Decrypting the Silvergate and Silicon Valley Bank Crisis: A High-Stakes Gamble Under the Dollar's Rate Hike Cycle

TechFlow Selected TechFlow Selected

Decrypting the Silvergate and Silicon Valley Bank Crisis: A High-Stakes Gamble Under the Dollar's Rate Hike Cycle

All-in on bonds feels great for a moment, but facing a rising dollar interest rate is hard to handle.

Author: 0xmin

U.S. mid-sized and small banks are collapsing one after another!

On March 8, Silvergate Bank—famous for its crypto-friendly stance—announced it would liquidate and return all deposits to customers.

On March 10, Silicon Valley Bank (SVB), which specializes in providing financial services to tech companies in Silicon Valley, sold $21 billion in available-for-sale securities at an $1.8 billion loss, raising concerns about liquidity issues. Its stock plummeted over 60% on Thursday, wiping out $9.4 billion in market value in a single day.

This spooked many prominent figures in Silicon Valley.

Peter Thiel, known as the "godfather of Silicon Valley," instructed portfolio companies of his venture fund Founders Fund to withdraw funds from SVB. Y Combinator CEO Garry Tan also issued warnings, advising startups in their network to consider limiting exposure to lenders, ideally keeping no more than $250,000...

More frighteningly, Silicon Valley Bank could be the first domino to fall, potentially triggering a crisis that affects not only other U.S. banks but also tech startups across Silicon Valley.

So what exactly happened?

Today, we’ll tell the story of how a bank goes bankrupt.

Understanding the Banking Business Model

First, we need to understand how banks operate.

Simply put, a commercial bank is a company that trades money. The banking business model is fundamentally no different from any other business—it's about buying low and selling high, except the product here is money itself.

Banks collect money from depositors or capital markets and lend it to borrowers, profiting from the interest rate spread.

For example: a bank borrows money from depositors at a 2% annual interest rate and lends it out at 6%, earning a 4% net interest margin. This difference constitutes its net interest income. Additionally, banks earn revenue from fee-based services and other operations—this is non-interest income. Net interest income plus non-interest income equals a bank’s total net revenue.

Therefore, just like any retail business aiming to avoid inventory buildup, banks aim to lend out every dollar they take in at low cost. After all, deposits aren’t free—they require interest payments to depositors.

This structure defines both sides of a bank’s balance sheet.

Equity + Liabilities: Equity refers to shareholders’ capital; customer deposits are liabilities because they represent money borrowed from clients. For banks, more deposits are better—as long as the funding cost remains low. Banks like Silvergate, which cater specifically to crypto firms, attracted large inflows from major crypto companies by offering unique services such as the SEN network.

Assets: Loans made to customers become the bank’s receivables—its assets—including mortgage loans, consumer credit, government bonds, municipal bonds, mortgage-backed securities (MBS), and high-grade corporate bonds.

Then how does such a seemingly simple business model lead to bankruptcy?

When a bank faces crisis, it means problems have emerged on its balance sheet, typically falling into two categories: bad loans (credit risk) or maturity mismatches (liquidity risk).

Bad Loans (Credit Risk): Normally, banks profit by collecting repayments. If loans or purchased bonds turn out to be junk assets with widespread defaults, the bank suffers real losses. Lehman Brothers collapsed during the subprime crisis precisely because its balance sheet was weighed down by massive non-performing loans, where asset losses far exceeded shareholder equity—leading to insolvency.

Maturity Mismatch: When asset durations don't align with liability durations—commonly known as “short-term deposits funding long-term loans,” i.e., short-term funding used for long-term investments.

For instance, suppose your rent is due on the 1st, but your only cash inflow comes from your salary on the 10th—you face a timing mismatch, also known as a liquidity crunch. What do you do? Either sell some assets (stocks, funds, cryptocurrencies) for cash, or borrow from friends to get through the month.

Returning to Silvergate and Silicon Valley Bank, maturity mismatch is precisely why they fell into crisis.

It’s not just these two banks—even crypto unicorns like Celsius, Bitmain, and AEX previously collapsed due to liquidity crises caused by maturity mismatches.

Ultimately, all these cases trace back to the Federal Reserve’s rate hikes—they are all casualties of the dollar cycle.

How Did Silvergate Go Bankrupt?

Founded in 1986, Silvergate Capital Corp (stock code: SI) was a community retail bank based in California that remained obscure for decades until Alan Lane decided to enter the crypto industry in 2013.

Silvergate Bank positioned itself as a crypto-friendly institution—not only accepting deposits from crypto exchanges and traders, but also building its own payment settlement network called the Silvergate Exchange Network (SEN), facilitating seamless fiat-to-crypto on-ramps and off-ramps. It became a crucial bridge between traditional finance and crypto—for example, FTX relied heavily on SEN for fiat deposits and withdrawals.

As of December 2022, Silvergate had 1,620 clients, including 104 exchanges.

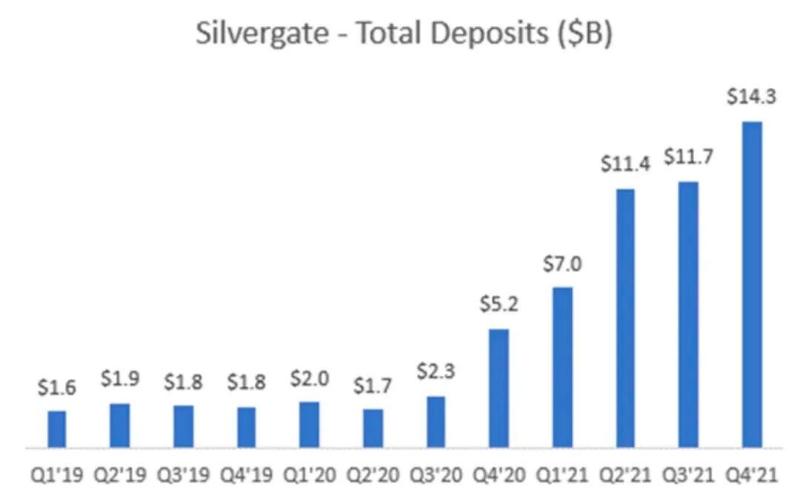

During the crypto bull run, massive inflows poured in, especially since the existence of SEN meant exchange funds were effectively locked within Silvergate.

From Q3 2020 to Q4 2021, Silvergate’s deposits surged from $2.3 billion to $14.3 billion—an almost sevenfold increase.

The surge in deposits—driven by crypto-friendliness and the bull market—forced the bank to deploy capital quickly. Since loan origination was neither fast nor Silvergate’s core competency, it opted instead to purchase billions of dollars in long-dated municipal bonds and mortgage-backed securities (MBS) throughout 2021.

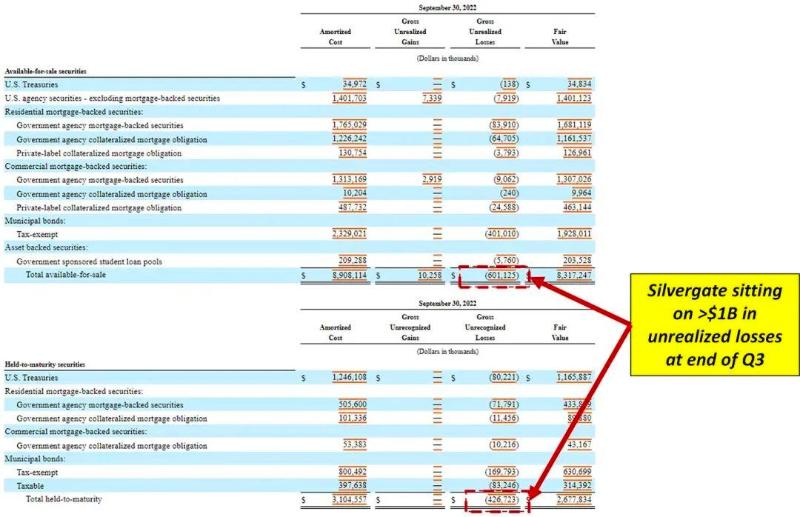

By September 30, 2022, the company’s balance sheet showed approximately $11.4 billion in bond holdings, compared to just $1.4 billion in loans. Thus, Silvergate had essentially become an “investment firm” arbitraging between the crypto world and traditional financial markets: using its banking license and SEN network to gather low-cost—or even zero-interest—deposits from crypto institutions, then investing them in fixed-income instruments to capture the yield spread.

With cheap liabilities paired with high-quality assets, everything seemed perfect—until two black swan events struck in 2022.

In 2022, the Federal Reserve entered a hyper-aggressive rate-hiking phase, causing interest rates to soar—and bond prices to plunge.

There's a fundamental equation in finance: today’s price × interest rate = future cash flow. Bonds have fixed repayment terms—their future cash flows are set—so when interest rates rise, today’s price must fall accordingly.

By the end of Q3 2022, unrealized losses on Silvergate’s securities portfolio had already exceeded $1 billion.

Additionally, during the height of the crypto boom, flush-with-cash Silvergate acquired Facebook’s failed stablecoin project Diem in early 2022 for nearly $200 million in cash and stock. By January 2023, Silvergate disclosed a $196 million impairment charge, writing down the value of intellectual property and technology acquired from Diem Group—effectively meaning the entire $200 million investment was completely wiped out.

In summary, Silvergate bought too many overvalued assets at the peak of the bubble. Yet even then, if liabilities hadn’t unraveled, it might have survived. But unfortunately, its biggest client, FTX, imploded.

In November 2022, FTX declared bankruptcy. Amid panic, Silvergate’s depositors began mass withdrawals.

In Q4 2022 alone, deposits dropped by 68%, with over $8 billion withdrawn—a classic case of bank run.

Faced with a liquidity crisis, Silvergate had no choice but to either borrow or sell assets to meet redemption demands.

First, it was forced to sell high-priced securities acquired earlier in Q4 2022 and January 2023, resulting in roughly $900 million in realized losses—about 70% of its shareholder equity.

It also borrowed $4.3 billion from the Federal Home Loan Bank of San Francisco—a government-chartered institution that provides short-term secured loans to banks in need of liquidity.

Eventually, as we now know, on March 9, Silvergate announced it could no longer continue operations and would voluntarily wind down in an orderly manner under regulatory supervision, promising full repayment of all deposits.

The Silicon Valley Bank Crisis

If you’ve understood Silvergate’s downfall, then SVB’s liquidity crisis follows nearly the same pattern—except SVB is much larger and more influential.

Silicon Valley Bank has long been one of the most popular financial institutions among tech and life sciences startups in Silicon Valley. If SVB collapses, it will inevitably impact countless startups, sparking a dual crisis in both technology and finance.

The trigger was SVB’s fire-sale disposal of $21 billion in bonds, incurring an $1.8 billion actual loss. In response, SVB said it would raise $2.3 billion through a stock offering to cover the shortfall.

This move terrified venture capital firms across Silicon Valley.

Peter Thiel’s Founders Fund directly advised its portfolio companies to pull funds from SVB; Union Square Ventures told its startups to “keep minimal cash in SVB accounts”;

Y Combinator CEO Garry Tan warned portfolio startups that SVB’s solvency risk was real and suggested limiting exposure to lenders—ideally below $250,000;

Tribe Capital advised its portfolio companies that if they couldn’t fully withdraw from SVB, they should at least remove part of their funds.

Thus, a bank run ensued, pushing SVB deeper into a liquidity crisis.

Let’s examine its assets and liabilities.

Liabilities: Previously, with low market interest rates, SVB attracted massive deposits at a mere 0.25% interest rate. Combined with strong performance in tech venture capital and IPO markets in recent years, SVB’s liabilities grew rapidly—from $61.76 billion in 2019 to $189.2 billion by the end of 2021.

However, today’s tech VC market has cooled significantly—especially the IPO market, which has been sluggish over the past year. SVB’s deposits have been steadily declining. Moreover, for depositors, buying U.S. Treasuries directly now offers better returns.

Assets: Like Silvergate, faced with abundant deposits but limited capacity to deploy them via traditional lending, SVB also invested heavily in bonds such as MBS—but not modestly. It went all-in.

When interest rates were low, most large U.S. banks kept deposits in safer government debt despite lower yields. SVB, however, bet that rates would stay low indefinitely and allocated most of its deposits into higher-yielding MBS for greater returns.

By the end of 2022, SVB held $120 billion in investment securities, including a $91 billion MBS portfolio—far exceeding its $74 billion in total loans.

According to public disclosures, the $21 billion bond portfolio SVB sold had a yield of 1.79% and a duration of 3.6 years. Compare this to the 4.4% yield on 3-year U.S. Treasuries on March 10.

As interest rates soared, bond prices crashed—leading to massive paper losses for SVB.

SVB holds $91 billion in held-to-maturity bond portfolios, now valued at just $76 billion in the market—representing $15 billion in unrealized losses.

Greg Becker, CEO of SVB, admitted in a media interview: “We expected rates to rise, but not to this extent.”

In essence, both Silvergate and SVB were caught off guard by the pace of Fed rate hikes, leading to flawed investment decisions. Going all-in on bonds felt great at the time—but paying the price under rising dollar rates proved unbearable.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News