Morgan Stanley Research Report Analysis: Samsung 2Q26 Profit Surges 18-Fold, Earnings Momentum Remains Strong

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: Samsung 2Q26 Profit Surges 18-Fold, Earnings Momentum Remains Strong

If 3Q guidance continues to exceed expectations, Samsung's valuation may undergo a round of systematic revaluation.

By: Rita

TechFlow Insight

Samsung Electronics released preliminary 2Q26 earnings on July 7: operating profit 89.4 trillion KRW (approx. 58.4 billion USD), up 1810% YoY, up 57% QoQ; revenue 171 trillion KRW, up 129% YoY, both exceeding market expectations. This figure surpassed Nvidia's 53.5 billion USD last quarter, making Samsung the company with the highest quarterly operating profit globally.

Morgan Stanley provided immediate analysis: in line with expectations, but earnings momentum remains strong. Memory business profit margin exceeded 70%, overall company operating profit margin reached 52%, still astonishing even after deducting approx. 10% employee bonus provision. Morgan Stanley maintains Overweight rating on Samsung, Top Pick, target price 381,000 KRW, current 318,000 KRW, implying approx. 20% upside.

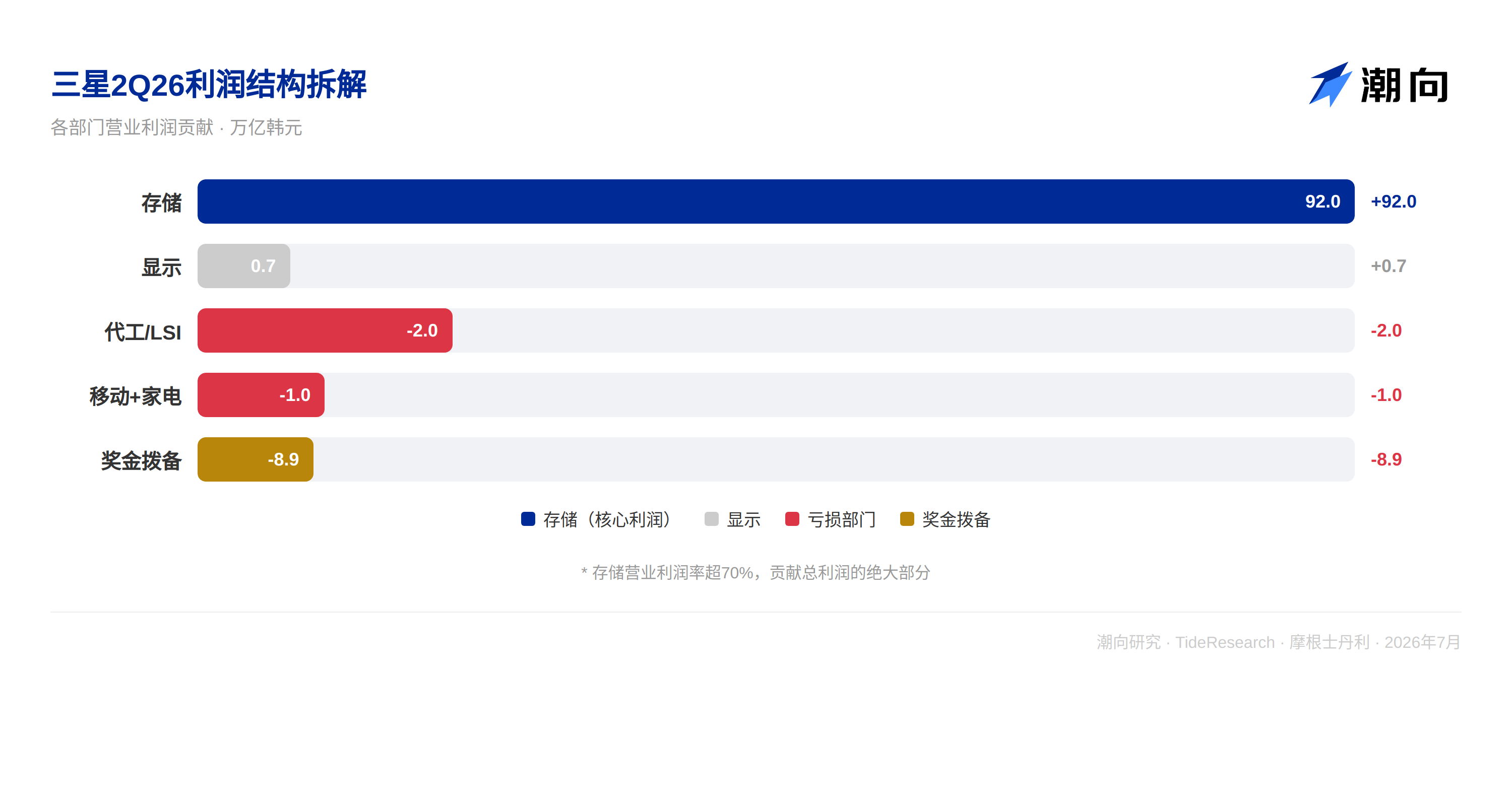

Memory is the sole protagonist, profit margin as high as over 70%

In Samsung's 2Q26 profit structure, memory is the absolute main force. Morgan Stanley estimates memory division operating profit close to 92 trillion KRW, accounting for the vast majority of total company profit. DRAM ASP rose approx. 56% QoQ, coupled with synchronized strength in NAND prices, storage business operating profit margin exceeded 70%.

Foundry and Logic System LSI (LSI) division losses narrowed to approx. 2 trillion KRW, Mobile and Home Appliances divisions combined losses approx. 1 trillion KRW, Display division contributed approx. 700 billion KRW profit. Except for memory, other business lines overall remain a drag.

Samsung Electronics' profit structure has completely become "storage dominating alone". 92 trillion memory profit corresponds to 89.4 trillion total profit, meaning all other businesses combined are loss-making. Foundry is losing, phones are losing, home appliances are losing, only the display division contributed meager profit of approx. 700 billion. Samsung has essentially become a storage company, other businesses are just dragging it down.

Bonus provision eats part of profit, but cannot hide real earnings momentum

There is an easily overlooked detail in the financial report data. In May this year, Samsung reached an agreement with employees, linking performance bonuses to operating profit, setting aside 10.5% of the semiconductor division's annual operating profit for special bonuses. Morgan Stanley estimates this provision accounts for approx. 10% of 2Q operating profit, approx. 8.9 trillion KRW.

Without this one-time provision, Samsung's operating profit would be close to 100 trillion KRW. The provision lowered the book figures, but real earnings momentum is stronger than the report shows. Morgan Stanley explicitly pointed out in the report that the operating profit margin is as high as 52% (memory business over 70%), this data was achieved after accruing huge bonus provisions. In other words, Samsung's real profitability is even fiercer than the report shows.

Employee bonus provision is an important variable in Samsung's profit structure. The higher the 2026 full-year operating profit, the larger the absolute amount of bonus provision, but the provision ratio is fixed at 10.5%. This means as profits continue to grow, provision amount will amplify synchronously, but will not change the direction of continuous profit expansion.

Morgan Stanley's full-year expectation: 412 trillion KRW, storage growth over 1100%

Morgan Stanley's core judgment on Samsung is: the earnings recovery cycle is far from over, the market may not have fully priced in the 2026 full-year earnings scale.

Morgan Stanley expects Samsung's 2026 full-year operating profit to reach 412 trillion KRW, storage business profit growth exceeding 1100%. If this number is realized, it means Samsung's 2026 profit will grow over 50 times compared to 2025. Samsung's 2025 full-year operating profit was only approx. 7.7 trillion KRW, while 2026 Q2 single quarter is already 89.4 trillion.

Morgan Stanley believes this is not impossible, because the current storage cycle is different from any previous one. AI data center demand for HBM and DDR5 is continuously squeezing traditional storage supply, while supply-side capacity expansion requires at least 2 to 3 years to release significantly. The duration of supply-demand mismatch far exceeds market expectations.

Focus on tracking two variables. The first is Long-Term Agreement (LTA). Storage manufacturers are signing more and more long-term agreements with customers, Morgan Stanley believes this will significantly enhance predictability and stability of Samsung's earnings, reducing market uncertainty pricing on cycle fluctuations. If LTA becomes industry norm, storage stock valuation method may need to switch from cyclical stocks to growth stocks.

The second is continuous demand for advanced storage from AI computing. Samsung's technology nodes at DRAM and logic substrate level are more advanced than competitors, "compute-power ratio" advantage is expanding. Against the background where AI computing power consumption is increasingly becoming a bottleneck, Samsung's advanced process advantage may translate into continuous pricing power premium.

TechFlow Perspective

Samsung stock price rose 165% within the year, already outperforming almost all peers, but Morgan Stanley is still calling Overweight. The core contradiction lies in: the market is pricing Samsung as a "cyclical stock", giving mid-cycle valuation, but Morgan Stanley believes the intensity and sustainability of this storage cycle far exceeds any previous one.

Morgan Stanley used a very straightforward comparison: Samsung's current stock price corresponds to 2026 P/E ratio of only 6.6 times, P/B ratio 3.2 times. If according to Morgan Stanley's full-year 412 trillion KRW profit expectation, implied P/E ratio is approx. 5.5 times. For a company with operating profit margin exceeding 50%, in oligopoly position in AI storage field, this valuation is obviously not expensive.

Verification point lies in the July 30 earnings conference call. Management's 3Q guidance given at that time will be more important than the preliminary earnings itself, what the market wants to know is not just "how much earned in the past", but "how long can it continue to earn in the future". If 3Q guidance continues to exceed expectations, Samsung's valuation may welcome a round of systemic revaluation.

Disclaimer

This article is TechFlow Research's organization and interpretation of third-party broker research report (Morgan Stanley, July 7, 2026). Ratings, target prices, earnings forecasts and related judgments cited in the text are all views of the broker's analysts, only represent their affiliated institution's stance, do not represent TechFlow Research's views, nor constitute any investment advice.

Market has risks, decisions need independence. This article should not be used as basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News