"King of Leverage" Arthur Hayes: From Financial Prodigy to Crypto Enthusiast, the Creator of Crypto Perpetual Swaps

TechFlow Selected TechFlow Selected

"King of Leverage" Arthur Hayes: From Financial Prodigy to Crypto Enthusiast, the Creator of Crypto Perpetual Swaps

An excellent educational background, a bold yet meticulous mindset, a value system that追求 high risk and high return, and a rebellious adventurer's personality have shaped Hayes as he is today.

Arthur Hayes, born in 1985, is an African American entrepreneur, banker, and co-founder of BitMEX, one of the world's largest cryptocurrency derivatives exchanges. Specializing in futures, options, and perpetual contracts for cryptocurrencies like Bitcoin, he and the other founders of BitMEX invented the perpetual contract, a product that reshaped the landscape of crypto trading.

Hayes graduated from the prestigious Wharton School at the University of Pennsylvania in 2008. He began his career as a trader at traditional banks before becoming captivated by Bitcoin and choosing to dive headfirst into the cryptocurrency revolution. He founded an exchange and briefly became a billionaire, making him the youngest African American billionaire in history. In 2022, Hayes was charged by the U.S. Department of Justice for violating the Bank Secrecy Act. He voluntarily pleaded guilty, ultimately receiving a six-month sentence of home confinement, two years of probation, and a $10 million fine. Now financially secure and having experienced both fame and legal consequences, Hayes has left the United States behind, settling in Asia where he lives freely and writes essays online.

This article synthesizes multiple sources to narrate Hayes' life story with a humorous tone. It’s clear that his elite education, bold yet meticulous mindset, appetite for high-risk and high-reward ventures, and rebellious adventurer's personality shaped the man he is today.

The Early Life of a Financial Prodigy

Though not wealthy, Hayes came from a solidly middle-class American family. His parents were employees at General Motors, and he was born in Detroit. To ensure their children received a better education, they sent him to a private school in Buffalo, New York.

Hayes showed athletic talent early on. He played on the school tennis team and ran cross country (a long-distance running sport held in natural outdoor environments, typically over courses up to 12 kilometers). He even earned scholarships through sports and later placed in the "Mr. Penn" bodybuilding competition during college.

His ambition emerged early. After enrolling at Penn in 2004, Hayes started waking up at 5:30 a.m. with friends to work out🏋️ at the university gym next to Wharton. According to interviews with NY Magazine, Hayes said they used these early mornings to dream about the future—fantasizing about becoming billionaires.

A friend who trained with him once remarked: “I think he already saw himself back then as a financial wizard, more like Gordon Gekko than Mark Zuckerberg.”

I Don’t Want to Stay in Buffalo—I Want to Go to China

Never one to follow convention, the rebellious Hayes believed that working in Manhattan or on Wall Street after graduation would make him just like everyone else—with no exciting path forward. So he chose a different route. During his junior summer in 2007, he secured an internship at Deutsche Bank in Hong Kong. From there, Hayes boarded a flight to Hong Kong, launching his journey across Asia.

Hayes: “The old-timers in Buffalo won’t leave. I don’t want to stay in Buffalo.”

Reporter: “What about Manhattan?”

Hayes: “Why do the same thing as my classmates? I’d get the same results.”

As an intern fresh off campus, young Hayes had duties beyond trading—he also bought lunch for his superiors. Interestingly, he once mentioned in a blog post: “I charged a substantial tip on every meal, earning hundreds of dollars in profit each week. And to avoid seeming shady, everyone in the trading desk knew what I was doing—and tacitly allowed it. We all understood.”

Can clubbing land you a job? Hayes made it happen. Near graduation, when Deutsche Bank sent recruiters to Penn, Hayes told them during interviews that he enjoyed partying at Hong Kong nightclubs. One interviewer asked about nightlife in Philadelphia, so Hayes recommended some spots. The result? They all ended up wasted at Philly House in Philadelphia—and Hayes landed his first real job: a trader at Deutsche Bank’s Hong Kong branch.

Hayes’ flamboyant personality was evident even during his internship. Hong Kong’s now-popular Casual Friday—where employees can skip formal wear on Fridays—was already practiced at his bank. As he recounted in a blog post, one Friday, a senior executive passed by his desk and asked his manager: “Who the fuck is that?” The manager looked up—Hayes was wearing a pink slim-fit polo shirt, faded jeans, and bright yellow sneakers. That day, Casual Friday was quietly canceled across the department. This kid always danced on the edge of danger.

First Encounter with Bitcoin

In 2013, Hayes first learned about Bitcoin. By then, he had moved from Deutsche Bank to Citigroup—but was soon laid off. According to his own recollection, his first trade involved buying BTC spot on Mt Gox, depositing it into ICBIT (the exchange that invented coin-margined futures), then selling at a premium a BTC/USD coin-margined futures contract expiring in June—netting a 200% return and making several thousand dollars instantly. From there, he never looked back.

At the time, China had strict capital controls, causing Bitcoin prices on mainland exchanges to carry a significant premium over Hong Kong. Spotting this arbitrage opportunity, Hayes began buying Bitcoin cheaply in Hong Kong and selling it on mainland exchanges. He would withdraw profits into a fake mainland bank account, then take a minibus across the border to Shenzhen, withdraw cash, and stuff it into his backpack to carry back to Hong Kong. Repeating this process raised red flags with Hong Kong authorities. Once, border officials detained him over suspicious Bitcoin activity. Hayes claimed he was merely a victim of fraud—and was released.

The Rise of BitMEX

After the collapse of Mt Gox, which once held 80% market share, three major Chinese exchanges—Huobi, OKCoin, and BTC China—took over most of the market. Overseas platforms like Bitfinex, ICBIT, and Bitstamp captured the rest. Competition was fierce: Bitfinex relied on its P2P lending market and USDT; ICBIT pioneered inverse futures (i.e., coin-margined contracts); Bitstamp… well, got hacked for 5 million and we’ll say no more; Coinbase catered to retail investors and was thriving as a newly launched exchange.

Despite this crowded landscape, Hayes saw his opening. At Deutsche Bank and Citigroup, he specialized in futures trading. He believed existing exchanges weren’t professional enough. He wanted to create a Bitcoin trading experience similar to how Wall Street traders handled stocks. Thus, the idea for a Bitcoin derivatives exchange was born. He envisioned a platform accepting only Bitcoin, resembling a Bloomberg terminal in look and function—making Bitcoin trading feel as institutional as equities. He teamed up with Ben Delo and Sam Reed, both coding geniuses passionate about crypto. In 2014, they registered a company in Seychelles and officially launched BitMEX—short for Bitcoin Mercantile Exchange (a nod to the Chicago Mercantile Exchange, CME)—with Hayes as CEO. On launch day, the exchange recorded $50 million in trading volume.

Despite a flashy start, business struggled in the first six months. By spring 2015, Hayes considered quitting and suggested to his partners: “Hong Kong’s secondhand electronics market is booming—why not resell used iPhones?” His partners declined. Ultimately, they decided to lean into high risk and high reward to attract users. Futures trading offers outsized returns because of leverage—borrowing funds against collateral. The higher the leverage, the greater the risk. Hayes and his team pushed BitMEX’s leverage to 50x: a 1 BTC margin could open a position worth 50 BTC. Later, they increased it to 100x—far exceeding competitors. This turned BitMEX into a magnet for high-stakes gamblers and miraculously flipped the exchange from losses to profits. High leverage became BitMEX’s core brand identity—even leading the parent company to rename itself 100x Group.

Inventing the Perpetual Contract

In a YouTube video, Hayes said: “Some competitors focus on retail users. Why don’t we go after them too?” But retail traders often lack formal finance training. Unsophisticated users entering BitMEX would quickly realize they didn’t understand derivatives—watching helplessly as their money vanished when contracts expired.

A real and amusing example: according to NY Magazine, many retail users emailed Hayes complaining their contracts “suddenly disappeared.” In reality, their contracts had simply expired—leading them to accuse Hayes and BitMEX of being scammers.

Delo was the first to suggest improving the product: “What if we created a futures contract with no expiry date?” That would solve the retail problem. Inspired, the founders brainstormed further—so creatively that they sketched out the concept on a napkin in a noisy bar.

The result? BitMEX’s greatest and most iconic innovation: the Perpetual Swap. It ingeniously avoids the drawbacks of traditional futures (constant expiries are problematic for a 24/7 market) while preserving core functionality—allowing longs to profit from price increases and shorts from declines.

Also known as “Perp,” a perpetual swap is a futures contract without expiry. It uses funding rates to anchor the contract price to the spot price, enabling leveraged trading without the hassle of rolling over positions. For more on Perps, see:What Is a Perpetual Contract?

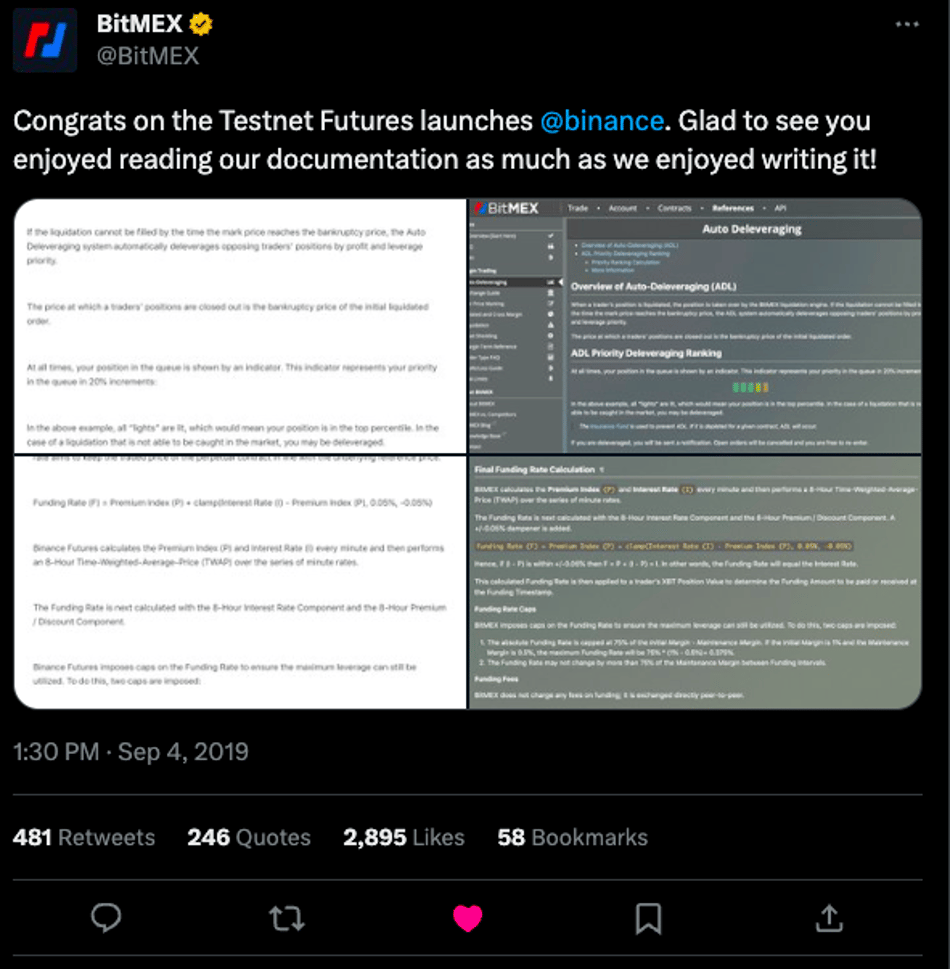

Since BitMEX launched its first perpetual product, XBTUSD perp, in May 2016, more exchanges have followed suit. Bybit and OKEx launched theirs in December 2018; FTX and Binance followed in October and December 2019. Ironically, when Binance launched its futures testnet, BitMEX trolled them on Twitter: “Congrats to Binance on launching your futures testnet. We’re thrilled to see you copying our docs as joyfully as we wrote them!”

Source: BitMEX

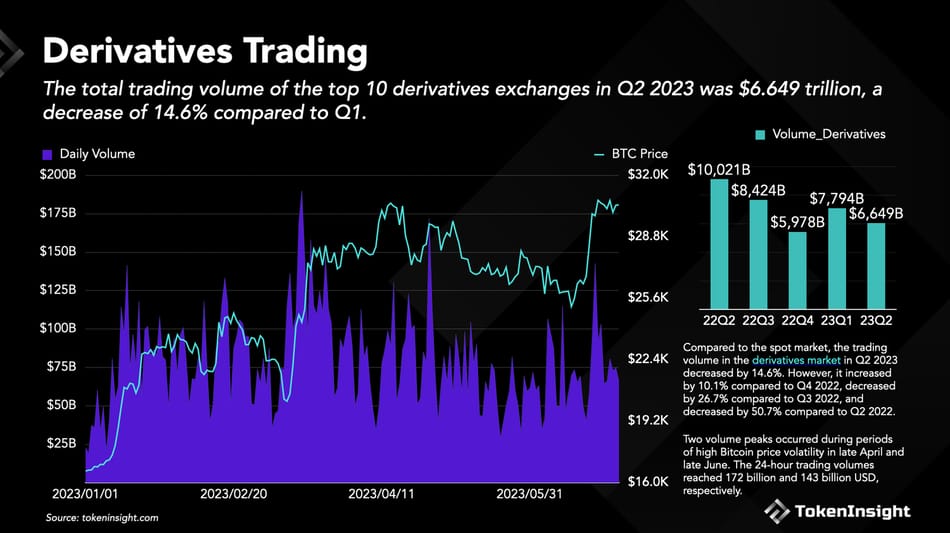

Although the perpetual contract didn’t explode overnight, this brilliant product eventually transformed the market. Today, the derivatives market sees quarterly trading volumes exceeding $660 billion, with perpetuals accounting for over 90%.

Source: TokenInsight

Living Large

In 2017, BitMEX was riding high. They were approached with acquisition offers, but Hayes and the founders rejected a venture capital bid. “Valued at just $600 million? Too low,” Hayes thought. Back when starting BitMEX, they’d struggled to raise funds—now, they chose to keep all equity. The following year entered a bear market, yet user activity surged on their platform. That summer, BitMEX hit a single-day trading volume of $8 billion, generating $4 million in revenue—a staggering display of profitability.

In 2018, Hayes returned to New York as a successful young tycoon. In May, he attended the Consensus crypto conference in NYC and instantly became the center of attention: three Lamborghinis rented by BitMEX parked illegally outside the Midtown venue. Hayes joked it was “guerrilla marketing” and admitted it might be “a little bit gauche.” Ironically, the cars were rentals—and incurred around $1,000 in parking fines. Classic Hayes: flashy, rich, and unapologetically reckless.

Source: Arthur Hayes

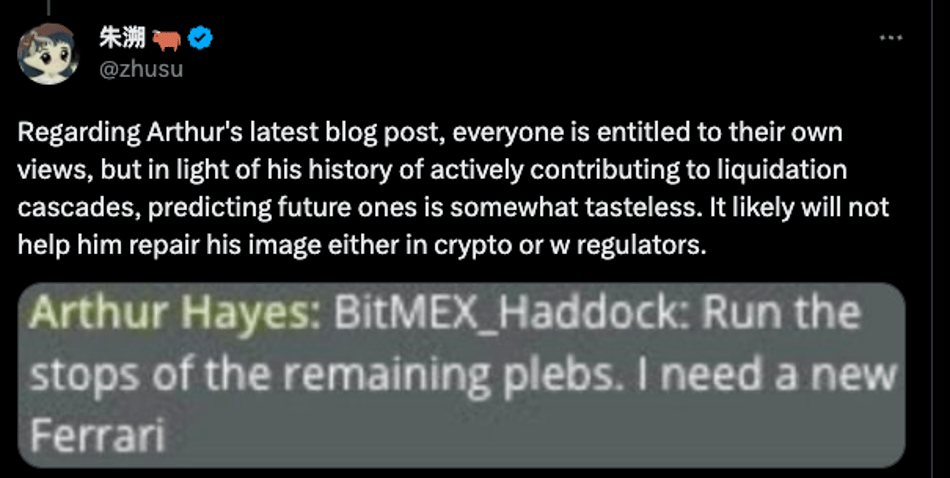

Sudden wealth made Hayes a lightning rod in the crypto world, drawing envy from those who thought he made money too easily. A popular joke circulated: “When others profit, Hayes profits. When others lose, Hayes still profits.” An amusing meme mocked him with a fake message to employees: “Trigger stop-losses for all retail traders—I want to buy a Ferrari,” implying Hayes manipulated the market against users.

Source: Zhu Su

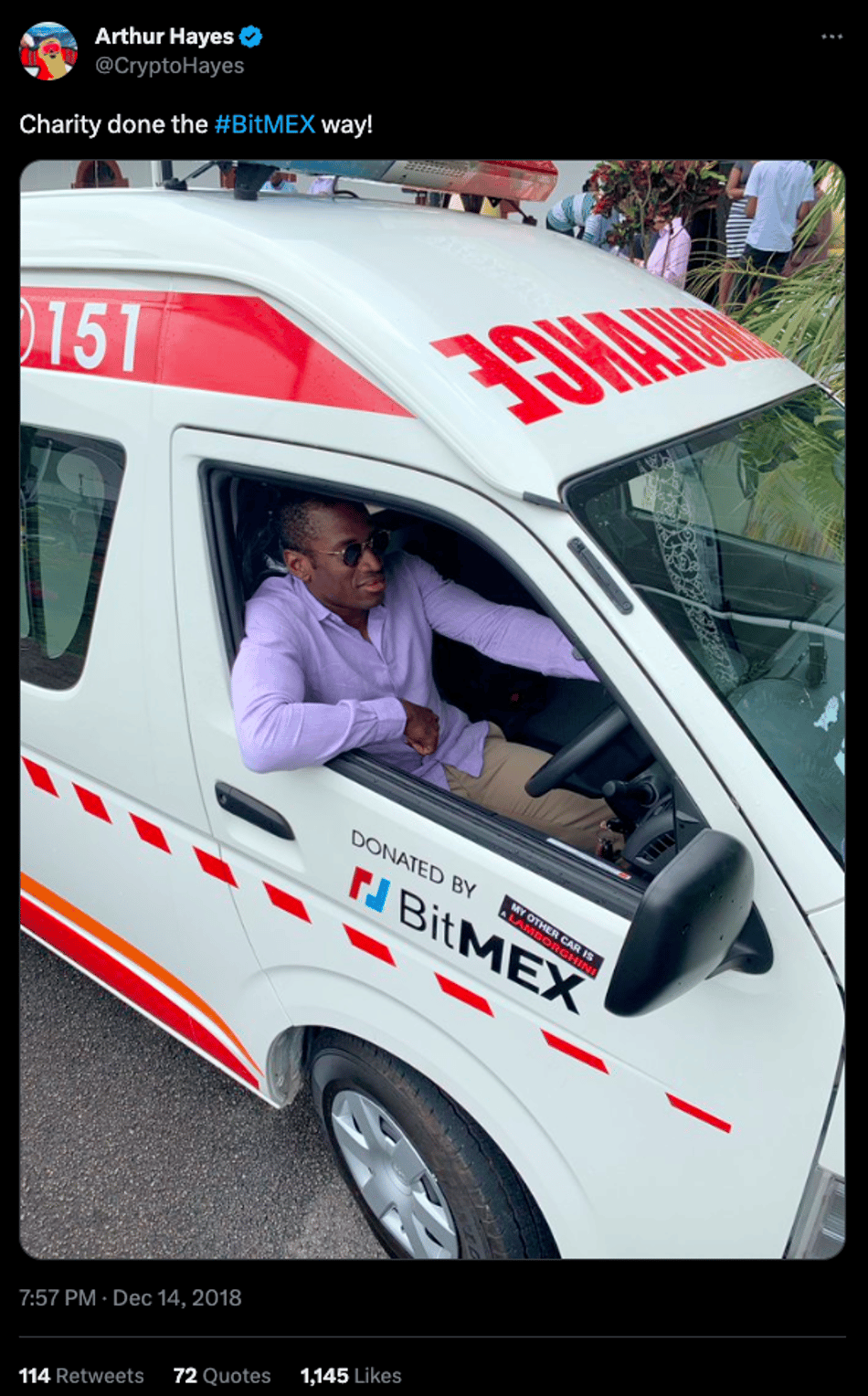

But Hayes wasn’t done showing off. At the end of 2018, he posted a photo on Twitter standing beside an ambulance BitMEX donated to Seychelles. Wearing sunglasses, he looked insufferable. The photo’s highlight? A sticker reading: “My other car is a Lamborghini.”

Source: Arthur Hayes

The 2019 Tangle in Taipei debate is another defining moment in Hayes’ story. A few quotes reveal how outrageously confident he had become. On the show, Hayes clashed fiercely with renowned economist and crypto critic Nouriel Roubini over Bitcoin and BitMEX.

Their attire alone signaled opposition: Roubini wore a suit, representing tradition, while Hayes wore tight jeans with large knee rips—symbolizing rebellion. Within ten minutes, the arrogant Hayes shocked viewers. Asked why BitMEX was registered in Seychelles, he replied: “I didn’t want to bow down and take an ass-fucking from the U.S. government just because it’s regulated.” When asked about differences between U.S. and Seychelles regulators, he went further: “They’re just more expensive to bribe.” How much for Seychelles? “Just a coconut.”

Tangle in Taipei

Inviting Trouble

There’s an old Chinese saying: “Stay quiet and get rich.” Excessive flaunting and constant rule-testing made Hayes many enemies. After the 2019 Taipei Tangle debate, backlash mounted—including from the U.S. government.

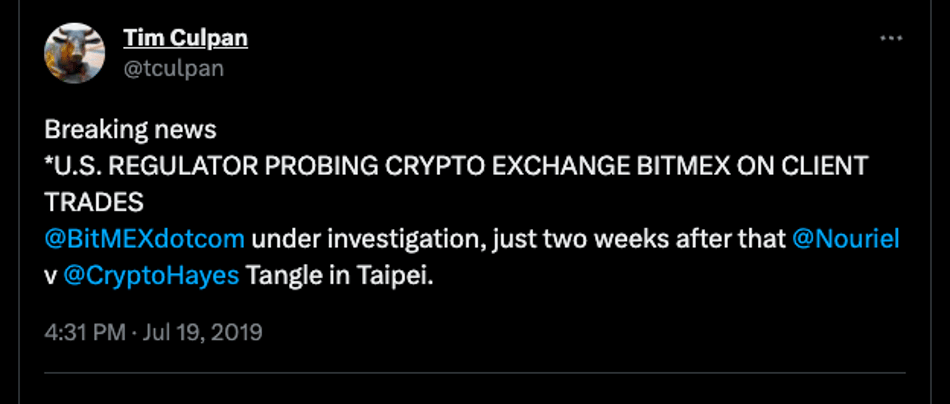

On July 19, 2019—just one week after the debate—the U.S. Commodity Futures Trading Commission (CFTC) opened an investigation into BitMEX, suspecting it provided services to U.S. customers. Under U.S. law, a Seychelles-registered entity like BitMEX cannot serve Americans. The U.S. government viewed this defiant, law-mocking “jester” as a threat—similar to how Ant Group was blocked from IPO after Jack Ma’s outspoken remarks.

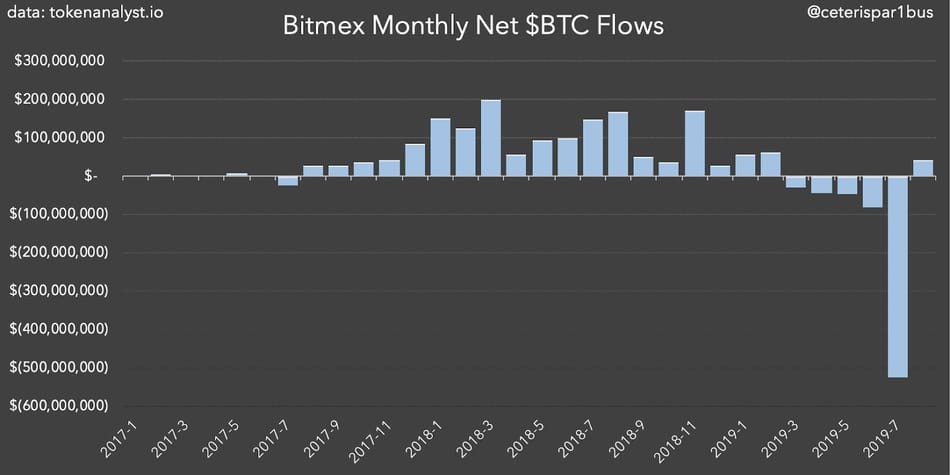

Within a day, BitMEX saw $73 million in net Bitcoin outflows. That entire July, outflows exceeded $500 million—setting a record (previously under $100 million monthly).

Source: ceterispar1bus

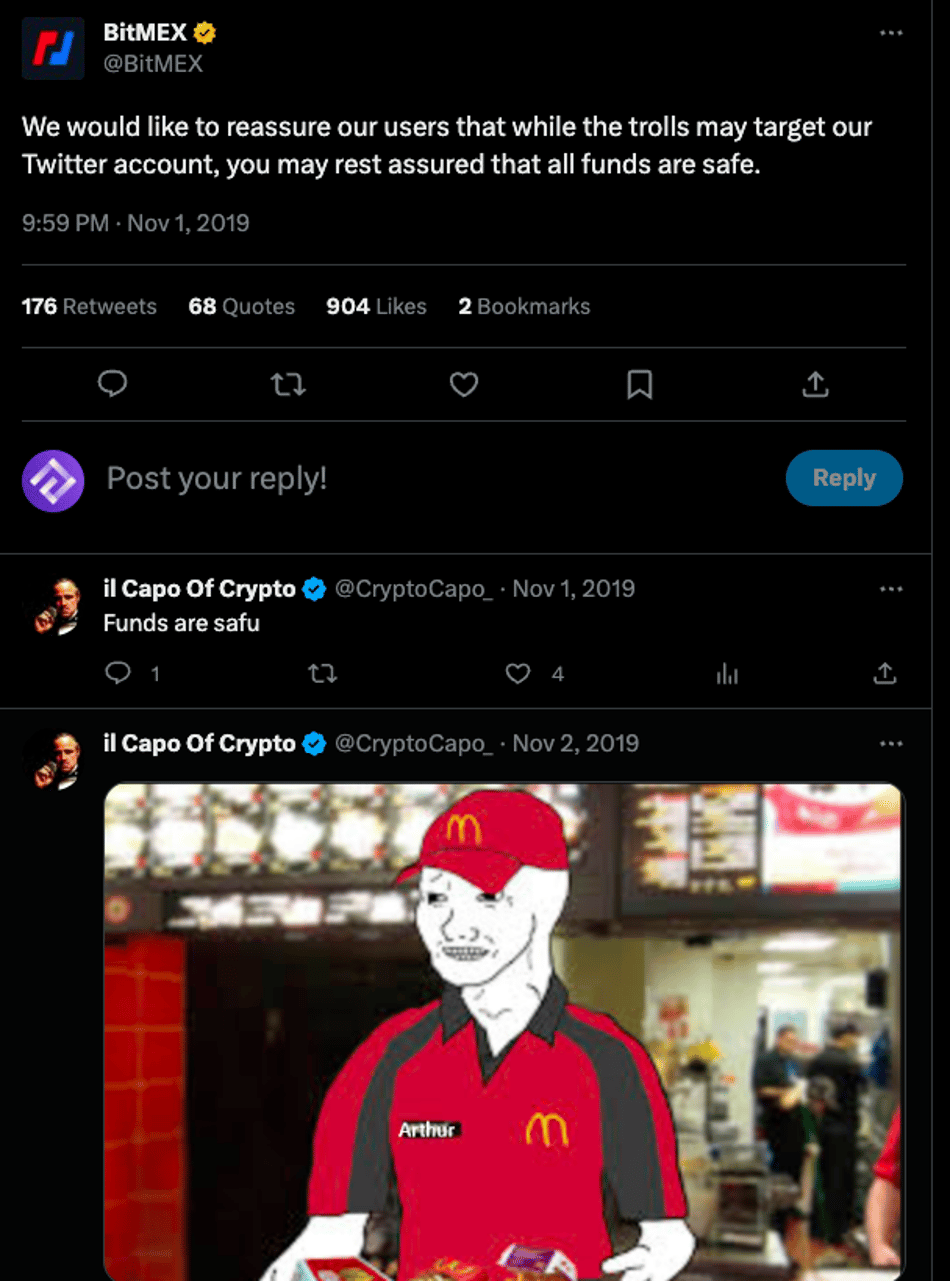

Then came more crises: on November 1, BitMEX accidentally leaked vast amounts of user email addresses, pushing the situation toward chaos. Soon after, hackers breached BitMEX’s Twitter account and mockingly tweeted: “Take your BTC and run. Last day for withdrawals,” and “Hacked.” Though quickly deleted, someone even created a new Twitter account to continuously leak user IDs and emails. All BitMEX could do was issue empty reassurances: “Funds are safe.”

Source: BitMEX

Legal Avalanche

In 2020, BitMEX hadn’t recovered from the March 12 crash when new trouble struck. On May 16, BitMEX was sued by BMA LLC (Bitcoin Manipulation Abatement), a California firm accusing BitMEX and executives including Hayes of money laundering, fraud, and operating an unlicensed crypto exchange. The plaintiff emphasized that in 2019, 15% of BitMEX’s volume—about $138 billion—came from U.S. users, calling it “the largest record of illegal U.S. trading.” As the saying goes: when things go bad, even water gets stuck in your throat. Amid this lawsuit, BitMEX suffered shutdowns in Japan, server outages, and other disasters.

But the plaintiff had little real leverage—BitMEX was deliberately registered in Seychelles to avoid U.S. regulation. BMA could only use customer email data to indirectly prove BitMEX operated in the U.S.—a flimsy argument BitMEX mocked publicly: “We’re registered in Seychelles—come and get us!” They remained defiant.

Source: US Gov

Unfortunately, the government was now serious. After the 2008 financial crisis, Bitcoin’s rise alarmed governments worldwide. Each Bitcoin bull run triggered fears among central banks that Bitcoin might disrupt their control—especially during the pandemic year of 2020. From MicroStrategy aggressively accumulating BTC, to Nigeria banning Bitcoin after citizens invested $140 million fearing loss of control, to Musk selling Tesla stock to buy Bitcoin—these signals made the Fed nervous. With Hayes being the loudest provocateur, they targeted BitMEX and Hayes as the perfect scapegoat: young, flashy, self-made, black, and accused of profiting immorally—it was a perfect storm.

In October 2020, just as a new bull market began, Hayes and two other BitMEX founders received joint charges from the U.S. Department of Justice and CFTC. The accusations were familiar: BitMEX operated in the U.S. without registration and allegedly engaged in illegal money laundering—thus violating the 1970 Bank Secrecy Act (also known as the Currency and Foreign Transactions Reporting Act). BitMEX became the first crypto exchange charged under the Bank Secrecy Act. Hayes was targeted partly because earlier, during negotiations with the CFTC, he refused to hand over customer data—an act that fueled retaliatory intent. Reports indicate that within 48 hours of the CFTC charges, over 45,000 BTC was withdrawn and moved to other exchanges.

Hayes reacted swiftly: he resigned as CEO and, together with Reed and Delo, formed a new entity, 100x Group, to manage BitMEX more securely. New CEO Alexander Hoptner stated readiness to face litigation. Reports suggest that on the day of Hayes’ resignation, BitMEX lost approximately $400 million in user deposits—appearing doomed.

Surrender in Honolulu

On April 6, 2021, a private jet from Singapore touched down in Honolulu, Hawaii. Hayes, wearing a casual T-shirt, was arrested at the airport. FBI agents boarded the plane, collected fingerprints and saliva samples, then handcuffed him—flanked by agents in bulletproof vests—and escorted him to court. This marked Hayes’ first return to the U.S. since 2018—but nothing like his previous arrival in New York behind the wheel of a Lamborghini.

Though he surrendered, Hayes initially did not plead guilty in court—following legal advice as the optimal strategy. He was still fighting. Earlier in March, co-founder Ben Delo had already surrendered in New York and also pleaded not guilty. After Hayes’ team posted $10 million bail, he endured over ten days of isolation before finally boarding a flight back to Singapore. He remained in Singapore throughout the pandemic. Months later, in August, BitMEX ultimately reached a settlement with the CFTC, agreeing to pay a $100 million fine—seemingly escaping unscathed.

By then, the first two founders had surrendered. But Sam Reed from Wisconsin had it worse: Reed was actually arrested in October, living in a Boston suburb with his wife and a three-month-old baby. According to media reports, at 6 a.m., over a dozen FBI agents and police officers kicked down his door and handcuffed him to a chair. He was taken to a mysterious federal building and held in a dark, damp basement for ten hours—shackled with leg irons.

Whether due to the horrors of detention or other reasons, Hayes eventually gave in. In February 2022, Hayes and the other two founders pleaded guilty in court, admitting to “willful disregard” of the Bank Secrecy Act and failure to implement anti-money laundering procedures—and agreeing to each pay an additional $10 million fine. The U.S. Attorney for the Southern District of New York told the court that BitMEX was a “tool for money laundering and criminal activity,” conducting over $200 million in suspicious transactions, and failed to report anything to authorities. Prosecutors claimed Hayes once unfroze an account linked to a hacker, allowing withdrawal of suspected stolen Bitcoin. Without KYC requirements, “the full extent of BitMEX’s criminal conduct will never be known,” prosecutors wrote.

DOJ attorney Damian Williams said: “Arthur Hayes and Benjamin Delo created a platform that openly defied legal requirements and voluntarily ignored basic anti-money laundering rules.”

With evidence presented, prosecutors demanded harsh punishment. Hayes tried to express remorse: “While I’m proud of BitMEX’s achievements, I deeply regret participating in these criminal activities.” Friends spoke on his behalf, including Mike Novogratz, head of Galaxy Investment Partners: “Let’s remember, Arthur is a young, successful Black man. Our country and industry need more people like him.”

In May 2022, under pressure from public opinion and racial discourse, the judge opted for leniency—sparring Hayes from prison—but sentenced him to six months of home confinement.

Let the Past Be the Past

According to media reports, Hayes served his confinement in a luxurious white three-bedroom apartment in Miami’s South Beach—his own property—with a massive balcony overlooking Biscayne Bay. There, Hayes watched Miami’s skyline, enjoyed sea breezes, spent days doing yoga and workouts, or went out to play sports and swim (he’s allowed several hours daily outside). Even when buying coffee, fans sometimes recognized him. A passionate writer, he rented a WeWork nearby for office space and blogging. Occasionally, he dined out and met local crypto-native community members.

Yet Hayes’ aversion to the U.S. shows in small details. Though house arrest resembled a vacation, he remained tense. “In the U.S., I worry about personal safety because people carry guns,” he said. He even took it out on bugs: frustrated that mosquitoes made the ground-floor pool unusable, he complained: “In Singapore, they’d spray for pests.” He criticized many aspects of America: extreme time zone differences, disgusting food—revealing deep cultural disdain. “I don’t plan to return to the U.S.—probably never again.”

By early 2023, Hayes had spent considerable time in Hokkaido. From his own words, one senses he’s truly mellowed: “I don’t have big visions anymore. For now, let’s just protect users’ money—don’t lose their Bitcoin.”

Final Thoughts

Once, there was a young man—brilliant, well-educated—who worked a few years as a trader in traditional finance, grew dissatisfied, and struck out on his own. He became instantly wealthy, a Twitter celebrity, the face of crypto, crowned king. Then he defied the U.S. government, becoming a rebel entrepreneur attracting mainstream attention. Arrogant and flamboyant, he eventually faced consequences. The government struck back. He resisted, but ultimately fell. Still, he changed crypto forever.

This story sounds familiar. SBF: That’s not me. Users: That’s exactly you. Hayes: That’s clearly me.

Of course, despite similar paths, key differences remain: one came later, one earlier. One paler, one darker. One born rich, one from a mechanic’s family. One a fat shut-in, one a muscle-bound giant. And crucially: one took customers’ money—proven. The other, despite numerous allegations, was never accused of misappropriating user funds.

Well then, dear listeners, that’s all for today’s story. What you’ve learned—reflect on it yourself. Until next time.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News