MEME Coin Investment Practical Guide: Methodology, Techniques, and Tools

TechFlow Selected TechFlow Selected

MEME Coin Investment Practical Guide: Methodology, Techniques, and Tools

The diversity of seed users can bring many surprises to a project in its early stages, especially when accompanied by wealth creation effects.

Author: Jarseed

Since the crypto market entered the MEME season, countless rags-to-riches stories and overnight collapses have been unfolding. People marvel at the hundred- or thousand-fold gains of $PEPE, $Turbo, $AIDOGE, and $MILADY, yet when they buy MEMEs themselves, they often lose money immediately and watch their holdings drop to zero. Many dismiss MEMEs as valueless, while others argue that trading MEMEs is all about sentiment and attention. Both views are somewhat mechanically reductionist. Today, I’ll analyze MEME tokens from the perspective of token distribution and how to trace on-chain address relationships, offering some support for your speculation decisions—perhaps not helping you pick the best performer, but possibly helping you identify which ones are worse.

If we treat token issuance as a business, we need to understand the following points:

-

The project team creates a product—even if it has no concrete utility, they must find ways to attract more buyers.

-

Every business must consider its cost-benefit ratio. The team can either hoard a large share during initial distribution (primary market), then dump when conditions are right; distribute cheaply at launch and later buy back from users (secondary market); or simply rug the liquidity pool and run.

-

Some MEME tokens even experience "change of control," where early developers fully dump their holdings, but speculation continues as new capital takes over, allowing the narrative to persist.

So how does one launch such a business? I believe the following issues must be addressed:

-

Lock in seed users

There are many examples at this stage: vampire attacks like $AIDOGE, which airdropped based on Arbitrum eligibility; presales or LGE/TGE (Liquidity Generation Event / Token Generation Event) via IDO platforms or Alpha communities; or fabricated bulk distributions (examples below).

-

Create initial liquidity

For an on-chain asset to circulate and trade, initial liquidity is required. Teams typically pair their token with ETH (in most cases) using Uniswap’s factory function to create a liquidity pool, enabling public buying and selling.

-

Media matrix coverage

When CT (Crypto Twitter) information streams are flooded with talk about a certain MEME token, curiosity drives us to check it out. Influencers may promote it organically for attention, get paid to shill, or even use deconstructionist narratives to sell other products.

-

Price and volume rise together

To facilitate dumping, teams often hold large amounts early to manipulate price pumps. As trading volume and price surge, platforms like Dextool and Dexscreen list the token on gainers’ charts, bringing it into retail investors' view.

Next, I will present two specific cases to show how these projects locked in seed users and initiated token distribution, and what kind of price action followed. A clear disclaimer: the tokens mentioned below do not constitute investment advice—please take responsibility for your own investments.

Case One:

Simpson

Contract Address:

0x44aad22afbb2606d7828ca1f8f9e5af00e779ae1

Main Liquidity Pool:

0x7945819d6cab17f94c4089c28767e164ed4acf3e

Deployer Address:

0xC43b6eCaF08b515001d58f4f427e03A4CE4758dd

Total Supply: 420,000,000,000,000,000

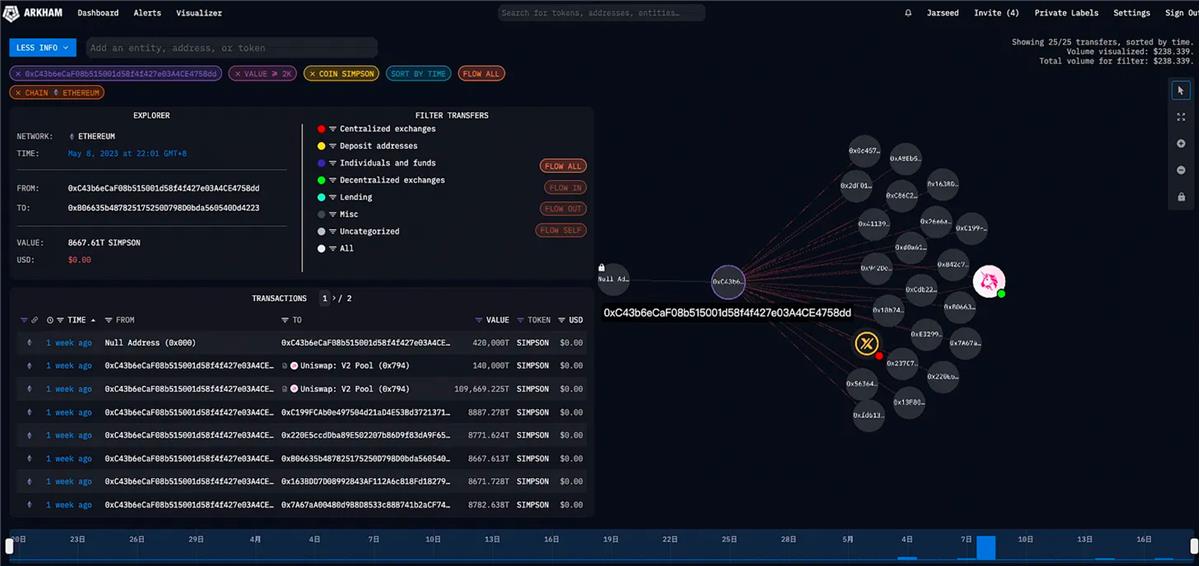

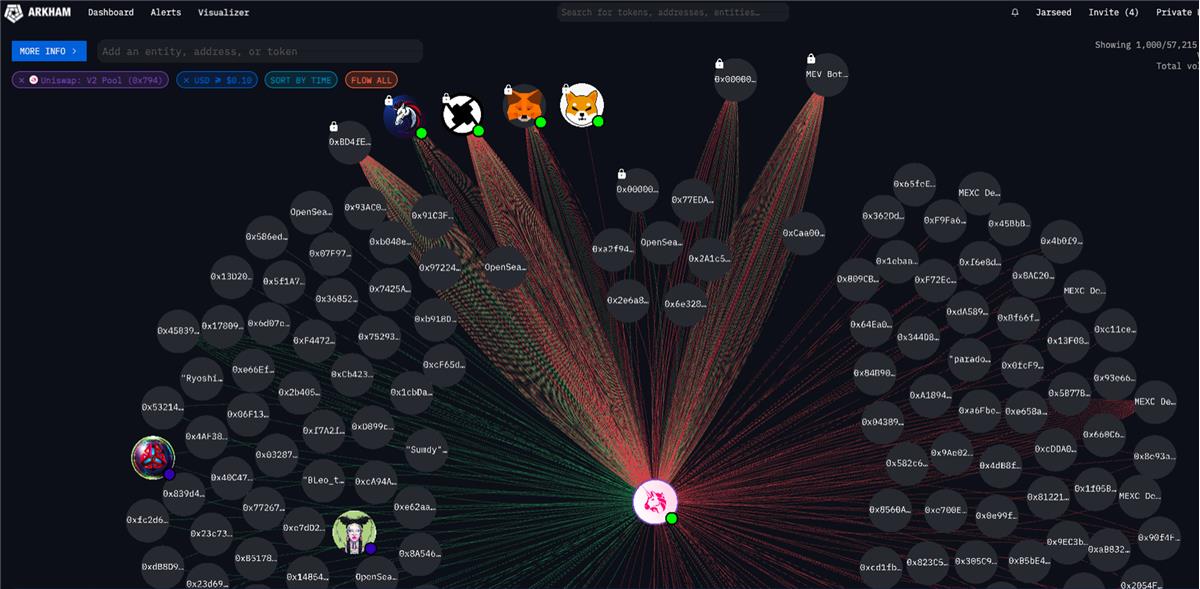

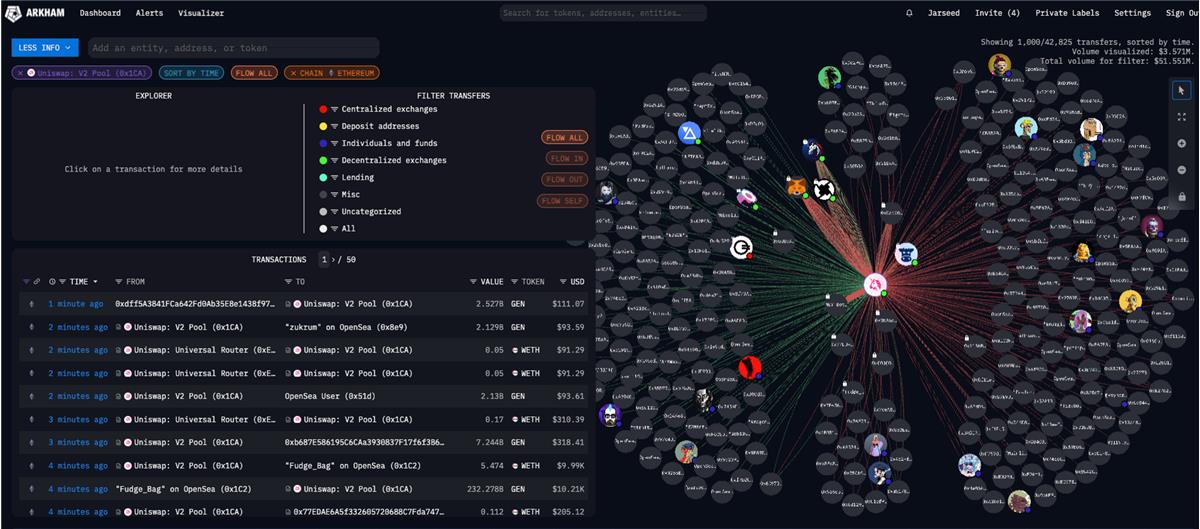

Let’s use Arkham to interpret Simpson’s initial token distribution:

Simpson creator's address distributing tokens

From the image above, we can see:

-

The Simpson token creator allocated approximately one-third of the initial supply to the Uniswap liquidity pool.

-

The creator distributed 8800T Simpson tokens to 20 addresses, each holding roughly 2% of total supply, totaling 40%.

With this, 70% of the tokens were already distributed. Now comes the creator’s clever maneuvering.

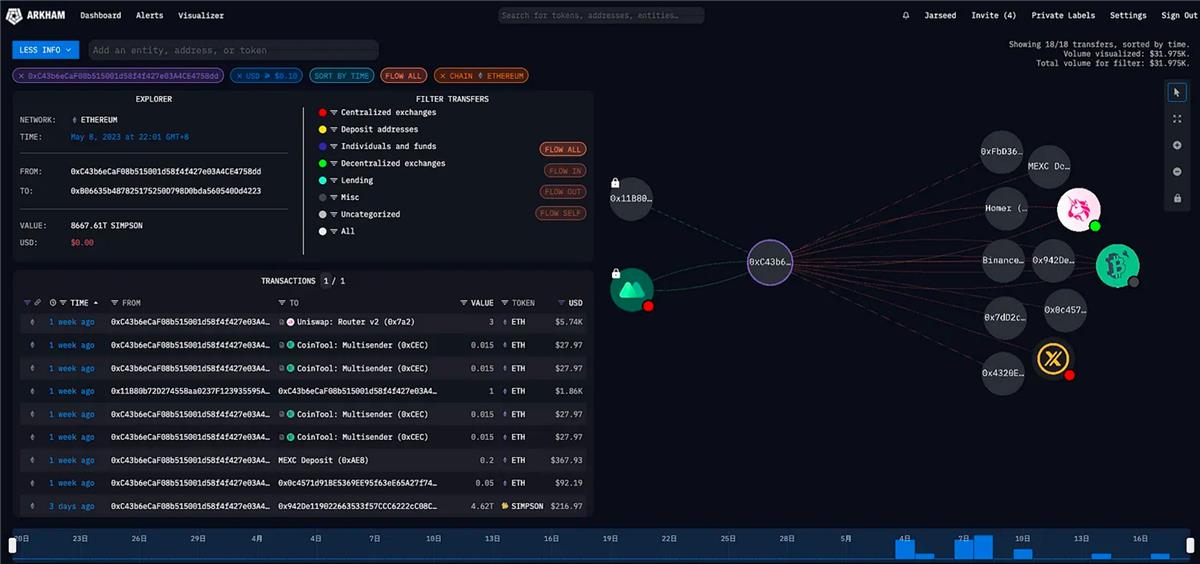

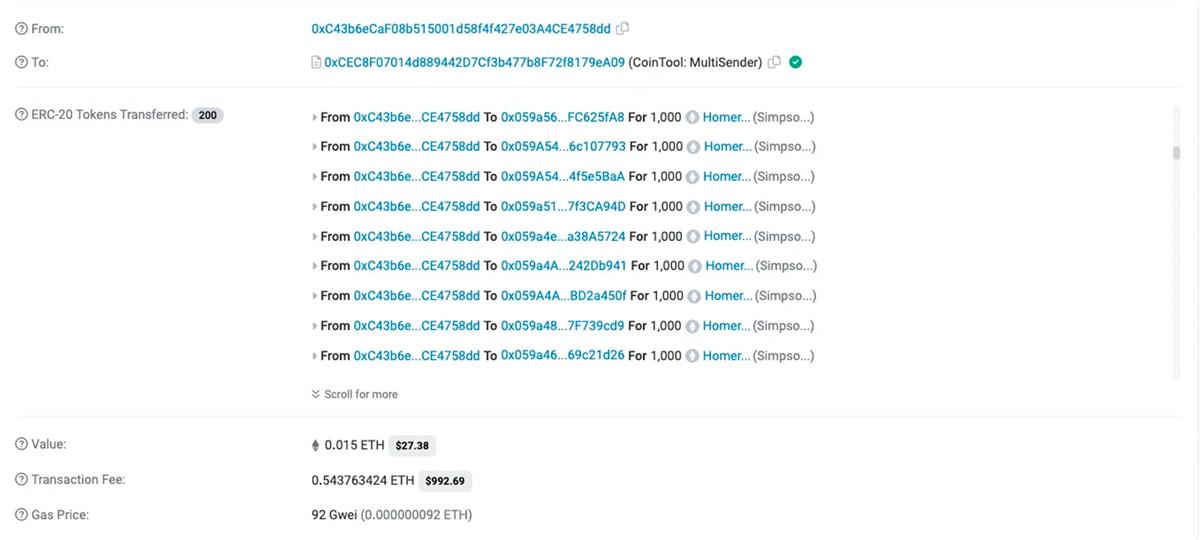

On-chain activity shows the creator used CoinTool’s Multisender feature. Those familiar with on-chain data may recognize CoinTool—it once dominated Ethereum gas usage rankings. The creator used CoinTool to distribute Simpson tokens to numerous addresses. Browser tools reveal the creator used CoinTool four times, sending tokens to 800 addresses, each receiving 1000 Simpson tokens.

We notice a pattern among these recipient addresses—all start with 0x059a. Those familiar with hash algorithms know these are batch-generated addresses, some of which the team may not even hold private keys for, randomly distributed since 1000 Simpson tokens mean almost nothing against a 420 quadrillion total supply. However, this move gave the project 800 on-chain holders at launch.

What happened next is well known. After Binance listed $PEPE on May 5, MEME tokens reignited traders’ enthusiasm, sparking a frantic search for the next $PEPE. What criteria do people usually follow? New token, decent number of holders, solid trading volume, simple and easily shareable meme, strong social media presence.

Yet, while buyers dream of riches, early-positioned players are already cashing out.

Beyond token distribution, another angle is interaction with the trading pool.

In addition to retail trades and aggregators, MEV bots also play a role in fueling the MEME frenzy.

Many MEME tokens casually achieve daily trading volumes in the hundreds of thousands—or even millions—of dollars, largely thanks to MEV bots. In fact, around 90% of trading volume for most MEME tokens comes from MEV bots. Tokens with transaction taxes force traders to increase slippage, making them easy prey for MEV strategies.

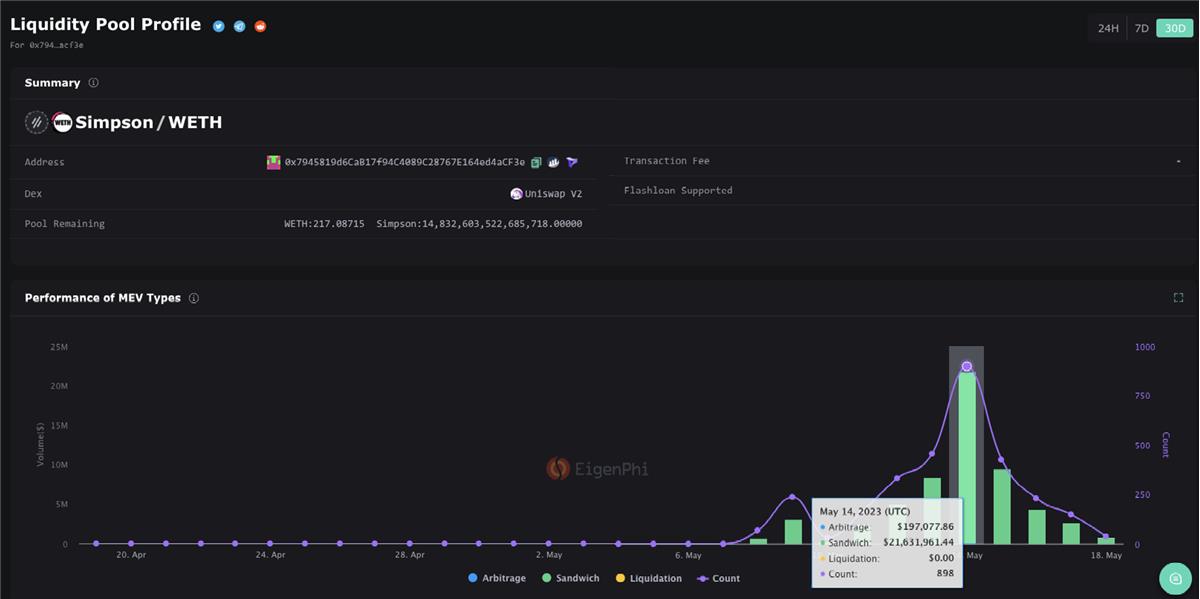

I recommend a tool called Eigenphi. Input your target token’s pool address to see MEV trading volume statistics, estimate real buyer demand, and compare across different MEME tokens.

Summary:

From the Simpson case, we can draw two conclusions:

-

To play the game against project teams effectively, estimate their costs. Here, the team spent 6 ETH on initial liquidity and 2 ETH on Gas using CoinTool to generate 800 holder addresses. Add marketing and pumping expenses, and you get a rough idea of their total cost.

-

Concentrated dumping: The initial 20 addresses dumped en masse around May 13. Joining the game after that point might not be wise.

Case Two:

GenerationalWealth (GEN)

Contract Address:

0xcae3faa4b6cf660aef18474074949ba0948bc025

Main Liquidity Pool:

0x1ca4713fc4a95f76fcb498b2a5fe8759c53df1a1

Deployer Address:

0x6579116367e0090d1cA6F5F712e172996E527E4c

Total Supply: 420,690,000,000,000

Let’s apply the same method to analyze GEN’s initial distribution:

GEN had a presale phase. First, we need to locate the presale contract address (contract link)

According to the team, 15% of GEN tokens were sold via presale. On-chain data shows 672 participants, each contributing 0.05 ETH and receiving 105B GEN tokens.

Among presale participants, many have ENS domains, and several are labeled by Arkham as OpenSea users. These addresses show diverse characteristics and varying degrees of on-chain activity—indicating healthy, diverse seed users, a sign of successful initial distribution.

On the other hand, among large holders:

-

The GEN creator deployed 302T tokens (72% of circulating supply) into the Uniswap liquidity pool.

-

Three major linked addresses—0x83Fae943b5381eCE611bda1fA44f744966Bc9552, 0xa0F06e6Ab3A999294E4b6B1EF8f4689c5D785482, and 0x7E0DaBBC101402880D281f86E51E439f897A752a—hold 6.9%, 3.68%, and 2% of the circulating supply respectively, totaling ~12.5%. Observations show two of these addresses currently lack ETH, making transfers impossible.

What do we observe—and what should we pay attention to—when speculating on such tokens?

-

First, the seed user base likely comes from NFT/Alpha communities or was driven by an NFT influencer. Presale participants paid 0.05 ETH and have already made over 20x returns.

-

Second, although the team visibly retains 12.5% of tokens, two key addresses lack ETH—so we can monitor them for future movements.

-

Is a rug pull possible? The creator deposited LP tokens into the GEN contract itself, with no further action yet—worth ongoing monitoring.

-

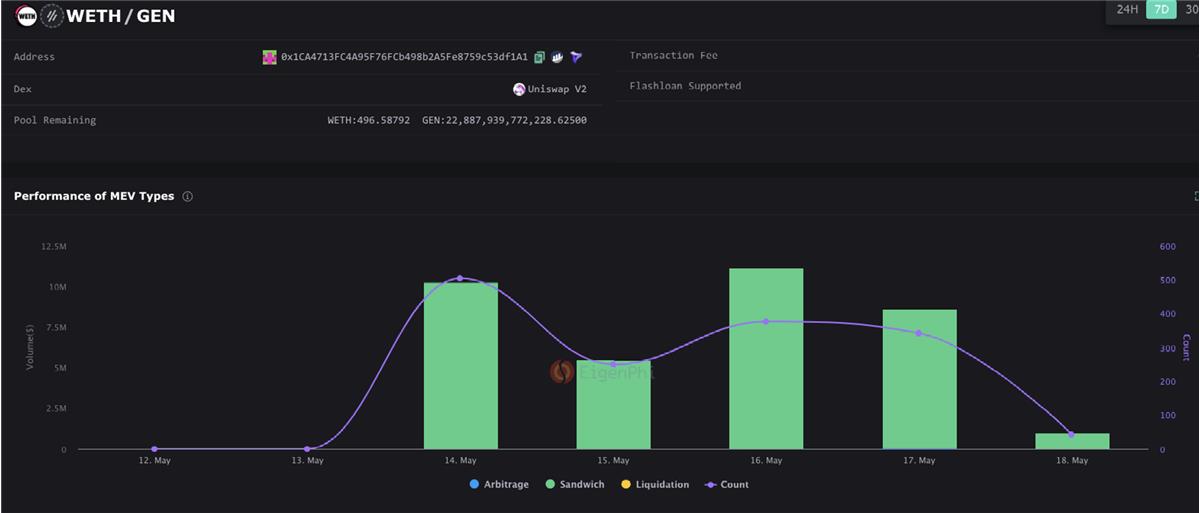

Using Eigenphi, we see strong organic buying pressure at certain times.

-

Pool interactions are also significantly more active.

Summary:

From the GEN case, we can conclude:

-

Diverse seed users can bring pleasant surprises in a project’s early stages, especially when wealth effects kick in.

-

By filtering out MEV volume, we can better assess real demand and make fair comparisons between MEME projects.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News