Morgan Stanley Research Report Analysis: Memory Cycle Approaching Peak, But 2027 Earnings Still Expected to Grow 35%-40%

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: Memory Cycle Approaching Peak, But 2027 Earnings Still Expected to Grow 35%-40%

Morgan Stanley suggests seeking opportunities in DRAM and traditional storage, while avoiding module manufacturers.

Written by: Rita

TechFlow Guide

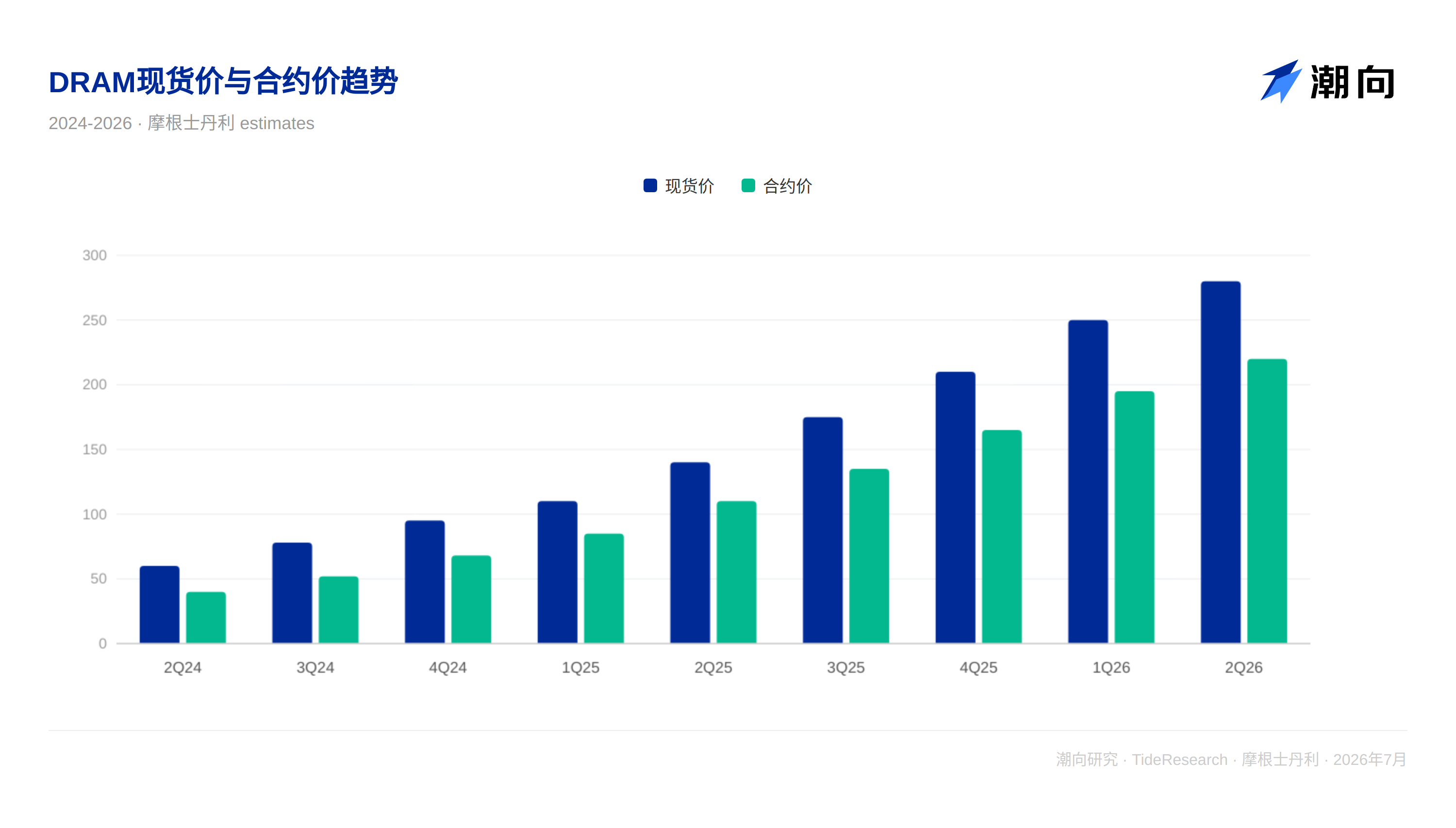

Morgan Stanley released its Asia-Pacific Memory Flash on July 6, giving clear judgments on the three most controversial memory issues currently: The largest AI spenders are rumored to have excess computing power available for sale, raising market concerns that the entire AI build-out is oversupplied; stock prices have failed to rise following the announcement of Long-Term Agreements (LTA); and whether the memory cycle has peaked.

Morgan Stanley's conclusion is clear: Memory is approaching peak rates of change across three dimensions: year-over-year prices, inventory, and breadth of earnings revisions. Short-term stock prices may face pressure, but this AI-driven memory bull market is far from over. Memory industry earnings in 2027 are still expected to grow by 35% to 40%, and the rise of AI Agents will continue to drive demand. Morgan Stanley suggests seeking opportunities in DRAM and traditional memory, while avoiding module manufacturers.

Controversy Over "Excess" Computing Power: Over-shipment or Positive Feedback on AI Construction?

Last week's hottest market topic was the rumor that a certain hyperscaler had excess computing power available for external sale. Morgan Stanley believes the market is doing what it always does: selling before the news comes out. The pessimistic interpretation is straightforward: if leading cloud providers have idle computing power, then the entire AI build-out is oversupplied.

But Morgan Stanley offers another interpretation: This恰恰 shows enterprises are smartly monetizing infrastructure and improving return on capital expenditure, which is different from "over-construction." The real moment that determines direction is the Q2 earnings season, specifically whether hyperscalers maintain or raise capital expenditure. If maintained, memory is a buy point; if lowered, the oversupply narrative will continue to ferment.

Another discussion focuses on the token economy. Morgan Stanley observes enterprises are shifting from "encouraging employees to generate as many tokens as possible" to "finding cheaper alternatives." Open-source models are rising rapidly in China, and enterprises are beginning to add an orchestration layer on top of frontier models: simple queries go through open-source, complex queries go through frontier models. This "token minimization" trend is changing market focus; investors are no longer just盯着 revenue growth, but are more concerned about what guidance will say.

Morgan Stanley's judgment is: Q2 AI supply chain performance is fine, but the market has shifted to worrying about second-half guidance, which significantly impacts memory. Memory is the most direct beneficiary of AI capital expenditure.

Why Didn't Stock Prices Rise After Long-Term Agreement Announcements?

Memory companies have consecutively announced Long-Term Agreements, but stock prices have not seen the revaluation the market expected. Morgan Stanley's explanation is straightforward: The market is rational. Investors have learned from the lesson during the pandemic where Long-Term Agreements for analog chips eventually became inventory burdens. Those agreements were either renegotiated, or customers were forced to accept unwanted inventory.

Morgan Stanley believes that this time the Long-Term Agreements are structurally stronger; as long as AI remains strong, the logic holds. But market skepticism is reasonable; they need to see actual execution, not just a piece of paper.

Morgan Stanley also admits the biggest obstacle is timeline uncertainty. How long and how much can memory prices rise, and where will 2028 Earnings Per Share actually end up? Market consensus on these issues determines the upper limit of stock prices. Among AI beneficiaries, the magnitude of earnings revisions for memory stocks is far ahead, but this point is already fully understood by the market.

Cycle Approaching Peak, But Far From Over

Morgan Stanley repeatedly emphasizes one judgment in the report: Memory is still a cyclical industry, just different this time, but the rate of price change is approaching its peak.

The report points out that since Generative AI emerged in November 2022, the memory industry has already experienced three cyclical corrections. Each correction was a necessary adjustment within a structural bull market; the start of a new bear market is not established. Sharp corrections triggered by crowded positions are actually healthy, clearing space for the next rise.

Morgan Stanley uses a very straightforward metaphor: Price momentum is beginning to fade, but that doesn't mean the cycle is over. Hyperscalers (the core drivers of AI spending) have recently underperformed, which may be a leading indicator that memory is about to enter a period of relative market underperformance. Meanwhile, the breadth of earnings revisions for memory stocks is approaching historical extremes, which is usually not a good signal.

Morgan Stanley's conclusion is: Positions need a correction. The decline in AI beneficiary stocks is not because valuations are too expensive, but because positions are too crowded. These stocks have risen a lot, and earnings revisions have confirmed these gains, but the breadth of revisions has reached extremes. The market needs to catch its breath, and volatility during earnings season may provide this opportunity.

Morgan Stanley remains bullish long-term, with 2027 earnings expected to grow by 35% to 40%; the rise of AI Agents is the next structural driver. But in the short term, the possibility of stock price pressure before earnings season is increasing.

Samsung and SK Hynix: Q2 Expectations Overview

Morgan Stanley provides Q2 outlooks for the two Korean memory leaders:

Samsung Electronics will release preliminary results on July 7. Morgan Stanley expects Q2 operating profit to be approximately 85 trillion Korean Won, basically consistent with market expectations. SK Hynix will release earnings on July 29. Morgan Stanley expects operating profit to be approximately 65 trillion Korean Won, in line with market expectations. Management guidance for both companies is expected to align with market expectations, with commodity memory continuing to strengthen in Q3, multiple Long-Term Agreement commitments materializing, and capital expenditure only modestly increased.

TechFlow Perspective

The most valuable point of this Morgan Stanley report is not the conclusion itself, but its admission of an easily overlooked fact: The magnitude of earnings revisions for memory stocks is far ahead among AI beneficiaries, but this is already information fully priced by the market, and stock prices may have already reflected too much good news.

The report's title is "Changing Tides." This metaphor is accurate: The tide is receding, but not ebbing, just changing direction. Morgan Stanley emphasizes that short-term stock prices may face pressure, but the long-term judgment of 35% to 40% earnings growth in 2027 remains unchanged. In other words, even if there is a short-term pullback, it is just a routine correction within a structural bull market, not the end of the cycle.

For investors focusing on memory, Morgan Stanley provides a clear framework: Crowded positions are a short-term problem, earnings growth is the long-term answer. The key lies in what hyperscalers will say during the Q2 earnings season; statements from memory companies themselves are not that important.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of third-party brokerage research reports. Ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, representing only the position of their affiliated institutions, not the position of TechFlow Research, nor do they constitute any investment advice.

The market carries risks; decisions must be made independently. This article should not serve as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News