Bernstein Research Report Analysis: iPhone Share Continues to Expand but Growth Slows, China Region Drag Significant

TechFlow Selected TechFlow Selected

Bernstein Research Report Analysis: iPhone Share Continues to Expand but Growth Slows, China Region Drag Significant

The fundamental problem facing Apple is not that iPhone shipments have peaked, but rather that the valuation logic is shifting from hardware growth to ecosystem and service monetization.

By: Rita

TechFlow Guide

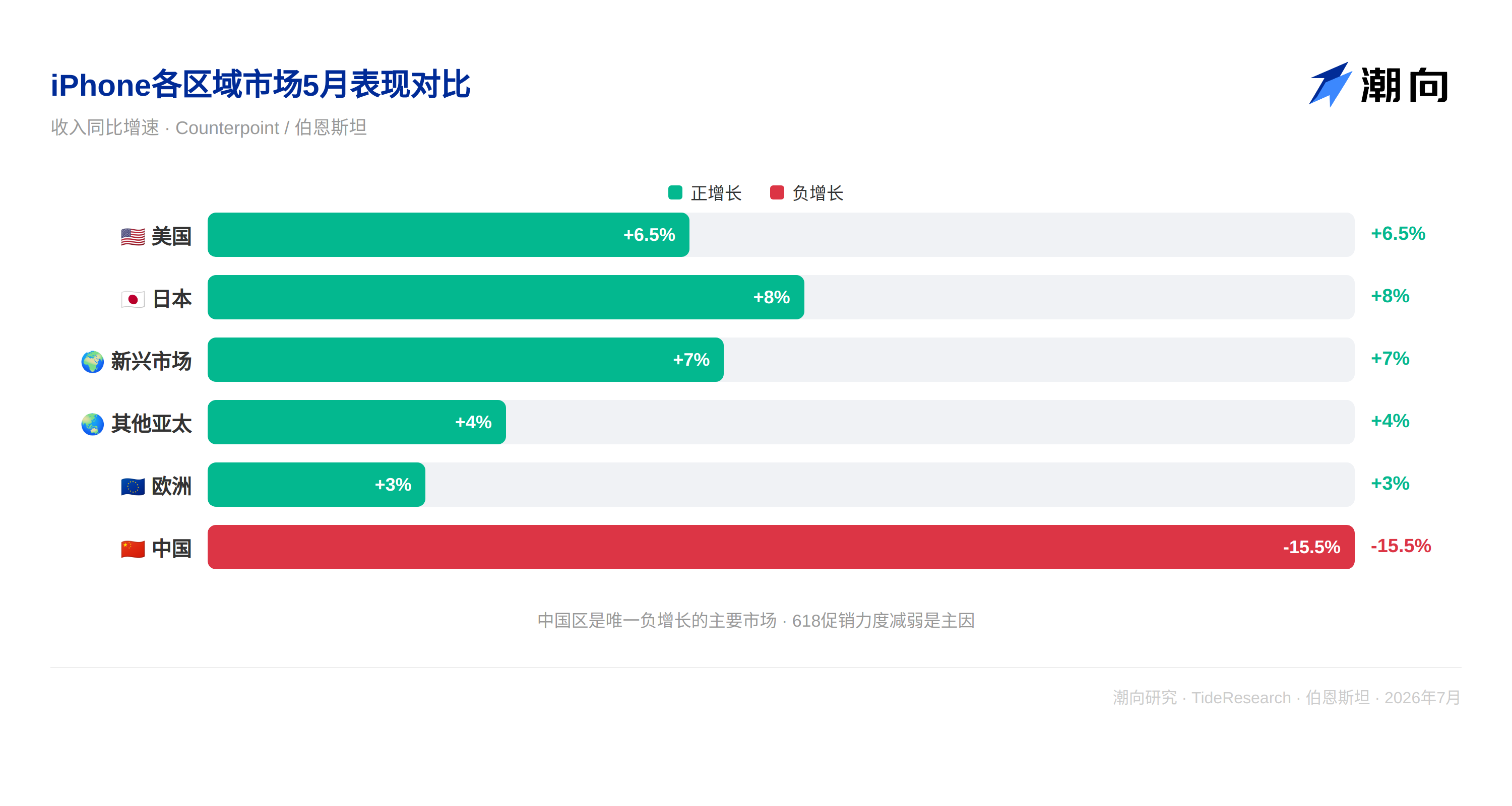

Bernstein released its May Apple tracking report on July 8, iPhone shipments in May grew 2% YoY and 1% MoM, with share continuing to expand. However, ASP decreased slightly by 1.2% YoY, ending a 6-month consecutive ASP growth trend. China region revenue declined 15.5% YoY, the only major market with negative growth, mainly due to weakened 618 promotion intensity. FQ3 first two months data was slightly below historical seasonal averages, Bernstein believes this may be a signal to watch, but remains positive on the supply chain overall.

Shipment volume growth slows, but share continues to expand

iPhone shipments in May grew 2% YoY and 1% MoM. Almost all markets achieved positive growth, Japan and emerging markets performed strongest, China region drag was obvious, revenue declined 15.5% YoY.

In the US market, iPhone sales grew 6.5% YoY, market share expanded from 50% in April to 53% in May, continuing to squeeze the Android camp. Europe and other Asia-Pacific markets also maintained positive growth.

Japan market growth was the strongest, emerging markets continued to contribute incremental volume. Bernstein believes iPhone's differentiated performance in different regional markets reflects differences in Apple brand penetration depth in markets with different price sensitivities, loyalty in high-end markets and penetration in low-end markets are both improving.

Bernstein emphasizes that slowing iPhone shipment growth does not equal share loss. In most markets, Apple's share is expanding, it's just that overall smartphone market growth is also slowing, especially in China.

China region is the biggest drag, 618 promotion intensity weakening is the main reason

China region iPhone May revenue declined 15.5% YoY, sales volume declined 19.1% YoY, ASP increased 4.4% YoY. This is the first YoY decline in China region since the iPhone 17 series launch, and also the only major market with negative growth globally.

The core reason lies in the 618 promotion. During 2025 618, iPhone 16 Pro discount was about 175-295 yuan, and after falling below the 6000 yuan threshold, could stack government subsidy of 500 yuan. During 2026 618, iPhone 17 Pro discount was only about 145 yuan, and price remained above 6000 yuan, unable to enjoy government subsidy. Base model iPhone 17 had about 30 yuan discount and fell below threshold, but overall promotion intensity was far less than last year.

Bernstein's interpretation is: this is not a problem of Apple product competitiveness, but more of a phased mismatch between promotion strategy and subsidy policy. Apple's pricing strategy for high-end models conflicting with government subsidy thresholds led to cost-performance advantage being temporarily weakened, but Apple's share in China market still expanded from 16% in April to 18% in May, indicating even with weakened promotion intensity, Apple is still eating Android's share.

ASP declines for the first time, e series share rise is the main reason

iPhone May ASP decreased slightly by 1.2% YoY, ending a 6-month consecutive ASP growth trend. The main reason is the sales share of iPhone 17e and 16e increased, e series combined sales volume increased from 1.7 million units in May 2025 to 1.9 million units in May 2026, proportion of total sales volume rose from 10% to 11%.

e series ASP is far lower than other iPhone family products, its share rise naturally pulled down overall ASP. Bernstein believes e series share rise itself is not a bad thing, it shows Apple is competitive in mid-range market, can find new incremental space when high-end market penetration is near saturation. But short-term drag on ASP is real, need to continue observing if e series share will rise further.

Supply chain: TSMC N3P under pressure but AI fills gap, DRAM content continues to grow

For TSMC, iPhone 17e sales were less than 16e, plus iPhone 17 discounts during 618 were not as good as last year, leading to N3P wafer shipments slightly weaker than previous generation N3E. But Bernstein believes even if Apple or other mobile customers release advanced process capacity, AI applications will fill the gap, TSMC will not lose revenue because of this.

In terms of DRAM, iPhone May average DRAM capacity reached 9.6GB, up 27% YoY. Models equipped with 12GB DRAM share rose to 43%, 8GB+ models share reached 95%. Bernstein points out Apple is accelerating DRAM content increase to support on-device AI, but need to watch if storage chip price increases will affect this trend.

In terms of supply chain individual stocks, Bernstein believes Luxshare Precision and lens suppliers sentiment is strong, iPhone shipments stronger than Android, and both have steady progress in AI-related business. Sony CIS will not have upgrades this year, may lose share to Samsung in 2027. Qualcomm's proportion in Apple revenue will decline as Apple self-developed chips advance, Android market weakness also constitutes pressure on handset manufacturers.

Bernstein gives Apple target price 350 USD, corresponding to about 35 times P/E ratio in 2026, based on judgment that iPhone 17 demand is stronger than expected, software and service ecosystem continues to expand.

TechFlow Perspective

The most valuable part of this Bernstein report is that it distinguishes between "iPhone sold less" and "iPhone sold poorly" these two completely different concepts. Shipment growth rate dropped from double digits to single digits, but share is expanding; ASP declined for the first time, but e series strategy is helping Apple reach wider user groups; China region revenue declined, but share is still rising.

The fundamental problem Apple faces is not iPhone shipments peaking, but valuation logic is shifting from hardware growth to ecosystem and service monetization. Bernstein's given target price 350 USD corresponding to 35 times P/E ratio, implies market's continuous growth expectation for service revenue, not iPhone shipment continued expansion. If service revenue growth rate slows in subsequent quarters, 35 times P/E ratio safety margin will narrow rapidly.

For investors, this report provides an important observation framework: in AI feature-driven replacement cycle, iPhone shipment growth slowing is normal phenomenon, key is whether Apple can improve single device value and service subscription rate through AI features. 2026 second half iPhone 18 series launch AI feature upgrade magnitude will be the key window to verify this logic.

Disclaimer

This article is TechFlow Research's organization and interpretation of third-party broker research report (Bernstein, July 8, 2026). Ratings, target prices, earnings forecasts and related judgments cited in the text are all the views of the broker analyst, only represent their affiliated institution's stance, do not represent TechFlow Research's views, nor constitute any investment advice.

Market has risks, decisions need independence. This article should not be used as basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News