A Brief Analysis of CRV's Short-Selling History and Current Potential Shorting Costs

TechFlow Selected TechFlow Selected

A Brief Analysis of CRV's Short-Selling History and Current Potential Shorting Costs

How did the CRV long-short battle take place last year?

Author: Yilan

Recently, the Curve founder's token-selling behavior and continuous collateralization of CRV to borrow stablecoins have become focal points amid market liquidity concerns triggered by SEC-related events. To analyze the on-chain shorting cost, feasibility, and related implications for CRV, it is useful to revisit last year’s CRV long-short battle and examine how previous shorting operations were conducted.

Shortly after the FTX collapse, when market confidence was low and liquidity severely contracted, a whale borrowed a large amount of CRV tokens from Aave and transferred them to OKX exchange, accumulating a total of 47 million CRV. Affected by this massive sell-off, CRV's price dropped from $0.545 to $0.424—a decline of 21.88%—hitting a low of $0.40. This maneuver exemplified a strategy of repeatedly borrowing and transferring tokens on-chain to facilitate large-scale shorting by depressing the token price.

Subsequently, founder Michael purchased CRV to prop up the price. Although the Aave account faced liquidation risks, the short position still held profit potential. One way to profit was through high-leverage short trades on centralized exchanges like OKX, taking advantage of thin market liquidity and the absence of strong bullish resistance to achieve high-probability gains. Another method involved flipping the short position into a long one—when market liquidity was exhausted, shorts could cover their positions and go long instead.

Following the CRV long-short conflict, Aave removed CRV as a borrowable asset (i.e., preventing the same kind of leveraged looping via on-chain lending).

Additionally, centralized exchanges continue to offer opportunities for borrowing and shorting tokens.

Currently, the distribution of CRV holdings is as follows: 116 million CRV held within Curve DEX, 65.47 million on Binance, 12.56 million on OKX, and a combined 53.29 million across other centralized exchanges.

It is evident that centralized exchanges hold a significant amount of CRV, accounting for approximately 15% of the circulating supply. However, due to the lack of transparent data from centralized platforms, calculating the actual cost or scale of potential shorting activities remains challenging.

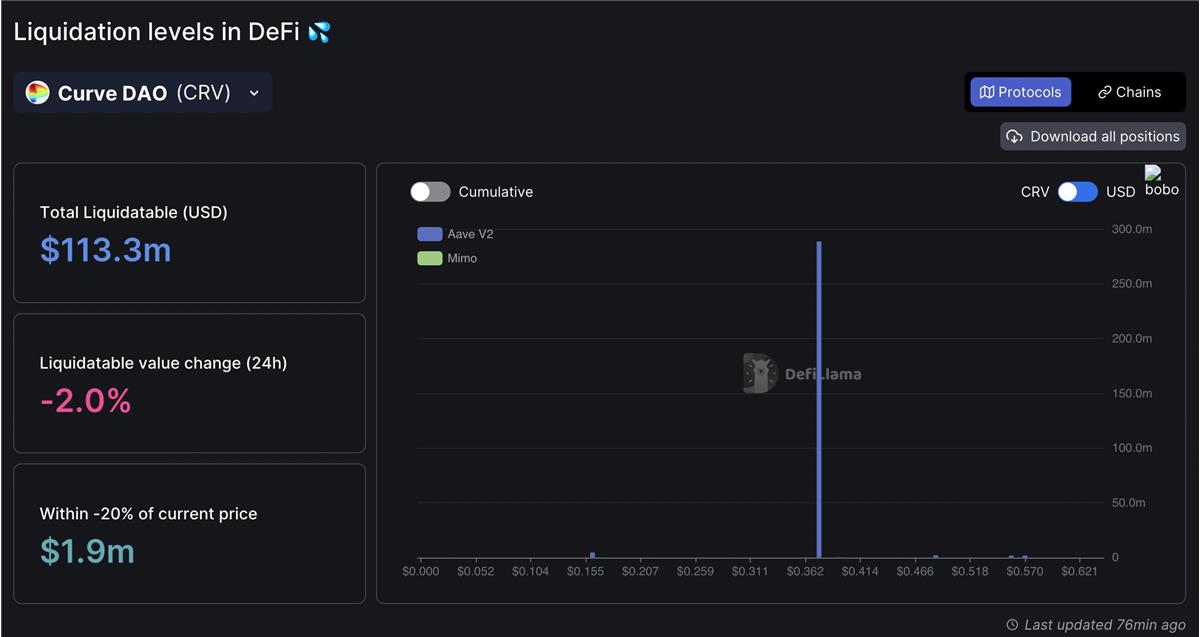

At present, the total on-chain liquidatable value of CRV stands at $113 million, with 99% (289 million CRV) concentrated around the $0.375 price level. — This implies that shorting via borrowed tokens could potentially push prices close to the liquidation threshold. However, the Curve founder has the capacity to add further collateral, thereby lowering the effective liquidation price. As a result, pure shorting would entail extremely high costs.

Aave enabling CRV borrowing and CRV liquidation levels

In reality, no party can liquidate such a large volume of CRV without causing massive slippage. Therefore, while reducing the LTV (Loan-to-Value) ratio in the CRV lending pool on Aave is a prudent risk management move to encourage Michael to repay his loan, abruptly setting the LTV to zero is inappropriate, as it would significantly increase Aave’s bad debt risk.

Although on-chain avenues to borrow CRV are now limited, spot selling pressure on-chain remains substantial. Moreover, shorting activity on centralized exchanges has surged notably over the past six hours (offering over 190% APY on BN to short CRV), with open interest increasing by $5 million in two hours and $14 million over 24 hours.

The Curve founder currently has borrowed over $44 million in stablecoins across Aave, Abracadabra, Fraxlend, Curve, and Inverse Finance. If liquidations occur (refer to the previous thread for details on liquidation prices), these lending platforms face potential bad debt exposure.

In practice, liquidating such a large amount of CRV on Aave would incur severe slippage. Thus, gradually reducing the LTV in the CRV lending pool is a sound risk control measure, but suddenly resetting the LTV to zero should be avoided, as it would drastically increase Aave’s risk of bad debt.

Over the past day, founder Michael withdrew over 700k wCRV (more than 25%) from Fraxlend and deposited it into Inverse Finance (fixed borrow rate at 6.84%). The address 0x73f8af was created by Inverse Finance’s FiRM CRV market. The Curve founder has pledged at least 600k wCRV in this address, and currently, the Inverse Finance CRV pool holds over 900k wTVL, mostly backed by the Curve founder’s collateral.

Additionally, another 4 million CRV remains pledged on Abracadabra, with nearly 80 million CRV locked in Abracadabra CDPs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News