Bernstein Research Report Analysis: CoreWeave 2Q Transition Quarter, Focus on Power Ramp-up Rather Than Revenue Surge

TechFlow Selected TechFlow Selected

Bernstein Research Report Analysis: CoreWeave 2Q Transition Quarter, Focus on Power Ramp-up Rather Than Revenue Surge

Bernstein's concern is that once data center supply is no longer tight after 2028, CoreWeave's business logic may not support its current valuation.

By: Rita

TechFlow Guide

Bernstein released its CoreWeave (CRWV) 2Q26 earnings preview on July 9, maintaining an Underperform rating with a target price of $67. With the current price at $90, this implies 26% downside. 2Q is likely a transition quarter; the real earnings inflection point will only emerge after power capacity ramps up to 1.7 GW in the second half. 1Q has already exposed execution issues, with adjusted operating profit at only $21 million, far below the company's previous guidance of over $100 million. Bernstein is concerned that once data center supply is no longer scarce after 2028, CoreWeave's business logic may not support the current valuation.

2Q is a Transition Quarter, Power Ramp-up is the Key Variable

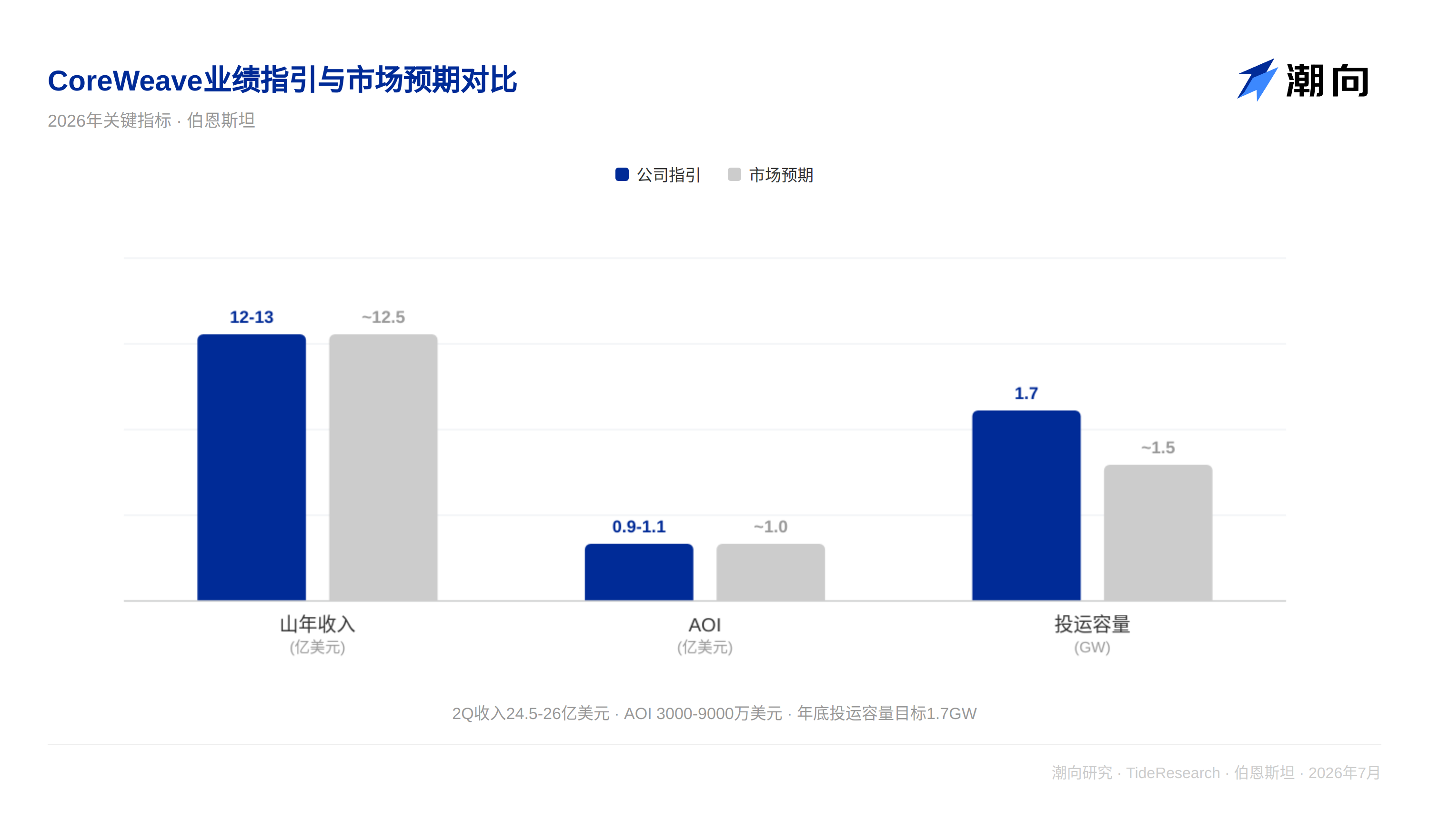

CoreWeave expects to release 2Q earnings in early August. The company's 2Q revenue guidance is $2.45 billion to $2.6 billion, with adjusted operating profit guidance of $30 million to $90 million. Management reiterated the target operational capacity of 1.7 GW by the end of 2026, full-year 2026 revenue guidance of $12 billion to $13 billion, and increased the annualized exit revenue target from $17 billion to $19 billion to $18 billion to $19 billion.

Bernstein believes a lukewarm 2Q meets expectations. 2026 capacity is fully sold out, and most of 2027 is also locked, so revenue surprises are unlikely in the short term. The real variable lies in the power delivery schedule; power will not truly come online until 2H26. Whether the operational capacity ramp-up proceeds smoothly will determine whether second-half earnings can materialize.

Management has repeatedly emphasized that there are no signs of slowing AI demand, but the growth rate of operational capacity is the key variable determining earnings. The leasing environment remains hot, but power supply will remain tight over the next 6 to 12 months. This supply-demand mismatch is both the source of CoreWeave's current pricing power and the area with the greatest execution risk.

Execution Issues Exposed in 1Q Worth Heeding

1Q26 adjusted operating profit was only $21 million, far below the company's previous expectation of "over $100 million." Management's explanation was "timing rather than economics"; powered shells begin incurring leasing, power, and depreciation costs before contributing revenue, while contributing gross margin typically normalizes in the third month.

Bernstein remains skeptical about this. Analysts calculate that if project-level gross margin falls below 21% or the average deployment cycle exceeds 8 weeks, FY26 adjusted operating profit may miss expectations; this threshold is not high. CoreWeave is in a hyper-growth phase, making perfect execution nearly impossible. Historical data shows that following earnings announcements in the past three quarters, the stock price fell by 11% to 21% respectively. One week later, the decline expanded to 11% to 38%, and after one month, there was still a decline of 14% to 22%. Even if operational data is solid, earnings season may still bring pressure to the stock price.

Long-term Concerns: 2028 Where is the Moat After?

Bernstein's long-term skepticism regarding CoreWeave focuses on the period after 2028. Once data center supply is no longer scarce, hyperscalers are likely to compete head-on with Neoclouds for enterprise clients. Bernstein remains doubtful whether CoreWeave's software moat can withstand attacks from AWS, Azure, and GCP.

Bernstein does not believe a structural shift will be seen before 2027 and expects CoreWeave to sign approximately $45 billion in new contracts by the end of 2027. However, after 2027, Bernstein's view begins to diverge from market consensus; by 2028, Bernstein's revenue forecast is about 15% lower than consensus, and the gap continues to widen. This time difference means that both short-term bullish and long-term bearish logic hold true simultaneously; investors need to clarify which time window they are betting on.

TechFlow Perspective

CoreWeave's valuation bets on two things: that the growth rate of AI compute demand can continue to exceed the speed of data center supply expansion, and that it can defend its niche market as an independent GPU cloud provider amidst encirclement by hyperscalers. Bernstein's Underperform rating essentially bets that at least one of these two assumptions will fail.

The most valuable part of this report is not the $67 target price, but the clear timeframe provided by Bernstein: before 2028, the supply scarcity story can still support the valuation; after 2028, if data center supply is released in large quantities, CoreWeave's moat may be much shallower than the market imagines. The pace of contract signing in 2027 will be an early signal to verify this judgment.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party brokerage research report (Bernstein, July 9, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage's analysts, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market involves risks; decisions should be made independently. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News