Founder's statement: After three years of unsuccessful efforts to achieve compliance for a tokenized fund, I am now forced to leave the United States

TechFlow Selected TechFlow Selected

Founder's statement: After three years of unsuccessful efforts to achieve compliance for a tokenized fund, I am now forced to leave the United States

Money is the final battle for freedom. We will not stand by silently while you continue to control and manipulate us.

By Heimi

This week is destined to be one that the crypto industry will remember.

On Monday, the U.S. Securities and Exchange Commission (SEC) filed a lawsuit against Binance, the world’s largest cryptocurrency exchange. Binance and its CEO Changpeng Zhao face 13 charges, including listing multiple tokens as “unregistered securities,” commingling customer assets with its own, allowing U.S. customers to use Binance Globe, and artificially inflating trading volume on Binance.US through sham trades.

Binance responded immediately, stating it had been actively cooperating with investigations and seeking negotiated settlements, but the SEC chose enforcement action instead. The company vowed to vigorously defend itself against the SEC and continue striving to become a secure and trustworthy platform.

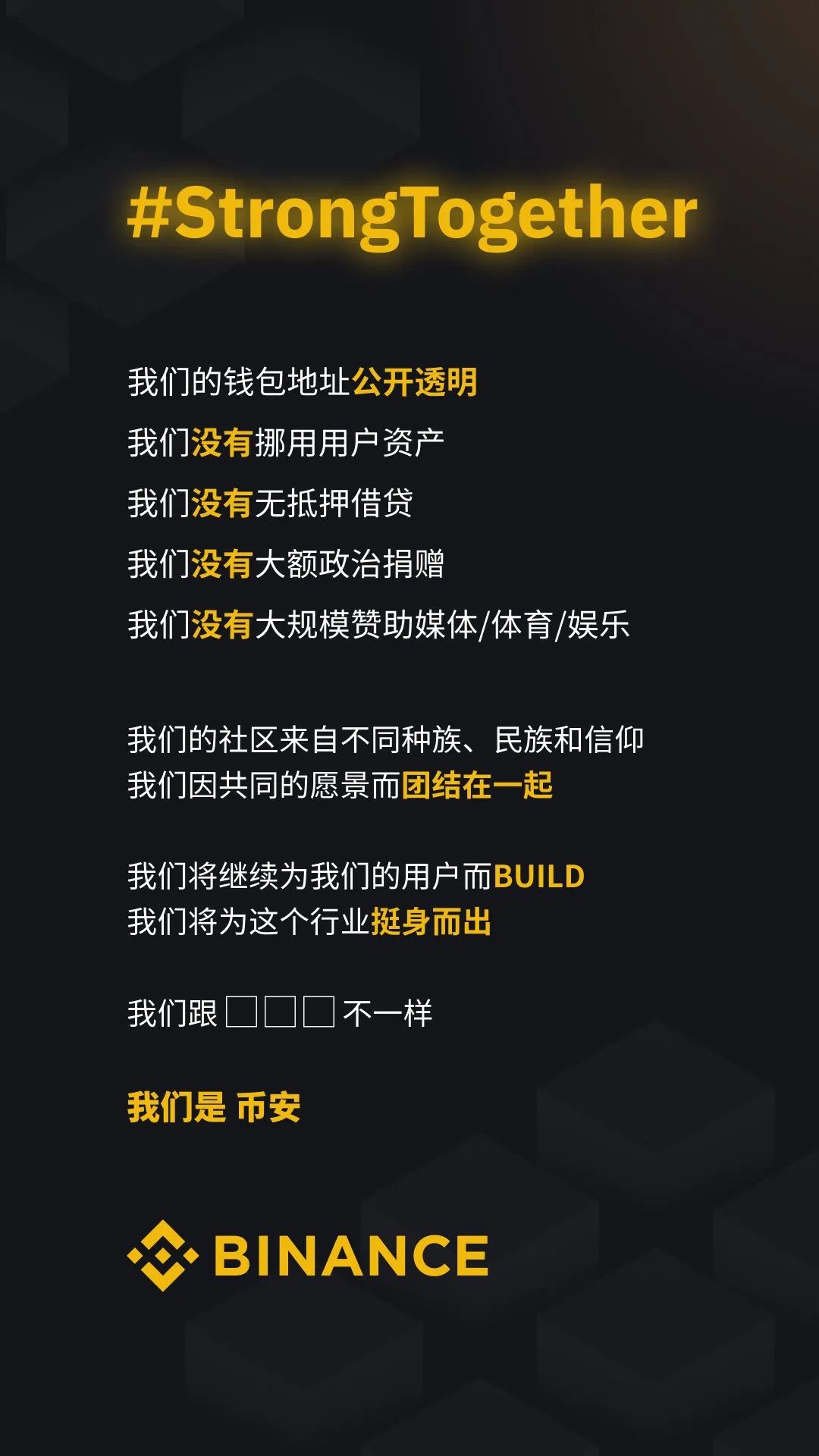

It later issued a "Strong Together" statement, asserting that Binance has not misappropriated user funds, maintains transparent wallet addresses, does not offer uncollateralized lending, and has made no large political donations or widespread sponsorships of media, sports, or entertainment. It pledged to continue building for users and standing up for the crypto industry.

On Tuesday, the SEC sued Coinbase, a U.S.-based compliant crypto exchange, accusing it of failing to register as an exchange, clearing agency, and broker-dealer. The SEC also explicitly labeled Coinbase’s staking services and numerous tokens traded on the platform as “unregistered securities.”

Currently, ten U.S. states—including Illinois, Vermont, Alabama, Kentucky, California, Maryland, Wisconsin, Washington, New Jersey, and South Carolina—have taken legal action against Coinbase over its staking services.

Coinbase responded via official Twitter: “Crypto has come a long way. In the U.S., it still has a long way to go. We’re ready!”

Clearly, Coinbase is also prepared to fight the SEC to the end.

Coinbase CEO Brian Armstrong questioned the true intent behind the SEC's lawsuit:

1. The SEC reviewed Coinbase’s business and allowed the company to go public in 2021.

2. Coinbase repeatedly attempted to register, only to conclude that the SEC did not provide a clear registration pathway.

3. The SEC and the Commodity Futures Trading Commission (CFTC) hold conflicting views on crypto regulation and have not even agreed on what constitutes a security versus a commodity.

4. While Congress is working to introduce legislation to formally establish regulatory laws, other crypto-friendly countries have already enacted clear frameworks. Instead of issuing clear rulebooks, the SEC is resorting directly to enforcement actions.

Why approve Coinbase’s IPO in 2021 only to sue two years later to ban the very same services?

Thus, the real motive behind the SEC launching major enforcement actions against two crypto giants within two days remains questionable—especially compared to the FTX collapse.

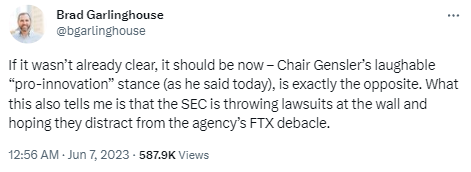

Ripple CEO Brad Garlinghouse quipped that this was the SEC attempting to “distract” public attention from the “FTX collapse.” SBF was Biden’s second-largest donor during his presidential campaign, and Biden appointed Gary Gensler as the current SEC Chair.

Some notable differences between the two lawsuits:

1. The SEC appears to deliberately aim to dismantle Binance

- Coinbase is required to disgorge all “ill-gotten gains” related to the alleged violations identified by the SEC, along with civil penalties and other forms of investor relief. When Kraken settled with the SEC in February over its staking product, it was forced to pay a $30 million fine.

- Binance, however, faces not only similar fines but also a permanent injunction barring it from engaging in securities and cryptocurrency trading activities altogether.

2. For Coinbase, it’s a battle for survival

In contrast to Binance, the fight between Coinbase and the SEC is a “life-or-death” struggle. Coinbase focuses more heavily on the U.S. market, with over 80% of its revenue coming from the U.S. last year. While Coinbase may continue operating normally in the short term, the SEC’s allegations could damage its reputation, potentially prompting users to withdraw funds from the platform.

Moreover, what would a settlement cost? If regulators seek to promote innovation through litigation rather than by establishing well-designed rules, how is that different from doing nothing at all?

It’s good—and necessary—to protect investors by helping the crypto industry shed its “Wild West” image. But persistently resorting to enforcement actions without clear legal guidance goes too far. This approach gives other countries the opportunity to become crypto havens. South America and the Caribbean are becoming increasingly attractive to crypto companies due to their friendlier and more open embrace of cryptocurrencies compared to the United States.

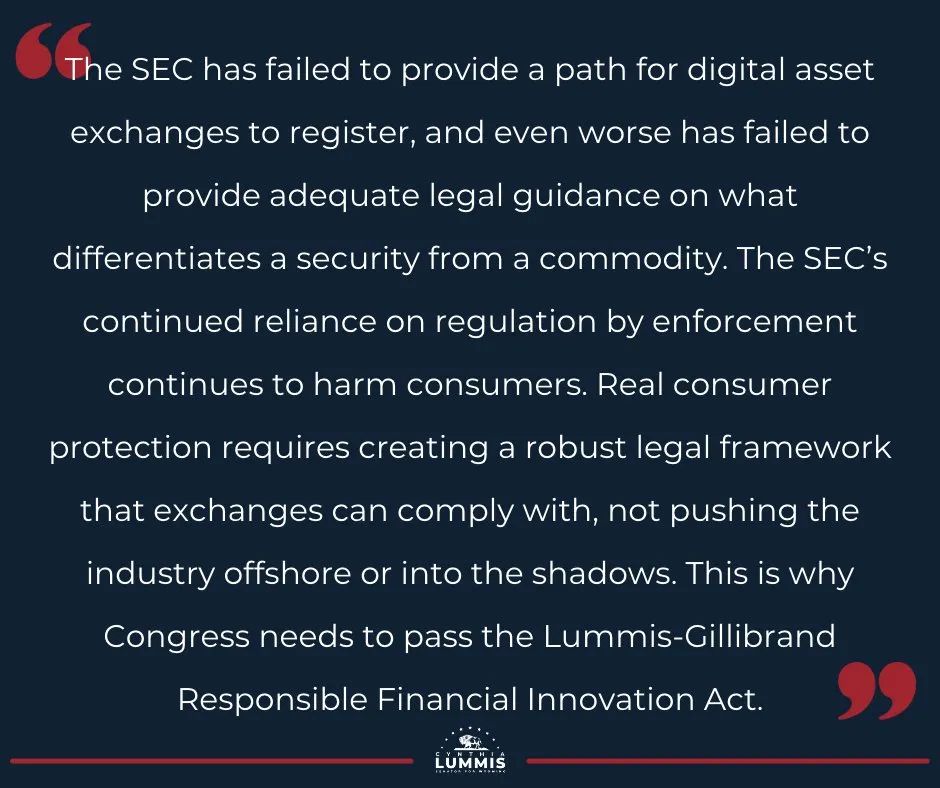

Senator Cynthia Lummis, who has long advocated for introducing crypto regulatory legislation in the U.S., stated in a press release: The SEC has failed to provide a registration pathway for digital asset exchanges and, worse, has offered insufficient legal guidance distinguishing securities from commodities. By continuing to rely on enforcement-driven regulation, the SEC is further harming investor interests. Real investor protection requires establishing a robust legal framework that exchanges can follow, not pushing the entire industry out of the United States. Congress needs to pass comprehensive crypto regulatory legislation as soon as possible.

This is no exaggeration. Recently, Derek Boirun, founder of Realio—a real-world asset (RWA) tokenization project—shared his frustrations in a blog post, bluntly stating that “hostile regulators forced me to leave the U.S.” BaiZe Research Center translated the following excerpt, with minor edits:

This summer—summer 2023—I will be leaving the United States indefinitely. A 42-year-old American citizen born and raised in the U.S., I am doing this solely to protect my constitutional rights, my family, and my company from excessive government interference. It sounds like something out of a surreal novel, but this is my reality.

I am the founder of Realio, a blockchain company focused on building digital infrastructure to bring real-world assets—such as real estate—on-chain. We began full-time development of this company in 2018, investing significant time and capital into its growth. From day one, our core focus has been regulatory compliance because investing in real-world assets—whether on or off the blockchain—typically falls under securities law. After all, investing in real estate isn’t new, nor are securities laws, so doing this “on the blockchain” seemed entirely feasible.

Fast forward to 2022. Having survived the economic collapse caused by the pandemic—largely thanks to rapid growth in the crypto market—we were scaling up and optimistic about businesses issuing compliant security tokens (publicly offered tokens within legal and regulatory frameworks) on our platform. Believing compliance was achievable, we generally ignored much of the narrative dominating the crypto space—the very place where most capital flowed. Many became extremely wealthy chasing “quick money,” whether anonymously or not, but we stayed the course. We even chose to tokenize our own company through a compliant security token offering. Fortunately, we managed to raise enough funding to sustain operations and development for several years. We’re deeply grateful for support from companies like Algorand, which invested in us through their ALGO token (today, I’m forced to hear Gary Gensler label ALGO as an unregistered illegal security). Without Algorand’s generous investment and the rise in ALGO’s price, our financial situation would look vastly different.

Between 2020 and mid-2023, most of our time was dedicated to compliance.

We launched a “tokenized” fund and spent substantial sums hiring top-tier lawyers to register the fund under the Investment Company Act of 1940 with the SEC. We spent more on this than many startups’ entire operational budgets. By the end of 2022, after multiple calls with SEC staff explaining our structure, we were ready to file registration documents. Then the FTX bankruptcy happened. Soon after, through conversations with our lawyers, I learned that the SEC was shutting down all registration efforts for “tokenized” funds seeking licenses. Yet this was the only path available to us for registration or compliance.

Meanwhile, we also applied to the Financial Industry Regulatory Authority (FINRA) for a Regulation CF portal license—a costly process in itself. Like with the SEC, we held multiple calls with FINRA staff and resolved all issues. But after FTX collapsed, FINRA requested another call to re-review our details. We prepared thoroughly and answered all questions sincerely. Still, we couldn’t help feeling these calls were merely performative—staff repeatedly asking basic questions, seemingly designed to wear us down or trap us in technicalities. After each call, we received extensive follow-up questionnaires that went far beyond our original application. It became clear that FINRA might delay our approval for years, so we decided to put the application on hold until a new administration takes office.

Most blockchain-based asset issuers actually lack any viable registration pathway—not due to lack of effort or unwillingness to comply. From firsthand experience, I can attest that regulators do not treat the crypto industry fairly or kindly. I'm no stranger to the various tactics regulators employ against us—classic “bureaucracy.”

Yet talented individuals across the crypto space are diligently building a better global financial system. This isn’t a game or a political stunt. Many of us left traditional careers to pursue this vision. Now, we are also leaving the United States.

Money is the final frontier of freedom. We won’t stand idly by while you continue to control and manipulate us. Despite your positions, you do not have this authority. You have no right to dictate what the market needs or doesn’t need. This is precisely the kind of overreach we fought for independence to escape. Capital markets are suffocating under regulations that don’t actually protect anyone except the wealthiest.

Leaving the U.S. isn’t easy. I have a family who loves New York, and so much else. But I have a duty to protect everything we’ve built—which means finding a country that supports our continued innovation.

We won’t stop. We will continue building the digital future we’ve always worked toward.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News