VCs on 2025 Crypto Investment: 118 Tokens, 84% Underperforming at Launch—Only One Type of Company Is Quietly Profitable

TechFlow Selected TechFlow Selected

VCs on 2025 Crypto Investment: 118 Tokens, 84% Underperforming at Launch—Only One Type of Company Is Quietly Profitable

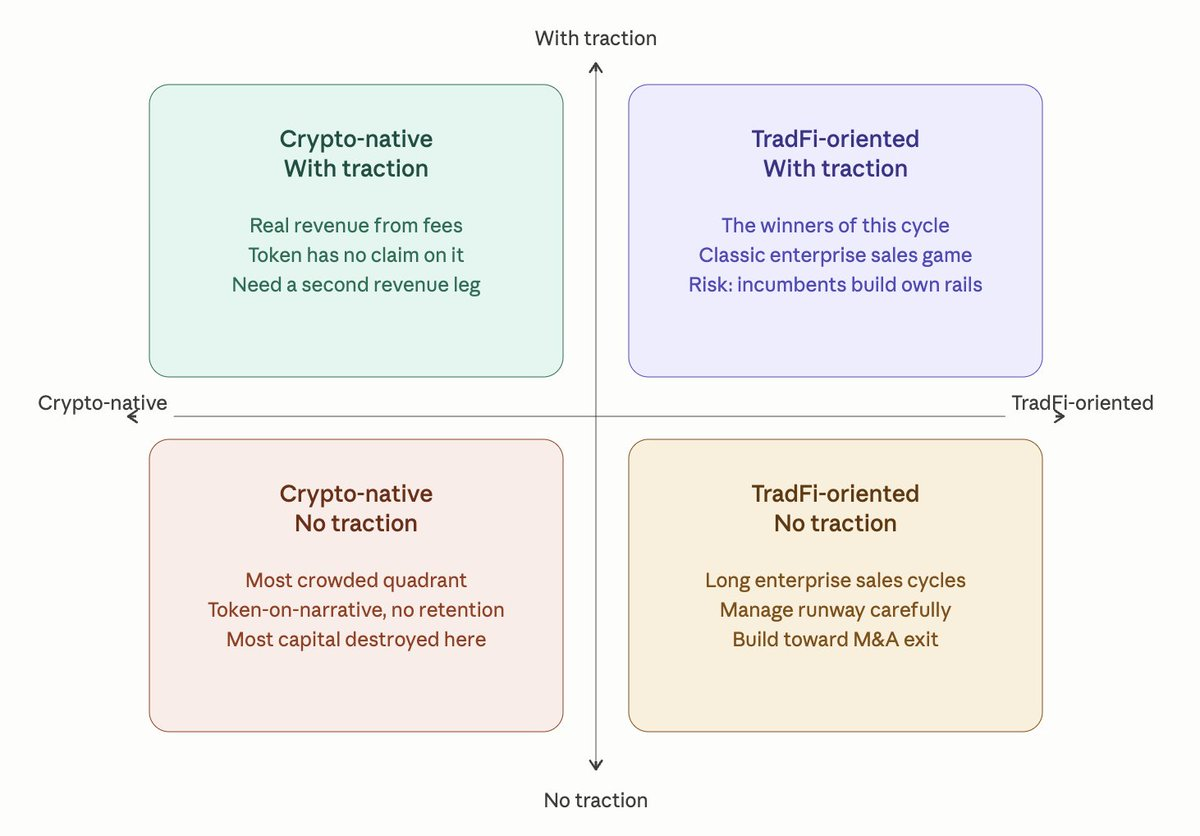

Crypto-native vs. traditional finance-oriented; traction-driven vs. tractionless. Four quadrants covering approximately 75% of the market.

Author: Ching Tseng

Translation & Editing: TechFlow

TechFlow Intro: Investor Ching Tseng categorizes crypto companies into four quadrants: crypto-native vs. traditional finance-oriented, and traction-positive vs. traction-negative. Of the 118 token launches tracked in 2025, 84.7% traded below their issue price. Crypto-native projects lacking traction are massively destroying capital, while traditional finance-oriented firms with traction are capturing the $18 billion RWA (real-world assets) market. This article clarifies where capital is flowing—and which tokenomics models have already failed.

This year, sitting on the investor side, I’ve found that nearly every crypto founder I meet falls cleanly into one of four categories. The two axes are simple: crypto-native vs. traditional finance-oriented, and traction-positive vs. traction-negative. These four quadrants collectively cover roughly 75% of the market.

The challenges each quadrant faces are fundamentally different. Below is my breakdown.

Crypto-Native, Traction-Negative

This is the most crowded quadrant—and the site of the most severe capital destruction.

These teams still showcase TVL figures inflated during the last cycle—but cannot explain why those numbers worked then. They seek valuations of $20 million, $30 million, or even $200 million, backed only by a utility token and a roadmap—claiming the token has a “clear use case” because it pays for fees or governs via voting.

The data is brutal. Of the 118 token launches tracked in 2025, 84.7% traded below their issue price, with median fully diluted valuations down 71%. Some of this cycle’s most hyped “native DeFi L1s,” after launch, saw TVL drop over 90% within the first year—mirroring near-identical token performance. AI-related tokens posted an average annual return of -50%; several top performers from 2024 have retraced over 80% from their peaks.

The pattern is consistent. Initial traction comes from users seeking quick profits—not genuine product affinity. Tokens priced purely on narrative, without revenue or user retention to support valuation, bled heavily in 2025. Massive token emissions revealed that onchain activity was largely mercenary in nature.

What this quadrant must internalize is this: long-term token value stems from a team’s ability to generate revenue and return capital to holders—not from artificial utility forcing users to spend it. Regulation still prevents anyone from openly stating “tokens are equity,” but empirically, that’s the only model proven to work. Everything else is, at best, cyclical trading.

If you’re here, the honest move isn’t launching another token. It’s returning to fundamentals: Who are your real users? What are they willing to pay for? And how do you capture a share of that value?

Crypto-Native, Traction-Positive

This quadrant is full of teams who built real things years ago—often during the last cycle—and have quietly generated solid revenue from trading, lending, or exchange fees. Teams are lean, cash flow covers salaries, and products work.

Sounds promising? Yet they face their own set of challenges.

Most launched tokens early—and now confront a structural problem: revenue exists, but the token holds no mechanistic claim on it. Some of the largest products in the market process tens of millions—or even hundreds of millions—of dollars in monthly trading volume, yet their tokens have captured zero direct value for years. Regardless of how strong their revenue or profit is, markets don’t consistently trade tokens at multiples tied to current economics; instead, pricing reflects growth expectations—not present fundamentals.

The buyback debate forms the second half of this quadrant’s story. Protocols that pledged weekly fee-funded buybacks early in 2025 saw prices surge over 40% in the following month. Others running automated, fee-funded buyback programs repurchased over $1 billion in tokens across seven months—with single-day buybacks peaking near $4 million. Total DeFi buybacks in 2024–2025 reached approximately $2 billion.

Buybacks sound like the answer—and sometimes they are. But for teams in this quadrant with no overflow revenue, buying back tokens is simply burning future runway to defend a price that may ultimately be indefensible. The harder—and more valuable—question is whether you can grow a second revenue stream decoupled from crypto volatility. Because if traditional finance-oriented competitors build superior distribution into institutions while you still rely on memecoin traders, your moat will rapidly erode into infrastructure-level commodity pricing.

Traditional Finance-Oriented, Traction-Negative

This group ballooned in 2024–2025. Custodial tools, compliance middleware, tokenization rails, onchain FX, institutional settlement—all genuinely useful. All expensive. All subject to enterprise sales cycles measured in quarters—not weeks.

The problem isn’t the product. It’s the math. Founders raised $15–30 million assuming institutional demand would materialize—but even onboarding a single Tier-1 bank customer can take 12–18 months and require extensive compliance infrastructure, consuming a full year of runway before the first dollar of revenue arrives.

The good news is that the exit environment for this quadrant is exceptionally healthy. Crypto M&A hit a record $8.6 billion in 2025, with over 140 VC-backed crypto companies acquired—a 59% YoY increase. Some of the largest deals involved established giants paying hundreds of millions—or even billions—of dollars for distribution, licenses, and enterprise relationships in derivatives, trading infrastructure, and payment rails.

If you’re in this quadrant, the disciplined approach is to manage valuation and cash runway as if your life depends on it—pursuing meaningful M&A outcomes, because those outcomes truly matter. Don’t price yourself out of the acquirer pool. Don’t burn 24 months of runway chasing a single enterprise logo. Instead, build complementary partnerships with larger players who may eventually want to acquire you.

Traditional Finance-Oriented, Traction-Positive

The current winners of the system.

Tokenized real-world assets grew from $5.5 billion at the start of 2025 to $18.6 billion by year-end—a 3.4x increase in twelve months. The largest tokenization platforms now handle billions in institutional liquidity; market leaders hold ~20% share and power one of the world’s largest tokenized Treasury funds—with AUM nearing $3 billion.

These companies don’t try to convince anyone that crypto is the future. Their institutional clients have already decided. Today’s game is straightforward enterprise sales: winning more banks, more asset managers, more issuers; building alliance structures so that when an institution buys one of your products, it naturally adopts three more from your partners; and tightening unit economics atop the compliant, custodial stack you’ve already built.

If the team operates purely as a service provider, this becomes a classic enterprise software war: sales velocity, net retention, integration depth.

The primary risk for this quadrant doesn’t come from crypto-native competitors—it comes from incumbents: large asset managers and global banks who may ultimately build their own rails and bypass startups helping them adapt to onchain infrastructure. That window is real—but it’s not infinite.

On the surface, the four quadrants look distinct—but all are navigating the same underlying shift: the market is maturing.

This doesn’t mean narratives are dead. Institutions chase thematic trends too—anyone who’s watched semiconductor and AI valuations over the past two years knows that. But in mature markets, narrative half-lives shorten dramatically. It can still get you started—but it won’t sustain you.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News