9 Catalysts to Watch in Q3: Bitcoin ETF, LSDfi, Frax...

TechFlow Selected TechFlow Selected

9 Catalysts to Watch in Q3: Bitcoin ETF, LSDfi, Frax...

Protocols with product updates and strong narratives tend to attract more attention and perform well in the short to medium term.

Author: THOR HARTVIGSEN

Translation: TechFlow

The second quarter was indeed a turbulent period for the cryptocurrency market. The market peaked around mid-quarter but then faced a series of bearish developments over the following six weeks, including lawsuits against major exchanges and concerns about USDT and TUSD de-pegging.

Before diving into what’s coming next, let’s first assess which protocols performed well in the past quarter.

In DeFi, several sectors continued growing and attracting organic demand, including liquid staking and on-chain perpetual trading.

Perpetual DEXs

During Q2 this year, on-chain perpetual exchanges such as dYdX, GMX, and Gains collectively generated $117 million in fees. These products have maintained high usage throughout the bear market. The ability to trade cryptocurrencies, forex, and other assets on-chain remains one of the most organically demanded areas in DeFi.

The table below compares trading volumes across the largest perpetual protocols in Q1 versus Q2.

Total trading volume declined by 8.2% compared to Q1—a relatively modest drop given the broadly bearish environment we experienced during Q2. Although dYdX still leads significantly in terms of volume, the protocol saw a substantial decline in its market share between quarters. The same is true for other "OG" perpetual exchanges like GMX and Gains.

Newer protocols such as Level and Kwenta have seen significant growth, driven primarily by generous trading rebates (i.e., native token emissions) offered to traders. As these incentives taper off over time, it will be important to observe whether users continue using these platforms or migrate elsewhere.

Vertex opened its Arbitrum-native exchange to the public in April and has recently seen a sharp increase in trading volume. Vertex has not yet launched its native token, so much of this volume may be driven by potential airdrop farmers.

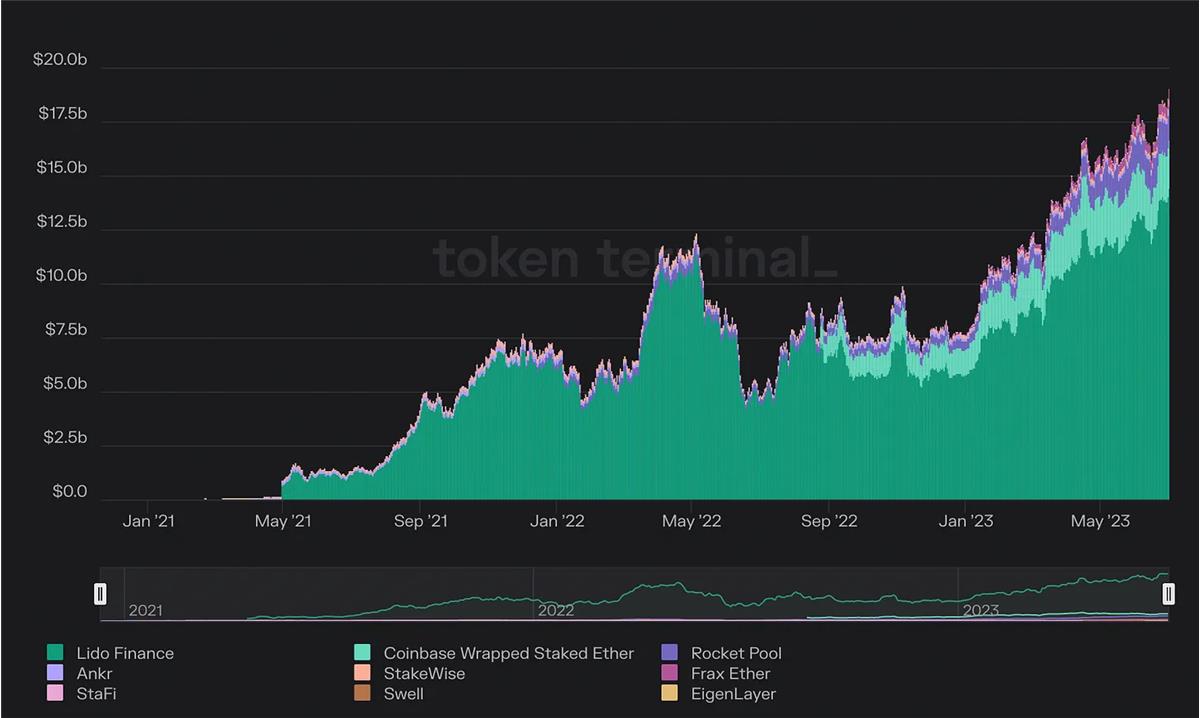

Ethereum Liquid Staking

Over the past six months, liquid staking has grown from approximately $7 billion to over $18 billion. With overall DeFi TVL hovering around $45 billion, an inflow of $11 billion is highly significant.

Following the Shanghai hard fork, withdrawals were enabled, driving significant liquidity into this sector. Below are some data comparisons on staked assets between Q1 and Q2:

The biggest beneficiaries from Q1 to Q2 were Lido, Rocket Pool, and Frax Finance. Lido not only attracted 1.6 million ETH ($3 billion) in inflows but also gained considerable market share despite emerging competition.

Both Rocket Pool and Frax possess unique moats that attracted new liquidity.

Rocket Pool launched its 8ETH mini-pool, while Frax Ether consistently offers the highest staking yield due to its dual-token model.

Swell launched in Q2 and quickly accumulated notable TVL. They are currently running a campaign where early depositors can farm the upcoming $SWELL token. Thus, part of this new liquidity likely comes from users aiming to participate in the airdrop.

Chains

Below are financial statements for larger-cap L1 and L2 blockchains in the crypto space. Definitions:

-

Fees = Transaction fees paid by users on-chain;

-

Revenue = Portion of fees remaining after validators take their share;

-

Profit = Revenue minus token emissions.

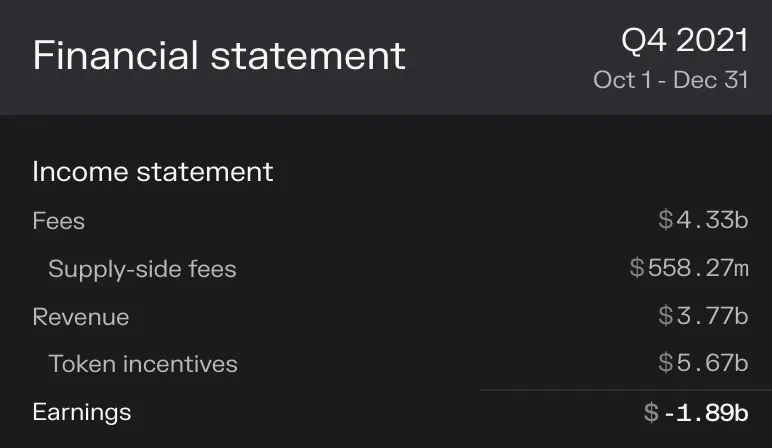

Ethereum achieved its best-ever quarter in profitability, growing more than 300% compared to Q1 of this year.

As shown below, in Q4 2021 Ethereum generated $4.3 billion in fees, but profits were largely negative due to massive ETH issuance prior to transitioning to proof-of-stake.

How would these fee levels translate into profit in today's environment?

If Ethereum maintains an average of $4 billion in annual fees and profit margins similar to Q2 2023, annual profit would reach approximately $24 billion—giving Ethereum a P/E ratio of no more than 9.5 at the current price of $1,900.

Arbitrum also saw a sharp increase in fees during this period and is one of the few chains with positive profitability. Currently, L2 profit margins are quite low because most fees go to Ethereum mainnet validators.

With Proto-Danksharding launching later this year, profit margins are expected to improve as rollup fees decrease.

Chains such as Solana, Polygon, and Optimism show large negative profits due to high token emissions used to incentivize users and pay validators.

9 Catalysts and Narratives to Watch in Q3

Crypto is an attention economy. Protocols with product updates and compelling narratives tend to attract attention and outperform in the short to medium term. Below are some top narratives worth closely monitoring.

Bitcoin ETF

Q2 was very positive for the crypto market due to sudden institutional interest in Bitcoin. Companies like BlackRock and Fidelity have filed for Bitcoin ETFs, and market sentiment generally views approval as highly likely. A few days ago, the SEC stated recent filings were incomplete; although prices initially dropped, they quickly rebounded as it appeared the applications mainly needed additional clarity on which exchange would list the product. Many ETFs have already been re-submitted—for example, Fidelity’s Bitcoin ETF now lists Coinbase as the intended exchange.

When could an ETF be approved?

Deadlines for BlackRock and Ark ETFs fall on August 12. While delays are possible, experts predict decisions are likely to come around that date.

The market appears to expect approval in August, so rejection or further delay could negatively impact prices. BlackRock’s ETF deadline is February 23 next year.

Why is a Bitcoin ETF important?

This is the single most important catalyst to monitor in the coming months. A Bitcoin ETF not only grants large institutions access to the asset but also ushers in a bullish phase for the entire crypto market. Without proper Bitcoin price movement, altcoins cannot rally.

DeFi also cannot receive fresh liquidity injections for the same reason. If ETFs are approved later this year, benefits will extend beyond just Bitcoin. With that in mind, the following catalysts could drive specific assets to outperform in a more optimistic macro environment:

EIP-4844

You’re likely aware that EIP-4844 will bring Proto-Danksharding to Ethereum in Q3/Q4. This upgrade allows rollups to send batches of transactions (called blobs) to Ethereum, reducing fees on Layer 2s by up to 20x. Therefore, the primary beneficiaries won’t be Ethereum itself—fees on mainnet won’t decrease until full Danksharding launches—but rather rollups like Arbitrum and Optimism. $ARB and $OP are trading far below their年初 levels, and if history repeats, both could see rebounds ahead of this event.

Liquid Staking and LSDfi

As previously mentioned, liquid staking of Ethereum (ETH) was the fastest-growing DeFi sector in Q2. Below are some protocols worth watching in Q3:

frxETH – Frax plans to launch frxETH V2 and the Frax Chain later this year, featuring a native lending market for LSDs and using frxETH as native gas to boost staking APRs.

EigenLayer – EigenLayer has already drawn strong investor interest, and with its official launch expected later this year, it’s likely to attract substantial liquidity.

swETH – Swell is running a campaign where early minter of its native LSD swETH earn “pearls” redeemable for the upcoming $SWELL airdrop. As long as this campaign continues, the protocol is likely to keep growing.

ETHx – Stader Labs will launch ETHx on mainnet on July 10, enabling Ethereum node operation with just 4 $ETH.

The explosive growth seen in the LSD sector in Q2 is unlikely to continue at the same pace in Q3. Higher staking ratios and reduced on-chain activity have led to lower APRs across the board. With diminishing returns, stakers are now seeking ways to boost yields—that’s where LSDfi protocols come in. The table below, from last week’s newsletter, shows current stats for top LSDfi projects.

Pendle has seen massive growth in liquidity, and its native token $PENDLE rose over 100% in the past week, peaking recently after news of Binance listing. The Pendle team tends to stay quiet about new features—but it’s safe to assume they have big plans for Q3. They recently applied for an OP-grant to boost liquidity on Optimism and hinted at a BNB Chain launch. Cross-chain expansion seems imminent.

LSD-backed stablecoin protocols like Lyra and Raft have also seen notable growth recently. Clearly, there’s demand for such products—but it’s equally clear that recent success owes much to generous token incentives/airdrop farming. Over three similar protocols plan to launch in the coming weeks/months, so competition for liquidity will undoubtedly intensify.

Base (Coinbase’s Layer 2 solution)

Just last week, Coinbase announced Base passed all security audits and met 4 out of 5 criteria for mainnet launch. Built on the OP Stack, Base benefits from Optimism’s recent Bedrock upgrade, which drastically lowered transaction costs on Optimism and other OP-based chains. Only “testnet stability” remains, so mainnet launch is likely within Q3. Coinbase has over 40 million registered users, many of whom may never have interacted with DeFi. This could be one of the most significant onboarding events of the year. Coinbase may initially support only battle-tested mainstream protocols like Uniswap and Aave, but bringing a vast retail user base into DeFi is highly beneficial for the ecosystem.

Additionally, this could be a positive narrative for $OP, as Base will commit a portion of its fee revenue to the Optimism treasury.

Frax Chain

Frax Finance has developed various products, including the $FRAX stablecoin, $FPI price index, Fraxswap, FraxEther, FraxFerry (bridge), and more. Frax also announced it is building an Ethereum-based Layer 2 blockchain aimed at unifying all these products into a single DeFi hub. It’s a hybrid rollup combining Optimistic Rollup architecture with zero-knowledge proofs for state consensus. The goal is to deliver high scalability, fast finality, and strong security for end users. The chain is planned for Q3/Q4 launch, but the most critical detail from the announcement is that frxETH will serve as the gas token. This could significantly increase frxETH demand if adoption grows. However, requiring users to swap into another token to use the chain might create friction and potentially slow adoption. I remain somewhat skeptical but am excited to see how it unfolds.

Polygon 2.0

Polygon recently unveiled “Polygon 2.0,” integrating various innovations built over the past few years. It combines Optimistic Rollups (like Arbitrum and Optimism) with Cosmos-like cross-chain security mechanisms. Polygon 2.0 consists of four layers:

Staking Layer: Validators stake MATIC tokens similarly to PoS chains.

Interaction Layer: Shared bridges allowing interoperable minting and burning of assets across chains on Ethereum.

Execution Layer: Polygon 2.0 will run two distinct execution environments:

-

Supernets: Application-specific blockchains, similar to Avalanche subnets or Cosmos app-chains.

-

Public Chains: zkEVMs using Ethereum for data availability—most secure but also most expensive. PoS-based zkEVMs use Polygon for data availability (secured by MATIC) and only post proofs to Ethereum for greater scalability.

$MATIC has recently declined due to forced selling by Celsius converting assets into BTC and ETH. Therefore, once Polygon 2.0 launches in the second half of the year, prices may rebound.

dYdX V4

V4 aims to decentralize dYdX by launching the exchange as a custom application chain within the Cosmos ecosystem. Order books previously operated off-chain in a centralized manner will now be managed on-chain by validators maintaining in-memory order books. Each block, validators submit transactions to ensure consistency across all nodes’ order book states. Current test results show over 500 transactions per second. $DYDX has previously faced criticism for high inflation and low token utility. With V4, the token is likely to gain more meaningful use cases, possibly including revenue sharing, as previously mentioned by the protocol.

“Starting with dYdX V4, dYdX Trading Inc. will no longer operate any part of the protocol. Therefore, it will no longer receive revenue from protocol trading fees. The same applies to all other centralized parties unless otherwise decided by the community.”

The $DYDX unlock schedule is as follows:

-

30% unlocked on December 1, 2023;

-

40% released evenly each month starting January 1, 2024 through June 1, 2024;

-

20% released evenly each month from July 1, 2024 through June 1, 2025;

-

10% released evenly each month from July 1, 2025 through June 1, 2026.

The public testnet launch signals mainnet is approaching. Any announcement regarding $DYDX fee-sharing mechanics could become a strong narrative for the token. However, it’s crucial to remember the significant unlock schedule beginning in December.

GMX V2

With the public testnet launched a few weeks ago, GMX V2 seems closer than ever. This upgrade introduces several new features, including Chainlink’s custom low-latency price oracle for improved trade execution. Another major change is isolated liquidity per trading pair and the ability to create synthetic pairs.

Each trading pair will have its own liquidity pool—e.g., ETH/USDC using ETH as long collateral and USDC as short collateral. Synthetic pairs like SOL/USDC could use ETH as long collateral and USDC as short collateral. This model simplifies deployment of new liquidity pools, and isolated liquidity reduces risk for liquidity providers.

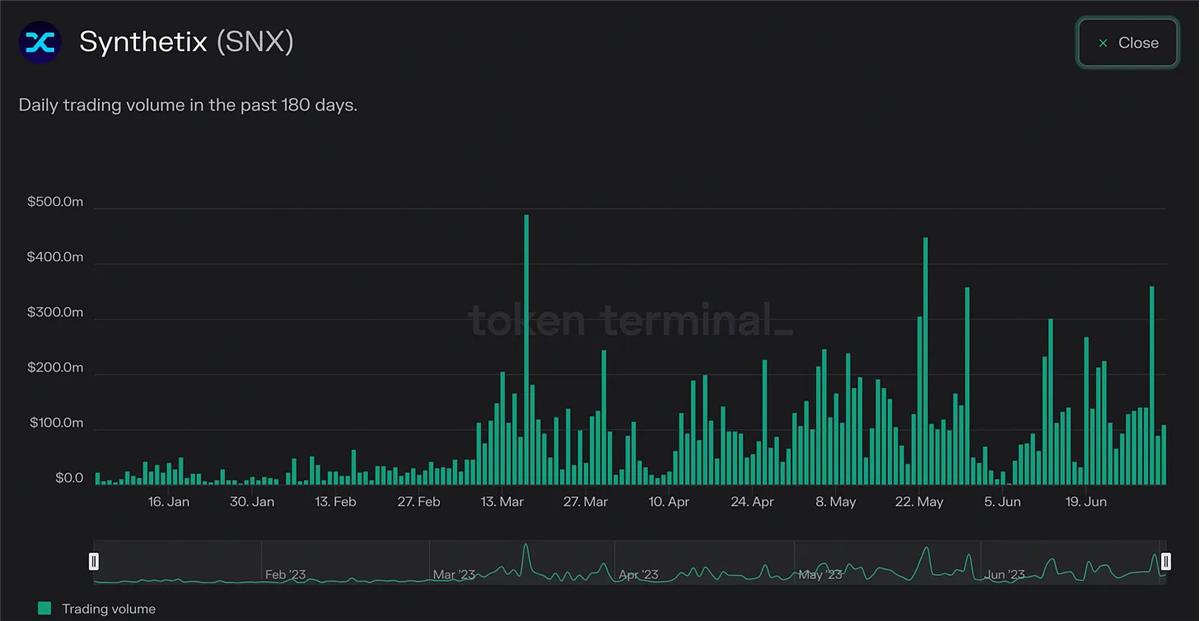

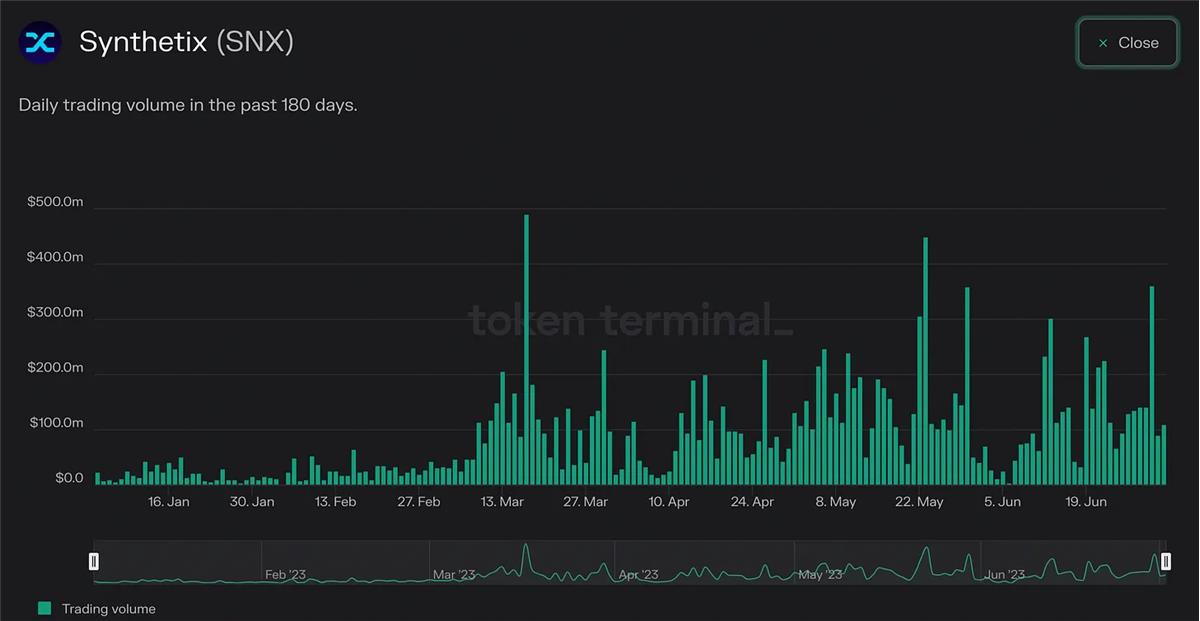

Synthetix V3

Synthetix is a DeFi liquidity hub powering various derivative protocols on Optimism, such as Kwenta, Lyra, Thales, Polynomial, and others. Trading volume has increased significantly this year, largely driven by Kwenta traders.

Synthetix V3 is a two-year upgrade aimed at transforming the protocol into a universal liquidity layer for all of DeFi. Currently, all synthetic assets are backed by the native governance token $SNX. V3 will introduce multiple upgrades, including multi-collateral staking, permissionless risk-isolated pools, cross-chain liquidity, and more. V3 is technically live on mainnet, but core innovations like Perps V3, Pools V3, Teleporters, and Cross-chain Synthesis are still under development.

Others

Other protocols in the space worth watching:

-

Vertex Protocol recently launched with strong volume growth;

-

Level launched recently on Arbitrum, with ~50% of its volume now coming from that chain;

-

Pear Protocol is即将 launching and will leverage existing infrastructure for liquidity on its trading platform.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News