Crypto-friendly banks vanish within a week—how can the crypto industry alleviate the liquidity crisis?

TechFlow Selected TechFlow Selected

Crypto-friendly banks vanish within a week—how can the crypto industry alleviate the liquidity crisis?

The future will undoubtedly give birth to fully decentralized banks. In Trustless we Trust.

Silvergate and SVB Bring Down the Crypto Industry

After a turbulent year, Silvergate Bank, a U.S. cryptocurrency-friendly bank, saw its parent company, Silvergate Capital, announce last Wednesday at market close that it would orderly wind down its banking operations in accordance with regulatory procedures and voluntarily liquidate its banking assets.

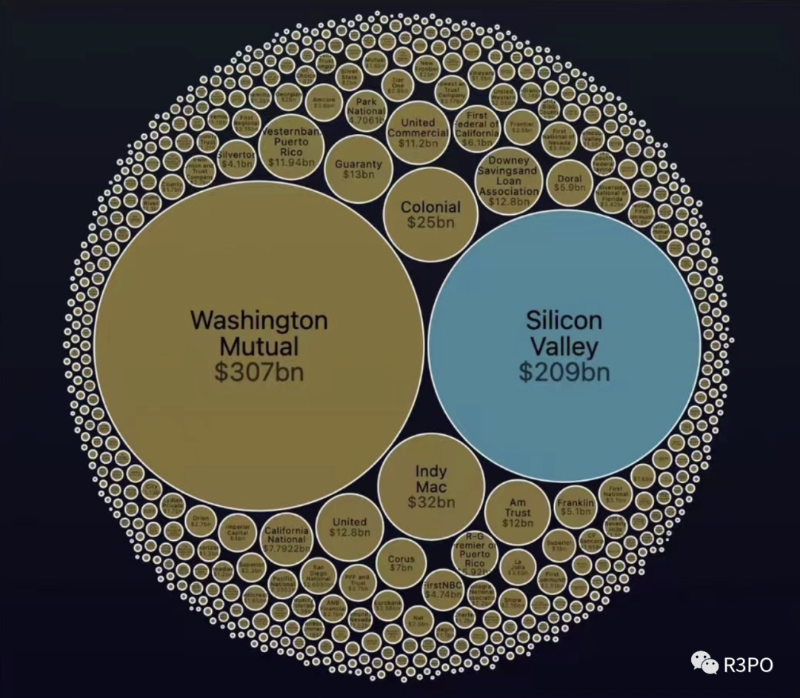

The collapse of Silvergate has spread to more traditional financial institutions, triggering a broader liquidity crisis. On March 8th last week, Silicon Valley Bank (SVB), one of the oldest and most crypto-friendly banks in the United States, announced it was facing financial difficulties. By Friday, the California Department of Financial Protection and Innovation had officially shut down SVB, appointing the Federal Deposit Insurance Corporation (FDIC) as receiver and placing its deposits under control. This marks the formal collapse of the bank—the largest U.S. bank failure since the global financial crisis. Meanwhile, numerous other small and mid-sized banks are also losing ground amid the Federal Reserve's aggressive interest rate hikes.

SVB’s collapse triggered panic among global investors. Many prominent blockchain venture capitalists (VCs) held over $6 billion worth of assets in SVB accounts. Although the U.S. government intervened, guaranteeing depositors full access to their funds, equity and debt holdings in crypto-linked bank entities were nearly wiped out. On November 16, 2022, Block.one and its CEO collectively held approximately 16.8% of Silvergate shares, theoretically suffering investment losses exceeding $70 million on those holdings.

The demise of two federally insured members of the Federal Reserve system—SVB and Silvergate—has triggered cascading effects across the cryptocurrency ecosystem, sparking a crisis of confidence. Uncertainty surrounding Circle’s $3.3 billion in deposits held at SVB caused USDC, the stablecoin issuer, to depeg over the weekend, dropping as low as $0.889.

R3PO analyzed and predicted this scenario in an article from January titled “The Agony of Crypto-Friendly Banks: Silvergate’s Implosion Hurts Abra”, noting that 2023 could mark the end for many more crypto-friendly banks.

Signature Bank—Second Financial Institution Shut Down After Silicon Valley Bank

On Sunday evening, U.S. regulators announced the closure of Signature Bank, a regional bank headquartered in New York. The U.S. Treasury Department, the Federal Reserve, and the FDIC issued a joint statement saying: “We are also announcing a similar systemic risk exception for New York-based Signature Bank, which was closed today by its state chartering authority.”

Despite having proactively reduced its exposure to the cryptocurrency market, Signature Bank still could not escape collapse. As of February 1, 2023, it ceased supporting any crypto exchange transactions under $100,000—applying this policy uniformly across all exchanges. This move underscored Signature Bank’s determination to reduce risks tied to crypto assets, limiting services for Binance only to transactions exceeding $100,000. In December 2022, following the FTX collapse, the bank stated it was broadly retreating from the crypto sector and intended to reduce up to $10 billion in customer deposits related to crypto assets. On March 2, in its quarterly report, Signature Bank reiterated that it currently makes no loans against crypto collateral, holds no investments in digital assets, and provides no custody services for clients’ digital assets.

So why was Signature Bank still shut down by regulators? According to The Wall Street Journal, as early as January, the Federal Home Loan Bank System (FHLB) provided over $13 billion in loans to the two largest crypto-focused banks—Signature Bank and Silvergate—to mitigate liquidity pressures caused by surging withdrawals. Notably, nearly $10 billion of that amount went to Signature Bank in the final quarter of 2022 alone, marking one of the largest borrowing deals in recent banking history. Additionally, Silvergate received at least $3.6 billion in loans from FHLB. This indicates that the liquidity crisis at these prominent crypto-friendly banks had already begun emerging after the FTX implosion.

Cryptocurrency Industry Plunged into Fiat Liquidity Crisis

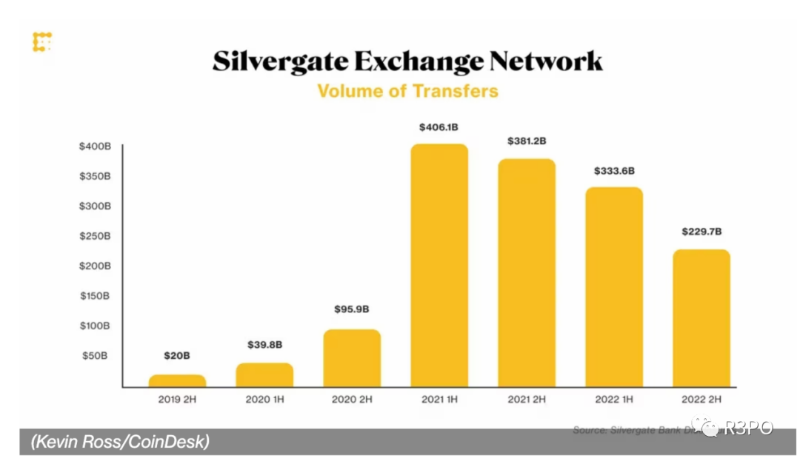

A critical point worth emphasizing is the Silvergate Exchange Network (SEN), which played a pivotal role in facilitating off-blockchain fund transfers between major investors and cryptocurrency exchanges. Launched by Silvergate in 2018, SEN was rapidly adopted, processing nearly $800 billion in transaction volume throughout 2021. Almost every major U.S.-based cryptocurrency exchange became a client of Silvergate and began using this network for fund transfers. For crypto traders, the technology appeared game-changing—a seamless bridge between traditional finance and the crypto ecosystem.

With Silvergate entering voluntary liquidation last week, JPMorgan had predicted clients would migrate to Signature Bank’s Signet payment network. Crypto companies can integrate the Signet network into their platforms via application programming interfaces (APIs). However, Signature Bank is now also struggling to survive.

When USDC—one of the foundational asset pricing infrastructures in the crypto industry—experiences depegging, it once again reveals the fragility of stablecoins. When people realize that decentralized finance remains vulnerable to centralized financial conditions and can lose value, they may shift toward greater demand for fiat currency. But with the crypto industry losing both Signature and Silvergate—its two primary crypto-friendly banks—crypto firms have lost key channels for accessing fiat money. Crypto companies now face extremely limited options for fiat deposits and withdrawals, and any new crypto startup will find it exceptionally difficult to open new bank accounts. Until new banks step in, fiat-to-crypto liquidity will remain severely constrained.

R3PO believes that as nascent infrastructure for the crypto market, blockchain transaction networks hold immense core value. The shutdown of platforms like SEN and Signet will undoubtedly further damage the already strained liquidity in the crypto market. However, for competing banks, this presents a potential opportunity—to swiftly enter the space, fill the void, and gain leadership in crypto-related banking services. Currently, the only remaining crypto-friendly banks in the U.S. are Customers Bank and Sygnum, with Seba Bank, Deletc Bank, and BCB operating in other regions.

Crypto Industry Responds with Self-Help Measures—Opportunities Amid Crisis

Circle, at the center of public attention, released a statement today: “Our 100% deposits held at SVB are safe, and we will resume normal business tomorrow. 100% of USDC reserves remain secure and reliable. We are completing the transfer of remaining cash from SVB to BNY Mellon. As previously stated, USDC liquidity operations will resume when banks reopen tomorrow morning. Following tonight’s announcement of Signature Bank’s closure, we will no longer process mints and redemptions via SigNet and will instead rely on settlement through BNY Mellon. We expect to onboard a new transaction banking partner with automated minting and redemption capabilities as early as tomorrow. We are committed to building robust and automated USDC settlement and reserve operations with the highest standards of quality and transparency.”

Coinbase issued a statement saying: “Despite recent turbulence in traditional banking, Coinbase continues to operate normally. All customer funds remain secure and accessible, including USDC conversions set to resume on Monday. Cash held on behalf of customers in banks remains protected by FDIC pass-through insurance. Due to the FDIC’s suspension of Signature’s transactions, we are currently facilitating cash transactions for all customers through alternative banking partners.”

Although the closures of Silvergate and Signature Bank have regressed the crypto capital market to pre-2014 conditions—where newly established companies have no chance of securing banking relationships—cryptocurrencies have effectively become unbanked. However, regulatory failures and financial crises within centralized financial institutions will stimulate greater reliance and faith among crypto-native capital in native crypto assets such as Bitcoin. In the future, the blockchain industry will likely reduce its dependence on USD-pegged stablecoins, expand the universality and stability of blockchain payment networks, and increase direct use cases for cryptocurrency payments—thereby reducing reliance on centralized financial institutions. R3PO firmly believes that fully decentralized banks will eventually emerge. In Trustless we Trust.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News