Bernstein Research Report Analysis: AI Agents Ignite CPU Demand, Memory Interface Chip TAM Triples in Three Years to $20 Billion

TechFlow Selected TechFlow Selected

Bernstein Research Report Analysis: AI Agents Ignite CPU Demand, Memory Interface Chip TAM Triples in Three Years to $20 Billion

Memory interface chips are transitioning from a supporting role of "following the DRAM cycle" to a direct beneficiary of "AI computing power expansion".

Written by: Rita

TechFlow Guide

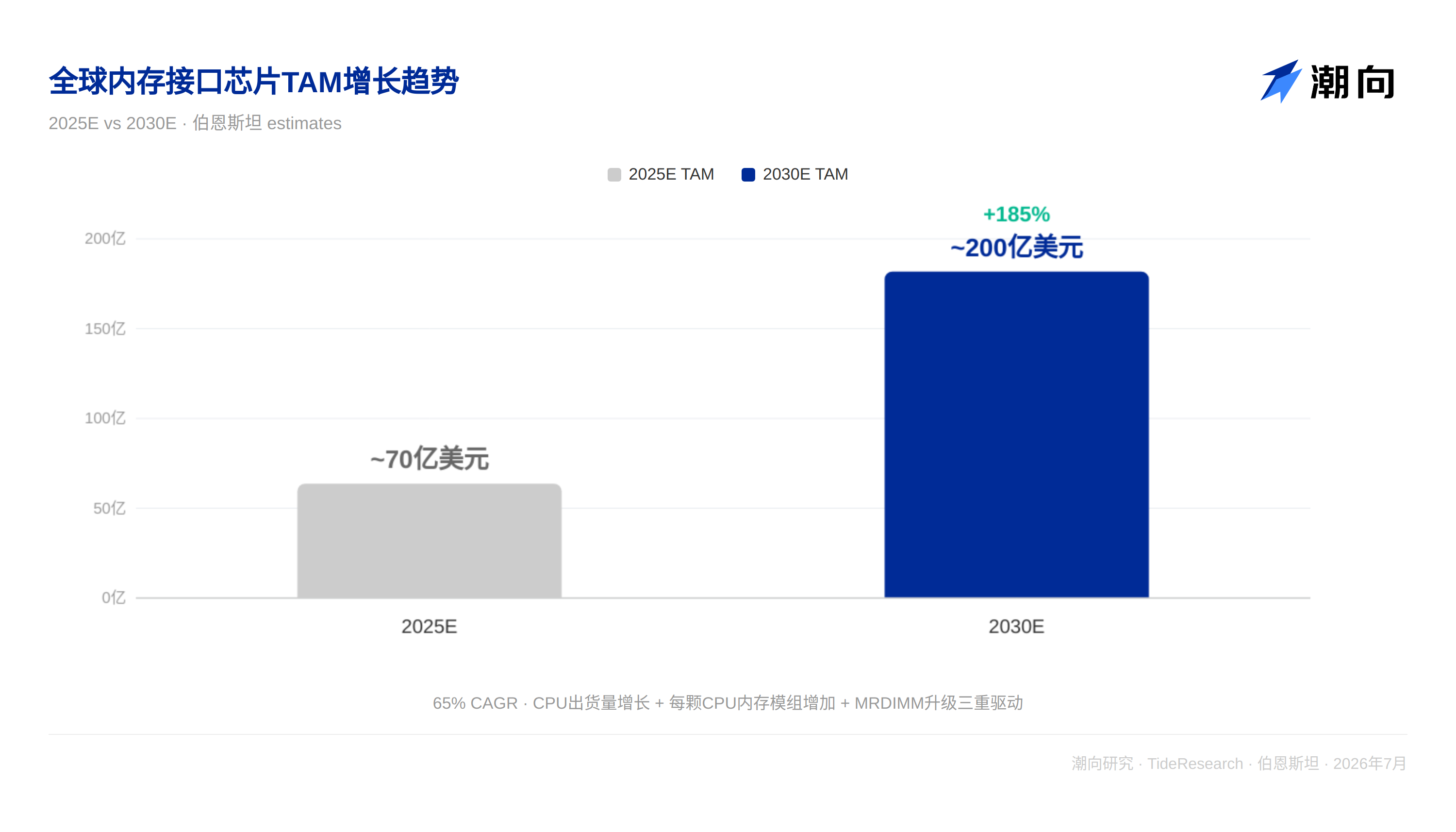

On July 9, Bernstein released an in-depth primer report on memory interface chips, pointing out that AI is evolving from training-intensive to inference-intensive, with CPUs becoming core orchestrators again in AI agent workloads, driving structural growth in server CPU shipments. The report significantly raised the global memory interface chip TAM forecast to $20 billion by 2030 (previously about $7 billion), corresponding to a 65% five-year CAGR. Montage Technology's A-share target price was raised from 220 yuan to 400 yuan, and H-shares from 320 HKD to 520 HKD, both maintaining Outperform ratings. Renesas Electronics target price is 6,300 yen, also maintaining Outperform.

Three Drivers Overlap, TAM Jumps from 7 Billion to 20 Billion

Bernstein judges that memory interface chips are encountering a rare window where triple structural benefits overlap simultaneously.

The first is accelerated growth in server CPU shipments. In AI agent workloads, responsibilities undertaken by CPUs such as task scheduling, KV cache management, and real-time security checks can account for 50% to 90% of task completion time. AMD recently doubled its 2030 global x86 server CPU TAM forecast to $120 billion, confirming this trend. Bernstein expects global server CPU shipments (excluding Nvidia proprietary CPUs) to increase from 30.6 million units in 2025 to 89.3 million units in 2030, corresponding to a 24% CAGR.

The second is the continuous increase in the number of DRAM modules equipped per CPU. To maximize accelerator utilization, AI servers generally increase DIMM slot fill rates to 70% to 80%, far higher than the about 50% in general-purpose servers. As CPU channels evolve from 8 channels to 12 channels and 16 channels, the demand for memory interface chips per CPU directly doubles.

The third is the leap in value per module brought by MRDIMM upgrades. MRDIMM adopts a "1 MRCD + 10 MDB" architecture, while traditional RDIMM requires only 1 RCD. The value of memory interface chips per module surges from about $7 to $70 to $80, an increase of about 10 times. Bernstein expects MRDIMM penetration to rise from about 3% in 2026 to 25% in 2030.

The three drivers are a multiplier effect rather than simple addition. Bernstein raised the 2030 TAM from about $7 billion to $20 billion.

MRDIMM Why Can Succeed? Three Structural Differences

The question most frequently asked by the market is: LRDIMM in the DDR4 era never exceeded 1% penetration, why is MRDIMM different?

Bernstein gave three structural differences. First, LRDIMM solved the capacity problem; it increased capacity but not bandwidth, and capacity was not the bottleneck in the DDR4 era. MRDIMM solves both capacity and bandwidth dimensions simultaneously; its multiplexing architecture doubles single-module bandwidth, directly hitting the bandwidth bottleneck of AI workloads. Second, RDIMM was "good enough" in the DDR4 era, but cannot maintain signal integrity at speeds above DDR5 8800MT/s; migration to MRDIMM is driven by physical laws, not marketing. Third, neither Intel nor AMD has released a product roadmap for DDR5 LRDIMM, while MRDIMM has obtained clear support from both major CPU platforms.

In addition, AI servers created a customer base that did not exist in the DDR4 era. AI servers fill DIMM slots to full capacity and push every specification to the limit, making them the most natural customer group for MRDIMM, which pursues maximum bandwidth. DRAM price increases are also narrowing the cost gap between MRDIMM and RDIMM, further reducing migration resistance.

Oligopoly Pattern: Three Companies Control Over 90% Share, Extremely High Barriers

The memory interface chip market is a textbook oligopoly. Montage Technology (about 37%), Renesas (about 36%), and Rambus (about 20%) collectively occupy about 92% of the global market share.

Entry barriers are extremely high. JEDEC standard certification requires chips to pass verification by DRAM manufacturers, CPU platforms, module manufacturers, CSPs, and others; the entire process usually takes 18 to 24 months. Any design flaw or interoperability failure may lead to the supplier being completely eliminated. In addition, RCD and MRCD are the most technically complex components in DIMM chipsets, using the most advanced CMOS processes; DDR4 RCD was on the 40nm platform, DDR5 first-generation RCD started from 28nm, and will evolve to below 10nm in the future. All three suppliers are deeply involved in JEDEC standard setting; Montage and Renesas are even JEDEC board members, setting thresholds that new entrants must cross while defining standards.

In the MRDIMM field, Montage and Renesas jointly lead the first-generation products, while Rambus chose to skip the first generation and directly enter the second generation. Competition for the second-generation MRDIMM (12,800MT/s) will be more balanced.

Montage Technology: Rare AI Target, H-Shares Enjoy Premium

Bernstein raised Montage's A-share target price to 400 yuan (previously 220 yuan), based on 50x rolling P/E for 2027Q3-2028Q2; H-share target price 520 HKD (previously 320 HKD), implying about a 15% A-share premium.

The H-share premium reflects global investors viewing Montage as a rare Chinese AI exposure target, and unlike other Chinese semiconductor companies, it does not face direct geopolitical risks from the Entity List or export controls. H-shares have limited float due to lock-up periods, and the premium is expected to be maintained in the short term.

Montage's growth drivers come from three aspects: the volume increase of interface chips brought by MRDIMM penetration increase, memory interface demand driven by CPU shipment growth, and contributions from new businesses such as PCIe Retimers. Bernstein expects Montage's 2027/2028 EPS to reach 5.68 yuan/10.82 yuan respectively.

TechFlow Perspective

The core judgment of this Bernstein report is: memory interface chips are changing from a supporting role "following the DRAM cycle" to a direct beneficiary of "AI computing power expansion." The re-evaluation of the CPU's role in the AI agent era, from a "bystander" during training to a "commander-in-chief" during inference, is the starting point of the entire logic. The multiplier effect of the overlap of three drivers made the TAM jump from about 7 billion to 20 billion; this magnitude of leap is extremely rare in semiconductor sub-sectors.

Whether MRDIMM can succeed is the key variable validating the entire story. The lesson from LRDIMM's failure shows that technical upgrades must simultaneously solve real bottlenecks (bandwidth rather than capacity), obtain clear support from CPU platforms, and have a sufficiently large customer base. The explosion of AI servers happens to satisfy these three conditions.

The premium of Montage H-shares relative to A-shares is worth noting. The premium caused by limited HK stock float may be maintained in the short term, but there is a risk of narrowing after the lock-up period ends. For A-share investors, Montage's scarcity logic and H-share premium logic are exactly opposite; A-shares do not have a geopolitical discount, but also lose the H-share scarcity premium. The dynamic change in the price difference between the two places is itself a trading signal worth continuous tracking.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party brokerage research report (Bernstein, July 9, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News