Will the stablecoin issuance protocol Vesta be a potential alpha on Arbitrum?

TechFlow Selected TechFlow Selected

Will the stablecoin issuance protocol Vesta be a potential alpha on Arbitrum?

Vesta is Arbitrum's native protocol, ranking fourth in TVL among native protocols.

Written by: DeFi Mochi

Translated by: TechFlow

Vesta is a native protocol on Arbitrum, ranking fourth in terms of TVL among native protocols. Since June, Vesta’s TVL has been steadily growing (reaching $25 million), but more importantly, its market cap remains under $3 million! Could it be a hidden gem within the Arbitrum ecosystem? Let’s analyze the data together using Dune Analytics and find out!

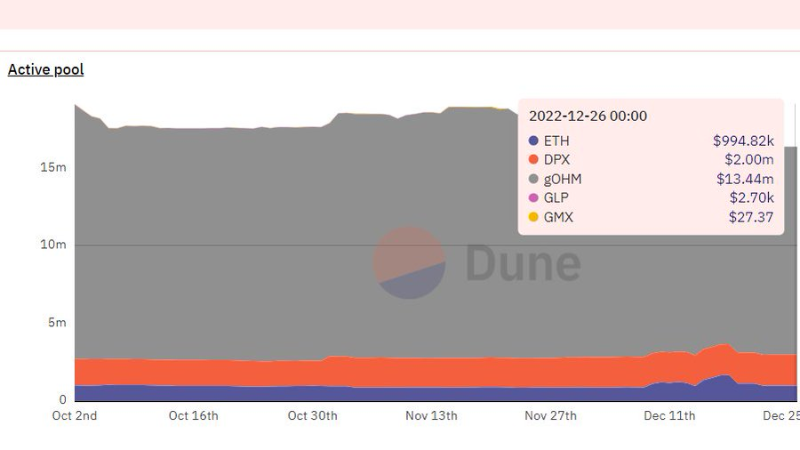

Vesta is a CDP protocol where users can deposit assets as collateral to mint the $VST stablecoin based on their collateral ratio (CR). Assets deposited into Vesta go into the Active Pool. The Active Pool's TVL stands at $15,902,792.

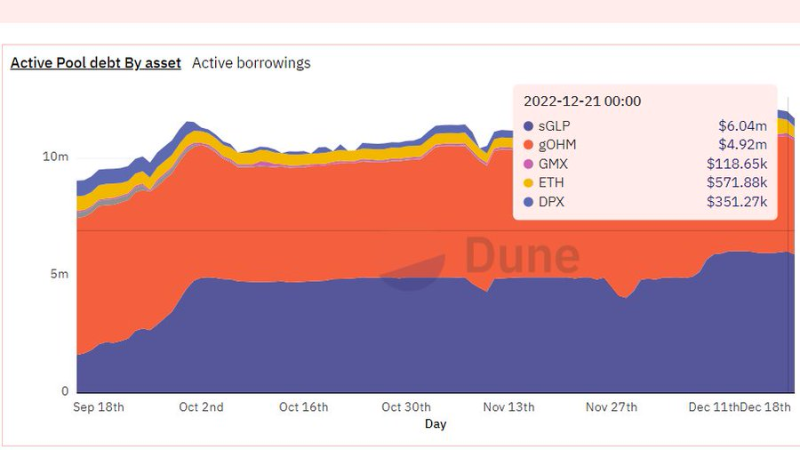

These charts show the total active debt broken down by asset. Currently, total outstanding borrowings amount to $11,694,559. Approximately 51% of the debt is backed by $GLP, and 43% by $gOHM.

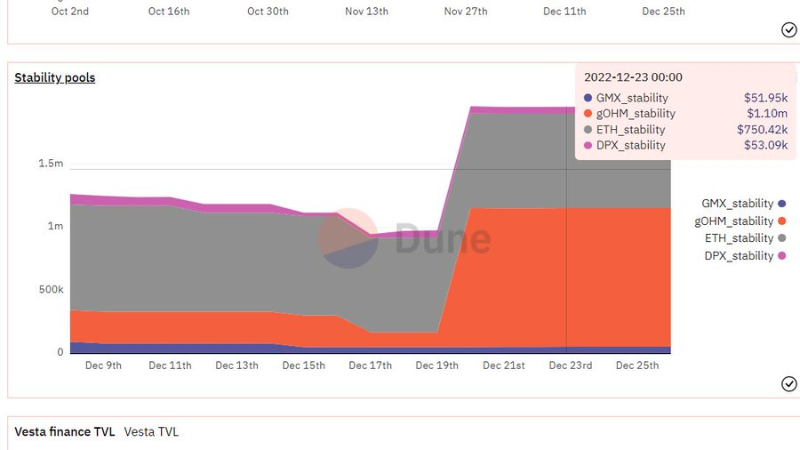

Liquidations occur when CR falls below 110%, and are offset by the Stability Pool. Users can deposit $VST into the Stability Pool to receive collateral tokens from liquidations—often profiting when liquidations happen just slightly below 110%. Total $VST in the Stability Pool amounts to $860,170.

If the $VST in the Stability Pool is insufficient to cover the debt, Vesta redistributes the undercollateralized vaults to other borrowers. Vesta compensates liquidators with 0.5% of the collateral to ensure prompt liquidation.

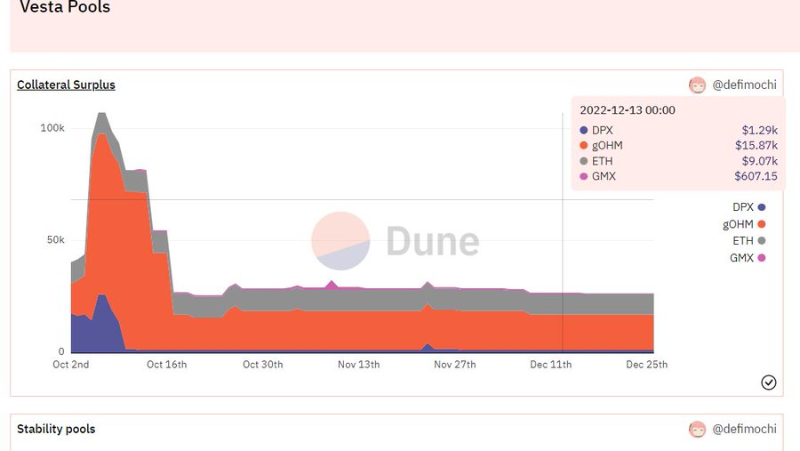

Vesta defines surplus collateral in liquidations as collateral minus debt (when CR > 100%). This surplus collateral is distributed pro-rata to Stability Pool LPs based on their share in the pool.

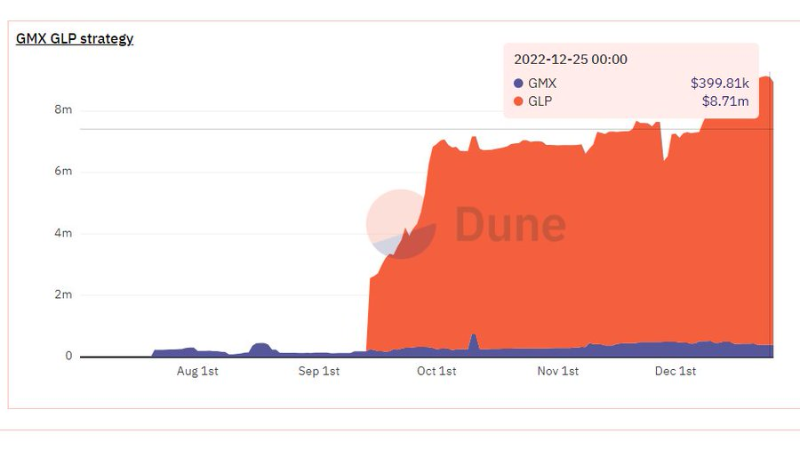

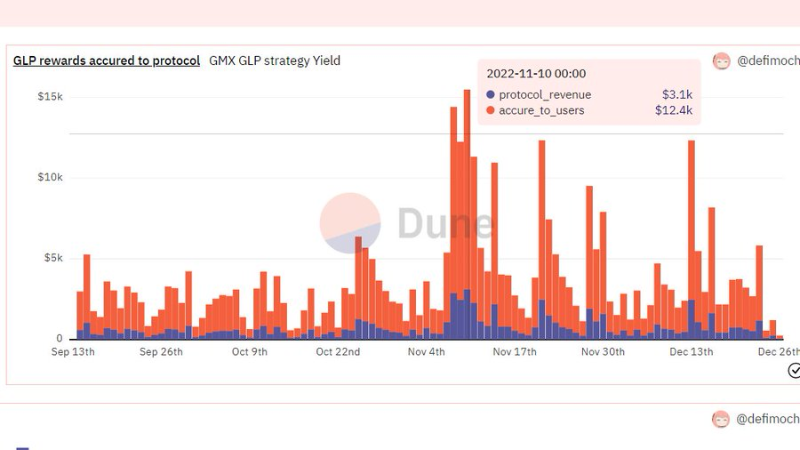

Vesta utilizes its collateral through yield-generating strategies. Currently, collateral is only deployed in the GMX-GLP strategy.

Vesta captures 20% of the $GLP rewards as protocol revenue, while the remaining yield goes directly to users. Based on the average $GLP rewards accumulated over the past month, the annualized protocol revenue is $264,990.

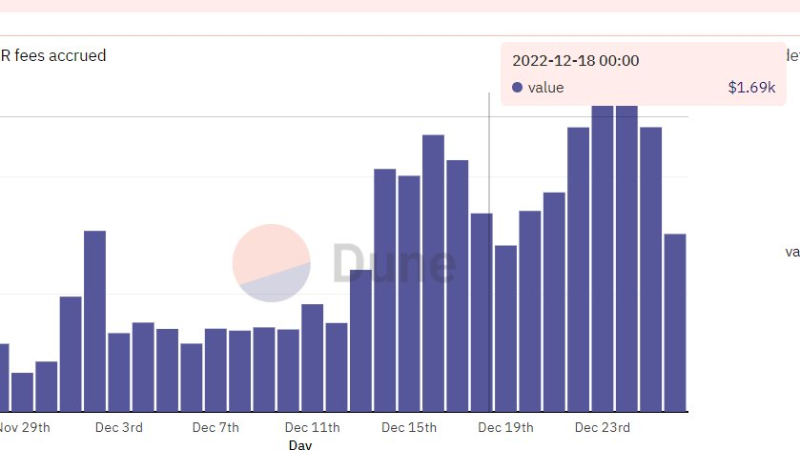

Vesta has transitioned from a burn-and-redemption fee model to a VRR model (Vesta Reference Rate). When $VST trades below $1, borrowing fees increase to incentivize more $VST deposits into the Stability Pool for higher VRR yields.

When $VST trades above $1, the VRR decreases to encourage more borrowing and selling of $VST, pushing it back toward the peg. The fees collected via VRR go into an emergency reserve to guard against shortfall events.

The total $VST in the emergency reserve is $40,400.

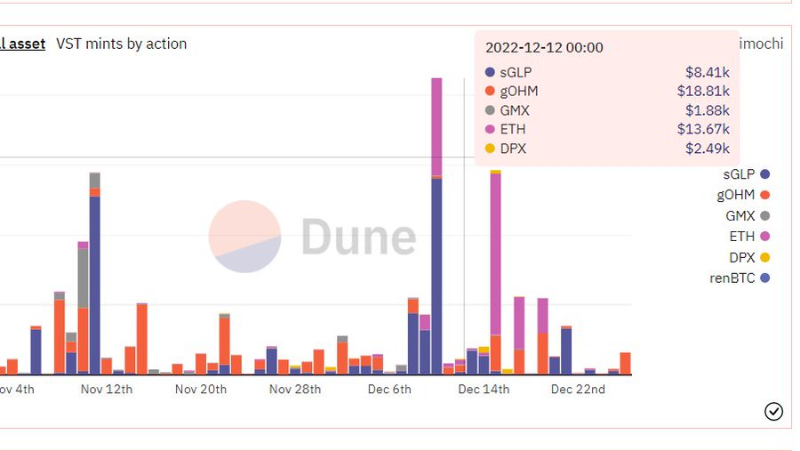

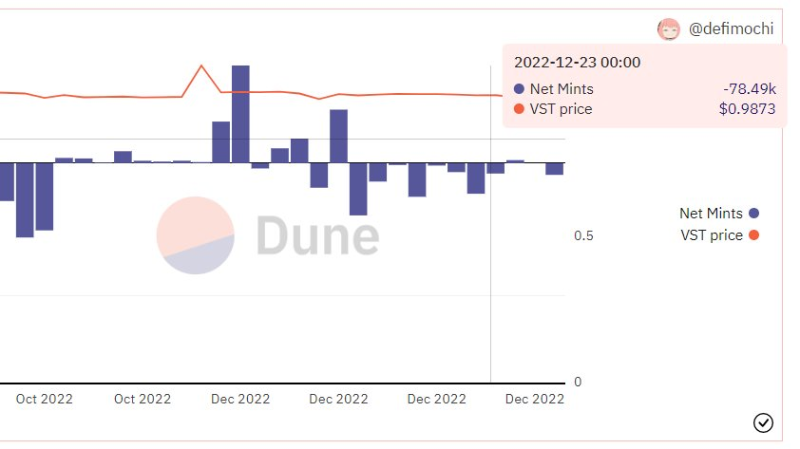

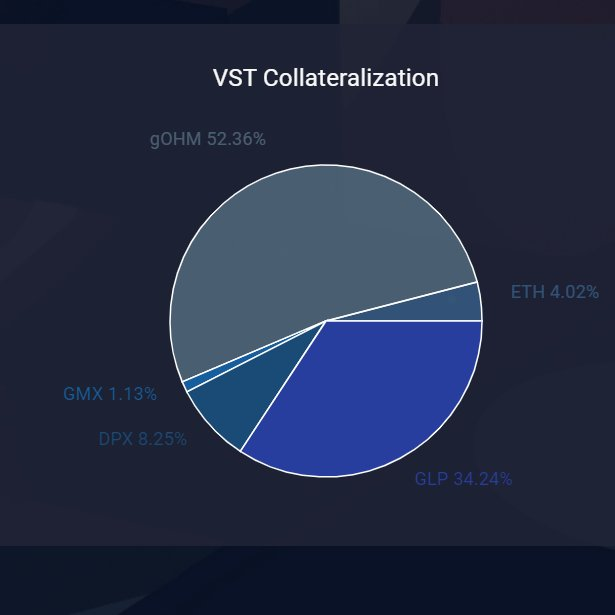

This chart shows the distribution of $VST minted against different collateral assets. We observe a shift from previously dominant $GLP usage to increasing use of $ETH recently. As part of the Olympus incubator program, $gOHM also constitutes a significant portion of collateral used to mint $VST.

Looking at the minting volume versus $VST’s peg, we see that $VST has mostly traded below $1, indicating opportunities to earn higher borrowing fees as a Stability Pool provider.

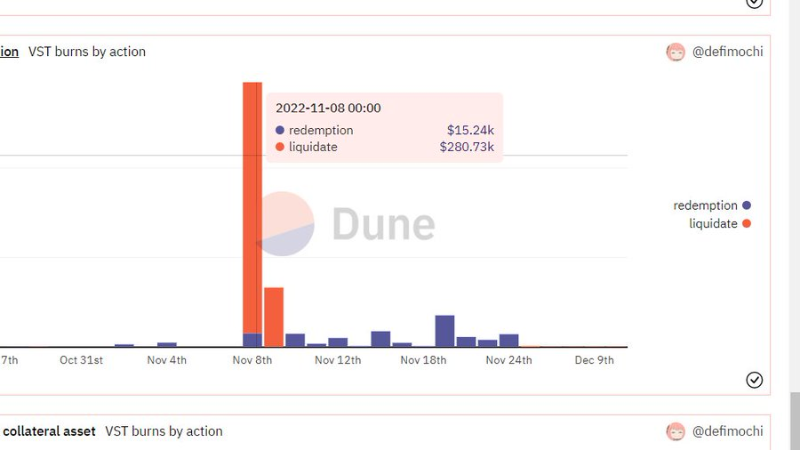

Interestingly, nearly $280,000 worth of $VST was burned, while $67,000 worth of $VST was liquidated on November 9.

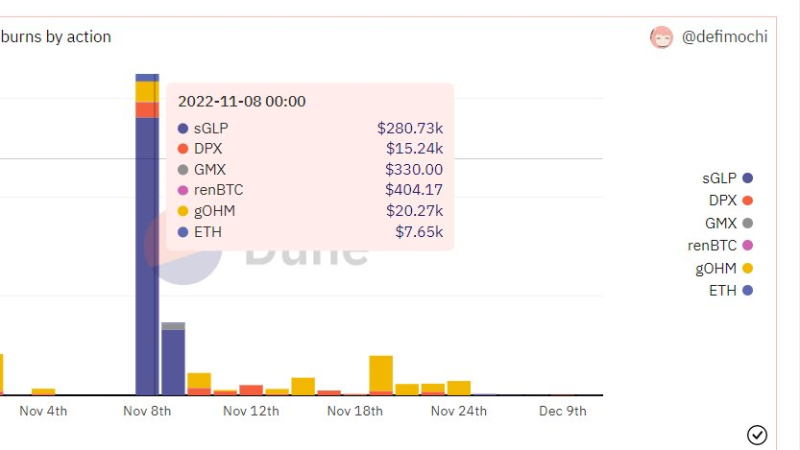

Examining the chart of $VST burned by collateral type, we find that most burned $VST came from $GLP-backed vaults. Most other liquidations were conducted via $gOHM, likely due to its volatility.

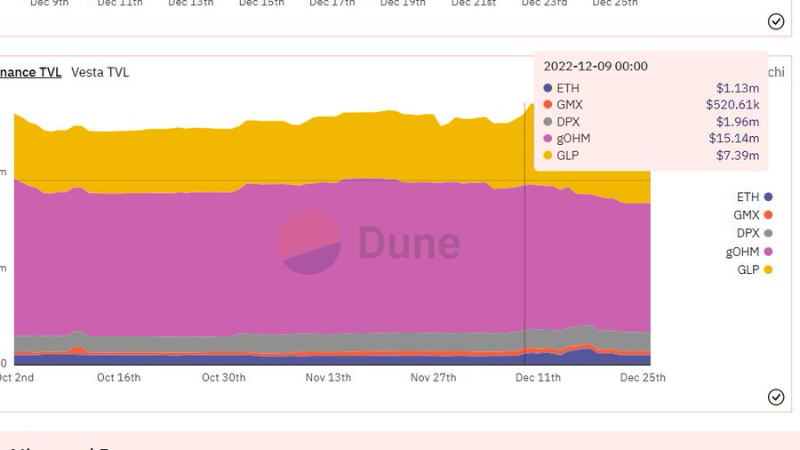

TVL is calculated as total assets in the Active Pool plus deployed collateral (via the $GMX-$GLP strategy), currently totaling $25,387,009. I believe this is quite high for a token with a market cap under $3 million.

The $VSTA token can currently only be used for governance or liquidity mining. Frankly, it would make sense if they allowed staking of $VSTA and redirected 20% of the $GMX-$GLP strategy rewards to $VSTA holders. That would certainly boost demand for $VSTA.

Potential Risks:

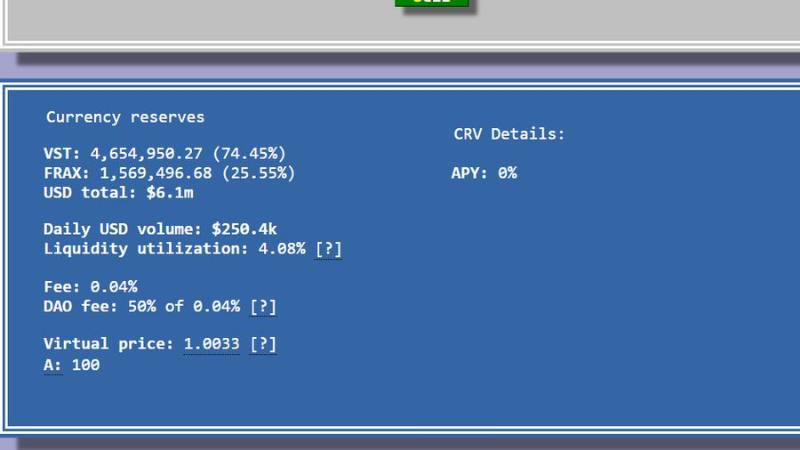

1) Weak peg stability. A persistently weak $VST peg may discourage borrowers from minting $VST. Currently, $VST can be acquired via the $VST-$FRAX liquidity pool on Curve or the $VST-$USDC pool on SwapFishFi. This risk could be mitigated with deeper liquidity.

2) Overreliance on $gOHM and $GLP. The team does plan to introduce new assets as eligible collateral to address this issue.

Overall, as one of the highest-TV L native Arbitrum protocols, I believe $VSTA is a promising project, but its main drawback lies in the lack of utility for its governance token. If the team can effectively address this, adoption of $VSTA could reach much greater levels.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News