After $HYPE hits a new all-time high, is $PURR—the “HYPE version of MicroStrategy”—worth considering?

TechFlow Selected TechFlow Selected

After $HYPE hits a new all-time high, is $PURR—the “HYPE version of MicroStrategy”—worth considering?

PURR is not a company with actual operations; it is essentially a pure $HYPE stock packaging product.

Author: TechFlow

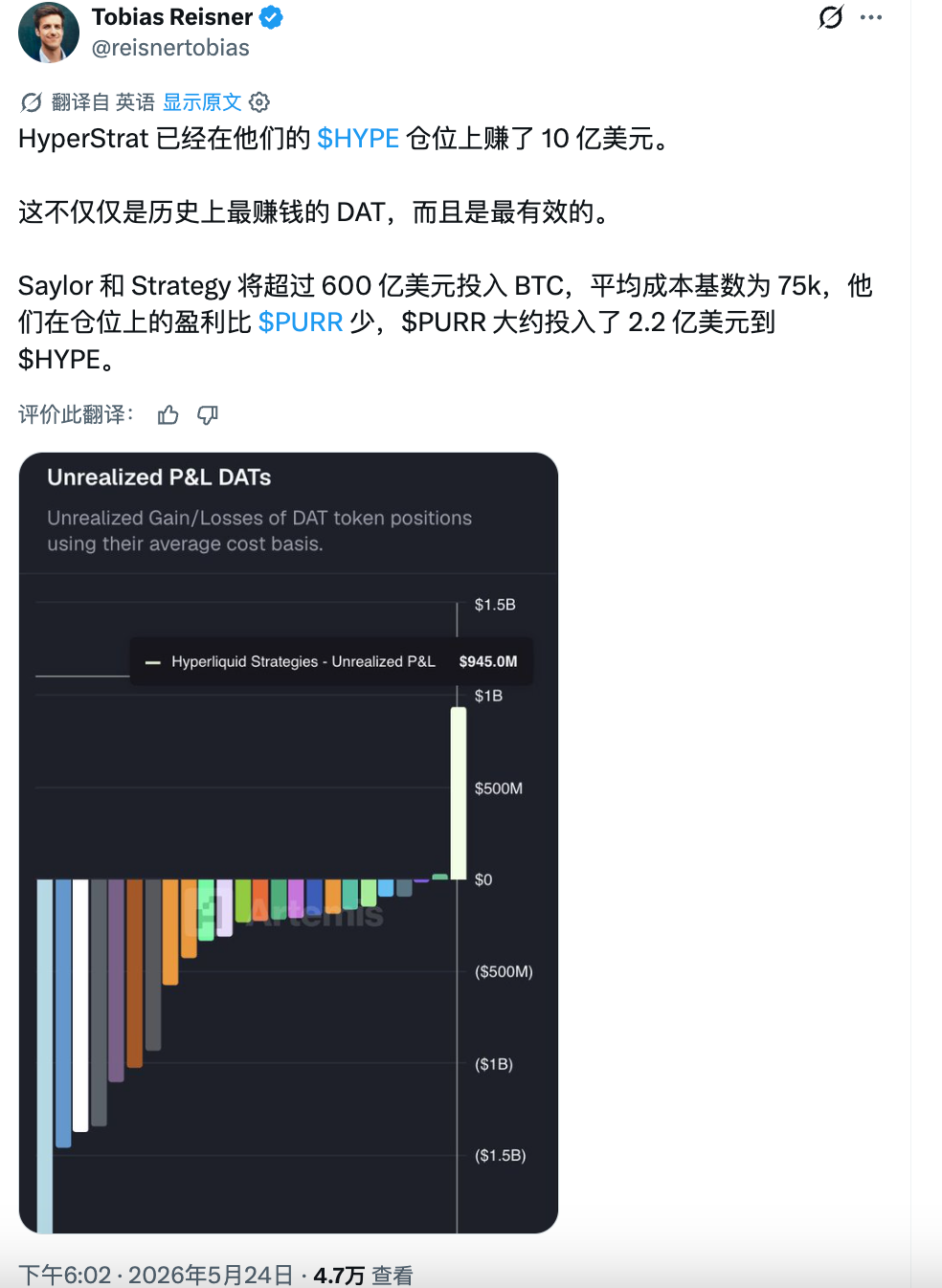

On May 24, a tweet about Hyperliquid Strategies (NASDAQ: PURR) sparked significant discussion across English-language crypto Twitter (CT):

The company purchased HYPE for approximately $220 million; its current unrealized gain is nearly $1 billion—surpassing even Michael Saylor’s Strategy (formerly MicroStrategy) in terms of capital efficiency on BTC.

This topic is now gradually spreading into Chinese-speaking communities. HYPE recently hit an all-time high above $62, with year-to-date gains exceeding 150%—making it one of the strongest-performing major crypto assets this year.

As the only publicly listed U.S. equity proxy for HYPE, PURR has also surged over 100% year-to-date, naturally becoming a FOMO target for U.S. equity investors and analysts.

However, before jumping on the bandwagon, several questions must first be clarified:

1. What exactly is this company?

2. How does it differ from buying HYPE directly?

3. Does the claim that its “capital efficiency exceeds MicroStrategy’s” hold up under scrutiny?

$PURR: A Pure DAT

Bottom line: PURR is not an operating company—it is effectively a pure stock wrapper for $HYPE.

Its business model can be summarized in one sentence: buy HYPE, stake HYPE, hold HYPE. As of April 2026, public disclosures indicate the company holds roughly 20 million HYPE tokens, along with approximately $113 million in cash and zero debt.

This means the entire value of the stock depends on a single variable: the price of HYPE.

With no underlying operations to analyze, evaluating such companies comes down to just two dimensions: the quality of the underlying asset itself—and who is managing the shell.

The latter determines capital allocation capability—for example, timing decisions around share issuance to buy more tokens, share repurchases to support the stock price, or management of the premium/discount relationship between market price and net asset value (NAV)—and ultimately shapes institutional investors’ willingness to use this vehicle as an access point.

Historically, PURR’s predecessor was Sonnet BioTherapeutics, a small Nasdaq-listed biotech firm. In July 2025, it announced a merger with Rorschach I; the transaction closed in December 2025 at an overall valuation of $888 million, after which the company rebranded as Hyperliquid Strategies and changed its ticker to PURR.

Notably, the merger was initiated by Paradigm and Atlas Merchant Capital.

Paradigm is one of the most prominent venture capital firms in the crypto industry, having backed Uniswap, Blur, Friend.tech, and others. Its involvement in the Hyperliquid ecosystem runs deep—and in this case, it directly participated in structuring the SPAC.

Atlas Merchant Capital is a financial services investment firm headquartered in New York and London. Its two founders occupy key leadership roles at PURR: Chairman Bob Diamond, former CEO of Barclays Bank, and CEO David Schamis, formerly a partner at JC Flowers.

The board also includes Eric Rosengren, former President of the Federal Reserve Bank of Boston, and Larry Leibowitz, former COO of the NYSE. Other participants include Galaxy, D1, and Pantera—all top-tier institutions in crypto and macro investing.

Most DAT companies are led by executives from native crypto backgrounds; PURR’s leadership team, by contrast, consists almost entirely of veterans from traditional finance.

$HYPE Strength Drives $PURR Surge

PURR’s recent attention in Chinese-speaking circles stems directly from HYPE’s own strength.

HYPE rose steadily from ~$25 at the start of the year, breaking above $62 in May to set a new all-time high—delivering over 150% year-to-date gains. Against a backdrop of BTC trading sideways and relatively muted YTD performance from ETH and SOL, HYPE stands out as the brightest performer among major crypto assets this year.

Our prior article already dissected Hyperliquid’s fundamental flywheel: ~70% market share in perpetual DEXes, weekly fee revenue exceeding $10 million, and 97% of protocol fees allocated to HYPE buybacks and burns—a self-reinforcing cycle that remains firmly in acceleration mode.

(See also: “Market Watch: From HYPE to ZEC—Four Narrative Threads Behind Recent Altcoin Momentum”)

As HYPE rises, PURR naturally follows suit.

As the only HYPE proxy currently listed on U.S. equities markets, PURR has gained over 100% YTD—rising from ~$3 to a recent peak of $8.79.

For investors with only U.S. brokerage accounts—and no direct access to crypto markets—PURR is virtually the sole option to gain exposure to HYPE. Yet what propelled PURR from a niche instrument to a social-media talking point were several institutional signals that converged in May.

Goldman Sachs disclosed a purchase of ~650,000 shares of PURR in its Q1 13F filing—an amount modest in dollar terms (~$3.3 million), but bearing the powerful endorsement of Goldman’s name. Concurrently, 21Shares and Bitwise launched their HYPE spot ETFs on Nasdaq and NYSE respectively, while Cantor Fitzgerald raised its price target on PURR from $6 to $8.

These developments coincided with HYPE’s all-time high, thrusting PURR into broader investor awareness.

Then came the tweet referenced at the outset: PURR deployed $220 million to buy HYPE and now boasts nearly $1 billion in unrealized gains—implying, on a short-term basis, superior capital efficiency versus MicroStrategy.

Such sharp appreciation inevitably draws intense attention. Still, investors considering action should proceed with caution.

Is PURR Truly the Most Capital-Efficient DAT?

Strategy (formerly MicroStrategy) has invested over $60 billion in BTC at an average cost of ~$75,000 per coin; PURR spent only ~$220 million on HYPE yet achieved nearly identical—or even greater—unrealized gains. Does this mean PURR’s “capital efficiency” vastly exceeds MicroStrategy’s?

Numerically, the comparison checks out—but logically, it’s misleading.

PURR’s early HYPE holdings carry an average cost of ~$7, compared to the current price of $62—a near 9x increase. Strategy’s BTC average cost sits around $75,000, and BTC’s current price hovers near that level—meaning virtually no appreciation.

Thus, PURR’s higher unrealized gains stem not from smarter corporate actions, but simply from the underlying asset’s vastly superior price performance. Any investor who had bought HYPE spot at the same time with the same capital would have achieved identical returns—without assuming equity dilution risk.

In other words, this is a victory of “picking the right token.” If PURR had been established six months later—entering at $40 for HYPE—the “capital efficiency” narrative would completely collapse.

For U.S. equity investors newly noticing PURR, the more practical question is: At today’s price, are you paying a premium or discount relative to the intrinsic value of the HYPE held by the company?

This brings us to the core valuation metric for DAT companies: mNAV (modified Net Asset Value per share).

We performed a quick mNAV calculation using data from PURR’s official dashboard and SEC filings.

The company currently holds 20.8 million HYPE (valued at ~$1.296 billion at current prices), plus $114 million in cash. After deducting deferred tax liabilities and other obligations, its net asset value totals ~$1.34 billion.

Based solely on the 134.6 million shares currently outstanding, NAV per share is ~$9.98—versus the current stock price of $7.67, implying a ~23% discount. Including the ~29.8 million outstanding warrants fully dilutes the share count to ~155 million, bringing NAV per share to ~$8.66 and narrowing the discount to ~11%. However, the company has recently registered an additional 35.16 million shares for issuance; if all are fully exercised, the denominator expands to ~190 million shares, reducing NAV per share to ~$7.07—turning the current price into a slight 1.08x premium.

Therefore, whether PURR is “cheap” or “expensive” hinges entirely on how much future dilution you expect.

Share issuance isn’t inherently negative. If management issues shares at a substantial premium and uses proceeds to acquire more HYPE, the HYPE holdings per share may actually increase. But if the company continues issuing shares during periods of weak sentiment—when the stock trades below NAV—it erodes existing shareholders’ value.

The company is only six months old and has yet to weather a full market downturn. There is no historical record of how management will behave under extreme conditions.

Also note: Our calculation uses deferred tax liabilities of $60.5 million, as reported in the Q3 financial statements ending March 31. Since then, HYPE’s price has risen significantly further—so the corresponding unrealized tax liability has likely increased, meaning actual NAV could be lower than our estimate.

What’s the Real Difference Between Buying PURR vs. HYPE Directly?

This is the most practical question. Since PURR’s entire value derives from HYPE, why not bypass the middle layer and buy HYPE outright?

The answer is simple: Some investors physically cannot. U.S. retirement accounts (IRAs, 401(k)s), traditional brokerage accounts, and certain institutional funds subject to strict compliance requirements are prohibited from holding crypto assets directly.

Moreover, Hyperliquid’s platform frontend explicitly restricts access for U.S. residents.

Thus, PURR provides a Nasdaq-listed equity wrapper enabling these investors to obtain HYPE exposure via standard stock trading. Paradigm’s shell, in essence, sells precisely this regulatory conduit.

If you fall into this category, PURR truly is—at present—nearly the only viable option. Although 21Shares and Bitwise’s HYPE spot ETFs launched in mid-May, they’re still extremely new, with liquidity and tracking error yet to be proven.

But if you *can* buy HYPE directly, then PURR’s equity wrapper becomes nothing more than friction—with purely negative implications—not an additive source of HYPE beta exposure.

This cost manifests across several dimensions:

First, dilution risk. Holding HYPE directly means your ownership stake cannot be diluted. Holding PURR shares exposes you to ongoing risk of new share issuance to fund additional HYPE purchases.

Second, incomplete return transmission. Direct HYPE holders can stake their tokens to earn staking yields, and receive airdrops and ecosystem incentives directly. Through PURR, staking rewards flow first into the company’s treasury, where operational costs and taxes are deducted before any residual benefit filters through to NAV per share.

Third, timing and pricing friction. HYPE trades 24/7; PURR trades only during U.S. equity market hours. If HYPE experiences large moves over weekends or after hours, PURR holders must wait until market open to react.

Fourth, counterparty risk. SEC filings disclose that PURR holds all its HYPE tokens with a single custodian. By holding PURR, your asset security depends entirely on that custodian’s solvency and the company’s continued operational integrity.

The author’s view is that PURR functions more like a “distribution product” than an “investment product.” Its sole value lies in bridging traditional financial accounts to HYPE—nothing more. If you don’t need that bridge, every added layer introduces unnecessary risk.

Therefore, for crypto and U.S. equity investors in Chinese-speaking communities, the conclusion is straightforward:

Your decision should hinge solely on whether you’re bullish on HYPE—not on whether you’re bullish on the PURR shell.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News