SEC Regulation Intervenes: How Can Web3 Games Dance on the Edge of a Blade?

TechFlow Selected TechFlow Selected

SEC Regulation Intervenes: How Can Web3 Games Dance on the Edge of a Blade?

This article starts from the entry point of web3 gaming and discusses key considerations under the U.S. regulatory framework regarding product design, business model development, operations, and distribution.

Author: Simon @IOSG Ventures

Since the inception of the industry, video games have always been high-risk and high-reward. The global gaming market has reached $350 billion and continues to grow rapidly, attracting countless entrepreneurs. In traditional gaming, from minors' addiction prevention to gambling classification, the dynamic interplay and mutual adaptation between the industry and regulation have always underpinned its development.

For web3 games, the addition of more financial elements and SEC oversight means founders face even more complex challenges—requiring significantly greater effort in navigating regulatory landscapes.

This article explores key considerations under the U.S. regulatory framework for web3 games—from product design, business model construction, operations, and distribution:

The following is not financial or investment advice, but recommended topics for founders and teams to discuss and research.

What are Securities & Why Do They Matter?

Compared to other products, game development is costly. In traditional gaming, common funding methods include financing through publishers, selling equity to VCs, or raising from angel investors. Web3 opens new avenues beyond crowdfunding platforms—enabling developers to raise directly from the public by selling tokens/NFTs.

These new fundraising models offer opportunities for small and mid-sized developers, but also introduce fresh complications—such as many early crowdfunding and publishing platforms avoiding digital assets altogether, uncertainty around securities classifications for tokens, and resulting hesitancy among traditional game investors toward web3 games.

The Howey Test

If a game’s token is classified as a security, it falls under SEC jurisdiction. Who can buy these tokens and how many they can purchase become strictly regulated. Most critically, such tokens cannot be listed on compliant centralized exchanges in the U.S. To understand this classification, we must examine the Howey Test.

The Howey Test is used by the SEC to determine whether a cryptocurrency qualifies as a security. Regulators assess three aspects: investment of money, participation in a common enterprise, and expectation of profit. In practice, projects are scored across criteria—the higher the score, the more likely the token is deemed a security. Once classified as such, tokens face stringent regulations similar to traditional securities, with much higher issuance barriers. Issuers lacking proper qualifications may face severe legal consequences.

Most blockchain projects—including Ethereum—actively work to minimize their scores on the Howey Test, aiming to avoid having their issued cryptocurrencies classified as securities.

The Howey Test evaluates four main factors:

(1) Investment of money;

(2) Investment in a common enterprise;

(3) Expectation of profit;

(4) Profit derived solely from the efforts of the promoter or third parties (not direct involvement).

Note that the Howey Test itself isn’t formally codified in law—it serves as a judicial guideline. When blockchain projects claim to “pass” the Howey Test, they usually mean their tokens score low enough to avoid being considered securities and comply with U.S. laws. Ultimately, such claims typically stem from legal opinions provided by law firms—not official recognition by U.S. courts.

Game projects often attempt compliance via structuring separate entities—for example, offshore token-issuing and operational entities (marketing, R&D, operations). However, independent legal entities do not fully eliminate regulatory risk. In practice, the SEC examines all active participants involved in a token offering, including affiliated third parties. Merely separating issuing and operating entities does not exempt a project from SEC oversight. Since such tactics are ineffective, let's directly address potential risks through the lens of the Howey Test.

#1: An Investment of Money

This is the easiest criterion to satisfy. Selling in-game currency, assets, or content—or even distributing them via airdrops/gifts—can qualify if the project benefits directly or indirectly (e.g., requiring users to follow the game’s Twitter account in exchange for a discount code). Any form of value exchange meets the “investment of money” requirement.

#2: In a Common Enterprise

A “common enterprise” implies aligned interests among participants, which manifests in two ways:

1. Horizontal alignment – shared investor interests

2. Vertical alignment – shared interests between investors and issuers

1. Horizontal Alignment Among Investors

This typically requires pooling investments where gains and losses are shared. Some argue that NFTs in games are unique, individually owned assets—so different investors’ outcomes (e.g., owning different STEPNS shoes) are independent. But in the Dapper Labs case, regulators noted that NBA Top Shot NFTs were grouped into collections used to attract attention and buyers. When floor prices rise, all holders benefit collectively—and vice versa. Thus, the argument that NFT investors lack shared interests fails.

2. Vertical Alignment Between Investors and Developers

In web3 games, investors and developers often share aligned incentives. After purchasing NFTs, both parties continue benefiting. Most NFT issuers earn royalties from secondary sales. As NFT prices increase, so does issuer revenue—sometimes exceeding primary sale income. Many games operate proprietary marketplaces taking trading fees. In the NBA Top Shot example, Dapper Labs earns both royalties and marketplace fees—any price increase directly benefits the company.

Game developers and NFT issuers continuously benefit from asset sales and issuance.

#3: With the Expectation of Profit

This factor is more ambiguous: do players expect profits when buying assets? Did the team explicitly design yield mechanisms? Regulators evaluate product design, marketing materials, user profiles, purchase motivations, and cost inputs. Marketing emphasizing “play-to-earn,” “P2E,” or “future dividends” raises red flags. Additionally, buyer profiles and purchase volumes matter—abnormal patterns draw scrutiny.

“Wait—you mean someone spent $1 million buying 80% of your skins and isn’t even playing your game?” That’s suspicious. In the Telegram case, many Gram Token holders weren’t actual users (though defining this remains fuzzy), but VCs and speculators.

Notably:

1) Price appreciation alone doesn’t constitute “expectation of profit.” For instance, CS:GO skin prices have skyrocketed, but owning one doesn’t entitle you to dividends. Profits from reselling on secondary markets don’t count as expected profit under Howey.

2) If users profit through their own efforts, it helps avoid this criterion. For example, Xiao Hong renting her STEPNS shoe to Xiao Ming off-platform isn’t due to project-designed yields.

NFT royalties, marketplace fees, revenue sharing, and NFT staking are standard tools to attract web3 users. Yet many projects overtly emphasize these during fundraising—essentially waving a sign at regulators saying, “We’re issuing securities.”

#4: From the Efforts of Others

Finally, regulators assess how reliant buyers are on the issuer’s efforts to profit. The more an NFT’s value depends on the team’s execution or the game’s success/failure, the more it resembles a security. In gaming contexts, this point cuts deep.

Beyond typical token reliance on issuers, in-game item values heavily depend on utility provided by the game. Often, when tokens are issued, the game isn’t even completed or launched—meaning 90% of the asset’s value hinges on the team, not individual user effort.

From here, some countermeasures come to mind:

– Requiring more user effort before earning profits: e.g., staking, completing in-game tasks or progression milestones.

– Delaying token issuance until the game matures.

– Expanding asset utility beyond one game—usable across multiple titles—to reduce dependence on a single issuer.

Side note: Fully on-chain, sufficiently decentralized games may also serve as a solution.

Still, developers needn’t panic. Howey Test outcomes are case-specific—meaning a ruling on one token issuance doesn’t automatically apply to others. Even if $GMT were ruled a security tomorrow, it wouldn’t imply all dual-token governance tokens are securities.

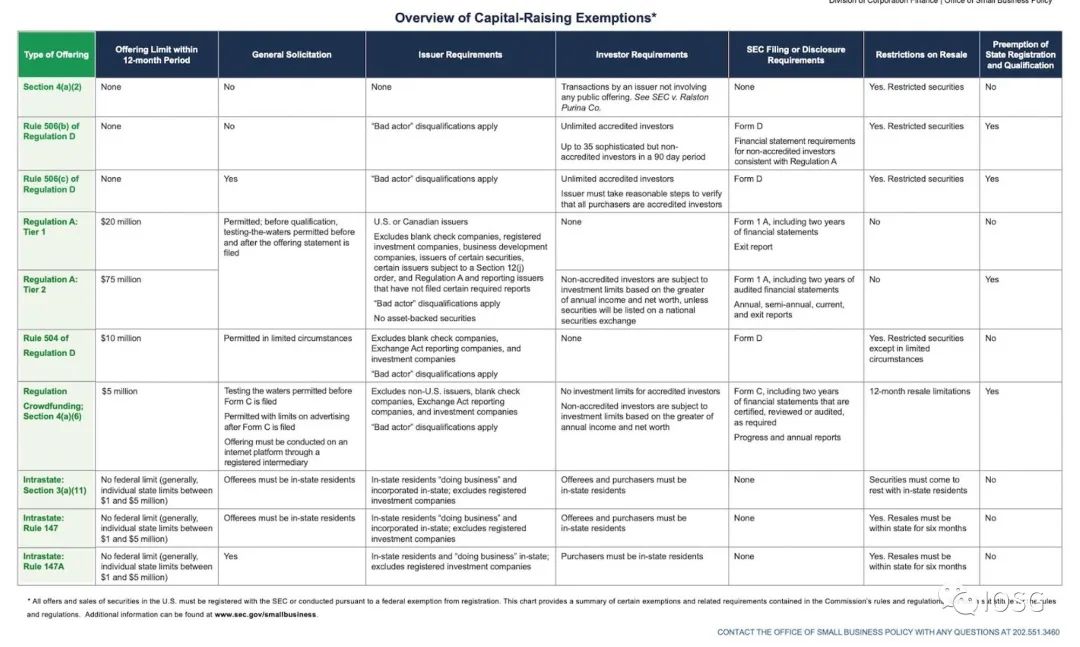

“Designing compliant token models from day one” and “avoiding issuance of potentially securities-like tokens” offer extremely high ROI for issuers. Alternatively, choosing safer fundraising paths means designing offerings according to SEC guidelines—detailing how many times a company can issue securities, fundraising caps, eligible buyers, disclosure obligations, and investor protections.

Source: www.sec.gov/education/smallbusiness/exemptofferings/exemptofferingschart

Dancing on the Edge: Pitfalls to Avoid When Designing Tokenomics

Fungible Tokens (FT)

Let’s briefly review common FT designs in the industry: web3 games typically use single-token or dual-token models.

In a single-token model, one token serves both governance and in-game utility functions.

In a dual-token model, these roles are split: governance tokens usually have fixed supplies and theoretically allow holders influence over development/operations; utility tokens typically have uncapped supplies and function as in-game currencies.

Before defaulting to a dual-token model and deciding supply parameters, developers should carefully consider each token/NFT’s actual functions and how value capture and distribution will work.

Designing token economics purely for ease of management exposes projects to greater regulatory risk.

Teams should reevaluate, among other things:

– Is each token truly necessary?

– Are token buyers actual consumers or real players?

– Though issued by the same entity, utility and governance tokens often yield very different Howey Test results. If core game design avoids regulatory sensitivities—and the game can function without dual tokens or any token issuance—why add unnecessary risk?

Governance tokens are often sold to retail investors via private sales or IEOs, while utility tokens are earned by players completing in-game tasks. Under the Howey Test, utility tokens generally appear less like securities in terms of issuance method and holder profile. But can we simply label a token “utility” and call it safe?

Unfortunately, to manage economic lifecycle and prevent gold farmers from devaluing utility tokens, developers often intervene post-launch—adjusting gameplay mechanics, altering token emission/burn rates to stabilize prices. This again triggers the final Howey criterion: reliance on “the efforts of others.”

Mere imitation of past token models is insufficient under current regulatory pressure.

Non-Fungible Tokens (NFT)

NFTs are widely used in web3 games—from characters and skins to land and buildings mimicking real-world assets. On the surface, these digital items seem far removed from securities. As previously analyzed, non-fungibility gives NFTs some resilience under the Howey Test. However, caution is still warranted: for certain series, individual NFTs remain highly fungible—such as repetitive in-game materials (Mahjong tiles, poker cards)—which regulators might view as part of a “common enterprise.” Moreover, with NFTFi advancements like fractionalization, NFTs increasingly exhibit fungible traits, enhancing their securities-like characteristics.

Another notable trend: in first-gen GameFi, many games used NFTs as entry barriers or “gold-mining tools”—requiring users to purchase Axies or running shoes (i.e., make upfront investments) to play.

Such upfront costs amplify the investment nature of NFT purchases, making “expectation of profit” more pronounced. Instead of using NFTs as paywalls, adopting free-to-play or free-mint models—as LimitBreak does—is preferable.

Another viable design: giving in-game NFTs limited lifespans—depreciating in value over time or usage, or periodically resetting the game economy. For example, Battlestate Games resets the economy in Escape from Tarkov; in Zelda, most weapons degrade with use. Such designs help reduce players’ expectations of profit.

Extended Discussion

SAFTs

SAFTs (Simple Agreements for Future Tokens) are a common fundraising mechanism, including in gaming projects. When viewed alongside the Howey Test, SAFTs become legally ambiguous.

Theoretically, SAFTs split token purchase into two steps: investors first receive a contract to buy tokens in the future, then obtain the actual tokens after TGE. At first glance, this could suggest the token itself isn’t a security.

However, in practice—using the Telegram case as precedent—courts consider the Howey Test applicable at the time of SAFT signing, not TGE. All agreements related to token issuance are subject to scrutiny.

Using Existing Publicly Issued Tokens

The Securities Act of 1933 and Securities Exchange Act of 1934 apply to companies with over $10M in assets and 500+ shareholders. Could a web3 game company adopt a token issued by a private entity that doesn’t meet these thresholds—thereby avoiding being a securities issuer?

Perhaps—but this comes at a cost: trusting a third party’s compliance and relinquishing part of value capture. Therefore, thorough due diligence on the token issuer is strongly advised.

Insights

1) Game teams must take regulatory risks seriously—engaging with regulators will be the new normal. As consumer-facing products with large user bases, games will inevitably sit at the epicenter of scrutiny. Build flexibility into product design from day one, rather than issuing tokens merely for the sake of it.

2) Focus on decentralizing your project’s economic system and operations. This isn’t just marketing fluff or community storytelling—it’s a crucial safety net when facing regulators.

3) From nearly every angle, GameFi currently appears high-risk. While it may represent a proven model, it’s ill-suited for today’s environment. If possible, even if harder, pursue more meaningful innovation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News