Stanford VC Course Highlights: Venture Capital Fundamentals Every Founder Should Know

TechFlow Selected TechFlow Selected

Stanford VC Course Highlights: Venture Capital Fundamentals Every Founder Should Know

Founders are most likely to lose money on liquidation preferences.

Author: Ilya Strebulaev

Translated and edited by TechFlow

TechFlow Intro: This is the first publicly released lecture note from Stanford Graduate School of Business’s VC course. The author has taught this course for many years; among over 1,300 students, approximately 500 went on to found startups, and about 600 joined venture capital (VC) or broader private equity firms as investors.

He has decided to fully open up the course content—starting with the most fundamental—and most commonly misunderstood—cash flow terms: convertible preferred stock, liquidation preference, and conversion rights. These terms determine exactly how much founders receive upon exit.

For founders preparing to raise capital—or already in negotiations—this is essential foundational reading.

Full text below:

This article explains how cash flow terms operate, how liquidation preference affects your returns, and how convertible preferred stock gives investors an advantage.

These are foundational concepts every entrepreneur should understand.

Welcome—and My Motivation

I have taught the venture capital course at Stanford Graduate School of Business for many years. Over that time, more than 1,300 students have taken the course—roughly 500 later founded startups, and roughly 600 entered venture capital and broader private equity as investors. I stay in touch with many of them and frequently receive emails or messages saying, “I’m pulling out your lecture notes and slides again, Professor, as I negotiate my financing round or term sheet.”

I’ve long wanted to widely share my knowledge and experience—especially because the VC and startup world is often shrouded in mystique and widely misunderstood. That’s why I began posting VC research almost daily on LinkedIn. But sharing the granular details of a complex, layered course—one where concepts build upon one another—requires a different medium. So here I am.

After reading each article, you should gain a deep understanding of how investors make decisions, how entrepreneurs and investors negotiate over cash flow allocation and corporate governance, and countless other everyday matters in the startup world.

In the initial articles, we dive straight into the core: cash flow terms in the first VC financing round. Cash flow terms are, fundamentally, the rules governing “who gets what when the pie is divided.” We’ll examine the most common financial security used in VC financing—convertible preferred stock—and cover all major contractual terms that determine how returns are allocated between entrepreneurs and investors. After covering the first VC round, we’ll move on to subsequent rounds. Only after that will we be ready to discuss pre-VC instruments—including SAFEs and convertible notes. Many students ask me why we don’t start with SAFEs—after all, that’s often the first security founders issue today. But the defining feature of a SAFE is its conversion into the securities the startup will issue later; without understanding those underlying securities, it’s impossible to truly grasp SAFEs. Once we finish covering cash flow terms, we’ll turn to control rights, corporate governance, and conflicts of interest in startups—absolutely critical topics. As I tell my students repeatedly: “You can lose control of your startup only once. Once lost, it’s gone forever.”

A Running Case Study

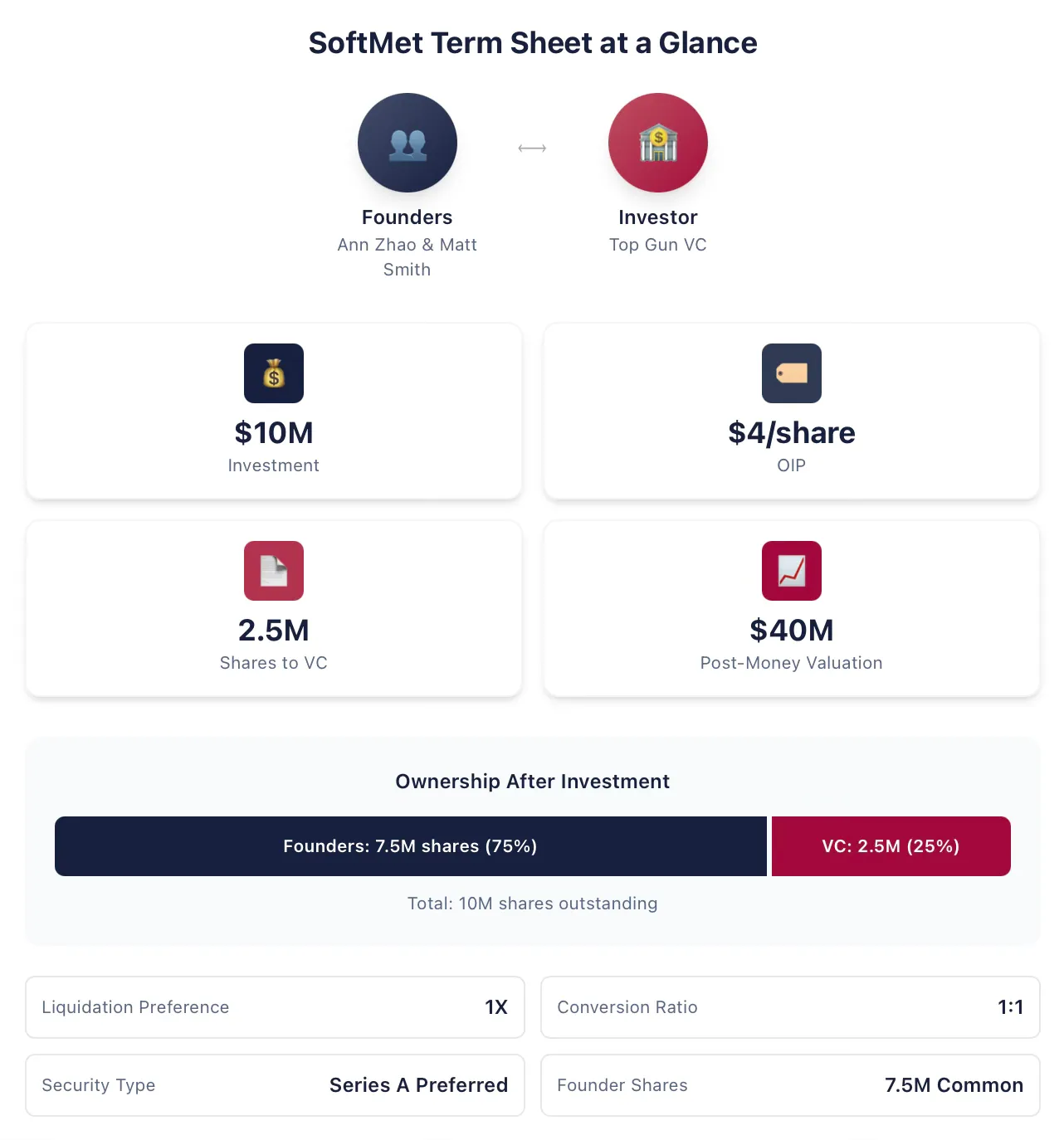

When explaining cash flow concepts, I’ll use a consistent case study throughout—modifying and expanding it as new concepts are introduced. Ann Zhao and Matt Smith are co-founders of SoftMet, a technology startup. During fundraising, they met Rob Arnott, a partner at Top Gun—a top-tier venture capital firm. Rob subsequently invited Ann and Matt to pitch their idea to Top Gun’s full partnership. A week later, the founders received Top Gun’s term sheet, which proposed:

Top Gun invests $10 million in SoftMet.

Top Gun receives Series A Preferred Stock in SoftMet, with an original issue price (OIP) of $4 per share.

The Series A Preferred Stock carries a 1x liquidation preference.

One share of Series A Preferred Stock is convertible into one share of SoftMet common stock.

The Series A Preferred Stock includes various additional terms and conditions.

The founders hold 7.5 million shares of common stock.

The company’s post-money valuation is $40 million.

Ann and Matt need to understand what this term sheet means: What exactly is Series A Preferred Stock? What is post-money valuation? What is liquidation preference? What is conversion? Which features of this proposal deserve special attention? Among all the terms, which carry significant financial implications—and which might warrant renegotiation? Which terms are more founder-friendly?

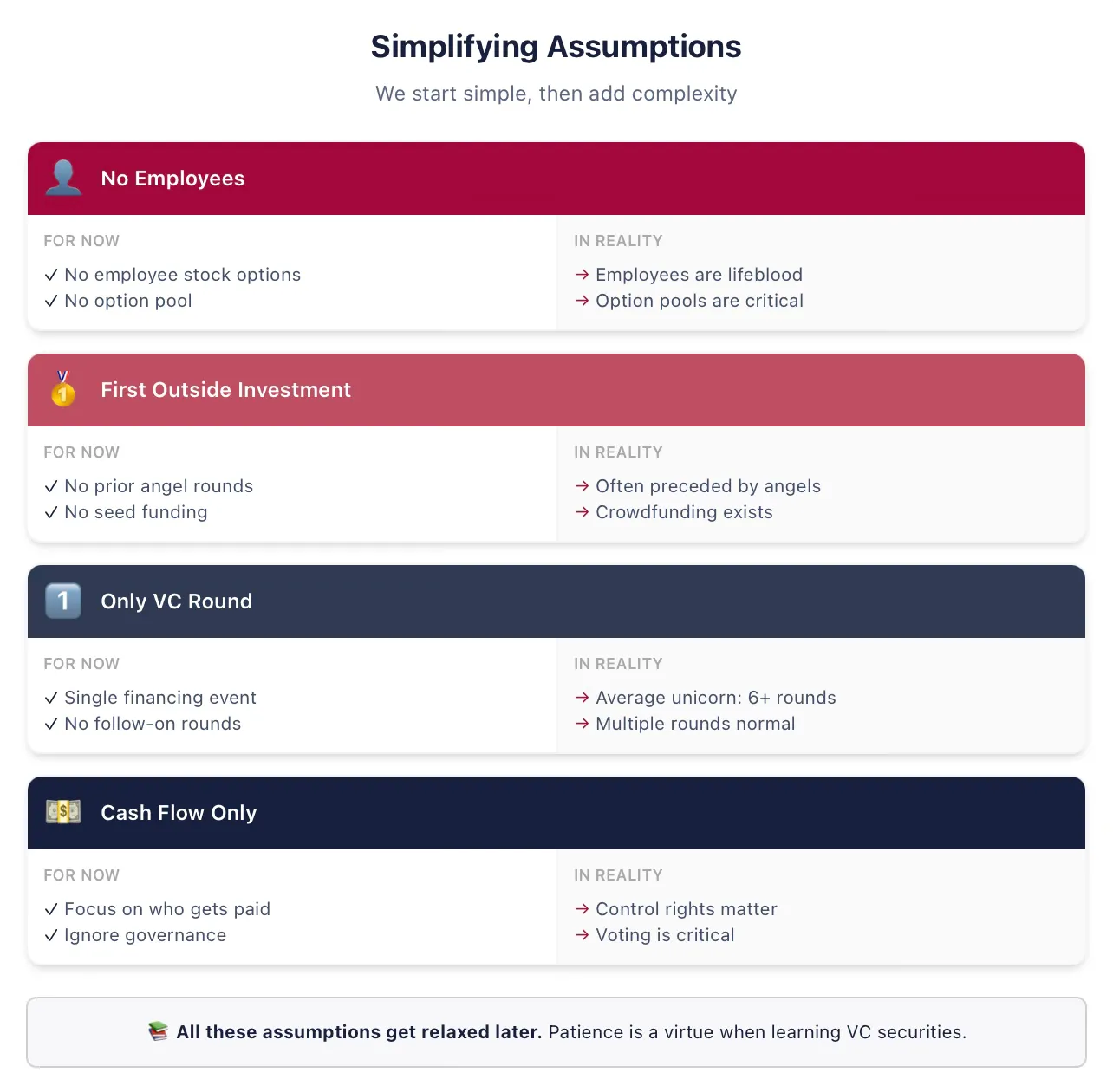

We’ll Begin with Simplifying Assumptions to Introduce All Concepts

To maintain clarity, we’ll start with some simplifying assumptions—which we’ll relax in subsequent notes, so stay tuned! Don’t tune out thinking, “Oh, this ivory-tower professor doesn’t know founders don’t ‘hold shares’ but rather ‘vest’ shares,” etc. I do know—and we’ll return to all of these points at the appropriate time.

Below are the assumptions I’ll consistently use in my initial notes on the first VC financing round (if any of these terms are unfamiliar, that’s precisely why we’re simplifying now):

Assumption: SoftMet hires no employees. This implies SoftMet incurs no cash or equity compensation expenses for employees—and treats the founders purely as owners, not employees. Vesting schedules and founder employment terms will be addressed later.

Assumption: Top Gun is SoftMet’s first external investor. In reality, most VC rounds follow angel or seed rounds using different securities.

Assumption: This round will be the only investment SoftMet raises as a privately held, VC-backed company. In reality, my research shows the average U.S. unicorn raises over six VC rounds—we’ll certainly relax this assumption soon.

Assumption: Only cash flow terms matter. Term sheets also cover corporate governance—control rights, voting rights, board seats—but we’ll address those later.

Investors Exchange Financial Securities for Returns

Top Gun’s $10 million investment constitutes a venture capital financing round—cash exchanged for securities. The $10 million Top Gun proposes to invest is called the investment amount.

In return for this investment, Top Gun receives securities granting it partial ownership of SoftMet. Specifically, a certain number of new securities—Series A Preferred Stock—will be issued in this round and allocated to Top Gun. But how many shares will Top Gun receive? What will Top Gun’s post-investment ownership percentage be? How will future returns be allocated between founders and VC investors?

The term sheet provides clues to answer these questions by specifying who receives what under different scenarios. The number of shares Top Gun receives is determined by the investment amount and the original issue price (OIP) of the Series A Preferred Stock. The OIP is the price per share paid by investors at issuance—commonly abbreviated as OIP, or sometimes referred to as the original purchase price (OPP).

Note: OIP differs from par value. Par value is an arbitrary value assigned to stock in the corporate charter during incorporation, bearing little relationship to the company’s actual valuation and having no real economic significance. Common par values are $0.001 or $0.0001—or “no par value.”

We can use the OIP to calculate the number of shares Top Gun receives. With a $10 million investment amount and an OIP of $4, Top Gun receives the quotient:

Thus, Top Gun invests $10 million in cash in SoftMet in exchange for 2.5 million shares of Series A Preferred Stock. More generally, the relationship among OIP, investment amount, and the number of shares received by investors in the round is:

Once you know any two of these three quantities, you can derive the third. Term sheets in practice vary widely in how they describe proposed investments—but you should always be able to back-calculate all three quantities from the information provided. SoftMet’s term sheet specifies both the investment amount and the OIP. Alternatively, a term sheet might specify the investment amount and the number of shares the investor receives.

Example 1: Original Issue Price

The VC fund Great Innovation Partners invested in the early-stage company Fox Solutions, Inc., acquiring 2 million shares of Seed Preferred Stock for a $25 million investment. What is the original issue price of this security?

The original issue price is:

In other words, Great Innovation paid $12.50 per share for the Seed Preferred Stock.

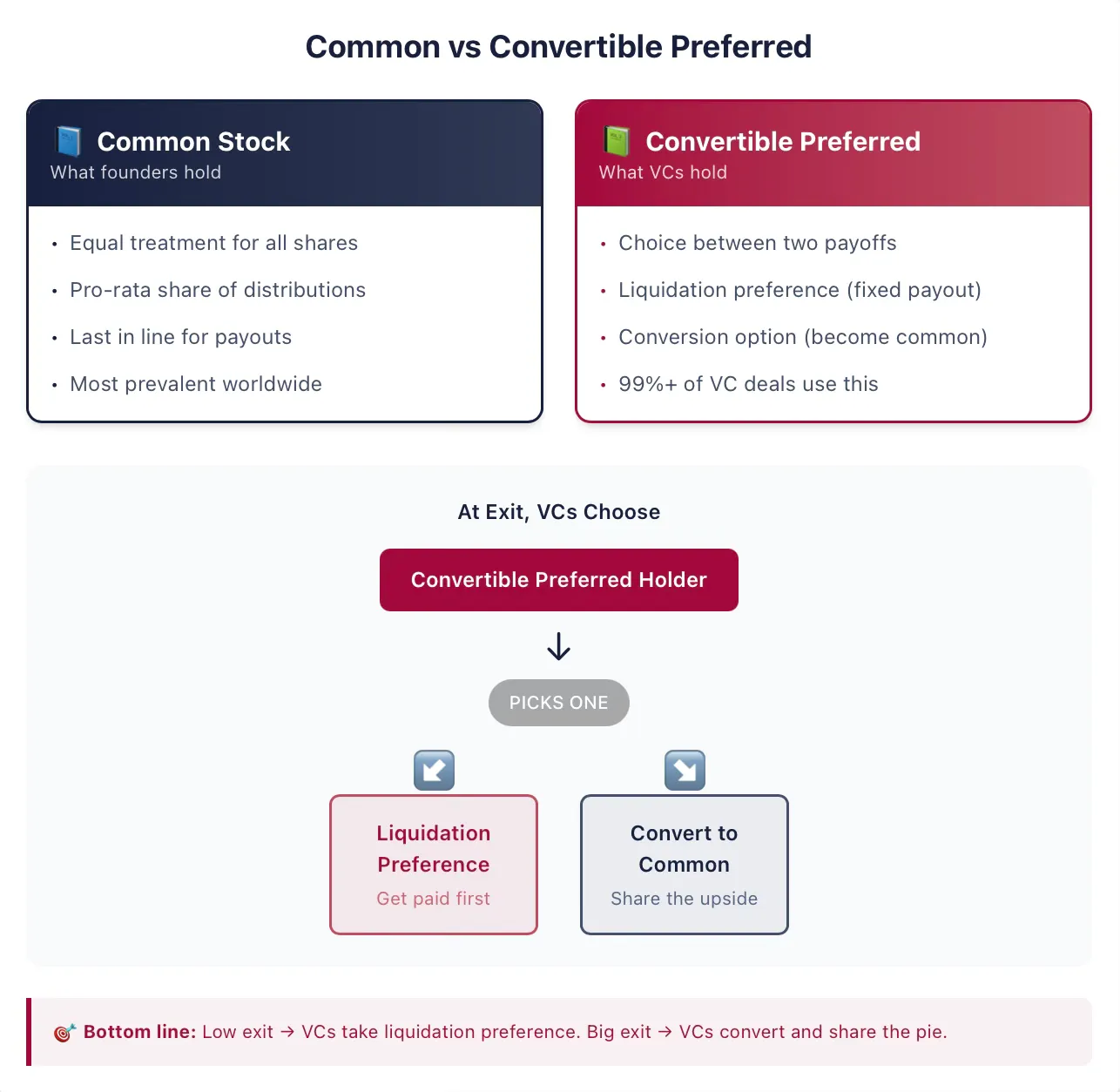

Founders Typically Hold Common Stock

Founders of early-stage companies typically hold common stock—the most widespread form of ownership in both public and private companies worldwide. Stock represents an ownership stake in a company and grants its holders (i.e., shareholders) certain rights. In other words, shareholders hold a claim on the company. Equity is another commonly used term describing this claim—and here, we’ll use “stock” and “equity” interchangeably. The terms “stock” or “equity” also distinguish these securities from another common type of corporate claim: debt.

The word “common” in “common stock” only acquires meaning if the company issues other types of securities. If common stock is the sole security issued, then every share stands on equal footing—there is only one class of claim! More generally, each share of common stock is treated identically to every other share of common stock.

When distributions are made, one share of common stock is entitled to the same distribution as any other share of common stock. Thus, distributions are allocated equally across all outstanding common shares. However, if other holders possess a different type of security, the distribution may differ substantially. In VC deals, this is almost always the case.

Investors Hold Convertible Preferred Stock

The Series A Preferred Stock Top Gun receives is an example of convertible preferred stock—the security most U.S. VC investors select. This instrument combines features of debt and common stock. Unfortunately for aspiring entrepreneurs or early-stage investors, its structure is relatively complex—especially compared to traditional financial securities like plain debt or common stock. Fortunately, we’ll master it together right now.

At its core, convertible preferred stock is a financial security granting its holder a choice between two possible payout options. The holder may elect to convert the convertible preferred stock into another security—typically common stock (this is the optional conversion feature). Or, the holder may receive a one-time payment before common stockholders receive any proceeds (this is the liquidation preference feature). This right usually comes with numerous附加 conditions and depends on many additional contractual terms we’ll explore. But the core idea is that the security gives investors the option to choose between the conversion feature and the liquidation preference feature.

A critically important point—especially for those with stock market or investment banking experience—is that companies in traditional financial markets sometimes issue securities called “preferred stock.” Though superficially similar, the securities issued in VC transactions possess many distinctive features that set them apart from public-market preferred stock. If your familiarity with preferred stock comes from the public markets—this is different. Do not skip this section.

Example 2: Publicly Traded Preferred Stock

In 2018, the large publicly traded insurance company MetLife issued a new series of preferred stock, MET-E, offering 28 million shares to the market. This preferred stock functions similarly to a debt instrument, providing investors with a perpetual fixed dividend. MET-E offers investors a 5.63% coupon rate but grants no voting rights (unlike common stock). Preferred stockholders enjoy priority claims on company income—receiving dividends before common shareholders (but after creditors). Preferred stock like MET-E typically lacks conversion features.

VC agreements commonly refer to this security simply as “preferred stock,” but whenever you see “preferred stock” in a VC agreement or term sheet, you can safely assume it is convertible. In my analysis of thousands of VC agreements, over 99% of “preferred stock” is, in fact, convertible.

Though agreements often omit the word “convertible” from the security’s name, they typically include other qualifiers. For instance, the security may be named “Series A Preferred Stock,” as in Top Gun’s proposed investment.

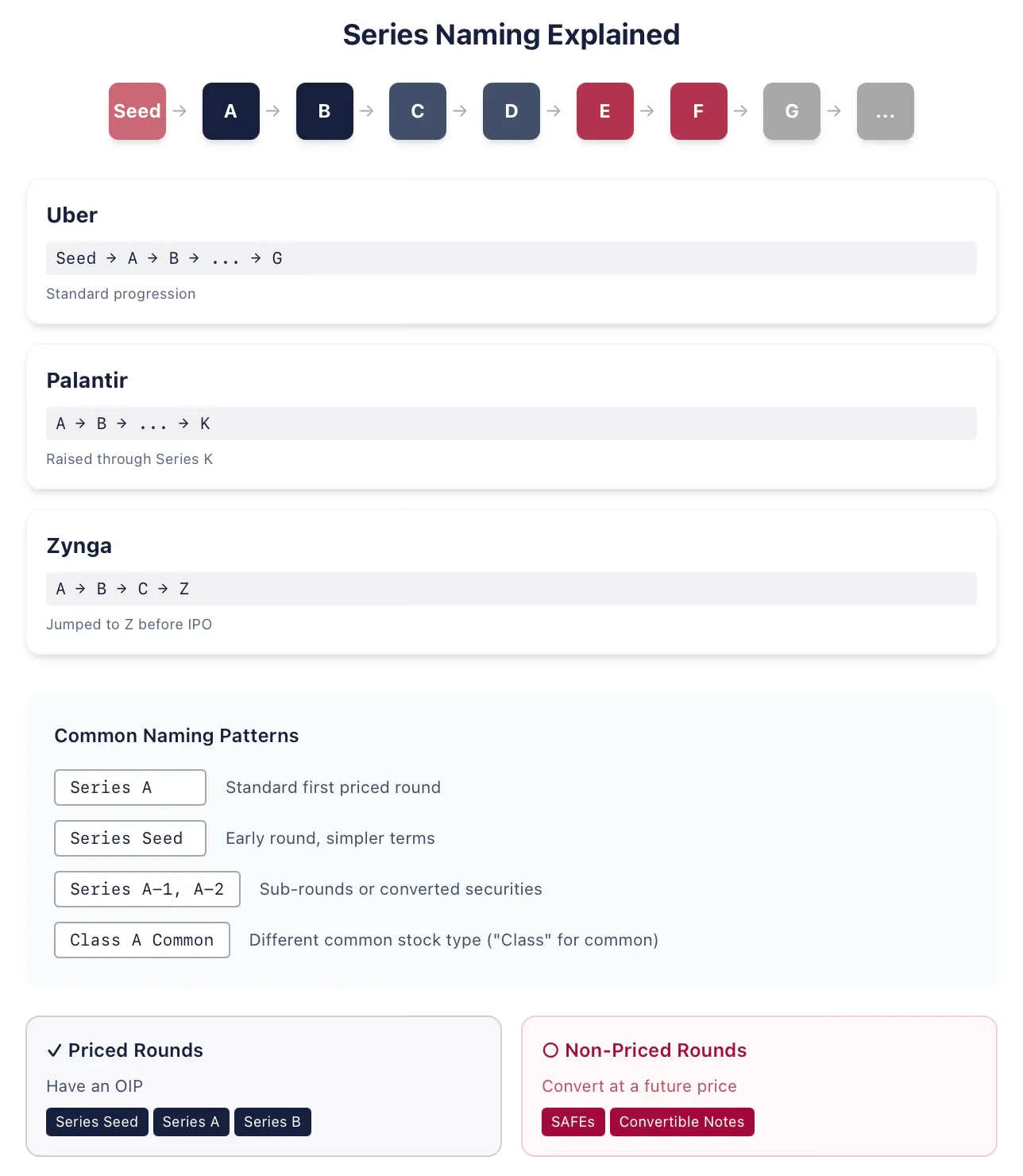

Example 3: Series Letters

The ride-hailing company Uber, while still a privately held, VC-backed company, sequentially issued Seed, Series A, Series B, and so on—up to Series G Preferred Stock. The big-data analytics company Palantir issued Series K Preferred Stock in its 2015 financing round (having previously issued Series A through J). The space company SpaceX, prior to its eventual IPO, will likely exhaust the entire alphabet naming its series of preferred stock (I’m writing this in January 2026). Sometimes companies issue securities out of alphabetical order—for example, during corporate restructurings. The online gaming company Zynga issued Series A, B, and C Preferred Stock, then jumped ahead to issue Series Z Preferred Stock just before its initial public offering.

Historically, Series A Preferred Stock was the name given to the security issued in the first VC financing round. Over the past fifteen years or so, the first security issued has also frequently been called “Seed Preferred Stock” (as with Uber). This often signals a simpler structure than a full Series A Preferred Stock—and may also convey that the company is very early-stage. Once the company completes another round, it typically issues Series A Preferred Stock. Thus, you shouldn’t assume “Series A” necessarily means the first VC round.

So what defines the first VC round? The best way to determine it is to ask whether the round is a priced round—that is, whether the securities have an OIP. If a company issues SAFEs or convertible notes, it is not a priced round; however, Seed Preferred Stock is a priced round. (Note: You’ll often hear that non-priced rounds assign no valuation to the company. This is incorrect—we’ll discuss why at the appropriate time.)

Lawyers advising VC investors and startups are quite creative with naming conventions—so there are many other variants. Sometimes subtle naming differences reflect specific arrangements. For example, any series may be followed by or accompanied by additional numbered sub-series (e.g., Series A-1, Series A-2, etc.). If part of the same round, such Series A-1 shares typically differ from Series A shares only in certain specific terms—otherwise they are identical—often because some outstanding securities were converted into (nearly equivalent) Series A shares. Or, they may belong to entirely separate financing rounds—for instance, because the company believes it hasn’t yet reached the milestones expected of a Series B company in its sector.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News