Interpreting the Chainalysis Report: How Retail Investors, Seasoned Traders, and Institutions Contribute Value to Exchanges?

TechFlow Selected TechFlow Selected

Interpreting the Chainalysis Report: How Retail Investors, Seasoned Traders, and Institutions Contribute Value to Exchanges?

This report provides in-depth data analysis and unique insights, revealing behavioral patterns of all exchange-related users and demonstrating how they influence the development of the entire cryptocurrency market.

Introduction:

The cryptocurrency market is becoming increasingly complex.

Retail investors, whales, institutions, and exchanges—different roles exhibit distinct trading behaviors, and identifying and understanding these behaviors is more important than ever.

This report from Chainalysis provides in-depth data analysis and unique insights, revealing behavioral patterns of all users related to exchanges and demonstrating how they influence the broader development of the crypto market.

The report dives into multiple dimensions including wallet types, activity levels, total value flowing into and out of exchanges, and user churn rates. Using the once-dominant FTX as a case study, it breaks down various user groups that sent funds to FTX and analyzes their behavior in depth.

These data help us understand the value contribution of different user segments to exchanges, along with their activity and churn rates. If you're an operator at an institution or exchange, this report will help you better understand your users and optimize operational strategies. If you're a crypto investor, it will enhance your understanding of market dynamics and support smarter investment decisions.

Key Data Summary:

-

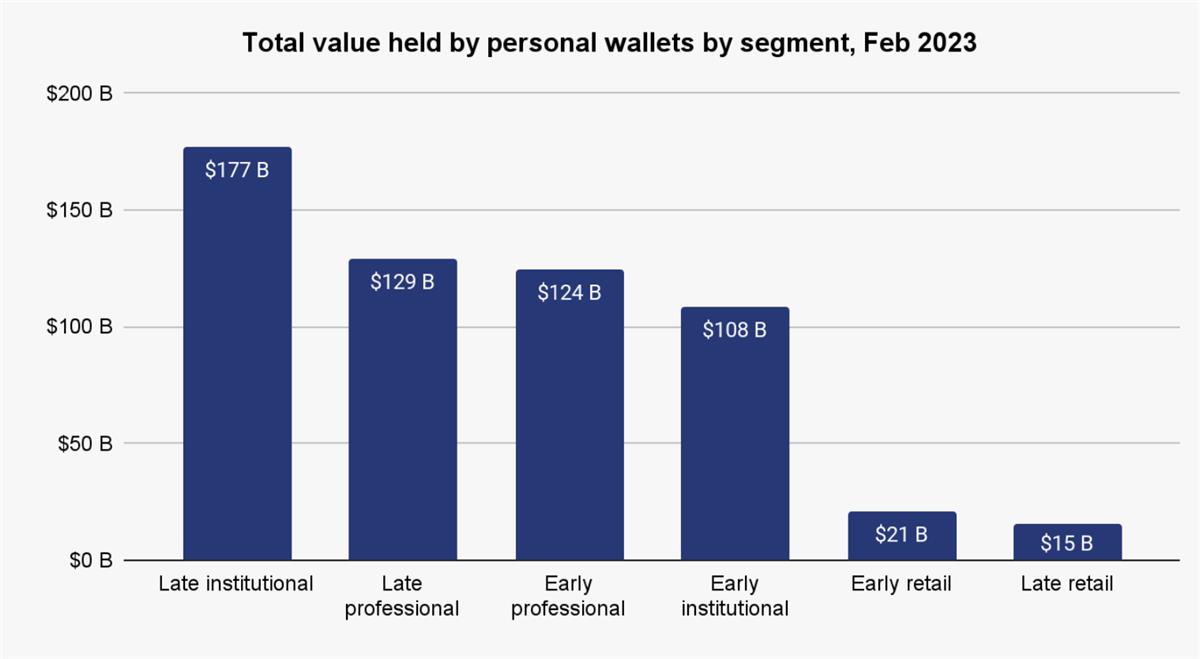

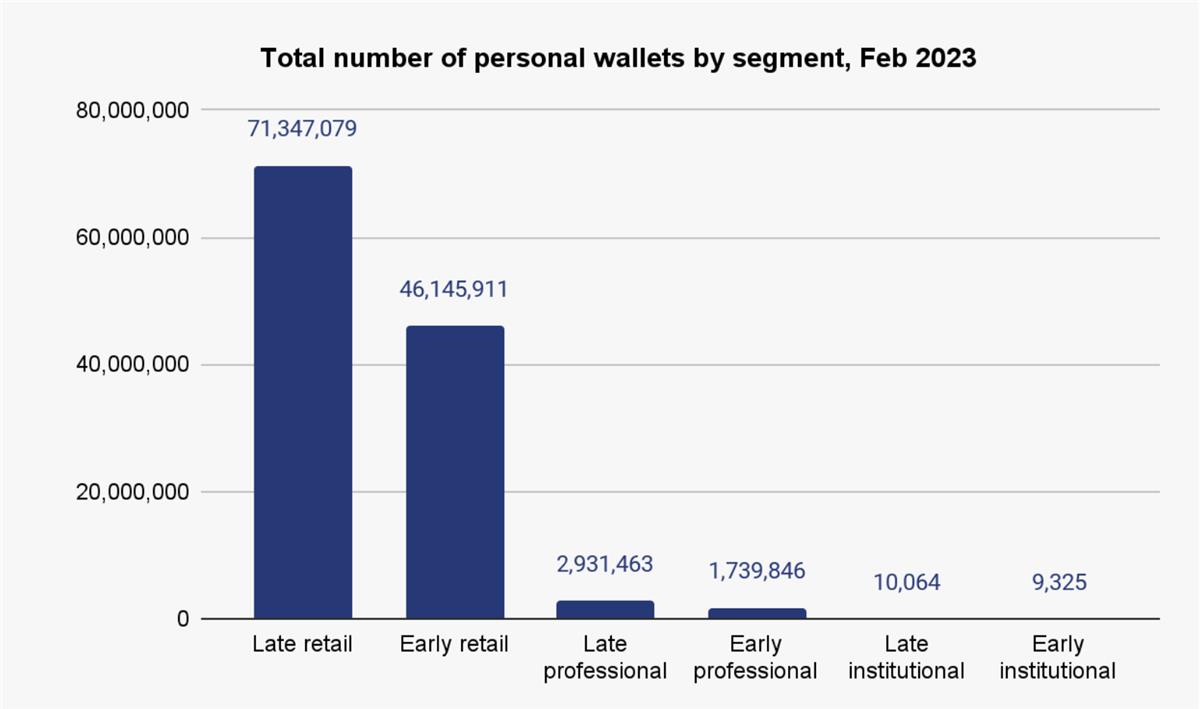

User Segmentation: Based on wallet age and asset holdings, users are categorized into six groups: early retail, early professional, early institutional, late retail, late professional, and late institutional. While retail (individual) users number in the hundreds of millions, their combined assets are dwarfed by institutional holdings.

-

Funds Flowing into CEXs: Late institutional wallets contributed the highest share of total value sent to centralized exchanges (CEXs), at 23.6%, followed closely by late professional and early retail wallets at 18.8% and 19.0%, respectively.

-

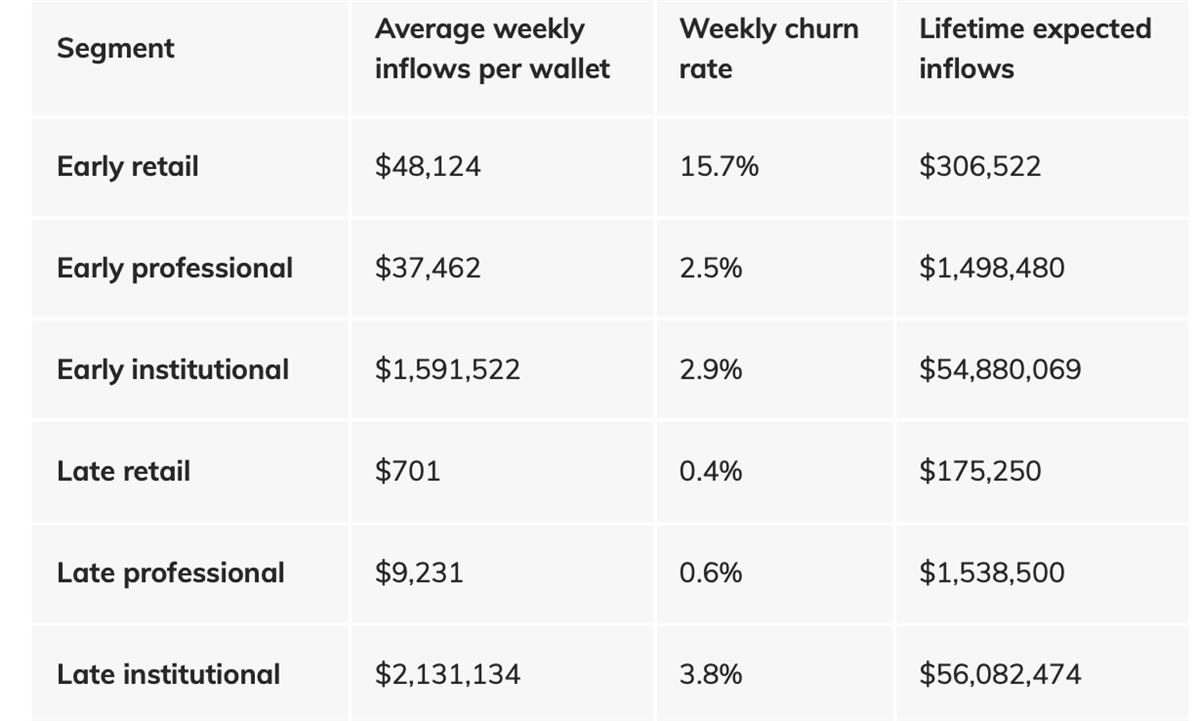

Funds Flow in FTX: Retail users made up most of FTX’s user base, but their average weekly inflow was only $700. In contrast, institutional users were few in number but contributed an average of $2 million per week.

-

User Churn Rate: Late professional and late retail wallets had low churn rates, below 1%; retail users, however, had a high churn rate of up to 15%.

Overall Market Situation

In 2023, the cryptocurrency market rebounded, with Bitcoin rising over 50%. However, exchanges faced challenges: the number of active centralized exchanges dropped from 750 at the beginning of 2022 to 640. With intensifying competition from decentralized exchanges (DEXs), CEX trading volumes declined further.

Despite this, the number of cryptocurrency users continues to grow. Looking at the count of individual wallets (i.e., non-custodial wallets) across all blockchains supported by Chainalysis that were active or held balances over the past five years, the upward trend in user growth is clear.

TechFlow Note: The chart below shows that the number of active individual wallets has grown from around 50 million in 2018 to over 300 million today. However, the original report does not disclose how these addresses were calculated, such as whether deduplication was applied.

When comparing the weakening position of CEXs against the steadily growing number of addresses, it becomes evident that exchanges must better segment their users and focus on attracting and retaining those who bring the greatest business value.

User Segmentation

Based on all available wallets, this report classifies users into six categories according to wallet age and asset holdings: early retail, early professional, early institutional, late retail, late professional, and late institutional.

TechFlow Note: Retail refers to individual investors (commonly known as "retail traders"). Professional users can be understood as whales.

Using this segmentation, the report aggregates the amount of assets held in Bitcoin and Ethereum networks across these six wallet types, yielding the following results:

As expected, retail wallets vastly outnumber institutional ones, yet their combined assets are far smaller.

Additionally, most currently active weekly wallets belong to the late retail category—these are newly created wallets with low balances. The number of active late professional wallets also exceeds that of early retail wallets, indicating that larger capital investments have entered the crypto space in recent years.

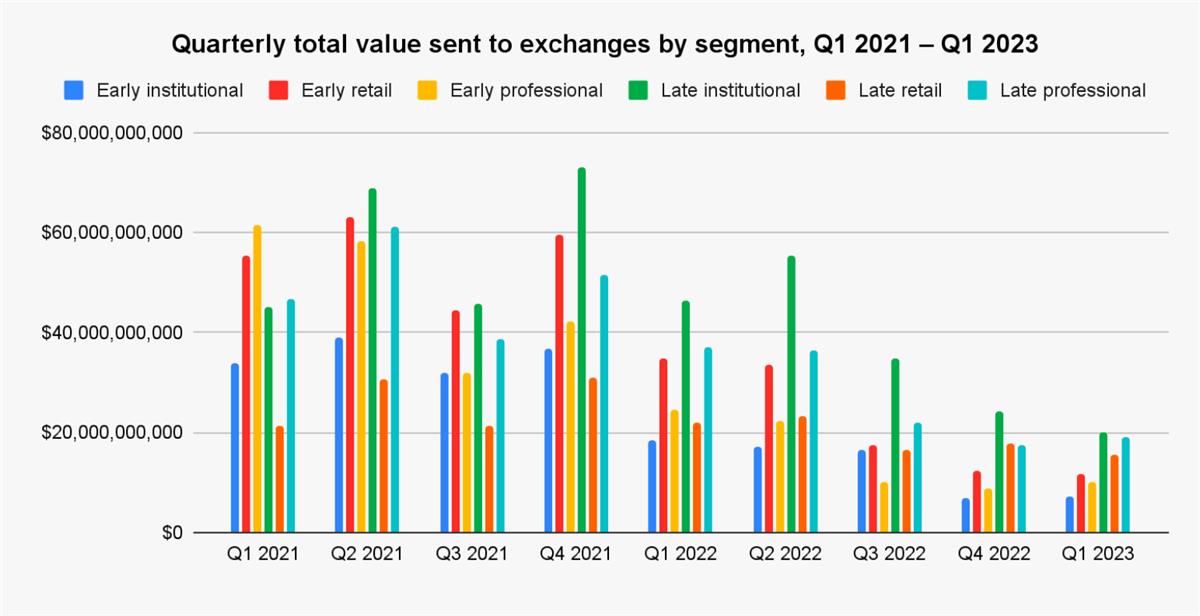

User Fund Flows in CEXs

Overall, relatively new late institutional and late large-holder wallets hold the majority of current Bitcoin and Ethereum assets in personal wallets. But for this study, the more critical question is: how do these groups interact with exchanges?

Centralized exchanges typically profit from trading fees. While we lack the order book data needed to calculate exact fee contributions from each group—we only have on-chain data.

However, we can reasonably assume that the total value each group sends on-chain to exchanges roughly correlates with the fees they generate. Cryptocurrencies are usually transferred from personal wallets to exchanges for trading rather than holding, making this assumption plausible.

Following this logic, since early 2021, late institutional wallets have contributed the largest share of total value sent to centralized exchanges, at 23.6%. Late professional and early retail wallets follow closely, accounting for 18.8% and 19.0%, respectively.

Across most quarters, the value sent by each group remains relatively balanced, except for late retail and early institutional wallets, which contributed only 11.4% and 11.9% of total inflows during this period.

The reasons for this lag differ: late retail wallets hold the least capital compared to other groups, while early institutional wallets represent the smallest share of all active wallets.

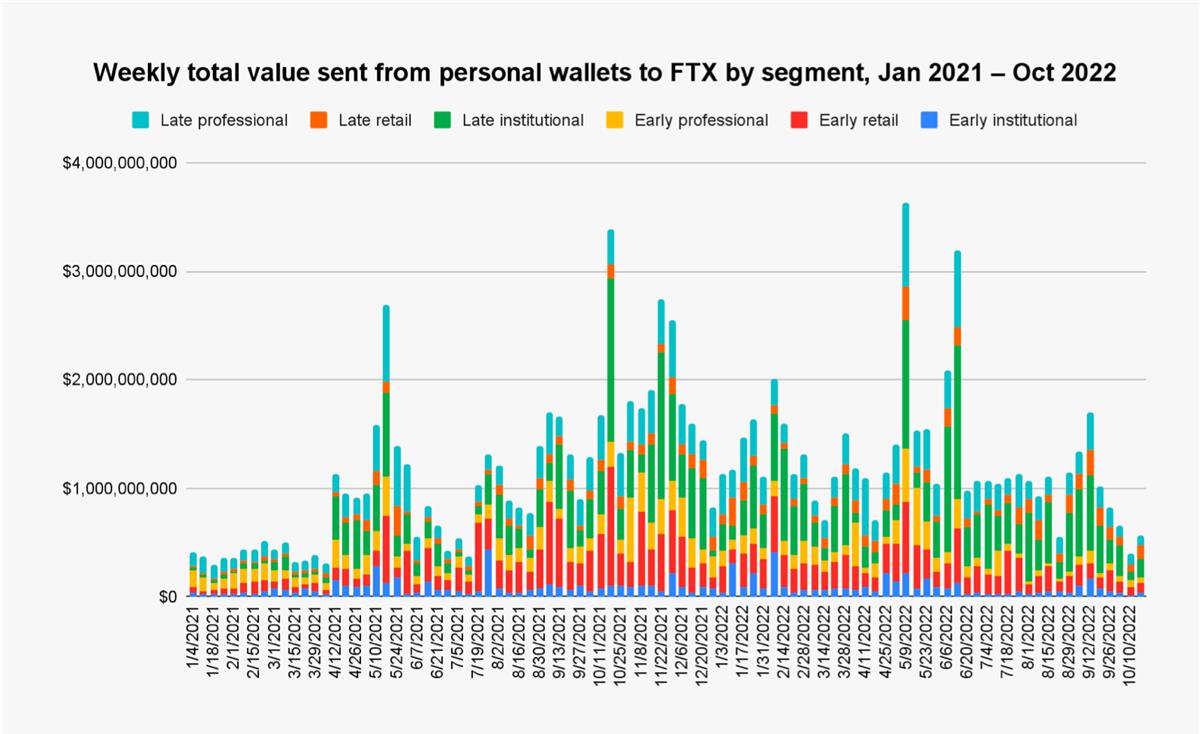

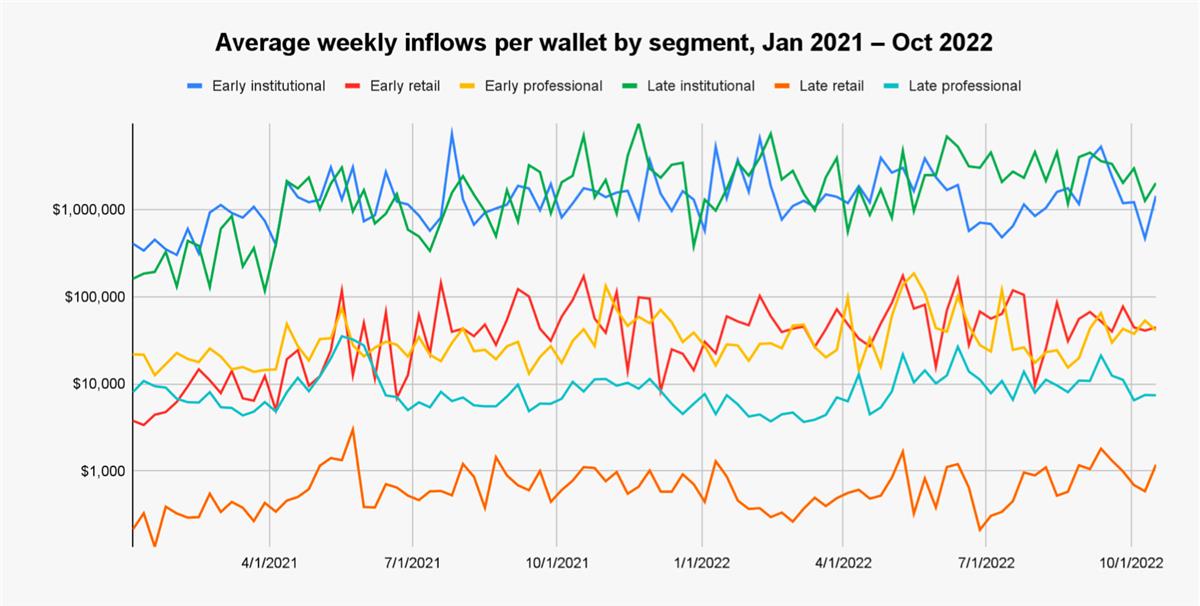

Case Study: User Fund Flows in FTX

Take FTX as an example. Despite its collapse in November 2022, it was one of the industry's most popular exchanges prior to that. Interestingly, FTX’s user base did not fully align with the overall wallet distribution described earlier.

In absolute numbers, late retail wallets constituted the vast majority of FTX’s user base, with late professional wallets consistently ranking as the second-largest group each week.

This suggests that, numerically, most funds sent to FTX came from retail users.

Meanwhile, late institutional and early institutional groups—the smallest but wealthiest segments—made up the tiniest portion of FTX’s user base. Yet, when assessing inflow volume, the picture changes dramatically:

-

Late institutional wallets dominated total inflows to FTX;

-

Despite making up only 0.1% of the average weekly user base, late institutional wallets accounted for 30.0% of total inflows during the study period;

-

Late professional wallets ranked second, contributing 21.4% of the value received by FTX—a figure more aligned with their 17.6% share of total users;

-

Late retail wallets contributed only 7.6% of total inflows despite representing 75.8% of weekly users.

At the beginning of the period—from January 2021 to mid-April 2021—late institutional wallets often had the lowest inflow share. It wasn’t until autumn 2021 that they firmly became the largest contributor group. This pattern may reflect increased institutional participation during the 2021 price rally—but it could also indicate FTX’s targeted efforts to attract high-value users.

If we rank the six user types by their value contribution to exchanges, institutions clearly sit in the top tier, with significantly higher total inflows than retail users.

The data show that despite fewer users, late institutional and late professional wallets contribute disproportionately high value to exchanges.

Churn rate is another key metric for evaluating user value. We found that early retail wallets have a much higher churn rate than any other group—at 15.7% per week—while late professional and late retail wallets have the lowest churn rates, at 0.6% and 0.4% respectively.

Moreover, considering the total funds a wallet sends to exchanges over its entire lifecycle allows for a better estimation of the expected value an exchange can derive from a user.

In this report, expected lifetime inflow = average weekly inflow / average weekly churn rate.

By this calculation, institutions are expected to contribute greater value to exchanges (due to low churn and consistent weekly inflows).

Conclusion

These insights are highly valuable for exchange user acquisition and retention strategies, as well as product development.

For example, FTX might aim to acquire new users by airdropping rewards to individual wallets active on other exchanges. By segmenting target wallets into these categories, FTX could precisely tailor reward amounts based on each wallet’s expected lifetime inflow value.

Similarly, if FTX wanted to improve retention among regular users, it might conclude that focusing on the early retail segment would yield outsized returns—even a small reduction in their high churn rate, given their substantial average weekly inflows, could significantly boost long-term value. Regardless of specific circumstances, the ability to assign value to each wallet enables FTX to market more effectively to both existing and potential users than through traditional methods.

At the same time, we believe this report sheds light on the overall structure of the crypto trading ecosystem. Retail traders contribute small volumes but in large numbers, with high churn; large players are the opposite. For individuals, gaining a deeper understanding of different counterparties’ characteristics and behaviors brings greater composure in the volatile world of crypto.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News