s ARR.

Starting with this edition, we’ve expanded our scope to include all consumer-facing products where generative AI has become a core part of the experience—including CapCut, Canva, Notion, Picsart, Freepik, and Grammarly. We believe this better reflects how people actually use AI today—though most top-ranked products remain AI-native.

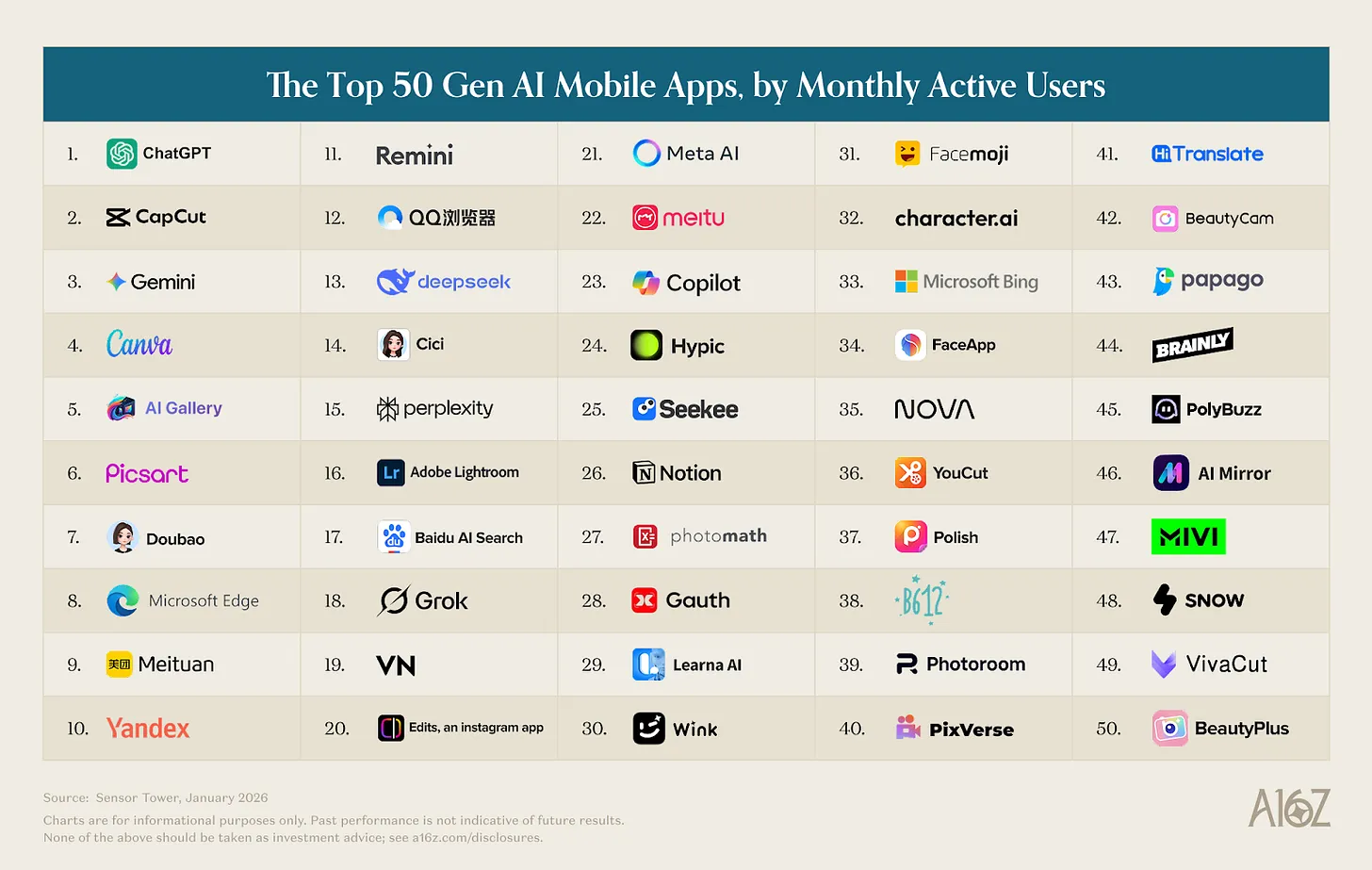

Caption: Full Top 100 Generative AI Consumer Applications Ranking, March 2026 Edition

As before, web rankings are based on monthly unique visits (data source: SimilarWeb, as of January 2026), and mobile rankings on monthly active users (data source: Sensor Tower, as of January 2026). Below are our key findings:

1. ChatGPT Leads—but the “Default AI” Battle Has Begun

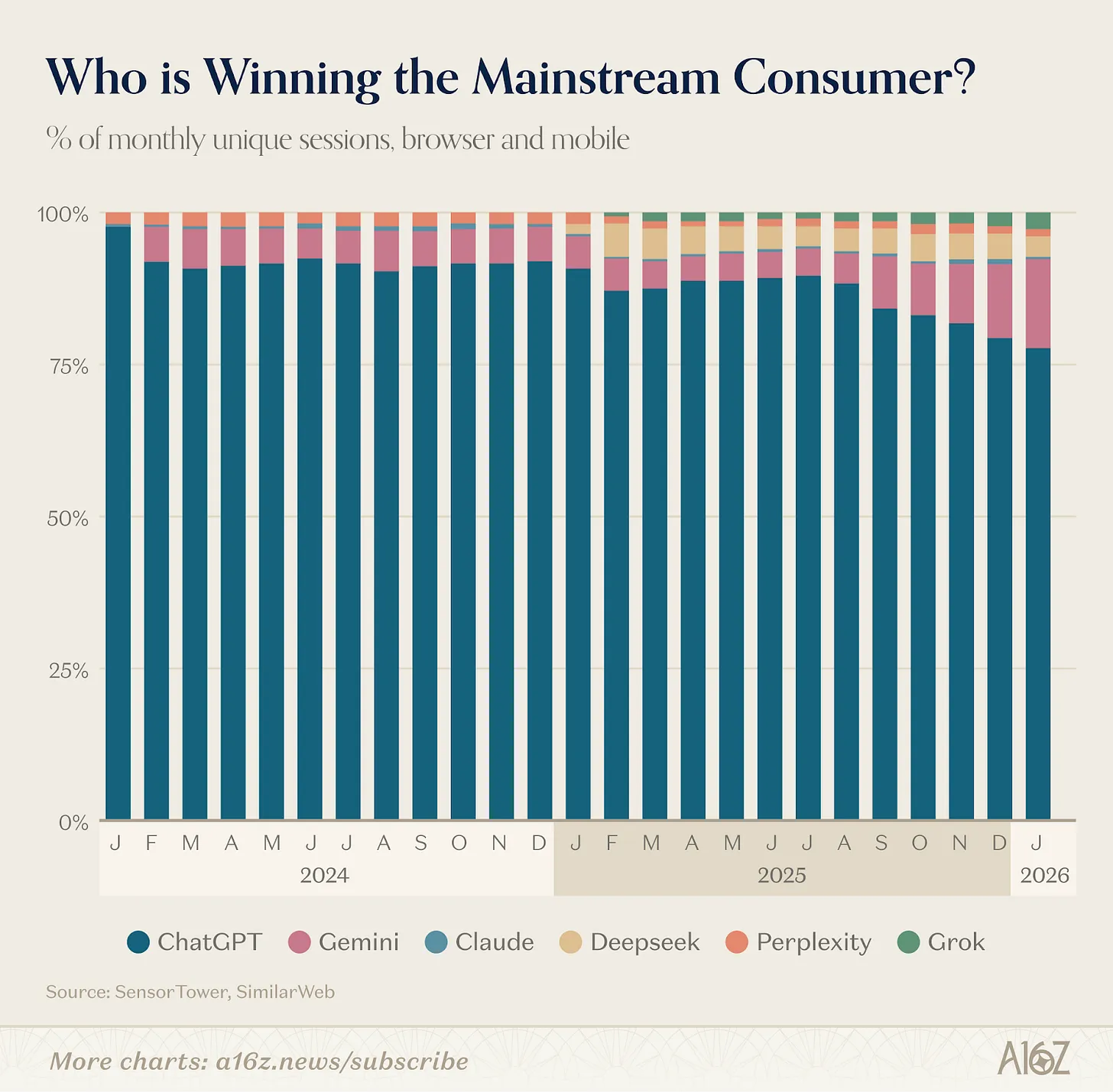

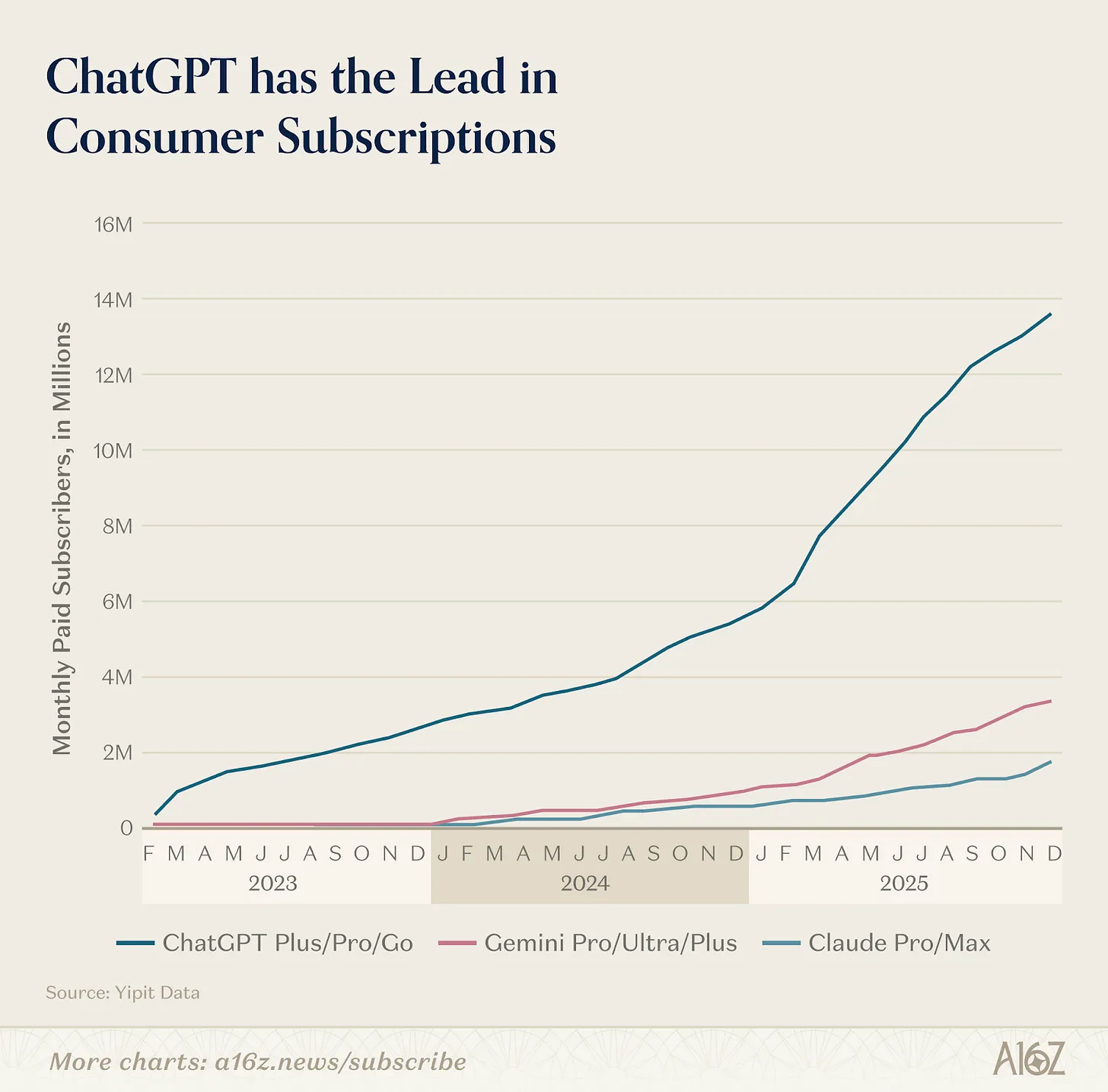

ChatGPT remains the largest consumer AI product—and by a wide margin. Its web traffic is 2.7x that of second-place Gemini; its mobile MAUs are 2.5x Gemini’s. Over the past year, ChatGPT’s weekly active users grew by 500 million, reaching 900 million. Given how difficult growth becomes at scale, this figure is staggering—more than 10% of the global population uses ChatGPT every week.

Yet we’re seeing the field broaden, as other general-purpose platforms gain traction in specific use cases. Both Gemini and Claude accelerated their U.S. paid subscription growth over the past year (though they still trail ChatGPT in absolute scale—ChatGPT’s paying users outnumber Claude’s by 8x and Gemini’s by 4x). Per Yipit Data, as of January 2026, Claude’s paid users grew over 200% year-over-year, while Gemini’s grew 258%. We’re also seeing more “multi-platform usage”: roughly 20% of ChatGPT’s weekly web active users also used Gemini in the same week.

What’s happening? Competitors are pushing hard. Google scored big in creative models—Nano Banana generated 200 million images in its first week, driving 10 million new users to Gemini; Veo 3 is widely regarded as a breakthrough moment for AI video. Anthropic focused on professional users, launching Cowork, Claude in Chrome, Excel and PowerPoint plugins—and critically, Claude Code.

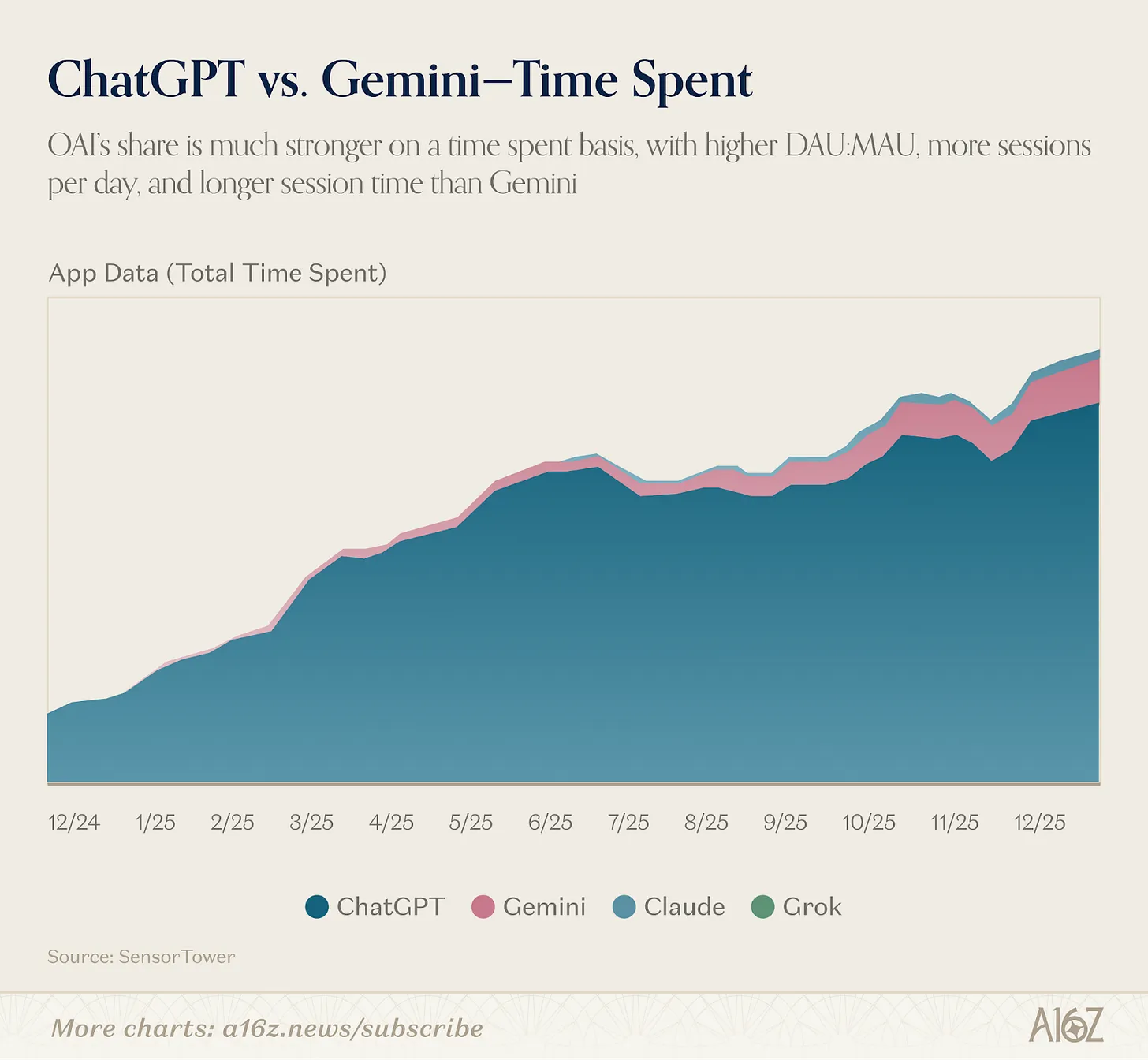

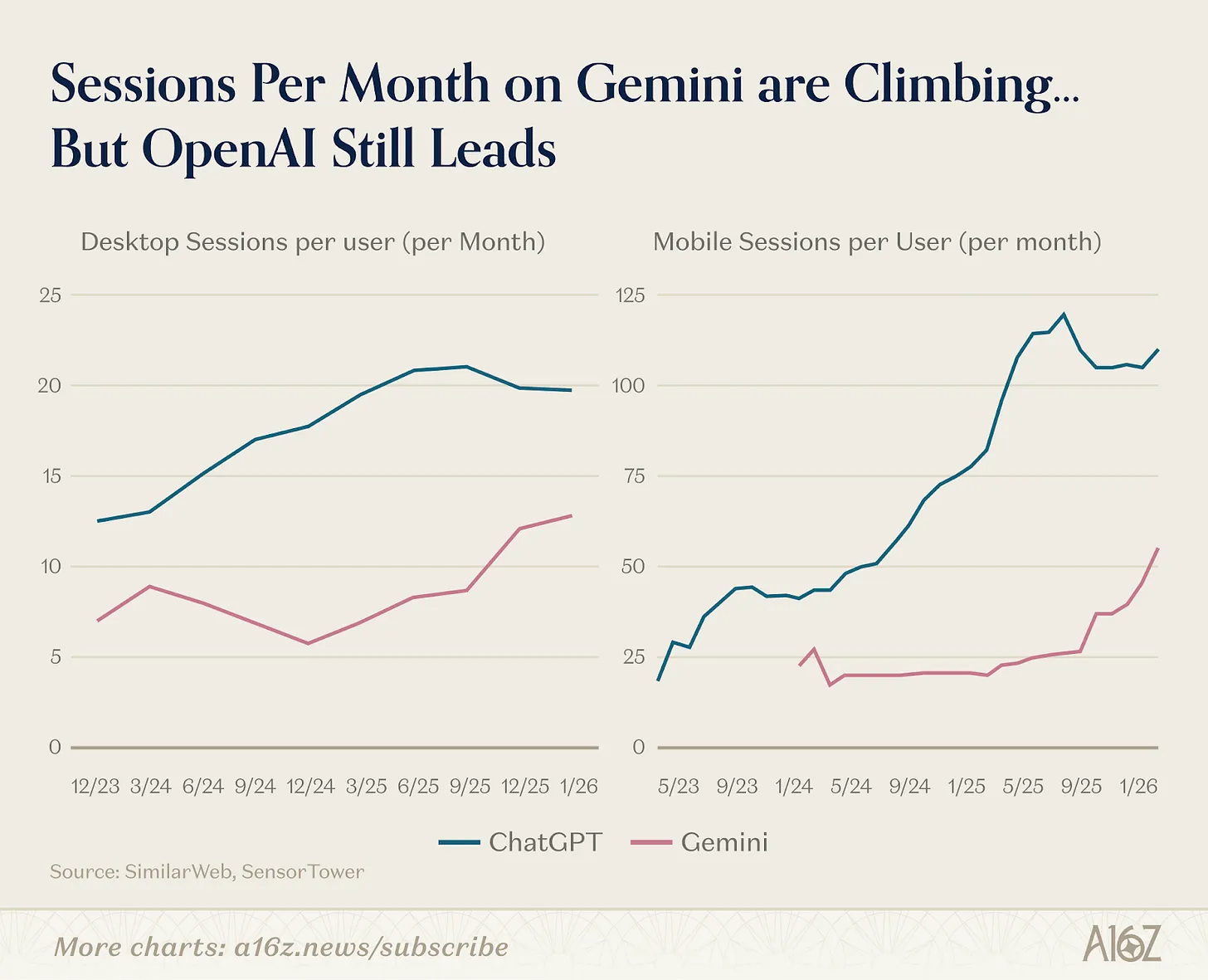

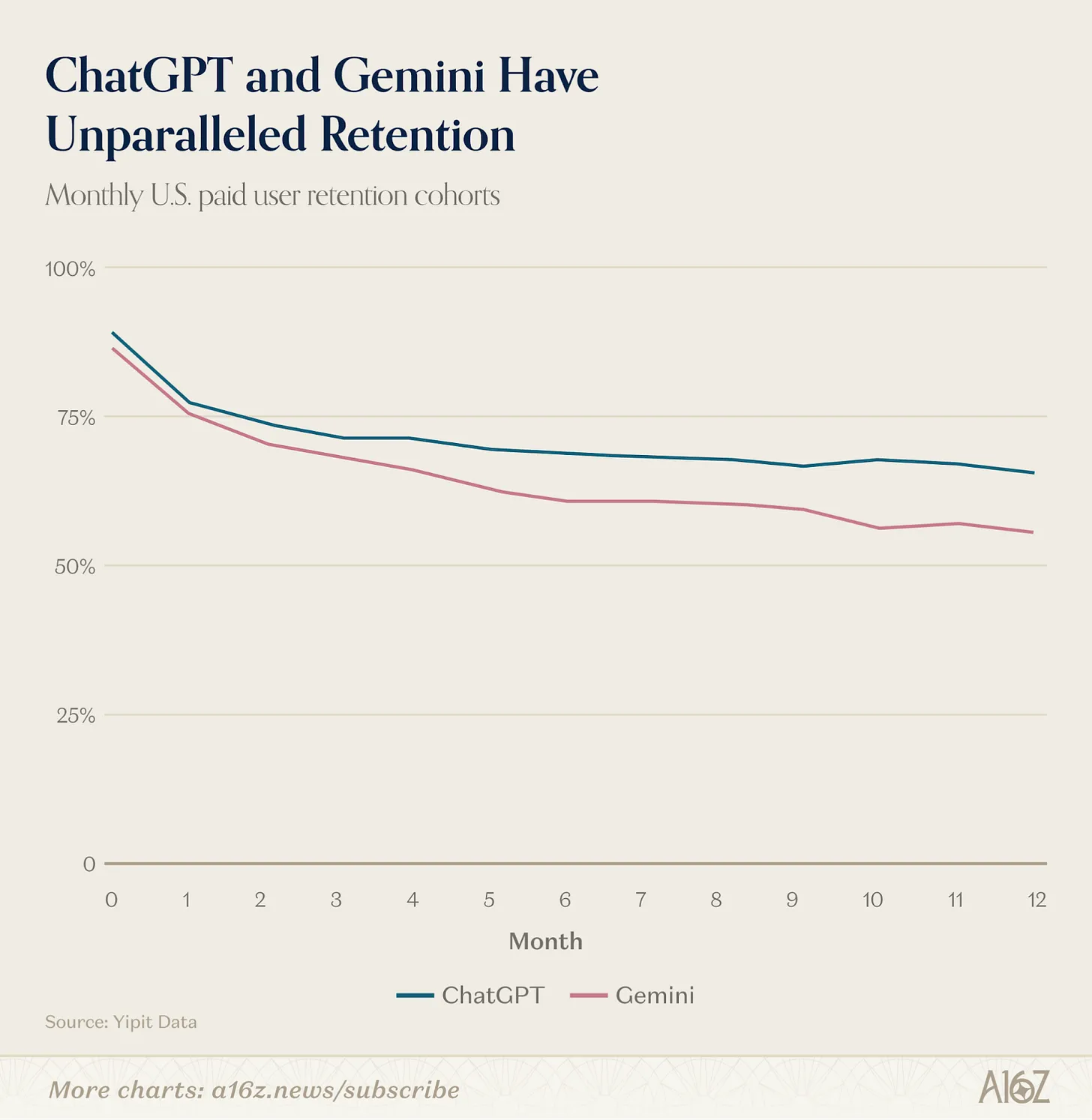

This race isn’t just about who leads today—it’s about who builds structural moats. Context accumulates: the more an LLM learns about you, the better its outputs become, and the harder it is to leave. Early data shows Gemini’s web-based monthly sessions per user are rising—but ChatGPT still leads by 1.3x. On mobile, ChatGPT’s advantage is even larger: its monthly sessions per user are 2.2x Gemini’s. Per Yipit Data, both platforms boast industry-leading paid-user retention rates in the U.S. consumer segment.

The next layer of lock-in comes from app stores. Both ChatGPT and Claude have launched connector ecosystems—ChatGPT with GPTs and Apps, Claude with MCP integrations and Connectors—enabling users to build workflows atop their assistants. Once users configure their AI to connect calendars, email, and CRMs, switching costs skyrocket. Developers may concentrate efforts on the platform with the largest user base—creating a flywheel effect akin to early platform wars.

We’re already seeing strategic divergence across platforms. Sam Altman previously stated OpenAI wants to “bring AI to the billions who can’t afford subscriptions”—which explains its move into advertising. He also announced plans for a “Sign in with ChatGPT” identity layer, positioning the AI assistant as the default interface between consumers and the internet. The ambition is for ChatGPT to be the starting point for everything: shopping, booking hotels, web browsing, health management, and daily life.

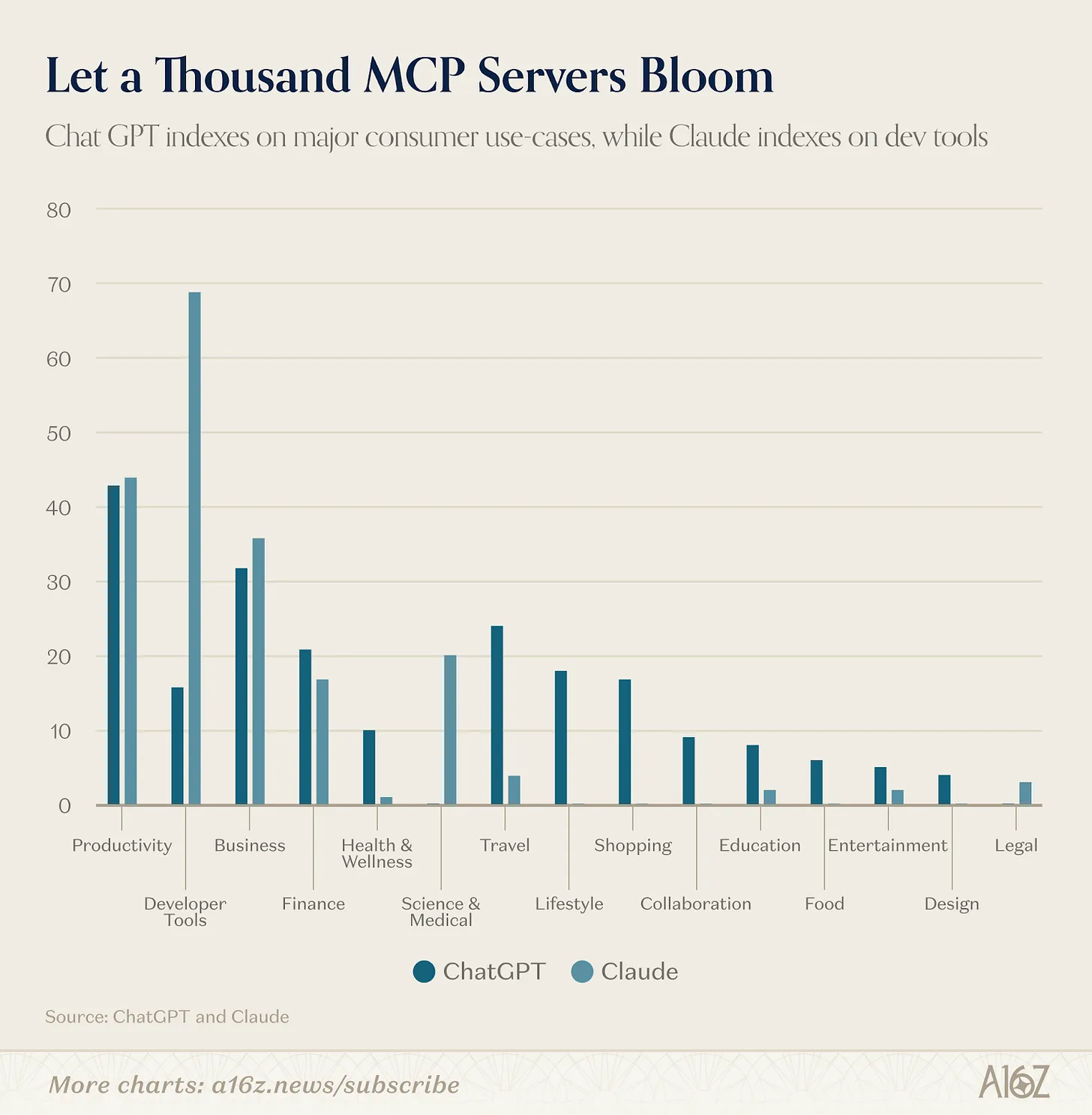

The app directories already reflect this difference. As of late February, ChatGPT’s App Store covered 13 categories and 220 apps. Claude offers roughly 160 curated connectors plus ~50 community MCP servers. Yet only 41 apps overlap—about 11% of the combined directory—and nearly all are universal productivity tools everyone needs: Slack, Notion, Figma, Gmail, Google Calendar, HubSpot, and Stripe.

Beyond these core utilities, the two platforms diverge almost entirely. ChatGPT has over 85 exclusive apps in travel, shopping, food, health, lifestyle, and entertainment—categories where Claude has virtually none. These are all consumer transactional use cases: booking flights on Expedia, grocery shopping via Instacart, browsing homes on Zillow, or tracking nutrition on MyFitnessPal. This is the most aggressive “super-app” play among all AI companies. In contrast, Claude’s exclusive integrations skew professional: financial data terminals (PitchBook, FactSet, Moody’s, MSCI), developer infrastructure (Sentry, Supabase, Snowflake, Databricks), scientific and medical tools (PubMed, Clinical Trials, Benchling), and an open-source MCP community with no ChatGPT counterpart.

Anthropic appears laser-focused on advanced AI users—developers, knowledge workers, etc.—who are both willing and able to pay premium subscription fees. While ChatGPT also serves this cohort (e.g., Codex, Frontier), it simultaneously aims to become a genuinely mass-market platform—a path that could unlock broader monetization as its user base scales. It’s already testing ads, and transaction fees represent a natural expansion vector.

If AI assistants evolve beyond chat windows into operating-system-level environments, this competition may ultimately resemble the mobile OS wars—not the search wars—where two fundamentally different platforms each build trillion-dollar ecosystems, rather than one capturing 90% market share.

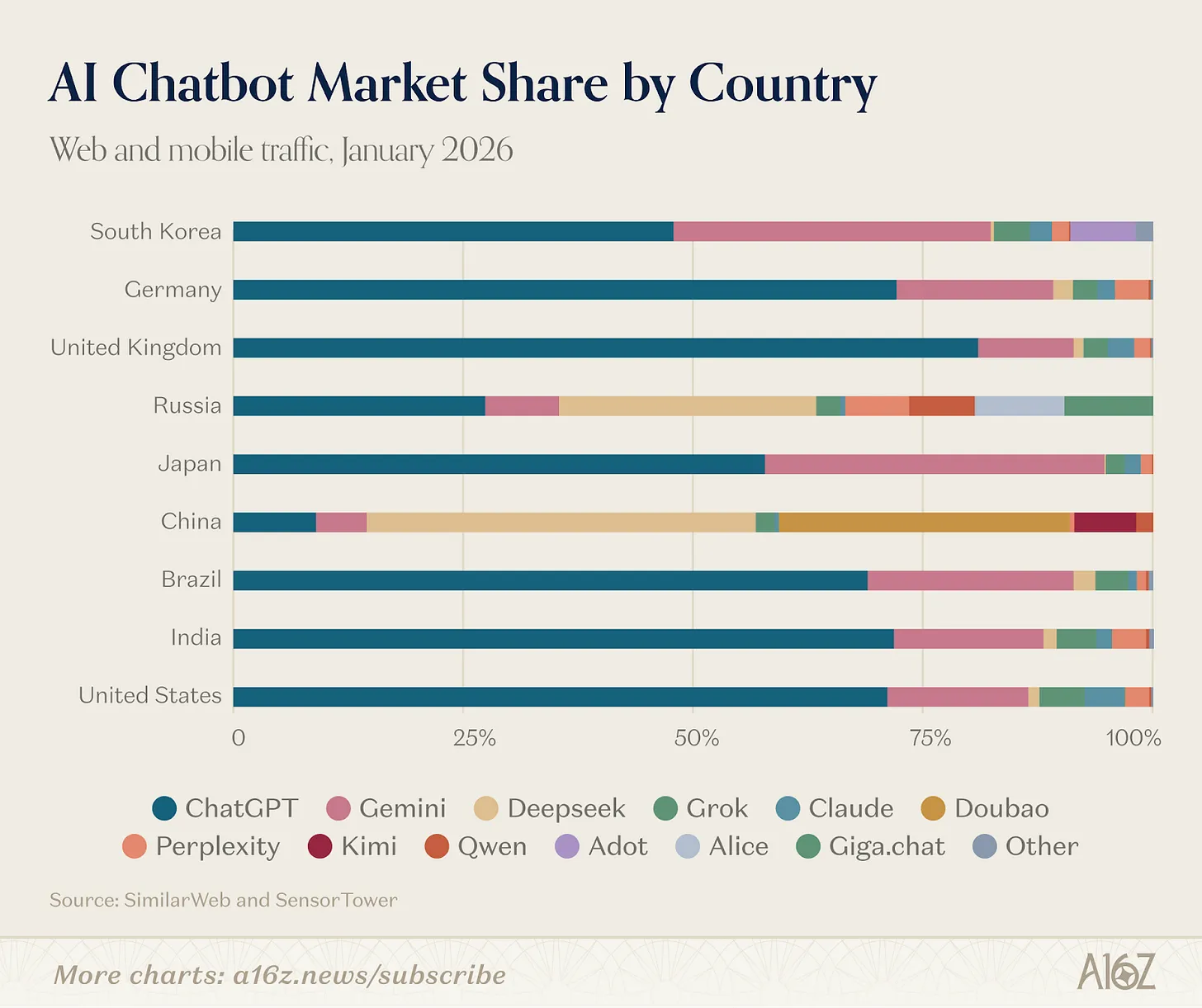

2. Global Usage Is Fragmenting by Product

Geographically, the AI market is splitting into three distinct ecosystems—and the gaps between them are widening.

Western AI tools share highly overlapping user bases. ChatGPT, Claude, Gemini, and Perplexity all draw core users from the same pool: the U.S., India, Brazil, the U.K., and Indonesia—just in varying orders. None see significant usage in China or Russia. The reason is policy: since 2022, Western tech sanctions have restricted Russian access to U.S.-based AI tools; China mandates registration, local data storage, and compliance with censorship rules for AI providers.

DeepSeek is the only product spanning multiple blocs. Its web traffic distribution is China (33.5%), Russia (7.1%), and the U.S. (6.6%); mobile follows a similar pattern. Chinese users also heavily adopt ByteDance’s Doubao and domestic product Kimi.

Russia—virtually absent as a standalone market in earlier editions—is now emerging as the third pole, with DeepSeek ranking second in penetration. The Yandex browser, integrated with Alice AI Assistant, hit 71 million monthly active users on mobile, placing it among the top ten global mobile AI products. Sber’s GigaChat also debuted on our web ranking this edition. This mirrors China’s trajectory—compressed in time: sanctions created a vacuum, and domestic products filled it within two years.

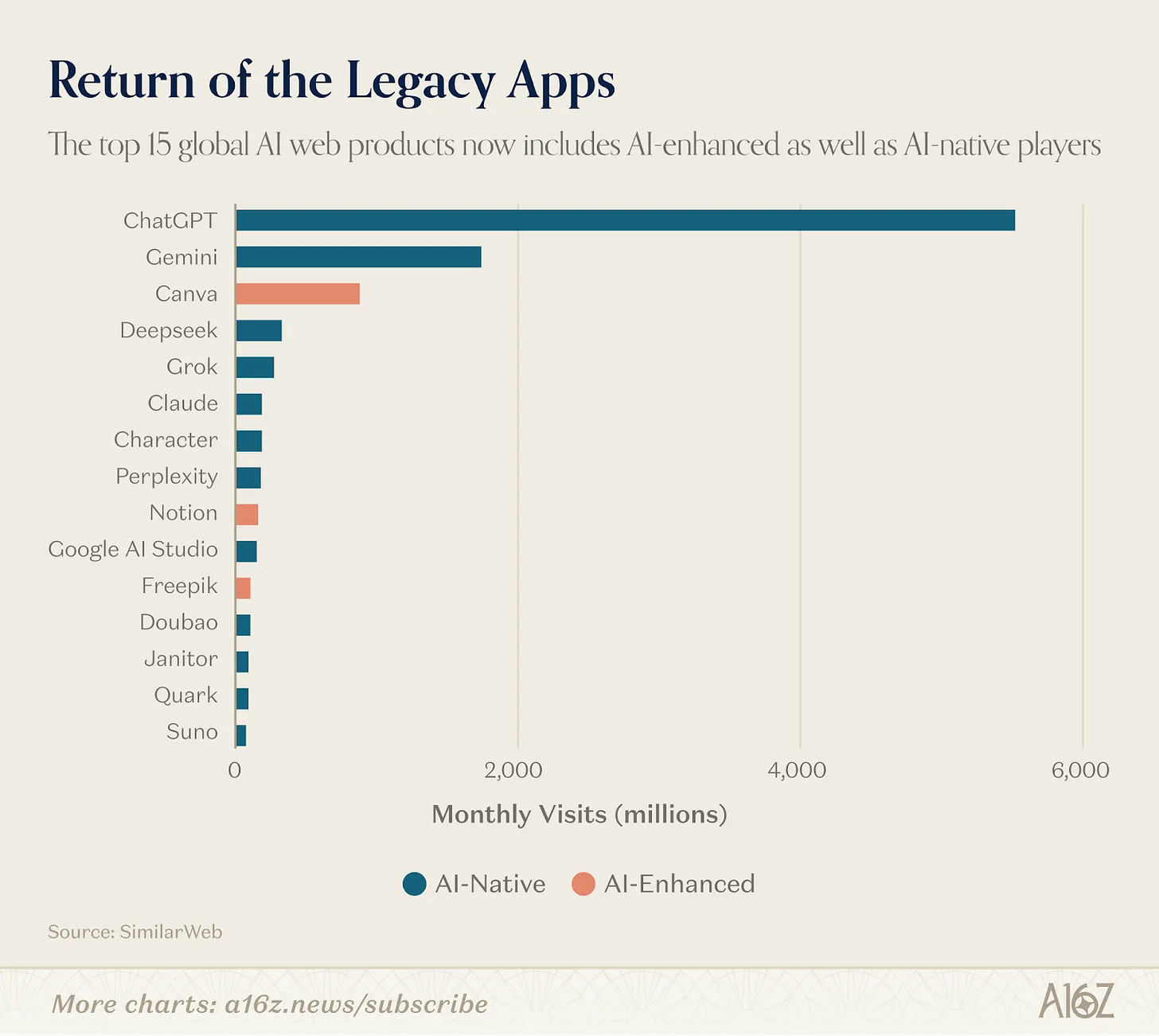

To measure AI adoption per capita, we built a simple index combining per-capita web visits and per-capita mobile MAUs, scored on a 0–100 scale. The results redefine the geographic landscape. Singapore ranks first, followed by the UAE, Hong Kong, and South Korea. The U.S.—birthplace of most AI products—ranks 20th.

Caption: Generative AI Per-Capita Adoption Index (0–100), with Singapore leading and the U.S. at #20

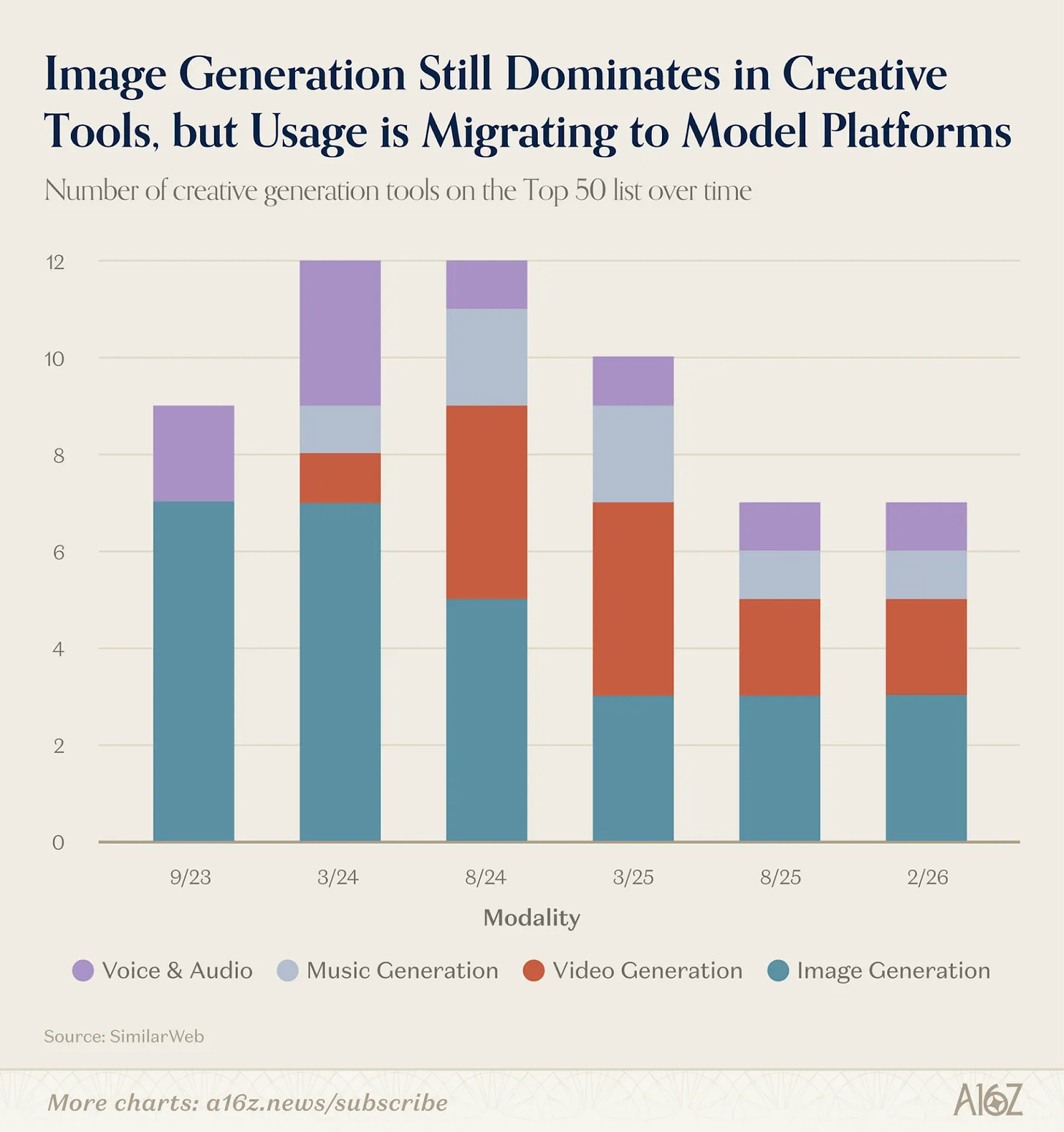

3. Creative Tools Are Being Reshuffled

Midjourney, DALL-E, and Stable Diffusion brought most early users into the generative AI world—each launched before ChatGPT. Image-generation tools not only dominated the creative category (video and audio generation arrived later) but consistently ranked near the top of our first three editions. This category has since undergone major shifts.

In the first edition (September 2023), 7 of the 9 web-based creative tools were image generators. Three years later, only 3 image generators remain on the list—but creative tools still total 7. The difference lies in what filled the gap: video, music, and voice products replaced image generators.

The story of image generation is one of bundling and absorption. As built-in image models in ChatGPT (GPT Image 1.5) and Gemini (Nano Banana) improved in quality, the bar for standalone image products rose sharply. In our first edition, Midjourney ranked in the top 10; today it sits at #46. Remaining players—Leonardo, Ideogram, CivitAI—tend to serve specific creative communities, differentiating through opinionated features rather than competing head-on with general-purpose generators.

Video generation is the most volatile category in this edition. Kling AI, Hailuo, and Pixverse have all built real user bases, with China-developed models continuing to lead in output quality. Apps built on Seedance 2.0 wouldn’t surprise us on next edition’s list. Veo 3—the first U.S. model to meaningfully close the gap—drove traffic growth for Google Labs (rising from #36 to #25).

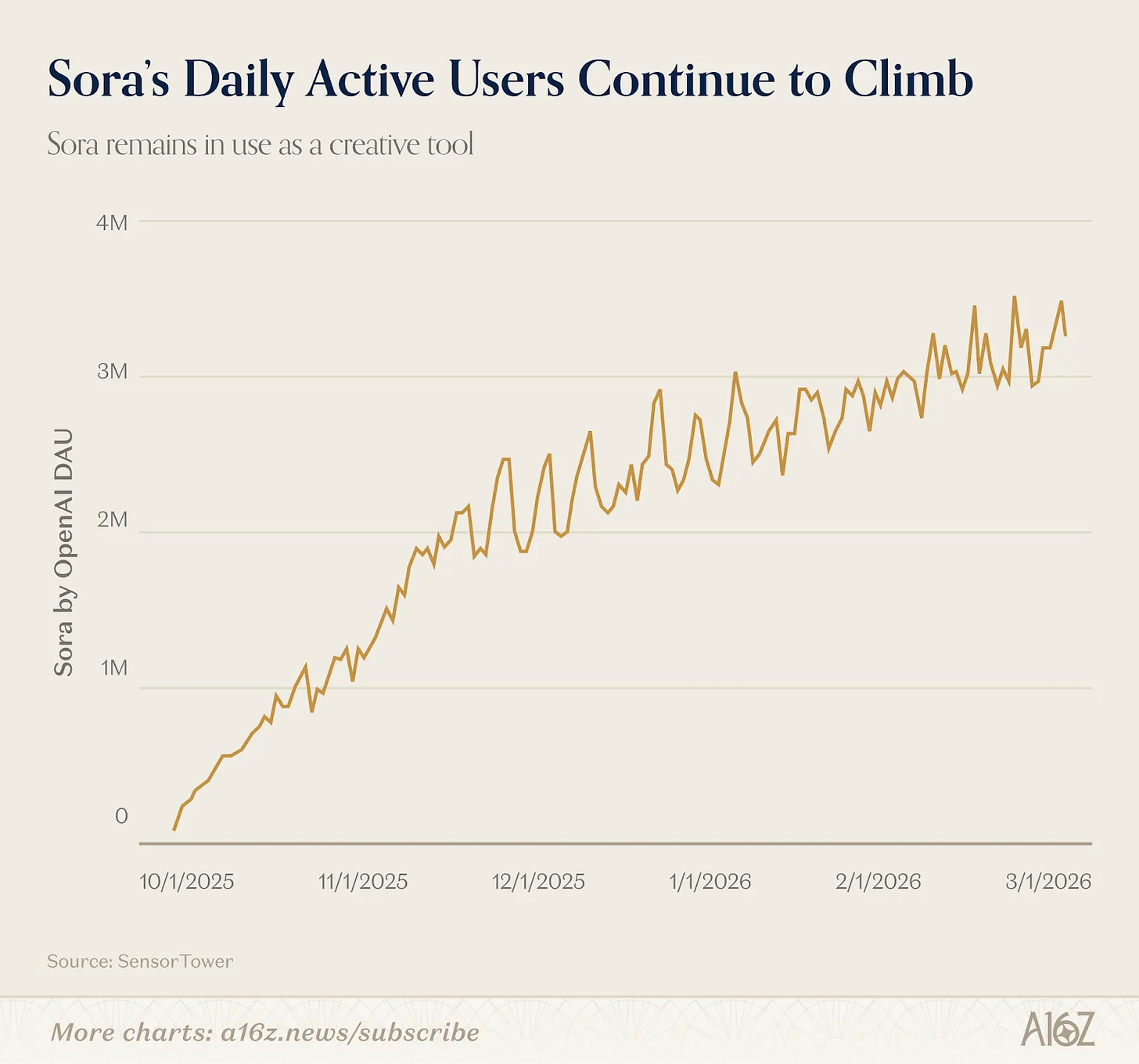

Who’s missing? Sora. OpenAI launched Sora 2.0 as a standalone app in September 2025, enabling users to upload their digital avatars as Cameos to generate videos featuring real people. Sora held the #1 spot on the U.S. App Store for 20 consecutive days, hitting 1 million downloads faster than ChatGPT did. Downloads later tapered off because Sora failed to sustain viral social growth (no one has yet cracked AI × social)—so it didn’t make this edition’s mobile ranking. Still, Sensor Tower data shows Sora maintains over 3 million daily active mobile users; AI video creators continue using the model—even if they post outputs elsewhere.

Music and voice tools prove more defensible. Suno retained last edition’s rank (#15). ElevenLabs has appeared on every edition since September 2023; its core capabilities—voice cloning, dubbing, audio production—remain specialized enough that they haven’t yet been reduced to checkbox features inside giant platforms.

In summary: when model giants and large players like Google and OpenAI invest heavily in a creative domain (images, and increasingly video), standalone products face traffic compression—though niche, opinionated, or higher-LTV offerings outside the mainstream retain space. Where giants haven’t yet invested (music, voice), independent players enjoy more breathing room.

4. Agents Have Arrived

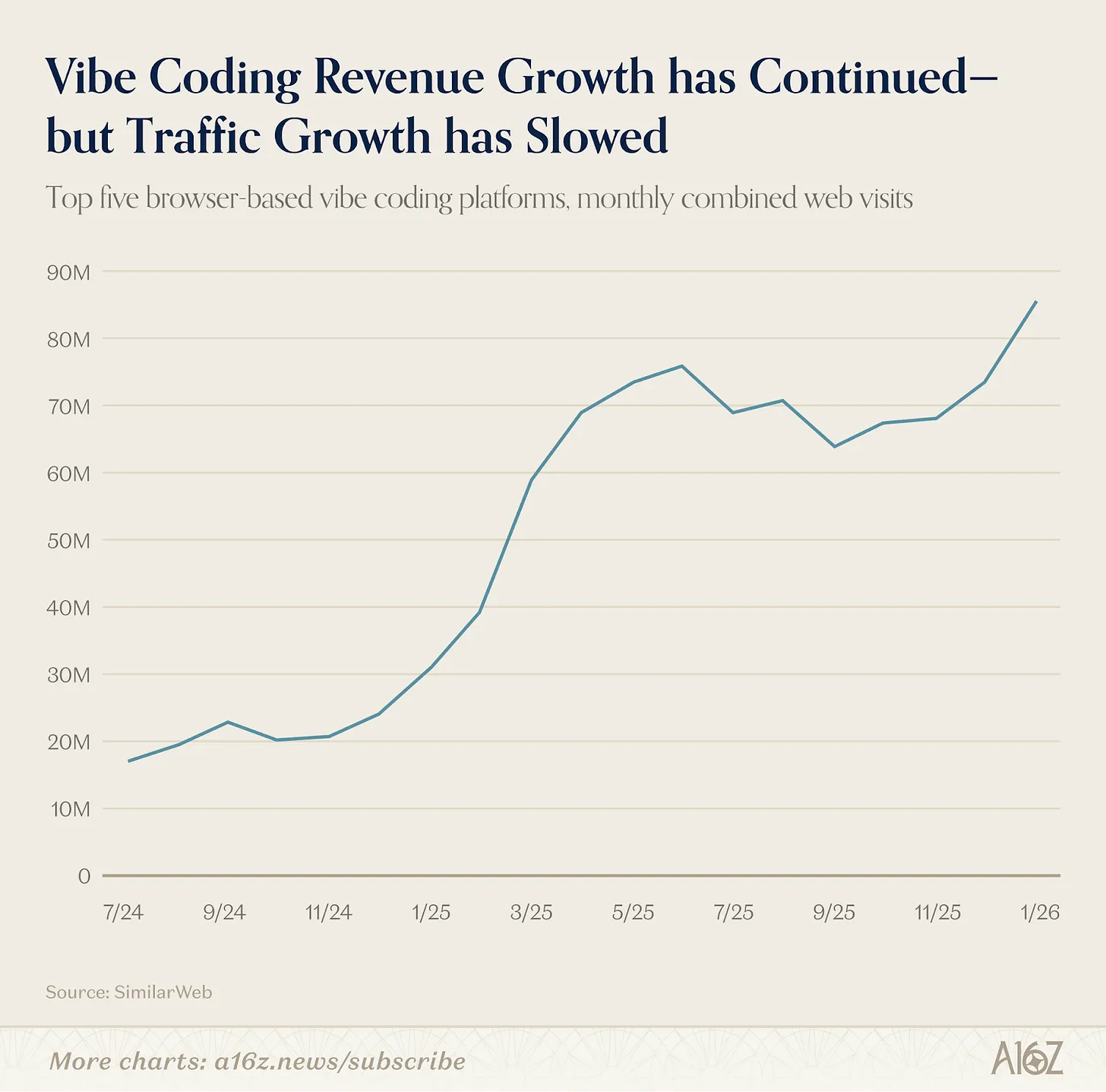

The shift toward agentified AI didn’t begin with this edition—it started last edition, under the banner of “vibe coding.” When Lovable, Cursor, and Bolt appeared on our March 2025 ranking, they signaled something new: AI products weren’t just answering questions or generating media—they were building things for users. That’s agent behavior—albeit confined to a vertical domain.

Vibe coding proved its stickiness among technical (and semi-technical) users. This edition includes Replit and Lovable, along with Claude Code (via Claude). More growth remains possible, as this trend hasn’t yet penetrated the mass market. Traffic for the top five vibe coding platforms continues to rise—though growth has slowed from initial explosive phases—while many products’ revenues keep climbing, driven by deeper usage intensity among developers and teams.

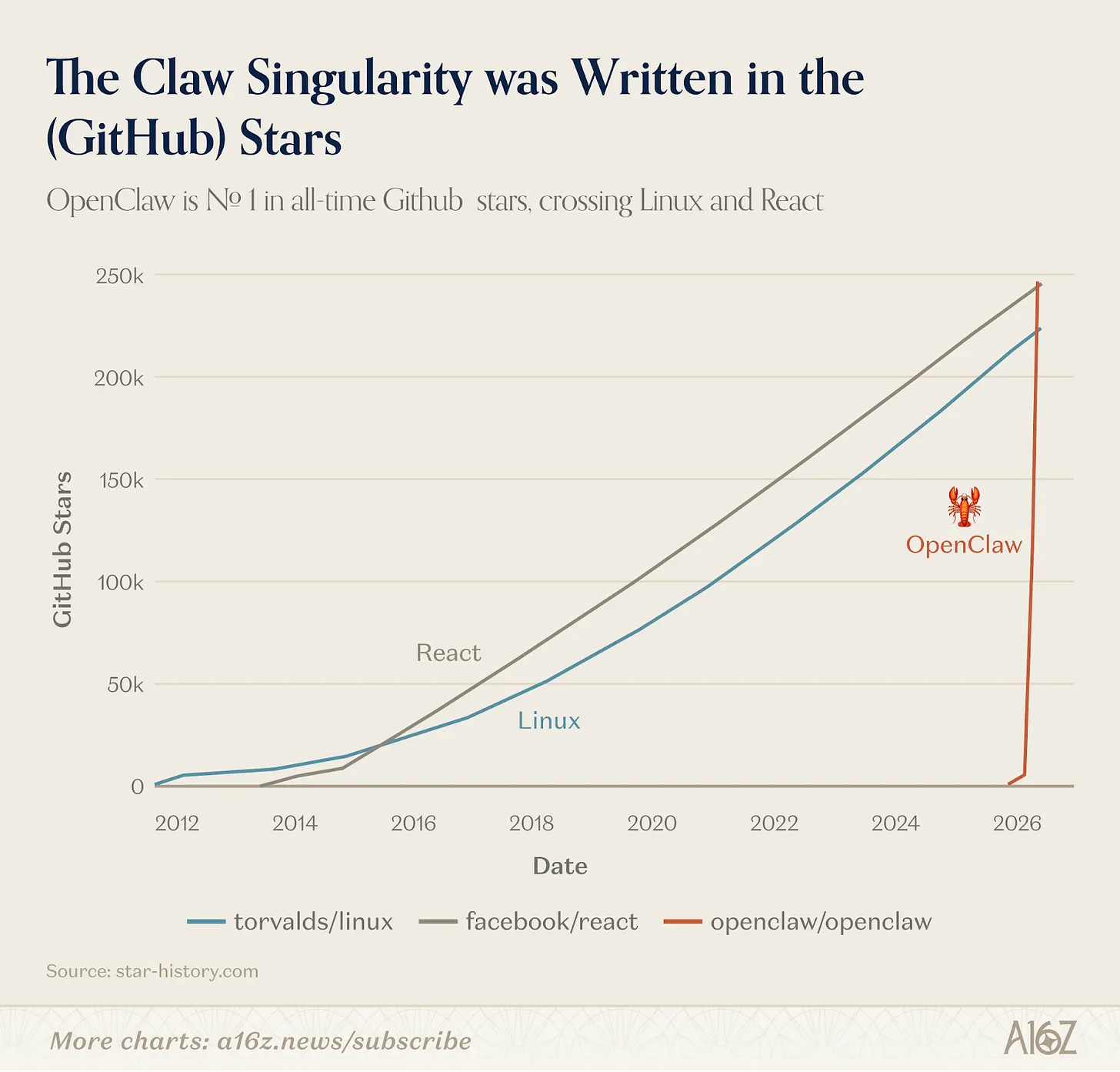

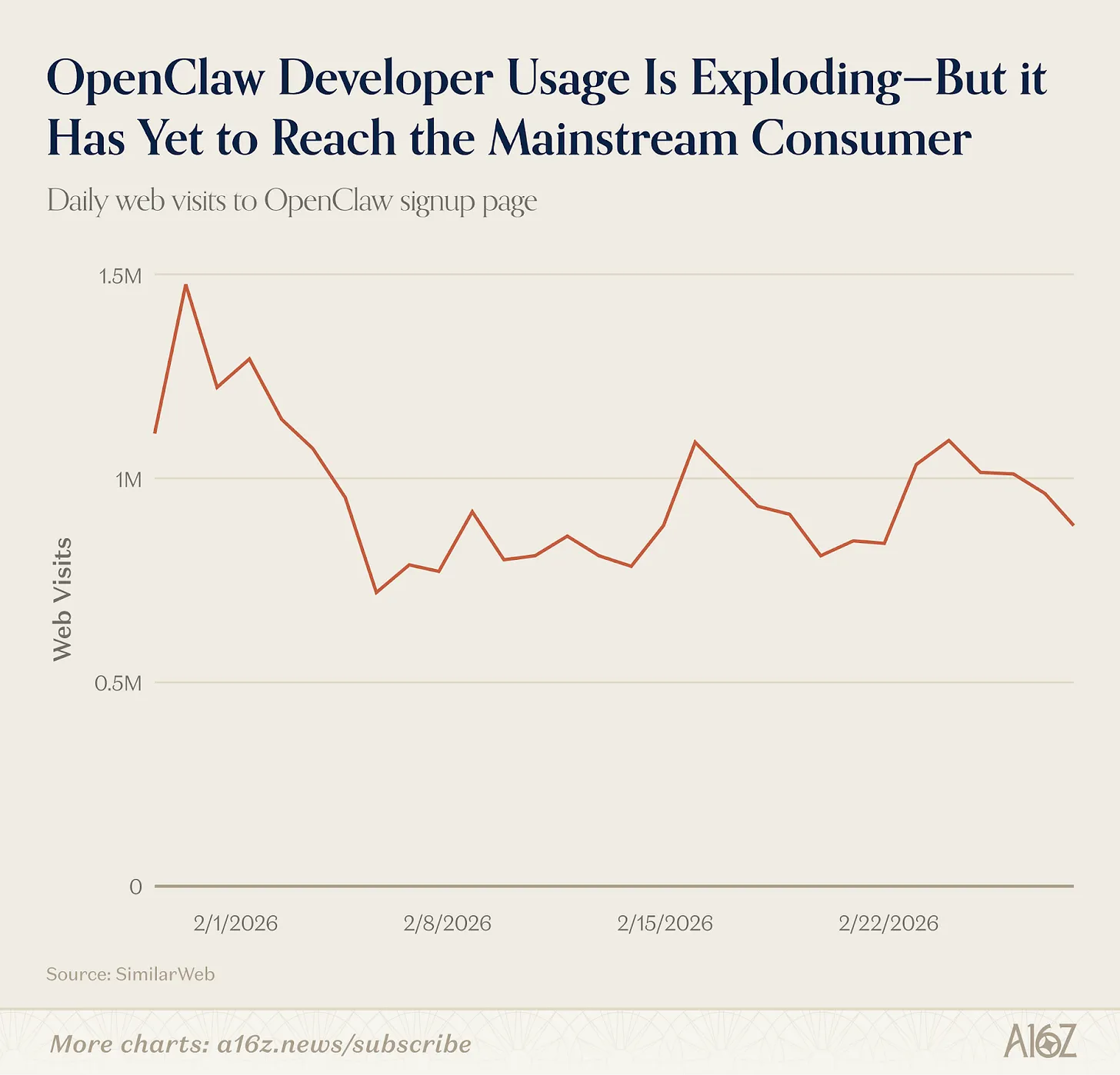

More recently, general-purpose agents have emerged. In January 2026, an open-source project called OpenClaw—originally a side project by a solo developer—exploded onto GitHub with 68,000 stars and mainstream media coverage, all within weeks. Created by Austrian developer Peter Steinberger, OpenClaw is a locally run AI agent capable of connecting to your messaging apps and executing multi-step tasks on your behalf.

If ChatGPT marked the moment consumers discovered AI could converse, OpenClaw may mark the moment they discover AI can act. The product ignited the developer community—if we extended our analysis window to February instead of January, OpenClaw would rank in the top 30 on web.

But OpenClaw isn’t yet a consumer product—installation and maintenance require terminal proficiency. OpenClaw continues gaining momentum among technical users, becoming GitHub’s most-starred project in early March—surpassing React and Linux. Yet it hasn’t yet “graduated” to true mainstream adoption—at least judging by flat new-visitor growth on OpenClaw’s installation webpage. The project was acquired by OpenAI in February 2026, suggesting a more user-friendly version may soon arrive.

OpenClaw isn’t the only general-purpose agent on the list. Manus and Genspark also made the cut—both platforms let consumers delegate open-ended tasks (research, spreadsheet analysis, slide creation) to AI, which executes the entire workflow end-to-end. Manus appears for the second time; after its prior appearance, Meta acquired it in December 2025 for ~$2 billion. Genspark is new this edition—the company raised a $300 million Series B earlier this year and announced $100 million in annualized revenue.

On mobile, consumers typically interact with agents via text—not dedicated apps. During setup, users connect OpenClaw to WhatsApp, Telegram, and Signal, issuing commands like they would to a friend; OpenClaw then executes tasks in the background. Other products like Poke offer similar agent experiences via SMS.

These products will compete directly with the general-purpose LLM assistants consumers use daily—ChatGPT, Claude, and Gemini—as those giants build their own connectors and app ecosystems. Will consumers choose one as their primary agent? The next six months will tell.

5. AI Is Moving Beyond Browsers and Apps

Every previous edition of this ranking evaluated AI products using two metrics: web traffic and mobile MAUs. But a new class of AI products is emerging—one invisible to both metrics. Some of the most important consumer AI growth over the past year has occurred in products completely undetectable through these two dimensions.

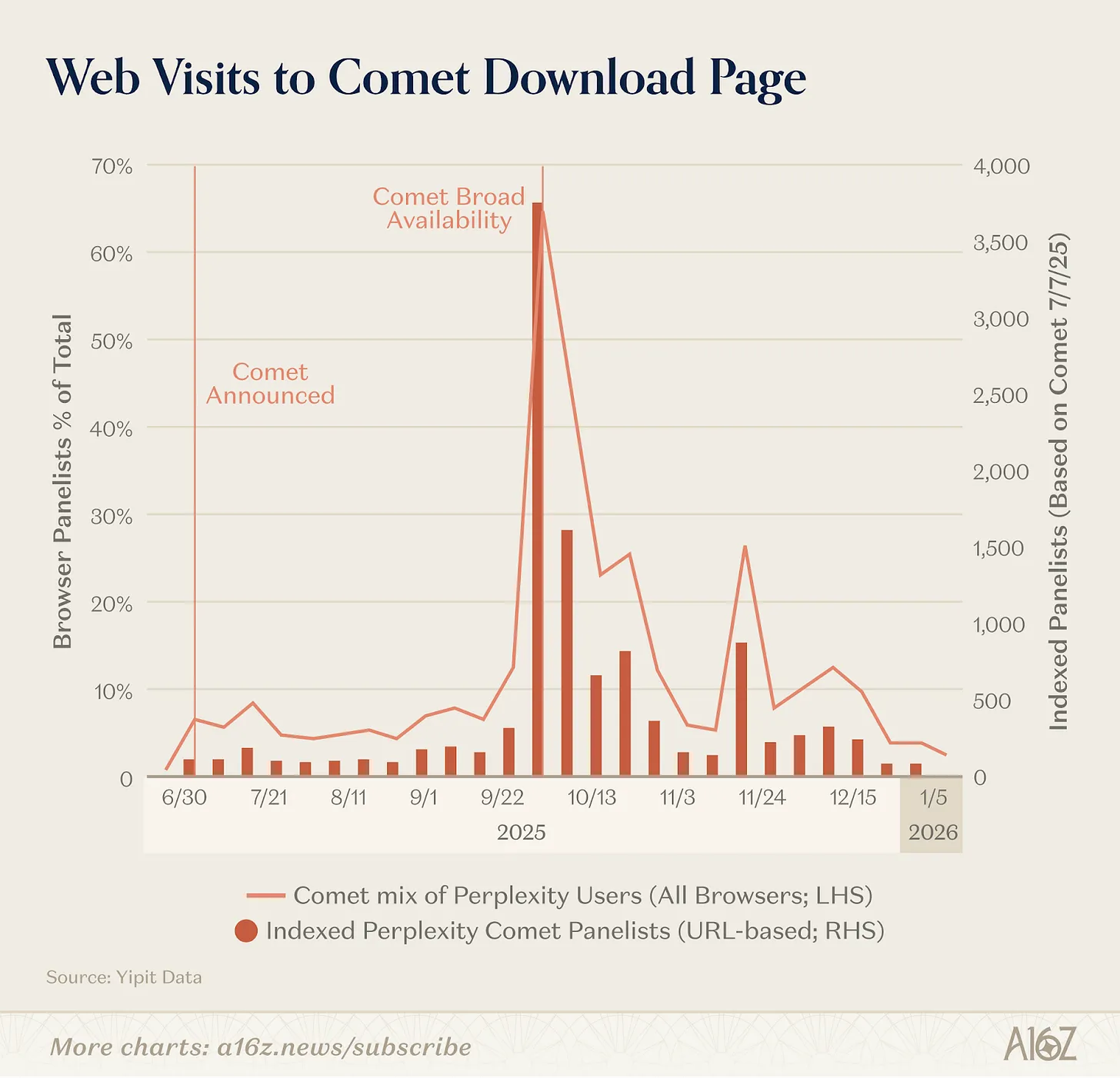

The most obvious shift is that browsers themselves are becoming AI products. Over the past nine months, OpenAI launched Atlas (a browser embedding ChatGPT on every page), Perplexity introduced Comet, and Browser Company (later acquired by Atlassian) released Dia. Per Yipit Data, Perplexity’s Comet had the largest market impact (measured by download-page visits), though no AI browser has yet achieved accelerating growth.

Other AI giants chose to embed AI into existing browsers rather than launch standalone AI browsers. Google integrated Gemini into Chrome and released a test version of Disco, which dynamically generates web apps based on users’ browser tabs. Anthropic launched Claude in Chrome, enabling users to connect their Claude or Claude Code sessions to drive actions directly on web pages.

Native desktop AI tools are growing even more explosively—especially developer tools. Claude Code—a command-line developer agent—reached $1 billion in annualized revenue within six months. OpenAI launched a standalone Mac-native Codex app, which the company says reached 2 million weekly active users by early March, up 25% week-over-week. Cursor retained its position in the top 50 on web.

For pure consumers, the most common native desktop AI applications are voice-related. Note-taking tools like Fireflies, Fathom, Otter, TL;DV, and Granola reach users via PLG (product-led growth) and are gradually penetrating enterprises—the top five players collectively attract over 20 million visitors. Workspace applications like Notion (appearing on this edition’s list for the first time) increasingly integrate AI via note-takers, research agents, and even task automation.

Finally, AI is embedding ever more deeply into tools people already use. Anthropic launched Claude in Excel and Claude in PowerPoint. OpenAI rolled out ChatGPT for Excel. Google deepened Gemini’s integration across Workspace—Docs, Sheets, Gmail, and Meet all now feature native AI capabilities. In January 2026, Google launched Personal Intelligence, connecting Gemini to Gmail, Google Photos, YouTube, and Search—enabling the assistant to reference your hotel bookings, purchase history, photo albums, and viewing records without requiring explicit input.

The implication for this ranking is clear: our methodology increasingly underestimates the AI products people actually use most. A developer spending eight hours daily inside Claude Code—or a knowledge worker dictating every email via Wispr—are heavy AI users, yet nearly invisible in web traffic data. As AI evolves from a destination into a feature, our measurement framework must evolve too.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News