Bankless L2 Year-in-Review: Clear Growth in On-Chain Data, Set for Explosion in 2023

TechFlow Selected TechFlow Selected

Bankless L2 Year-in-Review: Clear Growth in On-Chain Data, Set for Explosion in 2023

2023 will be another explosive year for L2.

Written by: Ben Giove

Compiled by: TechFlow

2022 was a brutal year for cryptocurrency, with stablecoins, hedge funds, lenders, and exchanges collapsing in terrifying fashion. Much of the space disappeared, yet amid the carnage there were still pockets of growth. One major area of such growth has been Layer 2 ecosystems.

Ethereum's scaling solutions also quietly exploded in 2022, achieving numerous milestone developments across infrastructure and application layers, along with solid growth across key KPIs.

With that in mind, let’s review the L2 landscape in 2022 and see whether they’ll break out again in 2023.

Metric Snapshot

TVL

The dollar value of assets connected to L2s declined from $5.7 billion to $4.1 billion, down 28.6%. However, this may be attributed more to falling crypto prices than user fund withdrawals, as TVL denominated in ETH rose from 1.6 million to 3.4 million, an increase of 120.6%. This suggests significant net inflows of liquidity into L2s over the year, price-adjusted.

Transactions

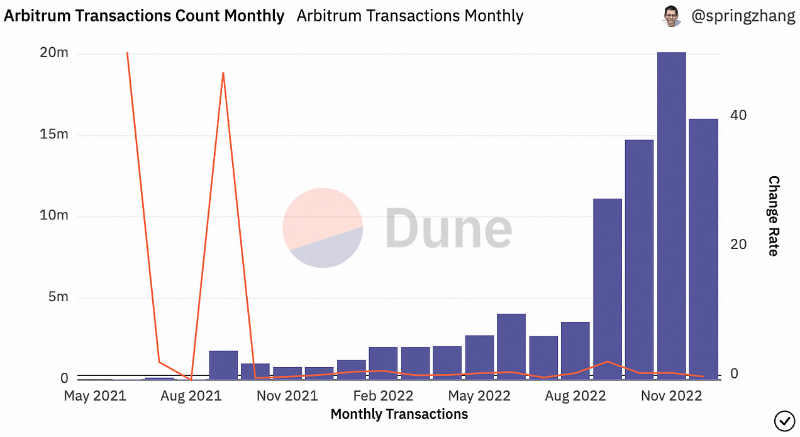

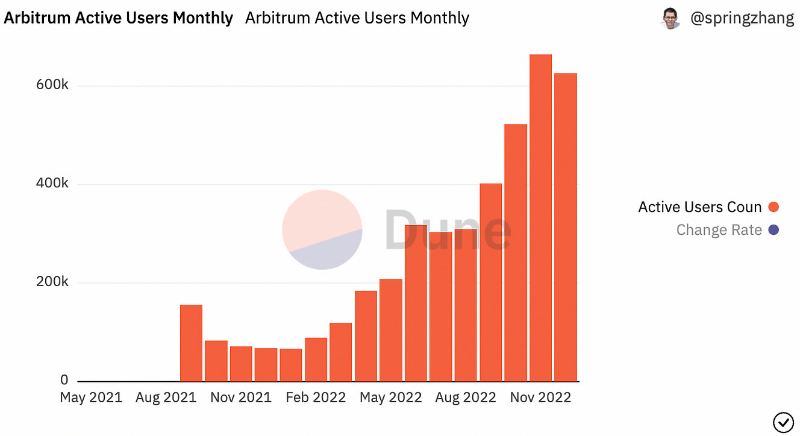

Throughout 2022, Arbitrum saw substantial transaction volume growth, driven by rising influence from native dApps like GMX and the Nitro upgrade significantly reducing transaction fees. The network’s transaction count surged 590% between Q1 and Q4, rising from 5 million to 34.9 million.

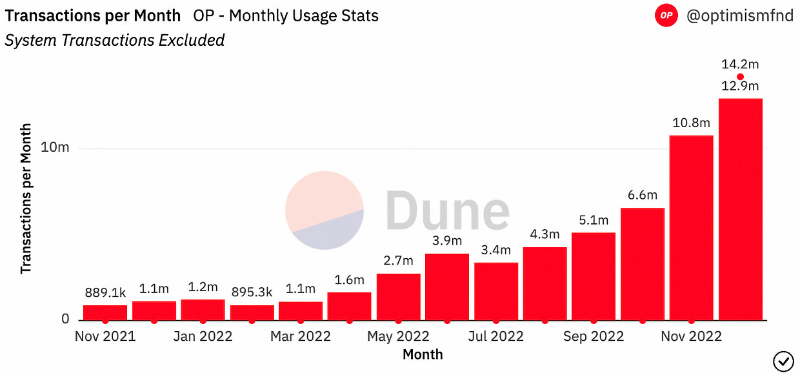

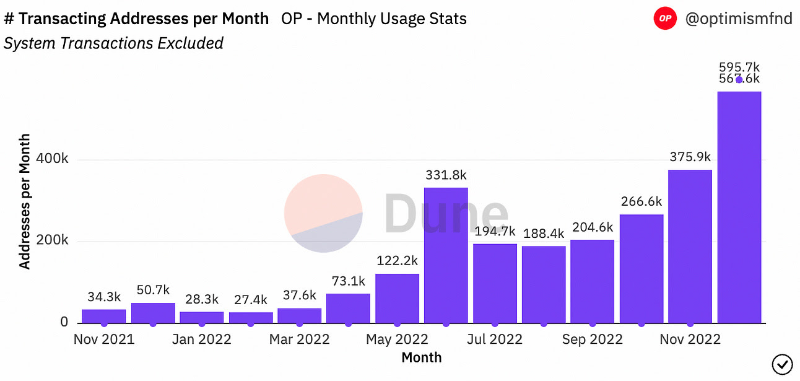

Optimism also experienced dramatic transaction growth, likely fueled by increased activity following the launch of its OP token and subsequent incentive programs. Optimism processed 3.2 million transactions in Q1 and 30.3 million in Q4—an 846.7% increase between the two periods.

Users

During 2022, Arbitrum experienced strong growth in active users, driven by usage of apps like GMX and scalability improvements from the Nitro upgrade. Monthly average active users on the L2 skyrocketed from 918K in Q1 to 6.05 million in Q4—a 559.1% increase.

Optimism also saw significant user growth during 2022. Riding the wave of token distribution and incentive programs mentioned earlier, Optimism’s monthly active addresses surged from an average of 33.1K in Q1 to 403.4K in Q4—an increase of 1,118.7%.

Highlights

Rise of GMX

GMX emerged as the breakout L2 application of 2022. As on-chain activity dried up and prices fell, usage of the Arbitrum-based decentralized perpetual exchange surged, generating $81.4 billion in trading volume and $33 million in revenue.

GMX has become a foundational pillar of Arbitrum, accounting for 39.5% of the network’s TVL. Numerous projects—including Dopex, Vesta Finance, Rage Trade, and Umami Finance—have built atop GMX and integrated its liquidity provider token GLP.

This growth, combined with robust tokenomics featuring revenue sharing, made GMX one of the top-performing assets in all of crypto, rising 87.4% against the dollar and 487.2% against Ethereum by the end of 2022.

L2 Token Airdrops

Several notable L2 projects launched tokens in 2022.

The most prominent was Optimism, which airdropped 5% of the OP supply to early users and stakeholders. This token launch catalyzed a surge in user activity and liquidity on the network, whose TVL increased by 86.9% since its release on May 31.

Another L2 to launch a token was zk-rollup provider StarkWare. StarkWare announced an $8 billion valuation funding round in May and distributed its STRK token in mid-November, though it remains non-tradable for now.

OP and STRK have not yet fully realized their value accrual potential, as neither is currently used for decentralizing the sequencer of their respective networks. Nonetheless, their launches represent exciting first steps in L2 token design and will continue serving as critical strategic tools for each ecosystem.

zkSync Launch

zkEVMs are considered the holy grail of scaling solutions, combining the network effects and developer tooling of the EVM with the massive throughput of zk-rollups. It was widely believed that zkEVMs would take many years to arrive.

Yet seemingly unnoticed by many, zkSync launched its zkEVM—zkSync 2.0 mainnet—in October. While it should be noted that the network is still quite early, representing only the first phase of a three-stage rollout and currently closed to contract deployments and general users, reaching this production stage remains a monumental achievement in scaling.

Lowlights of L2

dYdX Exodus

In June, the perpetual exchange announced it would migrate away from StarkEx and instead launch its own app-specific blockchain, V4, built using the Cosmos SDK.

This was a significant blow to the current L2 landscape, as dYdX was the largest decentralized perpetuals exchange, having generated $461.2 billion in trading volume over the prior 12 months. dYdX’s move also sparked speculation that many other prominent dApps might follow suit, opting to build sovereign chains rather than remain within the L2 ecosystem.

Such mass exodus hasn’t materialized—yet. Still, dYdX’s decision serves as a clear reminder that L2s will continue facing intense competition.

Centralization Elements Persist

Calling this a "lowlite" might be slightly harsh—but many L2s continue operating under major trust assumptions. For example, both Arbitrum and Optimism have not yet fully implemented trustless fraud proofs or decentralized sequencers. Moreover, each network can still be upgraded by their core teams.

This is understandable, as rollups are new technology and these centralized elements act as safeguards to prevent loss of user funds. Nevertheless, these trust assumptions remain sources of risk heading into 2023.

Looking Ahead

There are many exciting developments ahead for both existing and new L2s in 2023. Let’s go over some of them:

Arbitrum

Arbitrum has several catalysts that should drive growth in 2023.

Beyond the seemingly endless stream of innovative DeFi applications launching on the L2, the network stands to benefit from Arbitrum Odyssey—a campaign designed to encourage dApp usage by rewarding users with NFTs. Odyssey was delayed after its second week due to gas fee spikes but is expected to resume soon.

Odyssey may also serve as a prelude to the launch of the Arbitrum token. Such a token could be airdropped to early users and Odyssey participants. Arbitrum has kept details about its token tightly under wraps, but if (when) it launches, it could trigger a significant surge in user activity and liquidity inflows to the network.

Optimism

Optimism is also poised to see another year of strong growth in 2023.

With continued OP incentive programs and an upcoming second airdrop, Optimism is preparing for a major scalability improvement via the Bedrock upgrade. Currently live on testnet, Bedrock is an upcoming network upgrade expected to reduce the cost of submitting calldata to L1 and enable support for “alternative proof systems” like zk-proofs. Together with the forthcoming EIP-4844—which will drastically reduce gas costs for all L2s—Bedrock should lead to a substantial boost in Optimism’s scalability.

Optimism is also expected to see greater adoption of the OP Stack, a development framework enabling the creation of custom L2s. OP Stack should gain further traction with the launch of Aevo, a decentralized options exchange from Ribbon Finance, which will be built on an L2 leveraging the stack.

“Clone” L2s

2023 will see many L2s reach milestones, including mainnet launches of Polygon and Scroll’s zkEVMs.

As previously mentioned, zkSync will continue its phased rollout to support smart contract deployment. Additionally, other networks like Fuel—an ultra-scalable ORU utilizing Swell as its programming language—will gain more traction as developers grow more familiar with their tooling.

There were highlights, yes, and some low points too—but Ethereum is scaling, and 2023 will be another explosive year for L2s.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News