Polygon — The relentless industry leader pushing forward

TechFlow Selected TechFlow Selected

Polygon — The relentless industry leader pushing forward

Among all public blockchains, Layer 1s (base layer networks), and Layer 2s (scaling solutions built on top of base layers), Polygon stands out as a well-rounded contender, capable of competing across the board while also possessing unique killer features of its own.

Authors: JX (Partner of OFR), Nicole Cheng (Investment Director of OFR)

Research Support: Alastair (Analyst of OFR), Otto Verstl (Analyst of OFR)

Special thanks to community volunteers @Jessicashen6699 and @Pupig_Lily for translation support

Among all public blockchains, Layer 1s (base-layer blockchains) and Layer 2s (scaling solutions built atop base layers), Polygon stands out as a well-rounded contender—competitive across multiple dimensions while possessing unique killer advantages.

Polygon’s price, market cap, and trading volume from beginning of year

Project Rating: Outperforming the Market

Target Price: Y2023: $3.8, Y2024: $7.2 USD to $23.98 USD

Key Conclusions:

Securing a Leading Position Through Strategic Acquisitions

Polygon has assembled a comprehensive suite of zero-knowledge (ZK) proof and data availability (DA) solutions. This not only validates their strategic vision in using native tokens for acquisitions during the last bull market but also establishes deep moats at the infrastructure level.Hosting Innovative DeFi Products

Polygon's stable DeFi ecosystem lays a solid foundation for its identity as a "financial network layer." However, compared to other Layer 2s and Ethereum-killer Alt Layers, it needs more innovative DeFi products to drive higher transaction volumes and liquidity.Building an All-Star NFT Lineup

After successfully launching NFTs for major traditional brands such as Reddit, Starbucks, and Meta, Polygon has become the go-to platform for brands targeting young, fashion-forward Web3 users.Preparing for the Next Wave of GameFi

Having experienced multiple gaming booms during the 2020–2021 bull markets, Polygon has accumulated a large base of active GameFi users. Polygon Studio will continue to invest and build actively, contributing to the broader Polygon ecosystem.

Risk Warnings: Macro market risks, competitive risks, price volatility risks

Table of Contents

1. Betting It All on the “Endgame” — Polygon’s Zero-Knowledge Proof Strategy

1.1 Chasing the Holy Grail of zkEVM

1.2 Synergies Across the ZK Suite

Polygon’s ZK scaling products are neither mutually exclusive nor independently developed. Instead, each contributes core innovations that collectively form Polygon’s ZK-powered “zkVerse.”

1.3 Achieving Ethereum Data Availability

2. Aggressive Ecosystem Development Propels Mainstream Adoption

2.1 DeFi: Solid Performance, But Needs More Innovation

2.2 NFT: Premium Brands Lead the Way

2.3 GameFi: Riding the Cycles with Momentum

3. Valuation

3.1 Token Supply and Distribution

3.2 Token Utility

3.3 Valuation — EPT Analysis (Average Token Earnings Method)

3.4 Valuation — Comparable Analysis

3.5 Valuation — Post-ZK-EVM Mainnet Launch

4. Risks

1. Betting It All on the “Endgame” — Polygon’s Zero-Knowledge Proof Strategy

As described by Ethereum co-founder Vitalik Buterin in his article “Endgame,” after announcing a $1 billion treasury fund dedicated to ZK projects, Polygon acquired three teams pursuing different technical approaches to Ethereum scalability. By aligning closely with dominant crypto narratives, Polygon made a strategic bet on ZK-rollups.

This strategic move alleviated market skepticism about Polygon being merely a PoS sidechain (its current mainchain choice) and laid the groundwork for future narratives around blockchain tech stacks. The ambition and foresight demonstrated by the Polygon team are admirable—far more rational than players who misuse funds lobbying politicians or leveraged bets on illiquid assets.

Figure 1. Polygon’s In-Development ZK Scaling Solutions (Source: Old Fashion Research, Polygon)

Within Polygon’s ZK scaling portfolio, Polygon zkEVM (formerly Polygon Hermez) stands out as the flagship product, so we begin our analysis there.

This year, fierce competition among Scroll, Matter Labs, and Polygon reflects every project’s desire to be the “first” to launch a zkEVM product and capture first-mover advantage.

1.1 Chasing the Holy Grail of zkEVM

Developing zkEVM is extremely difficult but widely seen as essential infrastructure for scalable, low-cost blockchains. Only a handful of teams (as listed above) lead in this space—making it a focal point for capital markets, which assign higher valuations accordingly.

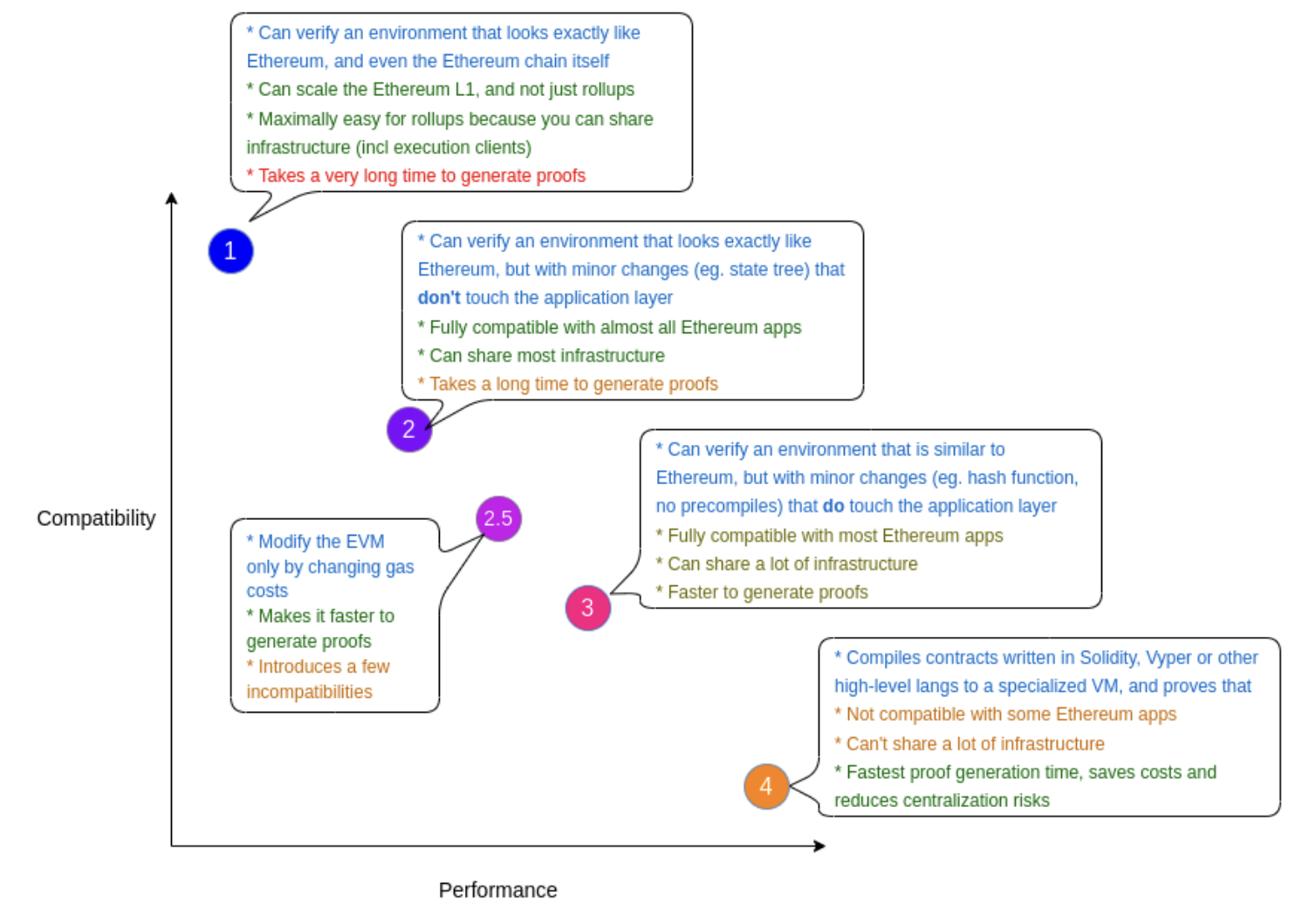

Vitalik categorizes zkEVM projects into four types based on trade-offs between compatibility, efficiency, and native integration.

Figure 2. Different Types of ZK-EVM Projects (Source: Old Fashion Research, Vitalik.ca)

Polygon zkEVM currently falls under Type 3, meaning it maintains high compatibility with most Ethereum applications. If no precompiles are required, developers don’t need to rewrite code for zkEVM adaptation.

Type 3 zkEVM isn’t Polygon zkEVM’s ultimate goal—compatibility can still improve. Considering performance trade-offs, Polygon aims to evolve toward Type 2 architecture: fully equivalent to Ethereum at the Virtual Machine level (“fully EVM-equivalent”).

In this setup, existing EVM applications will be fully compatible with Polygon zkEVM with minimal modifications. Current EVM developer tools (like debuggers) will also work seamlessly on Polygon zkEVM.

Like any infrastructure evolution, choosing a specific zkEVM path involves no absolute advantages or disadvantages. However, we believe Polygon’s approach is the most practical and best-suited for building its ecosystem among all peers:

Type 2 zkEVM prioritizes compatibility over some performance loss. Given Polygon’s extensive developer network on its current PoS sidechain, this maximizes absorption of EVM developers.

Performance gaps can be mitigated using enhanced proving systems developed by Polygon Zero (details later).

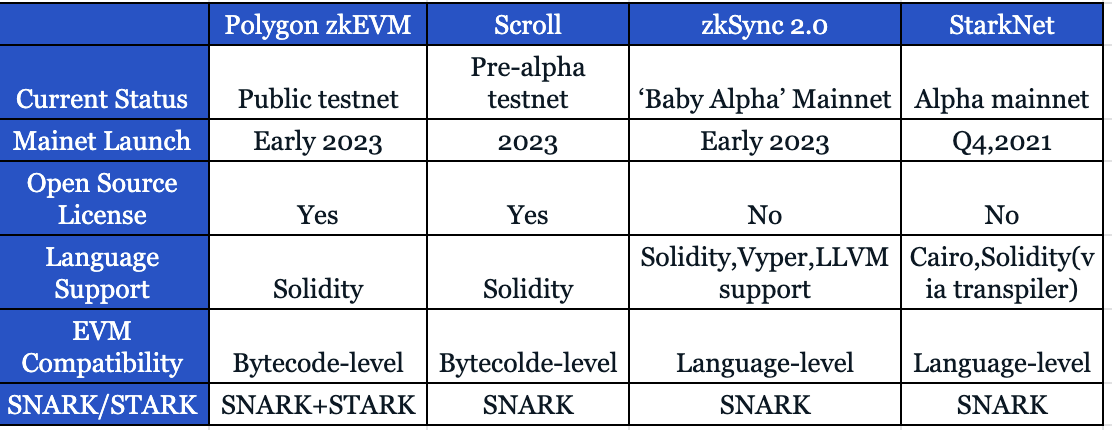

The current competitive landscape favors Polygon zkEVM—its rivals either have weaker EVM compatibility or less robust developer ecosystems (see Figure 3).

Figure 3. Comparison of zkEVM Solutions (Source: Old Fashion Research, Polygon, Scroll, Matter Labs, Starkware)

1.2 Synergies Across the ZK Suite

Polygon’s ZK scaling products do not compete with one another nor develop in isolation. Rather, each brings key innovations that together form Polygon’s ZK-centric “zkVerse.”

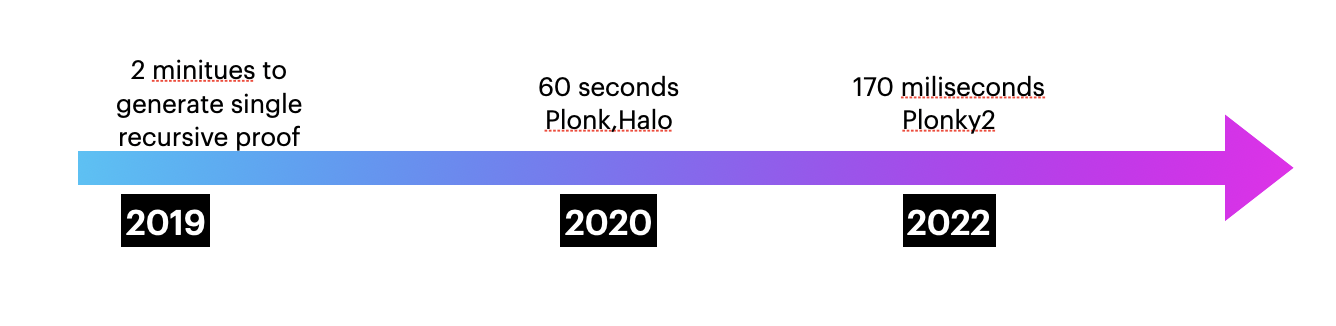

Polygon Zero, formerly Mir Protocol, announced Plonky2—its latest recursive zero-knowledge proof system—before being acquired by Polygon in 2021. Plonky2 generates zero-knowledge proofs (ZKPs) and achieved recursive proof generation in under 170 milliseconds on a 2021 MacBook Pro.

Figure 4. Polygon Zero Team Improved zk-prover Performance Over 700x in Three Years (Source: Old Fashion Research, Polygon Zero)

Interestingly, because Plonky2 uses FRI instead of the more common KZG as its commitment scheme, it achieves greater Ethereum compatibility—but must make certain trade-offs: either accept larger proof sizes for faster generation or maintain smaller proofs at the cost of longer generation times.

Plonky2 uses larger proofs when speed matters and smaller ones when size is critical. Assuming it opts for faster generation with larger proofs, this would require ~1 million gas (a significant cost).

However, this cost mainly stems from CALLDATA expenses when publishing proofs on Ethereum. If CALLDATA costs are repriced via EIP-4488, Plonky2 verification costs could drop to between 170k–200k gas—a reasonable range—and imply that Plonky2 gains clear cost advantages post-EIP-4488 implementation, in addition to superior proving speed.

Polygon Miden, a STARK-based Ethereum-compatible rollup solution, fills a missing piece in Polygon’s ZK-Rollup roadmap. In short, zk-STARK rollups offer advantages over zk-SNARK counterparts due to post-quantum cryptographic security and trustless setups, though they face challenges in scalability due to larger ZKP sizes.

True to its core philosophy across all products, Polygon takes a pragmatic approach to ZK-Rollup development—establishing Polygon zkEVM (a zk-SNARK rollup) as the flagship while implementing STARKs for recursive proofs like FRI.

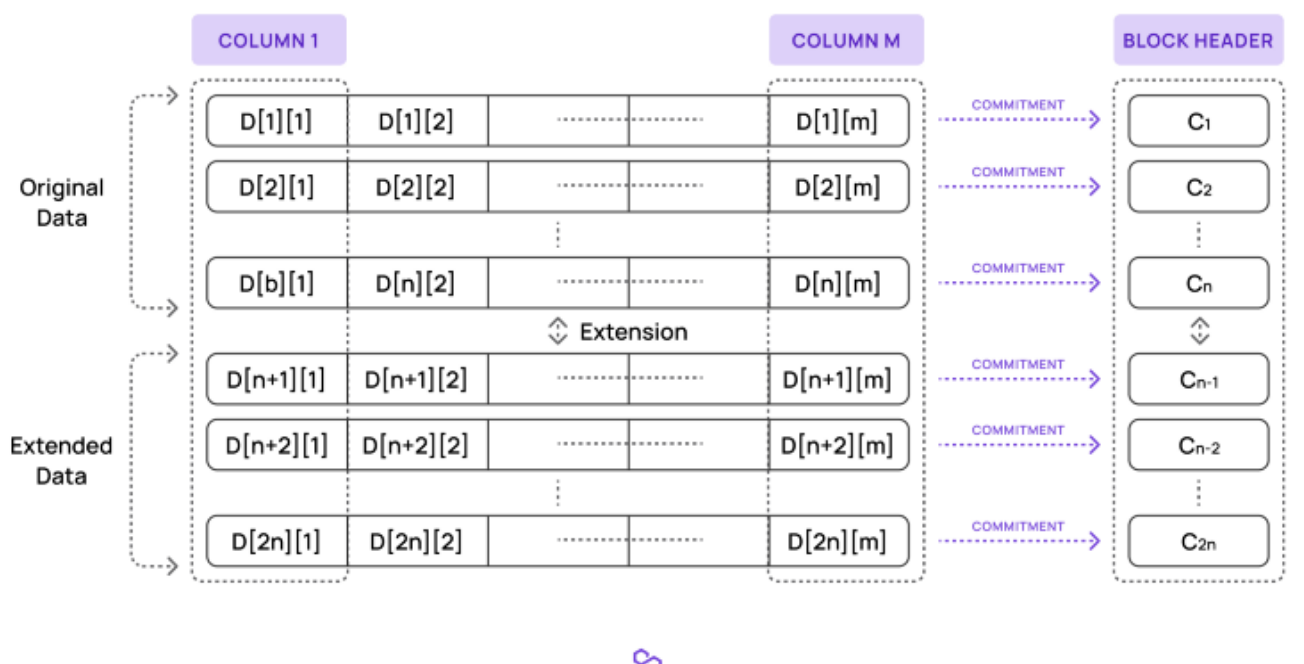

1.3 Achieving Ethereum Data Availability

While data availability has long been debated within the Ethereum community, few solutions have proven reliable—including Polygon Avail.

The key technical challenge lies in verifying that blockchain transaction data hasn't been manipulated by block producers or rollup sequencers, without requiring validators to download entire datasets.

In simple terms, both Polygon Avail and its main competitor Celestia use Data Availability Sampling (DAS) and Erasure Coding to ensure data is thoroughly verified and nearly impossible to maliciously hide.

Figure 5. Polygon Avail’s KZG Commitments (Source: Old Fashion Research, Polygon Avail)

Compared to Celestia, Polygon Avail’s key distinction is its use of KZG commitments—the same method used in Ethereum Danksharding—widely considered cleaner and more efficient than fraud proofs (Celestia’s method) for enforcing correct erasure coding by block producers. Notably, high gas costs for KZG proof verification in EVM will be resolved once EIP-4844 is implemented.

Both Polygon Avail and Celestia embrace the “modular blockchain” concept—offloading data availability functions from monolithic chains like Ethereum onto themselves, allowing base layers to focus on execution or settlement.

Modular architectures rely on native cryptocurrencies for security and stability. Thus, Polygon Avail benefits directly from MATIC token liquidity and value, saving tremendous effort compared to launching an entirely new project.

Summary on Polygon Infrastructure:

Deep Moats Ahead: Each of Polygon’s infrastructure initiatives leads in R&D within their respective domains—all core directions in the crypto industry where only single-digit teams may ultimately succeed.

Synergistic Product Matrix: As shown in the analysis, none of Polygon’s projects grow independently. While maintaining open-source repositories to contribute to the wider crypto community, these products reinforce each other, generating strong synergies.

2. Aggressive Ecosystem Development Propels Mainstream Adoption

2.1 DeFi: Solid Performance, But Needs More Innovation

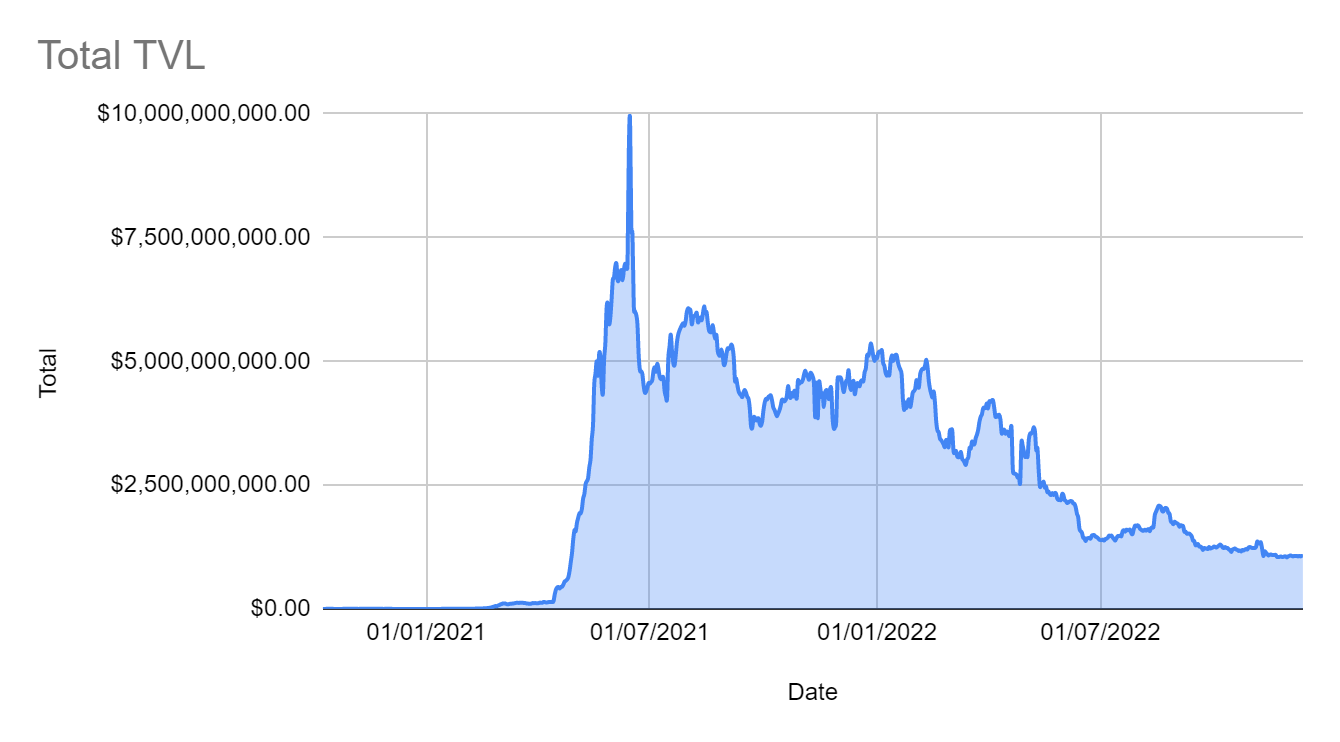

Polygon’s TVL has remained relatively flat since July this year, still holding close to $1.08 billion. Aave accounts for 25% of total TVL, while the top ten protocols collectively hold 70%, including Quickswap, Balancer, Uniswap, Curve, Beefy, Tetu, Klima DAO, SushiSwap, and Stargate Finance.

Figure 6. Polygon TVL Trends (Source: Old Fashion Research, DefiLlama)

At the time of writing, Polygon ranks third in TVL among all blockchains, behind only Ethereum and BSC. However, with Arbitrum and Optimism—two strong competitors—launching liquidity mining campaigns, Polygon saw a -43% quarter-over-quarter decline in TVL. Ironically, liquidity mining was precisely how Polygon initially attracted users during DeFi’s rise.

Figure 7. Polygon Ranks Third Among Major Blockchains in TVL (Source: Old Fashion Research, DefiLlama)

Prior to DeFi Summer, blue-chip Ethereum protocols like Aave, Curve, Sushiswap, and Balancer led the first wave and soon expanded to Polygon to reach broader audiences.

In April 2021, Polygon launched a $DeFiForAll ecosystem fund aimed at supporting and growing its DeFi ecosystem over the next two to three years, allocating 2% of total MATIC supply. Aave’s liquidity miners received 1% of MATIC, while another 1% was shared among 25 other protocols including SushiSwap, Curve, and Balancer.

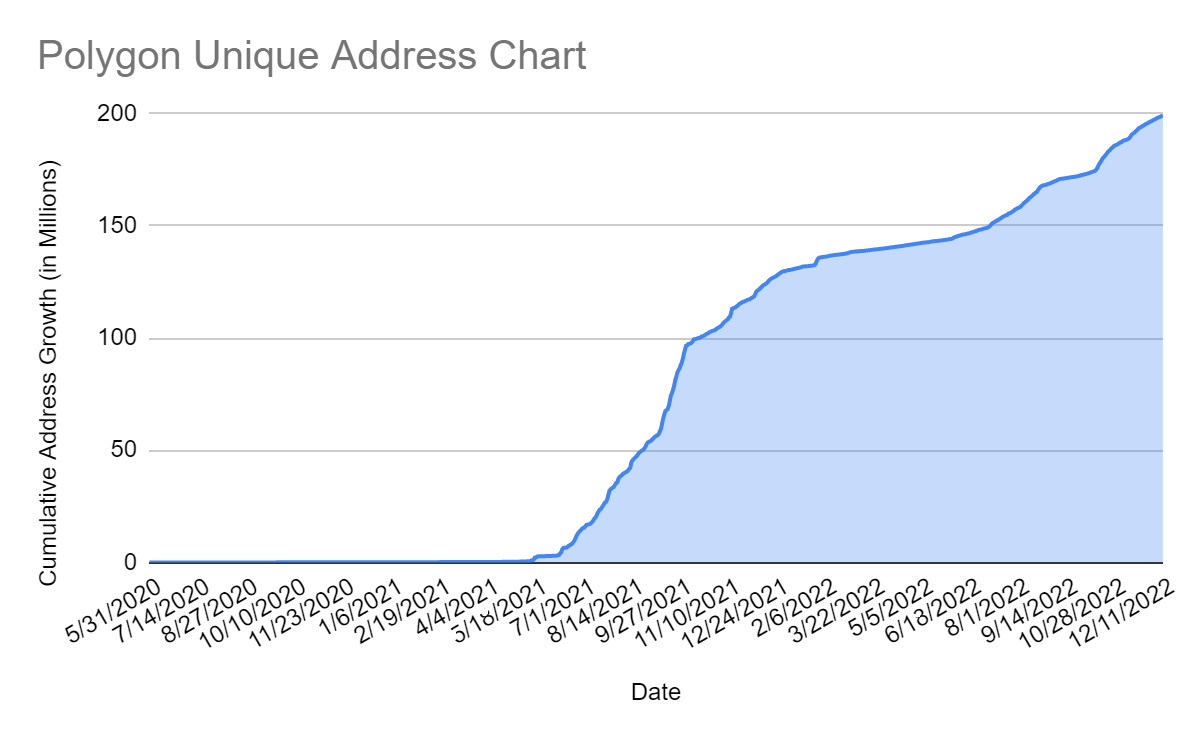

Directly incentivized by liquidity mining, top-tier DeFi app users were motivated to bridge to Polygon. With improved cross-chain bridges enhancing interoperability across chains, Polygon’s protocol TVL rose roughly tenfold within three months of launching incentives. Unique addresses surged 500% over six months—from 200,000 in April 2021 to 100 million by mid-October that year.

Figure 8. Number of Unique Addresses on Polygon (Source: Old Fashion Research, PolygonScan)

Yet successful user acquisition doesn’t guarantee retention. Long-term, growth driven purely by token incentives proves unsustainable—users often act speculatively and lack emotional attachment to the ecosystem. This is reflected in slowing address growth on Polygon after October 2021.

In April 2022, Polygon launched a second round of liquidity mining, now adopting stricter KPI-based criteria. Rewards were distributed weekly based on metrics like active users or TVL. Due to poor market conditions, results were mediocre—confirming earlier concerns about weak user stickiness in Polygon’s DeFi ecosystem, making users prone to chasing higher yields elsewhere.

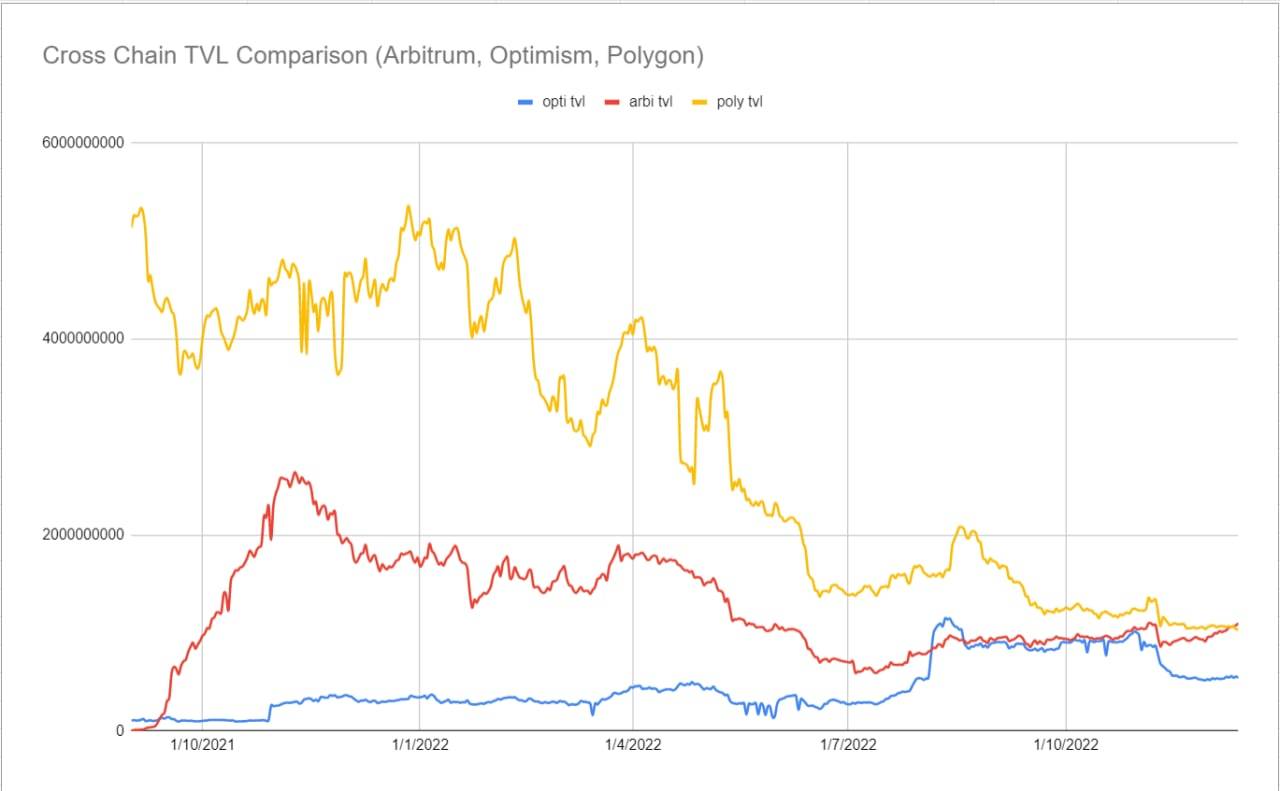

Figure 9. Cross-Chain TVL Comparison (Arbitrum, Optimism, Polygon) (Source: Old Fashion Research, DefiLlama)

Like Polygon, Arbitrum and Optimism aim to enhance Ethereum scalability, albeit with varying withdrawal difficulties. Withdrawals on Optimism may take up to 7 days; Arbitrum requires 2 weeks; whereas withdrawals via Polygon’s PoS bridge complete within 3 hours. Although faster withdrawals give Polygon an edge over competing L2s, they also place it at a disadvantage in preventing capital outflows. (Author’s note: One possible interpretation)

When Arbitrum and Optimism launched their own liquidity mining programs, capital began flowing toward these rival scaling solutions. Longer withdrawal periods created friction, inadvertently encouraging users to stay within those ecosystems. As shown in Figure 9, Polygon’s TVL decline coincided with rising TVL on Arbitrum and Optimism.

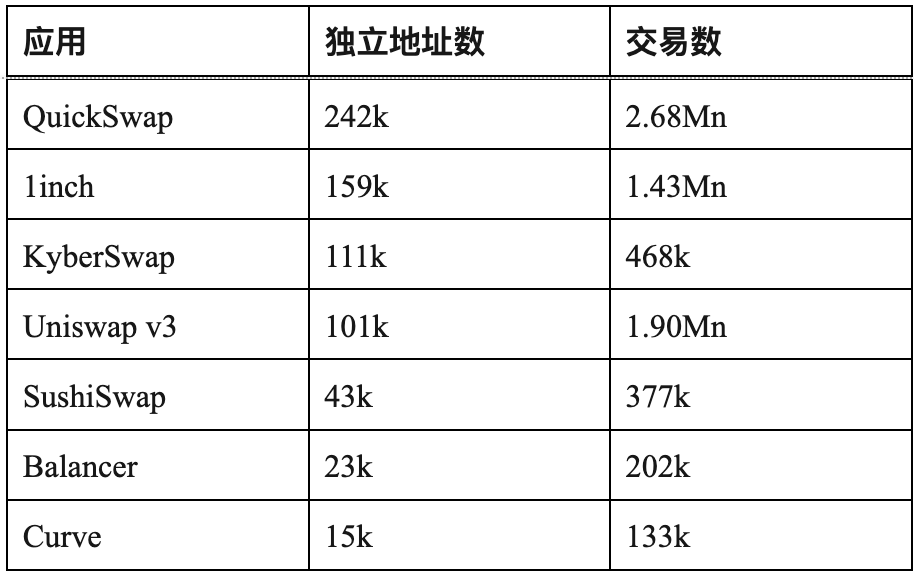

Another key reason is lack of innovation within its DeFi ecosystem. In Q3 2022, top DeFi protocols by unique addresses included QuickSwap, Inch, KyberSwap, Uniswap v3, SushiSwap, Balancer, and Curve. Except for QuickSwap, none are unique to Polygon. On Arbitrum, perpetual futures exchange GMX captured 43% market share and catalyzed an entire ecosystem of derivative DeFi protocols—highlighting the importance of innovation and native protocols to chain growth.

While Polygon’s current DeFi footprint isn’t exceptional compared to NFTs/GameFi, its stable DeFi ecosystem performs adequately, laying a solid financial layer foundation for NFT and gaming value capture. We look forward to seeing how Polygon fosters a tighter-knit, long-term-oriented community to jointly shape its future.

2.2 NFT: Premium Brands Take the Lead

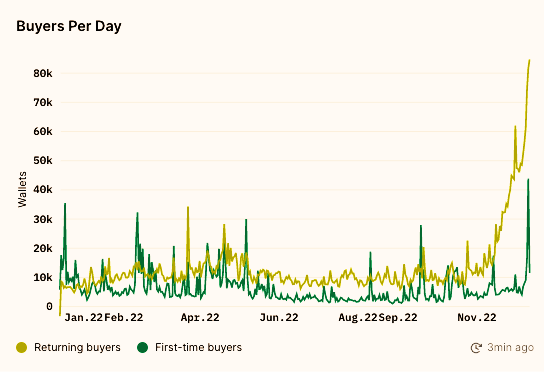

As overall NFT market volume peaked in January 2022, Polygon also hit record highs in weekly NFT buyers—growing from 10,000 in early October to over 120,000 by December. This surge in adoption was largely driven by partnerships with well-known brands, a trend Polygon anticipated early on.

Figure 10. Weekly NFT Buyers on Polygon (Source: Old Fashion Research, Nansen)

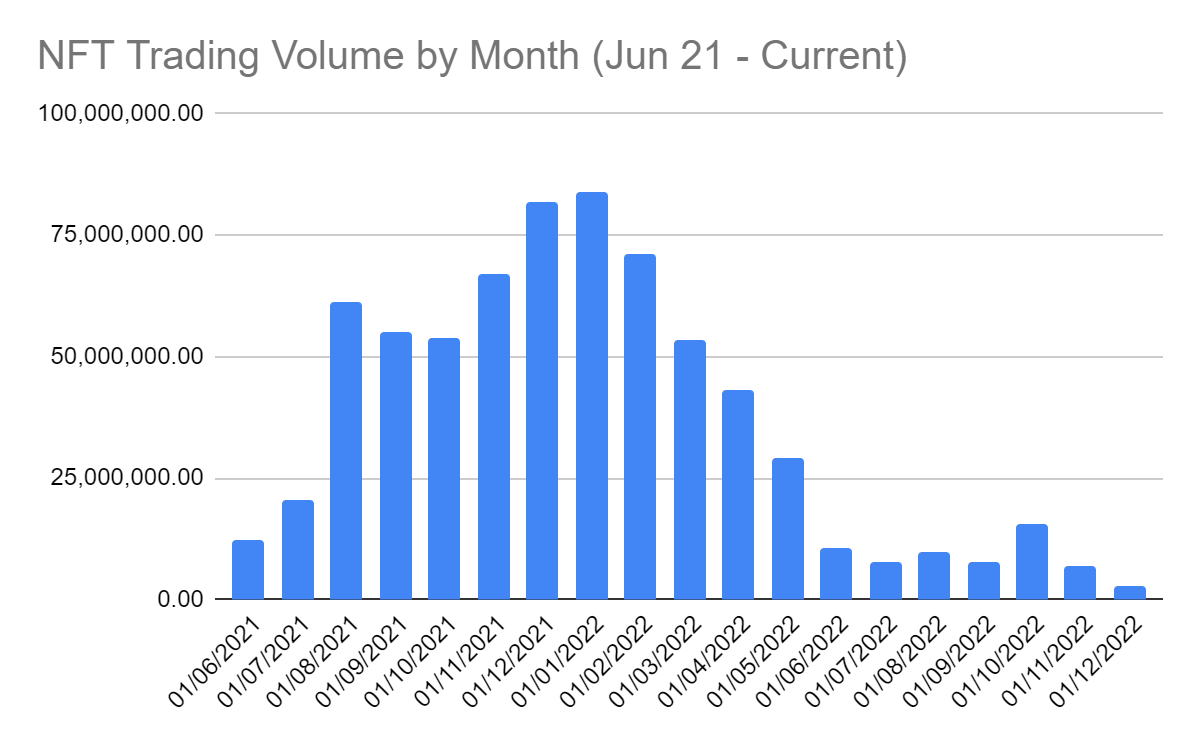

In June 2021, OpenSea added support for Polygon-based NFTs via Seaport, leading to a noticeable increase in listings and sales. Since then, interest in Polygon NFTs grew steadily, featuring popular projects like Aavegotchi, ZED Run, Pegaxy, and Crypto Unicorns. OpenSea’s Polygon NFT trading volume increased sevenfold between June 2021 and January 2022—from $11 million to $79 million.

Figure 11. Historical Record of Polygon NFT Volume on OpenSea (Source: Old Fashion Research, Footprint Analytics)

Nonetheless, besides Ethereum—the most established chain—Polygon faces tough competition from Solana and BSC.

Polygon’s strength lies in Ethereum compatibility and attracting dApps fleeing Ethereum’s high gas fees; BSC benefits from curated projects via Binance Launchpad and Binance NFT, along with easier access to Binance and PancakeSwap. Meanwhile, Solana offers cheaper, faster transactions but requires longer infrastructure buildout due to its Rust-based rather than Solidity-based foundation.

So what distinct positioning and value proposition does Polygon offer in NFTs? Polygon Studio rarely tweets, but in rare posts, it stated Polygon will “become home to top-tier developers, innovators, artists, and investors in the NFT ecosystem, and the preferred platform for IP owners and major Web2 brands entering Web3.” Looking back, Polygon has delivered on this promise.

Starting in 2022, luxury brand Prada and sportswear giant Adidas launched NFT collaborations on Polygon. Beyond consumer-facing brands, Polygon partnered with Adobe Behance. Thanks to Polygon integration, creators can now mint and showcase works directly on Behance.

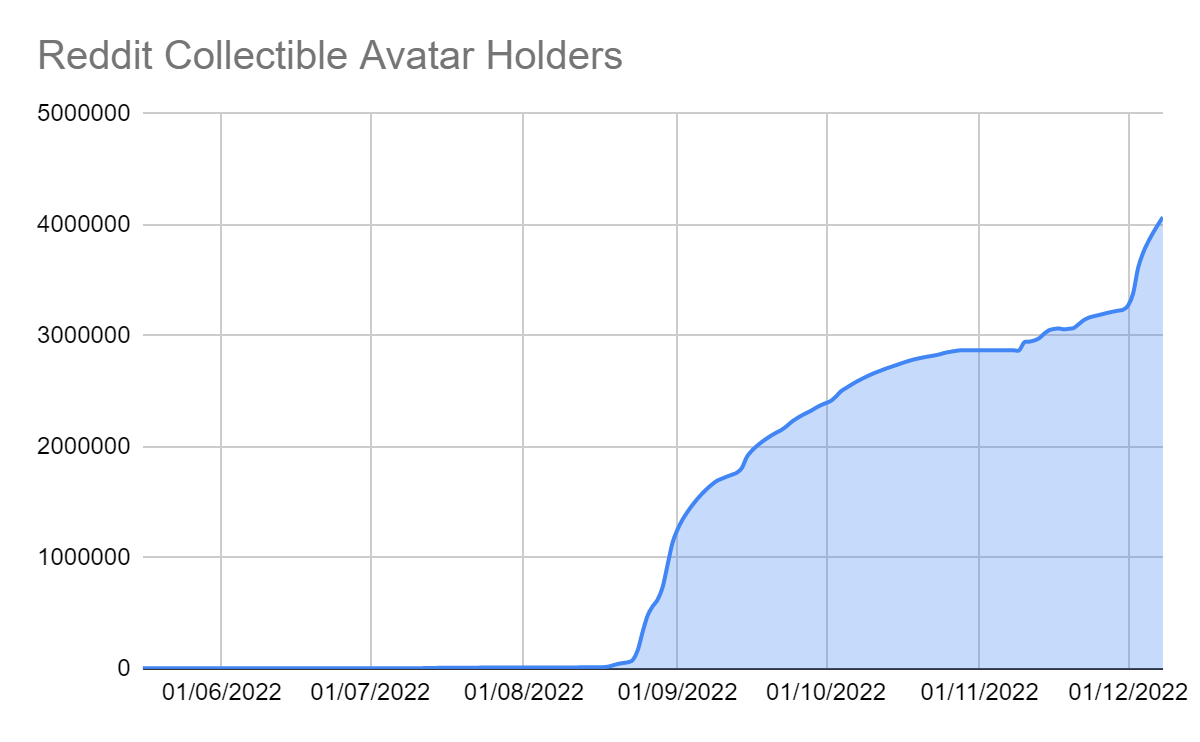

July 2022 was one of Polygon’s busiest months for NFTs. Social media giant Reddit launched a Polygon-based NFT marketplace focused on social avatars. Following the announcement, $MATIC rose 6%, with over 4 million unique Reddit NFT holders and $11 million in total sales.

Figure 12. Historical Count of Reddit Avatar Holders (Source: Old Fashion Research, Dune)

That same month (December), Disney’s 2022 accelerator program chose Polygon again for Web3 development. Days later, Mercedes-Benz selected Polygon to launch its Acentrik data-sharing platform. After two years of development, Acentrik chose Polygon to advance into decentralized exploration.

Then in early August, Coca-Cola released a new NFT on Polygon to celebrate International Friendship Day and mark one year since the brand entered Web3. A month later, California-based fintech firm Robinhood chose Polygon as the first blockchain network for its newly launched Web3 wallet.

Shortly after, in November, Meta revealed Instagram users could mint, display, and sell digital collectibles on Polygon, enabling creators to better engage fan networks and monetize content. Just days before this article was written (December 2022), Starbucks’ Odyssey loyalty rewards program went live, offering users Web3-based NFT collecting experiences. When news first broke in September, $MATIC price rose 3%.

Through these mainstream strategies, Polygon has become the top choice for brands seeking young, trendy Web3 audiences—enabling rapid, low-cost market entry. We expect more such partnerships ahead, further expanding Polygon’s reach beyond the crypto-native audience. We remain bullish on $MATIC long-term, believing breakout success is crucial for mass Web3 adoption.

2.3 GameFi: Riding the Waves of Cyclic Growth

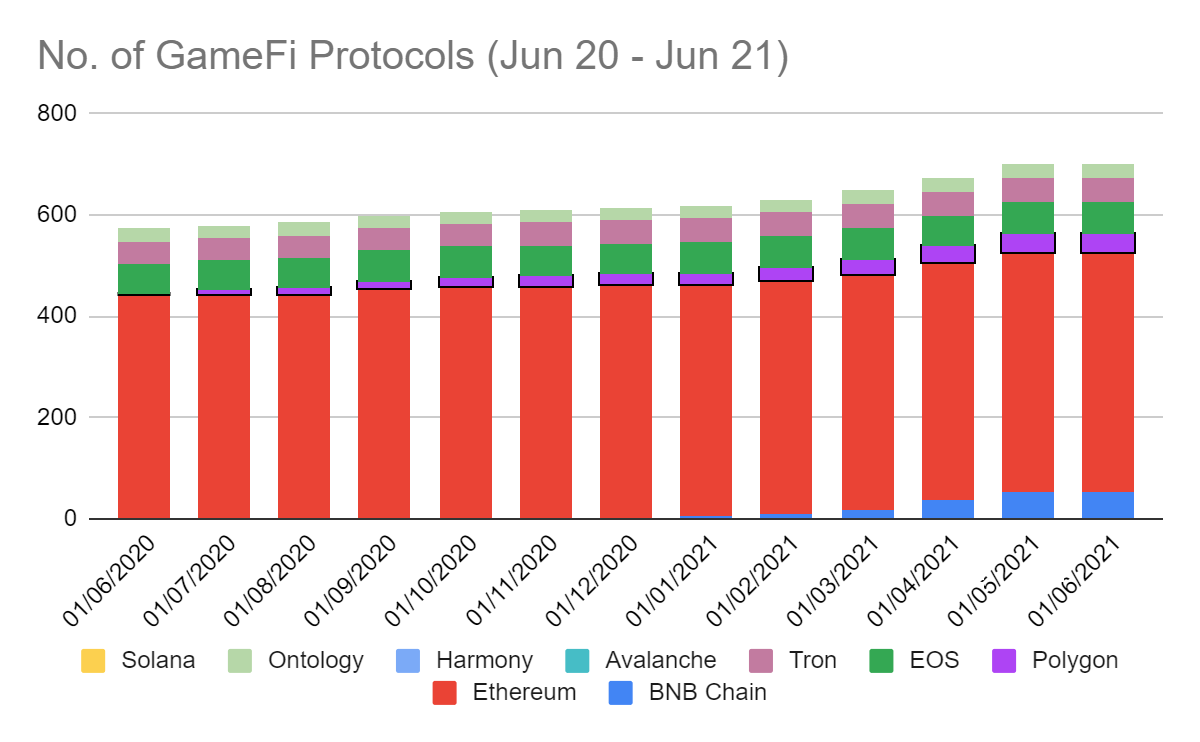

First Wave: The Summer of GameFi

The rise of GameFi caused gas prices on chains like Ethereum to spike, immediately making Polygon’s low fees a standout competitive advantage.

Figure 13. Number of GameFi Protocols (June 2020 – June 2021) (Source: Old Fashion Research, Footprint Analytics)

Similar to Axie Infinity’s explosive growth after launching Ronin, Polygon’s fast, low-cost transactions contrasted sharply with Ethereum’s rising gas fees—especially important in GameFi, where users conduct frequent small transactions, making low cost paramount.

Leveraging these strengths, the number of game protocols on Polygon increased by 50% over the past year, while Ethereum’s count remained nearly unchanged. Still, it faces competition from chains like BNB Chain, whose ecosystem growth is similarly fueled by low transaction fees.

My Crypto Saga, Brave Frontier Heroes, and EmberSword were early examples paving the way for Polygon’s gaming ecosystem.

Second Wave: Launch of Polygon Studios

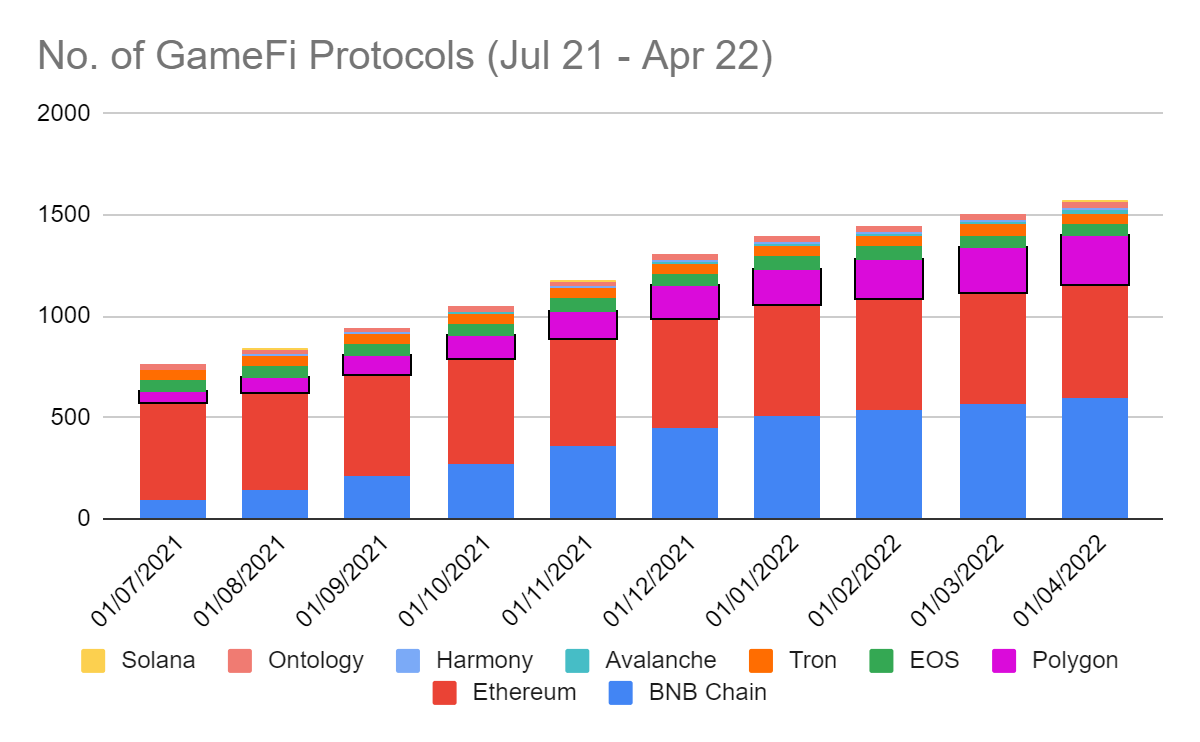

In July 2021, Polygon launched Polygon Studios, reaffirming its strategic focus on gaming: “Game projects will receive full 360-degree development support, big and popular brands can launch games on Polygon, and gamers will enjoy new decentralized gaming experiences.”

Figure 14. Number of GameFi Protocols (July 2021 – April 2022) (Source: Old Fashion Research, Footprint Analytics)

Since Polygon Studios’ inception, the number of gaming protocols on Polygon has surpassed Tron and EOS, ranking third after Ethereum and BNB Chain. Polygon also ranks highly in transaction volume and unique address counts. In July, one of its most popular games, Aavegotchi, attracted over 1,500 users.

Investors have shown strong interest in this sector. For instance, Animoca Brands—with subsidiaries Lympo and Gamee—joined as Polygon Studios partners. Gamee’s mobile game Arc8 on Polygon attracted over 373,000 unique active wallets in one month. Other blockchain games like Zed Run and 0xUniverse further expanded Polygon’s user base.

Beyond individual games, metaverse platforms like The Sandbox have integrated with Polygon, bringing their NFTs and tokens into the ecosystem.

Notably, most games at this stage followed Play-to-Earn models or gamified DeFi, letting users maximize token returns through gameplay. DeFi-related transaction volumes declined concurrently—see DeFi section for details.

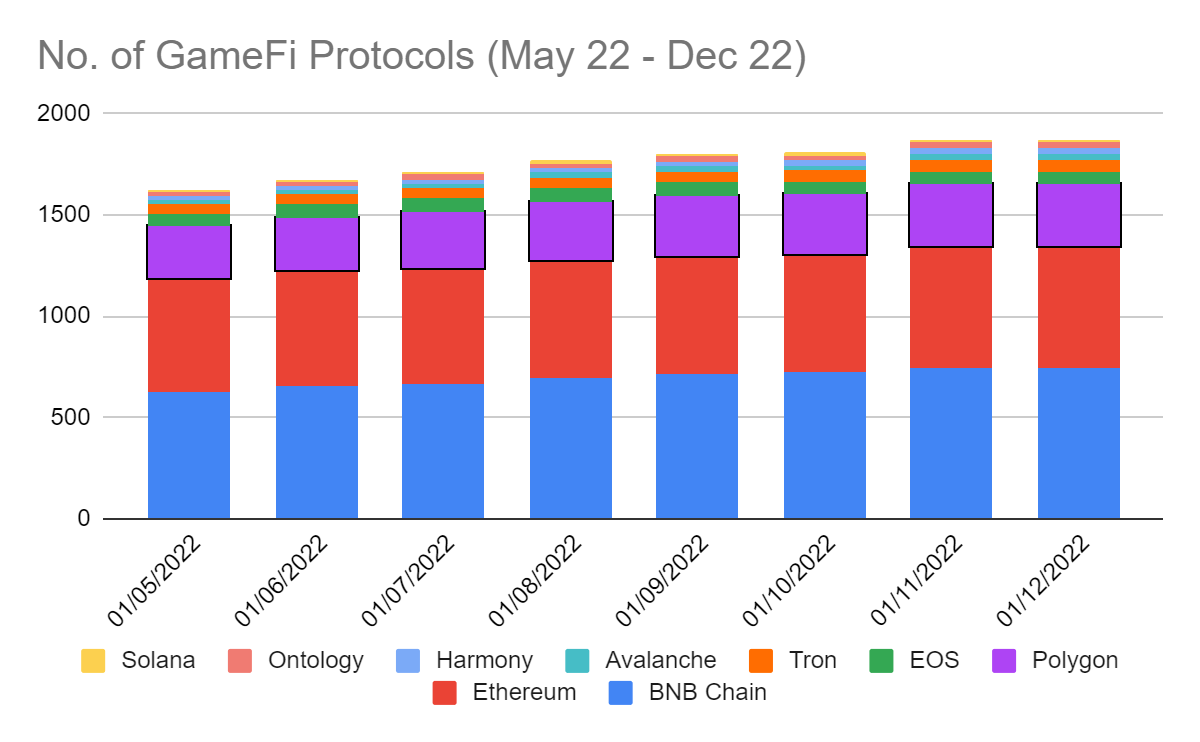

Third Wave: Harvesting Opportunities Amid Terra/Solana Turmoil

The third wave arrived just as Terra collapsed and Solana faltered. Polygon acted decisively, supporting and facilitating migration of promising projects, helping them leverage network effects within its ecosystem.

Earlier this year, the former head of YouTube Gaming joined Polygon Studios, aiming to expand the developer ecosystem through investment, marketing, and dev support—bridging the gap between Web2 and Web3.

In May 2022, the number of GameFi protocols on Polygon exceeded 230. After the UST-LUNA crash, Polygon launched a multi-million dollar Terra Migration Fund to attract suddenly displaced talent. Over 50 projects from the Terra ecosystem migrated to Polygon, including P2E game Derby Stars and GameSwift—an infrastructure platform bridging Web2 and Web3 gaming environments.

Figure 15. Number of GameFi Protocols (May 2021 – December 2022) (Source: Old Fashion Research, Footprint Analytics)

Current State of Polygon’s Gaming Ecosystem

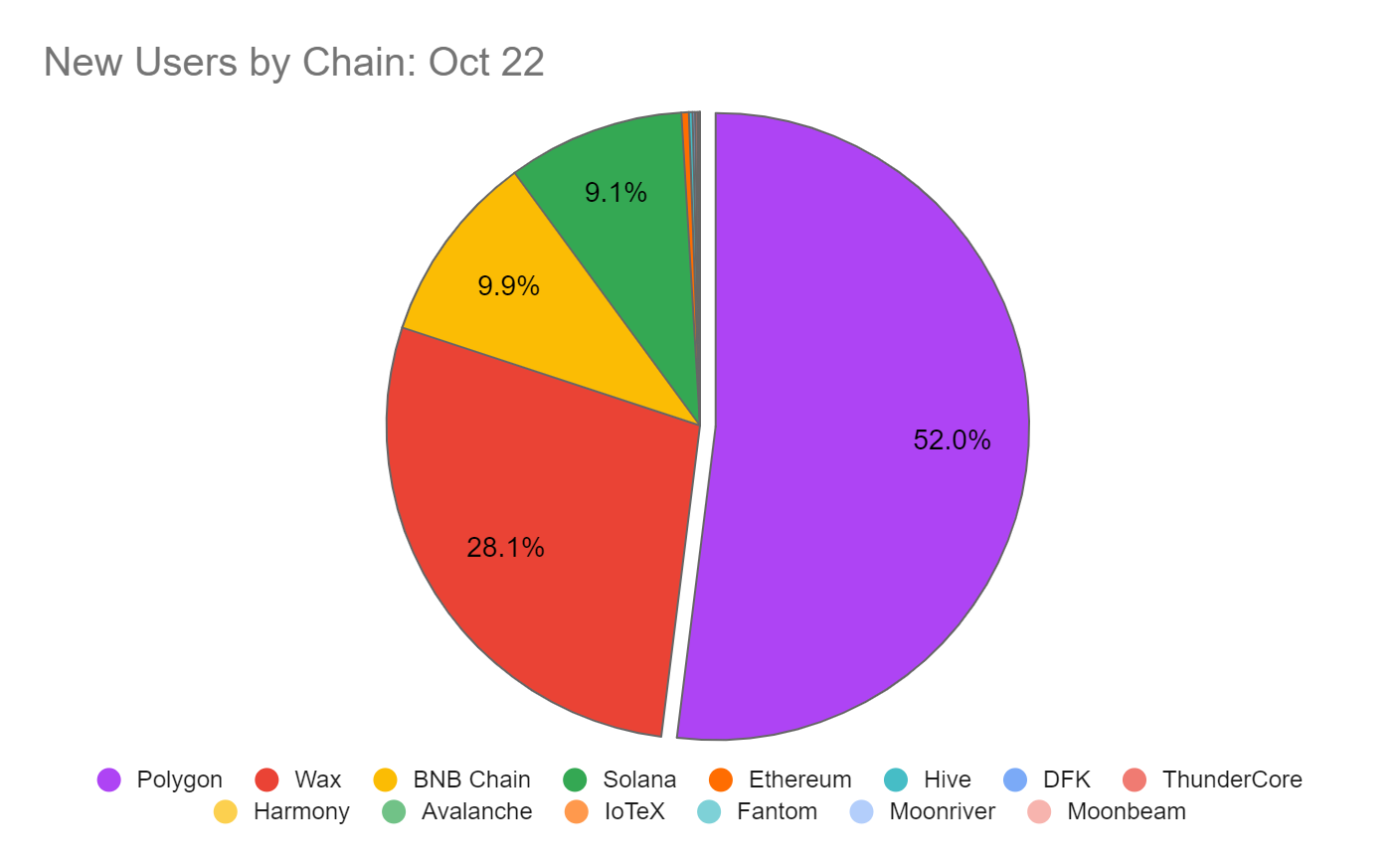

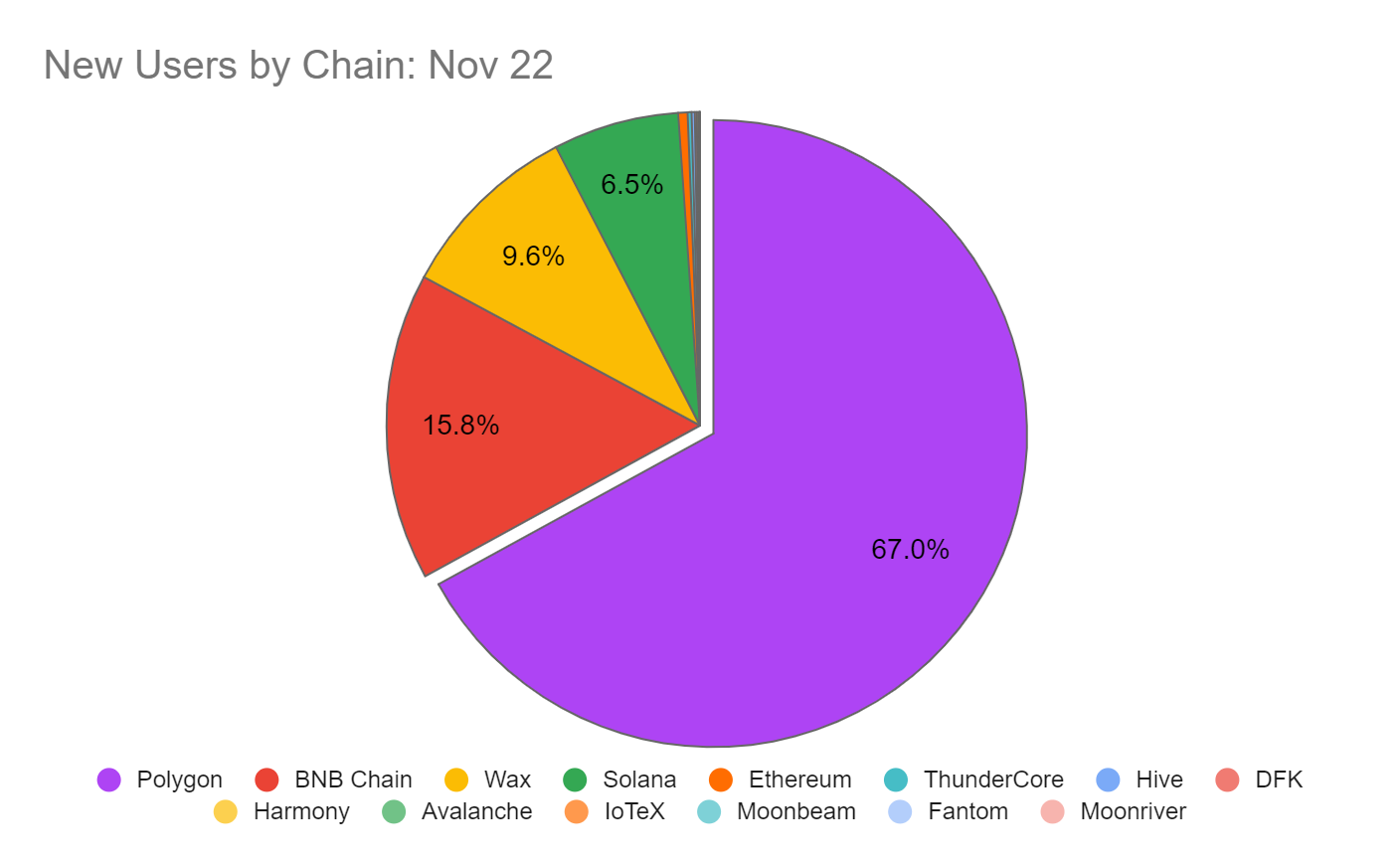

Diving deeper into changes in unique user counts from October to November 2022, we found Polygon had the largest percentage growth (7.5%), followed by Wax (6.4%) and BNB (1.8%). Moreover, Polygon contributed the most net-new users (561,285), accounting for 67% of total industry additions. Compared to October, Polygon’s new user count grew nearly 14% in November.

Figure 16. New Users Added by Public Chains in October 2022 (Source: Old Fashion Research, Footprint Analytics)

Figure 17. New Users Added by Public Chains in November 2022 (Source: Old Fashion Research, Footprint Analytics)

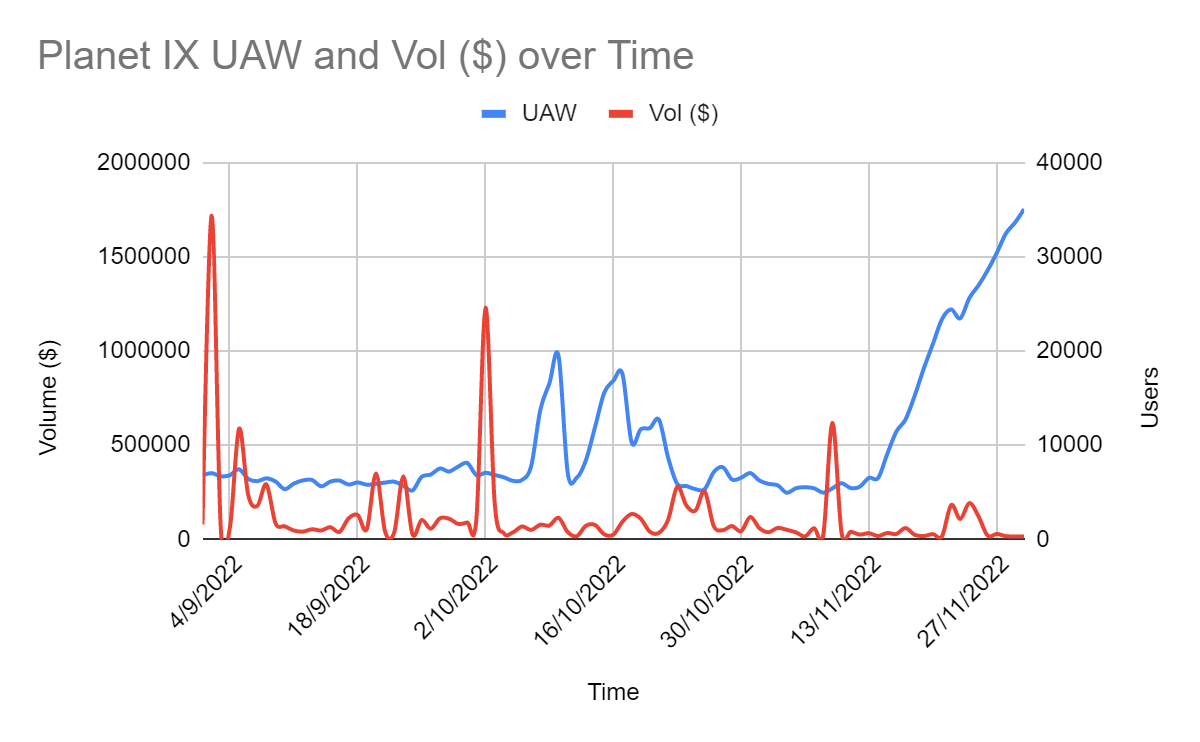

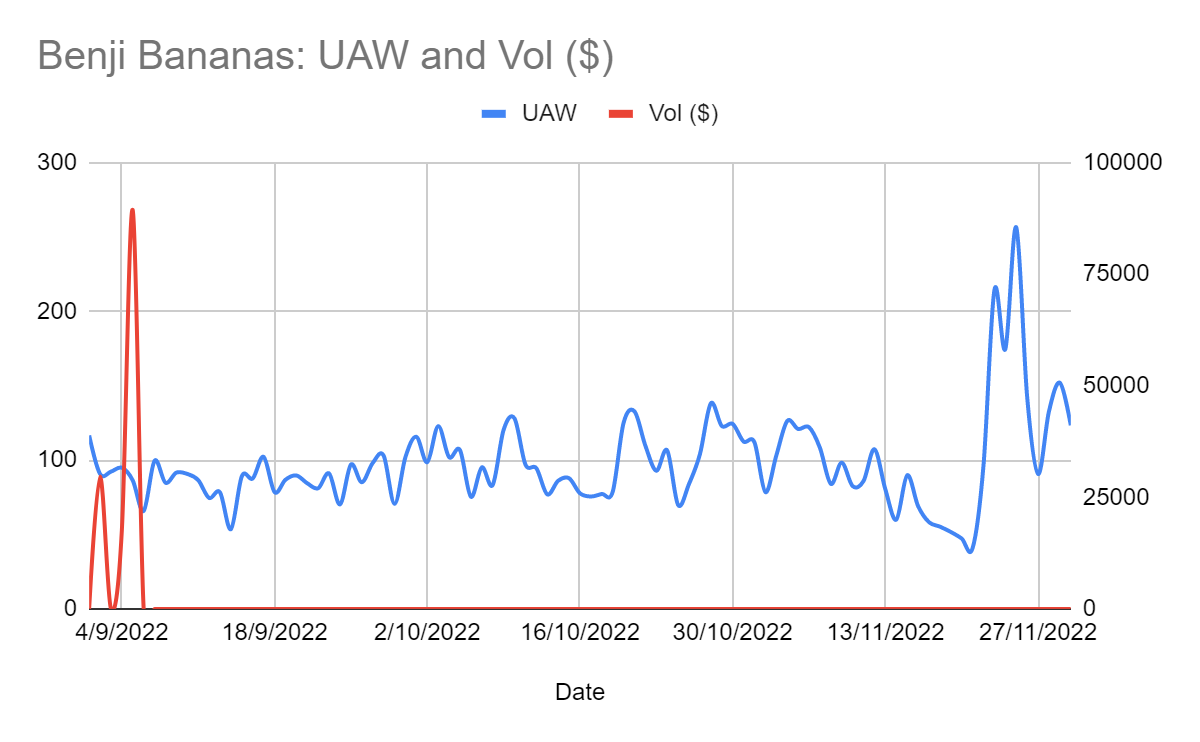

While user growth may stem from various factors—including numerous brand partnerships—we believe Polygon’s gaming ecosystem drove much of this new user influx. From October to November, games like Benji Bananas and PlanetIX saw sharp increases in sales and new users.

Figure 18. Planet IX: Unique Addresses and Transaction Volume ($) (Source: Old Fashion Research, DappRadar)

Planet IX and Benji Bananas significantly boosted Polygon’s user growth. From mid-November to end-of-month, Planet IX’s address count grew fivefold—from 6,514 to 35,058; Benji Bananas reached over 85,000 unique addresses by month-end. Despite some drop-off after initial spikes, both games maintained healthy average levels of 30,000–35,000 unique addresses last month.

Figure 19. Benji Bananas: Unique Addresses and Transaction Volume ($) (Source: Old Fashion Research, DappRadar)

Other contributors to Polygon’s gaming ecosystem include Cometh, Crazy Defense Heroes, and Arc8.

While leadership in blockchain gaming has shifted from Ethereum to BSC, Polygon remains firmly in third place. Skyweaver, a Hearthstone-like digital card strategy game, continues to represent one of the most iconic titles in Polygon’s ecosystem. By December 2022, Skyweaver had processed over 150,000 trades on NiftySwap.

Our Outlook for Polygon’s Gaming Ecosystem

Given Polygon’s ongoing partnerships and upcoming game releases, we are highly optimistic about its gaming future. Games like Oath of Peak, Swords of Blood, Shatterpoint, and Dvision Network have already drawn significant attention. With collaboration among game studios, guilds, and brands, Polygon’s gaming ecosystem is expected to expand exponentially in the coming years.

Whether Polygon’s gaming ecosystem will surpass rivals like BSC hinges on whether Polygon Studios can sustainably deliver exciting games and forge ecosystem-friendly partnerships to onboard more next-generation Web3 gamers.

3. Valuation

3.1 Token Supply and Distribution

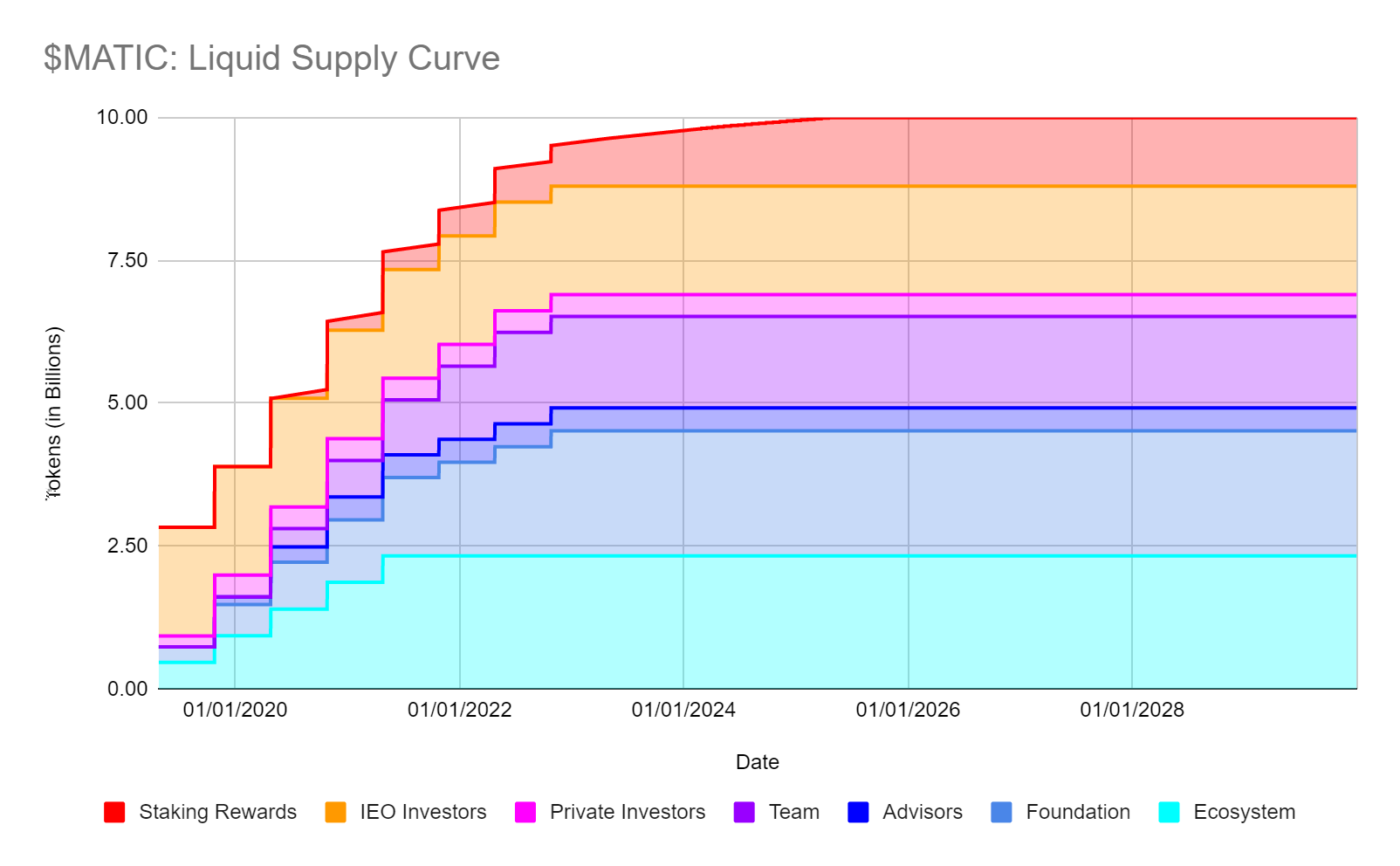

Total supply of MATIC tokens is 10 billion. By the end of October 2022, all tokens became circulating except for staking rewards, which won’t be fully distributed until early 2025.

For simplicity, we use the circulating supply as of October 2022—9,509,641,762 tokens—as the total floating supply of MATIC for valuation purposes below.

Figure 20. $MATIC: Circulating Token Supply Curve (Source: Old Fashion Research, Messari)

According to recent unlock data, 156.2 million $MATIC tokens were unlocked. During last year’s private financing, large amounts of tokens moved from Polygon’s ecosystem fund address to investors—marking the first third release of a three-year lock-up period.

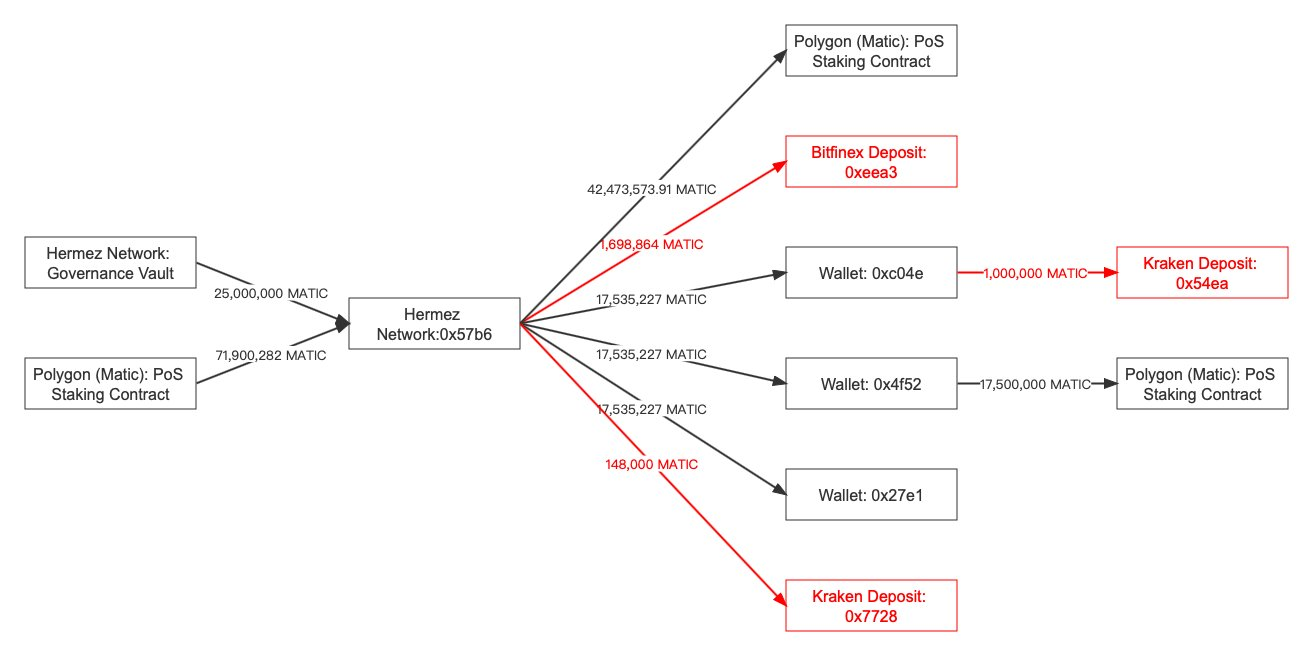

Between November 16 and November 28, a total of 131.2 million $MATIC ($121.7 million) were distributed to investors. Roughly half of these tokens were subsequently transferred to exchanges like Coinbase and Bitfinex.

Another portion was sent to Hermez Network—25 million $MATIC on December 9 and 71.9 million $MATIC on December 12.

Figure 21. Overview of $MATIC Transfers to Hermez Network (Source: Old Fashion Research, Twitter: @Lookonchain)

Of the 96.9 million $MATIC received by Hermez Network, only 2.8 million were withdrawn to exchanges like Bitfinex and Kraken; 60 million were re-staked into Polygon’s PoS staking contract.

3.2 Token Utility

Currently, the MATIC token serves two primary functions: paying gas fees on the PoS sidechain and staking.

Since adopting EIP-1559 in January 2022, base fees from transactions are burned. To date, approximately 5,022,420.1819 MATIC tokens have been burned—just 0.05% of total supply. Given that Polygon is a cost-efficient chain relative to Ethereum, the burn mechanism is unlikely to significantly impact token supply.

Current staking rate is 32.55%, with an average yield of 6.73%. After adjusting for inflation, real annual yield is 4.06%, slightly below Ethereum’s adjusted yield of 4.15%.

However, the biggest concern for MATIC stakers is that staking rewards will deplete by early 2025. Unless token price rises sufficiently or transaction volume surges dramatically, transaction fees may not adequately compensate stakers.

An alternative is introducing new value-capture mechanisms for MATIC alongside the rollout of new infrastructure suites—which we consider highly likely.

As co-founder Sandeep tweeted, when the MATIC token launches on the mainnet, it will serve as collateral for ZK-rollups—not just as a gas payment token on Layer 1.

Figure 22. Sandeep’s Vision for New MATIC Use Cases (Source: Old Fashion Research, Twitter)

3.3 Valuation – EPT (Earnings Per Token) Analysis

Given the crypto industry’s early stage, token valuations are heavily influenced by sentiment or whale activity. Traditional financial valuation models may not fully apply. Nevertheless, borrowing from EPS (earnings per share), we describe token value via EPT (earnings per token).

We assume: PoS Sidechain Revenue = Total Transaction Volume × Cost Per Transaction

Based on Polygon’s quarterly reports, total network revenue approaches $1.888 billion annually, implying each token earns ~$0.00188792 USD per year. At current prices, the token price/EPT ratio stands at 484x.

Figure 23. Polygon Network Revenue in 2022 (Source: Old Fashion Research, Polygon Analytics)

2023 Network Value Forecast:

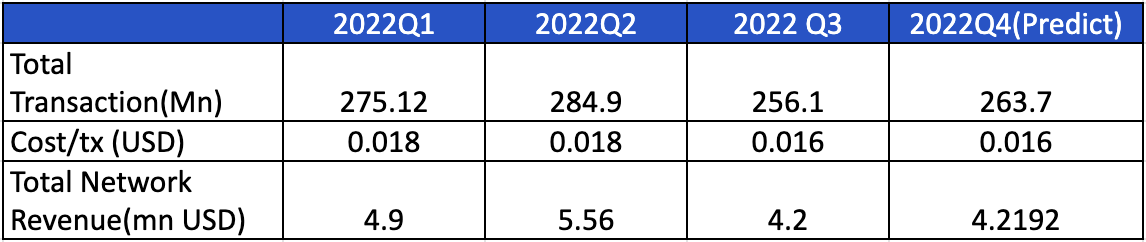

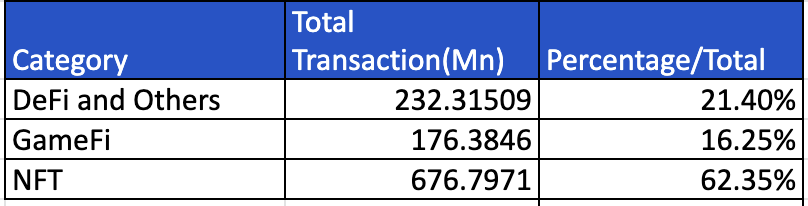

Breaking down Q1–Q3 2022 transaction volumes by category and annualizing the data yields the following table:

Figure 24. 2022 Transaction Volumes by Category (Source: Old Fashion Research, Messari)

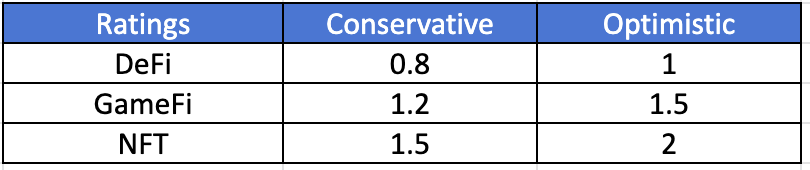

Based on our ecosystem analysis, we assign different ratings to Polygon’s application categories:

Figure 25. Polygon Application Ratings (Source: Old Fashion Research)

We also incorporate subjective forecasts based on our understanding of the crypto industry. While subject to bias, our model allows adjustments under different assumptions.

Figure 26. 2023 Multiple Forecast (Source: Old Fashion Research)

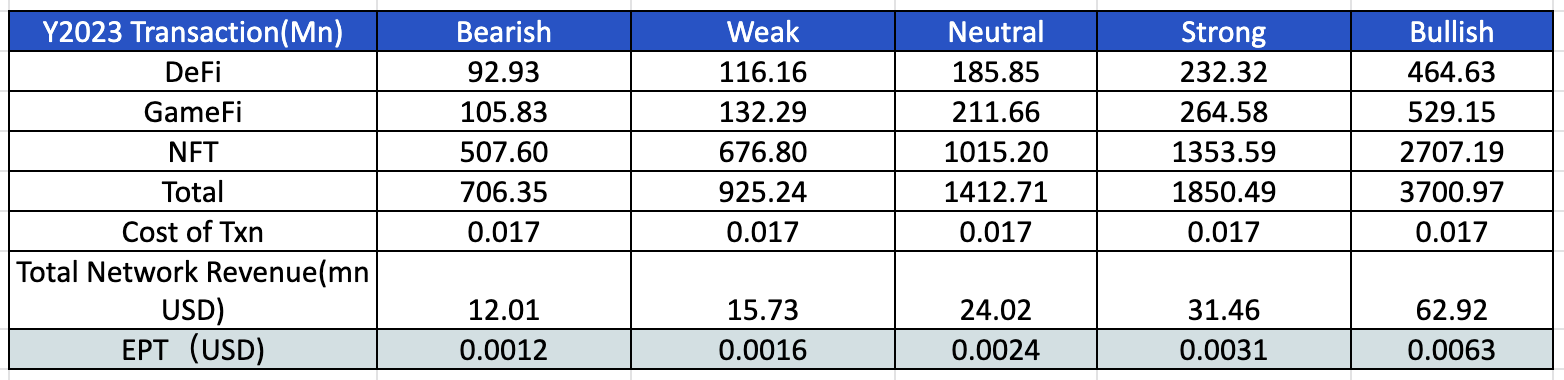

Multiplying these assumptions gives us a predictive matrix to evaluate Polygon’s ecosystem growth in 2023:

Figure 27. 2023 Matrix Forecast (Source: Old Fashion Research)

Finally, combining scenario analysis with the EPT (Earnings Per Token) model, we arrive at the following projections:

Figure 28. 2023 EPT Scenario Analysis (Source: Old Fashion Research)

3.4 Valuation – Comparable Analysis

Using prior calculations, we derive the P/E (price-to-EPT) ratio for MATIC tokens as shown below:

Figure 29. Polygon’s P/E Ratio (Source: Old Fashion Research)

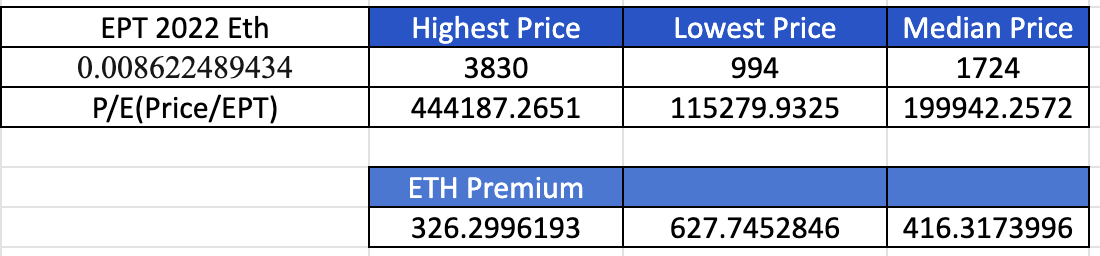

Due to extreme market volatility in 2022, the P/E range neared 10x. Using the same method, we calculate Ethereum’s 2022 EPT:

Ethereum Average EPT = 0.01538154902 USD

Ethereum Median EPT = 0.008622489434 USD

Thus, we conclude Ethereum not only has stronger profitability (higher EPT) but also commands higher market premium (over 300x P/E).

Figure 30. Ethereum’s P/E Ratio (Price / EPT) and Premium (Source: Old Fashion Research)

Given high uncertainty among other comparable peers, we use Ethereum as the sole benchmark to forecast MATIC’s 2023 P/E. Taking Ethereum’s median P/E as reference, we arrive at the following projection:

2023 Target Price for MATIC Token: $3.85

3.5 Valuation – Post-ZK-EVM Mainnet Launch

Although Polygon’s zkEVM Rollup is expected to launch on mainnet in early 2023, we assume a possibility of delay to Q2 or even Q3. Even if launched in H1 2023, ecosystem projects may require one to two quarters to reach full operational capacity compared to the current PoS chain.

Our analysis assumes full integration of Polygon zkEVM and ecosystem projects onto the mainnet

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News