LD Capital: Crypto Asset Management from the Perspective of U.S. Equity Index Enhanced Yield Strategies

TechFlow Selected TechFlow Selected

LD Capital: Crypto Asset Management from the Perspective of U.S. Equity Index Enhanced Yield Strategies

The market size and current state of U.S. equity index funds and enhanced index funds/ETFs offer reference value for the development path of enhanced index funds in the crypto market.

Authors: Yilan Liu, Jinze Jiang, Drake Zhang, LD Capital Research

Introduction

In recent years, index-based products represented by ETFs have developed rapidly in traditional financial markets, showing a trend where Smart Beta ETFs and actively managed ETFs experience faster capital inflows than conventional index ETFs. The asset management industry’s focus has gradually shifted from standard index products to more innovative series such as ESG ETFs, actively managed ETFs, and thematic ETFs. Active equity ETFs, in particular, have achieved new breakthroughs, attracting off-exchange products to transform proactively, becoming a hotspot in active product development. Global index providers continue innovating and refining their index systems to meet evolving market demands, driving the industry toward finer granularity and greater diversification while promoting continuous innovation in indexed products. In contrast, crypto index-enhanced products remain in a very early stage compared to traditional finance. As the overall cryptocurrency market cap grows, the potential for structured index-enhancement products should also expand rapidly. We believe the scale and current state of U.S. equity index funds and enhanced index funds/ETFs offer valuable reference points for the development path of crypto index-enhanced funds. Crypto index-enhanced funds could utilize various return-enhancing methods—such as multi-factor quantitative stock selection models, discretionary timing models, sector rotation models, or index futures derivative enhancement strategies—to deliver alpha returns tailored to investors with varying risk preferences.

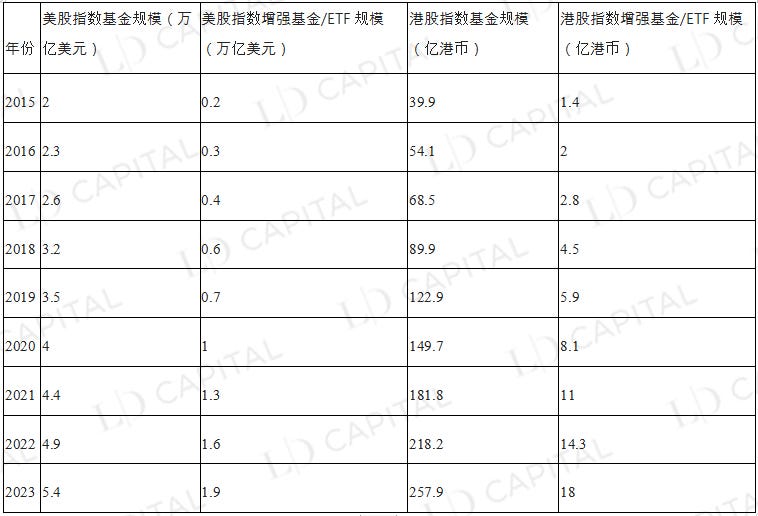

Scale and Development Trends of Standard Index ETFs and Enhanced Index Funds/ETFs in Hong Kong and U.S. Markets

Between 2015 and 2023, both standard index funds and enhanced index funds/ETFs in the U.S. and Hong Kong markets showed steady growth. Notably, enhanced index funds/ETFs—particularly actively managed ETFs—grew at a much faster pace, increasing tenfold over eight years and reaching nearly one-third the size of standard index funds by 2023.

Table 1: Total AUM Comparison of Standard Index Funds vs. Enhanced Index Funds/ETFs in U.S. and Hong Kong Markets (2015–2023)

Source: VettaFi, Statista

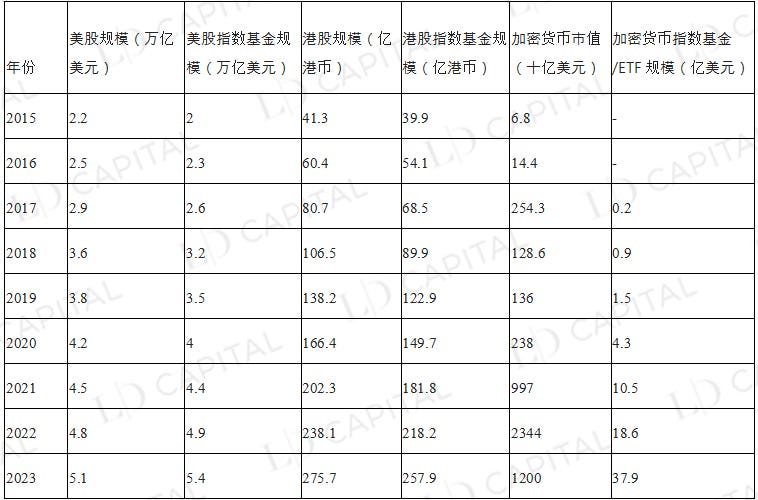

In traditional financial markets, the AUM of index funds in the U.S. and Hong Kong has even begun to approach or exceed the market cap of their underlying indices. In contrast, crypto index funds/ETFs remain far below their corresponding market caps. With rising interest from traditional investors in crypto asset management products, the development prospects for cryptocurrency index funds and exchange-traded funds (ETFs) are broad.

Table 2: Market Cap and Corresponding Index Fund/ETF AUM Comparison Across U.S. Equities, Hong Kong Equities, and Cryptocurrencies

Source: VettaFi, Statista

Active Management Characteristics of Enhanced Index Funds

Index funds generate market-correlated returns (β returns) by tracking characteristics such as tracking error, market-cap style, valuation style, industry weightings, and individual stock allocations.

Enhanced index funds, however, employ active management by fund managers aiming to generate excess returns (α returns) beyond the benchmark. This allows them to fall less than the index during market downturns and outperform during upswings, striving for stable compound performance over the long term.

Regarding benchmark tracking, enhanced index funds can follow a wide range of indices, including broad-market benchmarks, single-industry indices, or thematic indices. In the current U.S. and Hong Kong markets, major beta targets include broad indices such as the S&P 500, Nasdaq-100, Russell 2000, DJIA, HSI, and HSCEI.

Ways to Enhance Returns in Index Funds

With ongoing financial innovation, enhanced index funds can achieve excess returns through multiple approaches, creating the "enhanced" effect. These enhancements typically come from strategies such as multi-factor quantitative stock selection, discretionary timing models, sector rotation models, or derivative-based yield enhancement using index futures—commonly used methods in today’s enhanced index products.

Quantitative Multi-Factor Enhancement Strategy Products

The goal of quantitative multi-factor enhancement strategies is to improve returns by simultaneously applying multiple factors in stock selection. These factors span various dimensions, including technical indicators (market momentum and technical signals), macroeconomic indicators, statistical data mining (machine learning, deep learning), and fundamental factors such as corporate financial stability, dividend yield, and valuation metrics.

Table 3: Common Multi-Factor Enhanced Index Funds in the U.S. Market

Take the Invesco S&P 500 High Dividend Low Volatility ETF (SPHD) as an example. SPHD tracks the S&P 500 High Dividend Low Volatility Index, employing a multi-factor stock selection strategy focused on high dividend yield and low volatility stocks. It selects the 50 securities in the S&P 500 with the highest dividend yields and lowest volatility. Holdings are weighted by dividend yield, with a maximum 3% cap per stock to ensure diversification. To maintain its low-volatility objective, the fund rebalances semi-annually, reassessing stocks based on updated dividend and volatility metrics. Due to its defensive profile, the ETF typically outperforms the broader S&P 500 during bear markets but may lag in strong bull markets.

SPHD’s enhanced returns stem from overweighting high-dividend and low-volatility stocks. However, it significantly underperformed the S&P 500 benchmark over the past year, likely because high-dividend sectors—such as financials, energy, aviation, and tourism—were heavily impacted during the pandemic. Stocks in these sectors performed poorly, especially financials, which make up 26% of SPHD’s portfolio and were hit hard during recent banking crises. This underperformance led to a significant outflow in AUM.

Strictly speaking, SPHD and QUAL are considered passively managed funds that partially use enhancement techniques. These enhancements aim to optimize specific portfolio factors, but the overall investment strategy remains primarily benchmark-tracking. In contrast, QARP not only uses passive methods to track an index but also applies enhancement techniques and active management strategies in selecting portfolio constituents, making it a more typical actively managed fund.

When implementing quantitative multi-factor enhancement strategies, considerations must be made regarding factor weighting and the number of holdings. Different combinations of factor weights and holding counts can help achieve distinct investment objectives. For instance, emphasizing financial stability and earnings consistency factors may target conservative stocks, while focusing on market momentum and technical indicators may favor growth-oriented equities.

Discretionary Timing Enhancement Strategy

Discretionary timing as an investment strategy can be broken down into several methods: technical timing, fundamental timing, macroeconomic timing, sentiment-based timing, and event-driven timing. These approaches rely on different analytical frameworks to identify market trends, valuations, and opportunities, enabling better decisions on entry, exit, or portfolio adjustments.

1. Technical Analysis Timing: Technical analysis identifies potential market trends by studying historical price and volume data. Investors use tools like trendlines, moving averages, and RSI to determine market direction, strength, and turning points, helping to time buy/sell decisions.

2. Fundamental Analysis Timing: Fundamental analysis focuses on company-specific factors such as financial health, competitive advantages, and industry positioning. By deeply analyzing fundamentals, investors assess intrinsic value and growth potential. When market prices undervalue this intrinsic worth, they buy; when overvalued, they sell.

3. Macroeconomic Analysis Timing: Macro timing strategies base decisions on how macroeconomic data influences market movements. These involve analyzing interest rates, inflation, monetary policy, and geopolitical developments. For example, investors may increase equity exposure during economic expansions and reduce it—or shift to safer assets—during recessions. Portfolio adjustments reflect the manager’s outlook on global macro conditions, potentially generating excess returns compared to passive benchmark tracking.

4. Market Sentiment Analysis Timing: This method examines how investor psychology affects prices. Tools like the Fear & Greed Index or Investor Confidence Index help determine whether the market is overly pessimistic or optimistic. Buying during extreme fear and selling during excessive euphoria may yield alpha. Sentiment strategies are increasingly popular, with other indicators including AAII Sentiment Survey, VIX, market breadth, and put/call ratios.

5. Event-Driven Timing: This strategy focuses on specific events impacting company value—such as M&A, spin-offs, or restructuring—and times trades based on expectations around these events.

Take the Pacer Trendpilot US Large Cap ETF (PTLC) as an example. PTLC is a U.S.-equity ETF employing an active timing strategy, aiming to adjust exposure to large-cap U.S. stocks based on market trends to achieve relatively stable returns.

The fund primarily tracks the S&P 500 using a moving-average-based timing model. When the S&P 500 trades above its 200-day moving average and its last five closing prices are above its 5-day MA, PTLC is fully invested in the S&P 500. When the index falls below the 200-day MA, the fund allocates 50% to the S&P 500 and 50% to short-term U.S. Treasuries. If the 5-day MA stays below the 200-day MA for five consecutive days, the fund shifts entirely into short-term Treasuries.

Examining PTLC’s performance in specific market environments—such as the 2017 bull market, volatile 2018, and the 2020 pandemic shock—reveals key features of timing-enhanced funds. In 2017, the S&P 500 returned about 21.8%, while PTLC delivered approximately 20.4%, slightly underperforming due to management fees and trading costs. While it captured most of the upside, it trailed the benchmark in strong bull markets.

In 2018, the S&P 500 rose sharply early but fell sharply later, ending down ~4.4%. PTLC performed better, returning ~-3.7%, demonstrating some downside protection.

In early 2020, the COVID-19 crisis caused a ~34% drop in the S&P 500 before a strong rebound, resulting in a full-year gain of ~16%. PTLC returned only ~11.5%. Although the timing strategy reduced losses during the crash, it underperformed during the recovery phase, leading to lower annual returns versus the benchmark.

Thus, in rising markets, PTLC performs similarly to the benchmark; in falling markets, its timing strategy may mitigate losses, but due to tracking error, it does not outperform the index in all conditions.

Sector Rotation Enhancement Strategy

Sector rotation enhancement strategies anticipate which sectors will lead ahead of market moves by analyzing business cycle dynamics. They increase exposure to industries in upward trends or reduce exposure to lagging ones (“overweight” or “underweight”), deviating from index sector weights to generate excess returns relative to the benchmark’s performance.

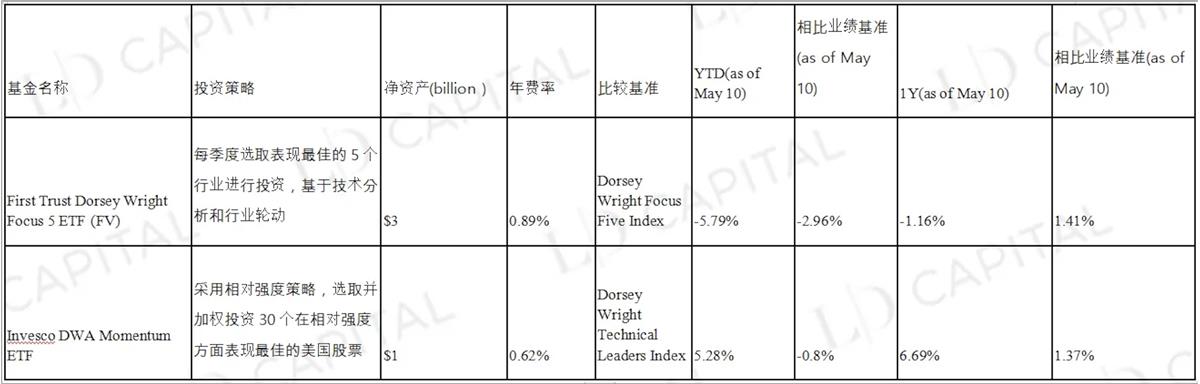

Table 4: Common Sector Rotation Enhanced Index Funds in the U.S. Market

Take PDP (Invesco DWA Momentum ETF) as an example. PDP aims to track the Dorsey Wright Technical Leaders Index, using a relative strength strategy to select and weight the top 30 U.S. stocks with the strongest momentum. If tech stocks show the strongest relative strength, PDP will overweight the best-performing tech stocks.

To execute this, PDP regularly rebalances to stay invested in the highest-momentum stocks. If market conditions change and other sectors—like consumer goods—start gaining relative strength, PDP adjusts its holdings accordingly, shifting weight to newly outperforming sectors.

Overall, PDP’s strategy relies on relative strength for stock selection and adapts to changing market trends through periodic rebalancing. The basis for selection is relative performance against peers or the broader market. Both funds in the table outperformed the benchmark over a one-year horizon, though their YTD performance has been weaker.

Derivatives-Based Enhancement Strategy

Derivatives-based enhancement strategies use options, futures, swaps, and other derivatives to boost portfolio performance. These often involve leverage, hedging, and speculative elements.

Some U.S. Equity-Based Derivatives Enhancement Strategies Include:

1. If index futures trade at a discount to the spot index, investing in futures instead of cash positions can capture convergence gains. When the futures price is below the spot level, buying futures offers theoretical profit as prices converge at expiry. This frees up capital, which can be deployed into fixed income or arbitrage strategies for stable returns.

2. Calendar Spread Arbitrage: Exploiting price differences between futures contracts of the same index with different expiration dates. When the forward contract trades at a premium to the near-term one, go long the near-term and short the forward. As the spread narrows over time, profits emerge.

3. Inter-Market Arbitrage: When highly correlated markets (e.g., commodities, rates, currencies) exhibit pricing discrepancies, take offsetting long/short positions. Over time, mispricing tends to correct, generating enhanced returns.

4. Options Strategies: A common approach is writing covered calls to boost income. The fund holds stocks and sells call options against them, collecting premiums to enhance total returns. The trade-off is capping upside if the stock rises above the strike price.

5. Pairs Trading: Involves two stocks in the same sector or with high correlation. When their spread diverges from historical norms, go long the undervalued stock and short the overvalued one. As the spread reverts, profits are realized.

Take ProShares UltraPro Short QQQ ETF (SQQQ), a U.S. equity-based derivatives-enhanced fund, as an example.

ProShares UltraPro Short QQQ ETF (SQQQ) delivers daily returns that are -3x the performance of the Nasdaq-100 Index. This inverse leveraged ETF is designed for experienced investors who expect short-term declines in the tech-heavy Nasdaq-100. To achieve its objective, SQQQ uses swaps, futures, and options to gain short exposure to the index. As a result, it magnifies gains when the index falls—but also amplifies losses when it rises.

Specifically, in swap strategies, SQQQ enters agreements with financial institutions to exchange returns on the Nasdaq-100 at a fixed rate, gaining synthetic short exposure without owning shares.

In futures strategies, SQQQ sells Nasdaq-100 index futures, agreeing to deliver the index at a set future price, allowing short exposure without direct ownership.

In options strategies, SQQQ buys puts on the Nasdaq-100, giving it the right to sell the index at a predetermined price. This generates profits when the index falls, establishing short exposure. These trades are executed across multiple platforms to ensure liquidity and optimal pricing. However, SQQQ is generally considered a high-risk, short-term instrument unsuitable for long-term holding.

Diverse Enhancement Strategies Tracking the Same Index Offer Tailored Risk Exposure

Even when tracking the same index, different enhancement strategies and leveraged products allow investors to choose exposure levels aligned with their risk tolerance, goals, and return expectations. Below is an overview of Nasdaq-100-linked products, most of which are passively managed, offering investors varied ways to gain targeted exposure and returns.

QQQ (Invesco QQQ Trust): As Invesco’s flagship product, QQQ is the most popular and well-known ETF tracking the Nasdaq-100 (AUM $175.78B). It replicates the index by investing in the same securities in identical proportions—specifically, the 100 largest non-financial companies listed on Nasdaq. QQQ is a market-cap-weighted ETF, meaning holdings are weighted by market size.

QTR (Global X NASDAQ 100 Tail Risk ETF): Aims to track the Nasdaq-100 while reducing tail risk. It invests in the same securities as QQQ but also holds put options on the Nasdaq-100 to hedge against sharp market declines.

QQQM (Invesco Nasdaq-100 ETF): A lower-cost alternative to QQQ, tracking the same index with similar holdings and strategy but a lower expense ratio, making it more cost-effective for long-term investors.

QQQN (Invesco NASDAQ-100 Triple Q Disruptive Innovators ETF): An ETF targeting the Nasdaq Q-50 Index, which includes non-financial firms ranked 101–150 by market cap on Nasdaq. These are typically high-growth, innovative companies. QQQN provides exposure to emerging disruptive innovators.

QQQA (ProShares Nasdaq-100 Dorsey Wright Momentum ETF): Seeks to track the Dorsey Wright NASDAQ OMX CTA Momentum Index, using a momentum strategy based on relative strength signals. It selects Nasdaq-100 components with strong short-term performance, assigning higher weights to stronger performers and excluding or reducing exposure to weaker ones.

TQQQ (ProShares UltraPro QQQ): Aims to deliver triple the daily return of the Nasdaq-100 High Beta Index—a leveraged ETF providing 3x the daily move of the Nasdaq-100. It tracks the full index but exhibits significantly higher volatility and risk due to leverage.

QQQX (Nuveen NASDAQ 100 Dynamic Overwrite Fund): An actively managed fund based on the Nasdaq-100. It employs a “covered call write” strategy—holding Nasdaq-100 stocks while selling call options. This generates premium income, boosting returns and offering partial downside protection in flat or declining markets. However, the strategy caps upside potential, as gains are limited if the index rises above the call strike price.

The goal of the overwrite strategy is to enhance portfolio returns through option premiums and provide some buffer during market drawdowns. However, selling calls inherently limits participation in strong market rallies.

Conclusion

Compared to the mature equity ETF/index fund market in the U.S., the crypto index-enhanced product market remains in its infancy. As the overall crypto market cap expands, the growth potential for structured index-enhanced products should increase rapidly. We believe the diverse enhancement strategies seen in U.S. equity index funds can be adapted to construct crypto index-enhanced funds. These include multi-factor quantitative models, discretionary timing, sector rotation, and derivative-based yield enhancement—all of which can help investors with different risk appetites achieve tailored exposure and excess returns.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News