Bankless: The Failure of FTX Is Why We Need More DeFi

TechFlow Selected TechFlow Selected

Bankless: The Failure of FTX Is Why We Need More DeFi

"FTX's failure declared the failure of DeFi."

Written by: Donovan Choy

Compiled by: TechFlow

“The failure of FTX marks the failure of DeFi.”

Over the past week, amid the shocking implosion of FTX and Alameda, this claim has found support among various Web3 skeptics.

The White House reiterated that FTX is a reason “why prudent regulation of cryptocurrency is indeed needed.” In a tweet, Senator Elizabeth Warren characterized the crypto industry as "smoke and mirrors," calling for the U.S. Securities and Exchange Commission to pursue "more aggressive enforcement."

And it's not just politicians. Anti-DeFi Bitcoiners are seizing on the FTX explosion to promote their mantra of “why only Bitcoin matters.”

FTX Is Not DeFi

The FTX disaster represents the failure of centralized financial mechanisms—precisely the kind of systems that DeFi has long sought to replace.

Consider where the roots of the FTX disaster ultimately lie—FTX lent out customer deposits instead of holding them 1:1 as redeemable deposits.

Worse, they over-leveraged their balance sheet by holding a disproportionate amount of illiquid FTT tokens as collateral, rather than safer assets like stablecoins.

In short, FTX tried to act like a bank in ways it shouldn’t have—and did so poorly.

Neither of these scenarios would be possible with a DeFi exchange or bank.

DeFi Is Self-Regulating

Take Uniswap, one of DeFi’s largest trading platforms.

Uniswap users never lose sleep wondering whether “Uniswap will trade their deposits,” simply because there are no individual “deposits” to begin with. Unlike FTX, users simply execute trades across hundreds of permissionless liquidity pools.

Funds in these pools come from liquidity providers/stakers, who likewise don’t worry about Uniswap misusing their funds. These liquidity pools are managed by immutable smart contracts, making it impossible for Uniswap to do anything else with the capital.

The same applies to any lending/borrowing DeFi platform such as Aave or Compound.

If you take out a loan on Aave, you must first deposit capital at a secure loan-to-value ratio. If the value of your collateral drops below a preset threshold, Aave automatically liquidates your position. This stands in stark contrast to FTX’s series of toxic loans extended to its sister hedge fund Alameda, which were then used as collateral elsewhere.

The most competitive, market-tested DeFi protocols follow these self-governing rules designed precisely to avoid situations like what’s unfolding at FTX today.

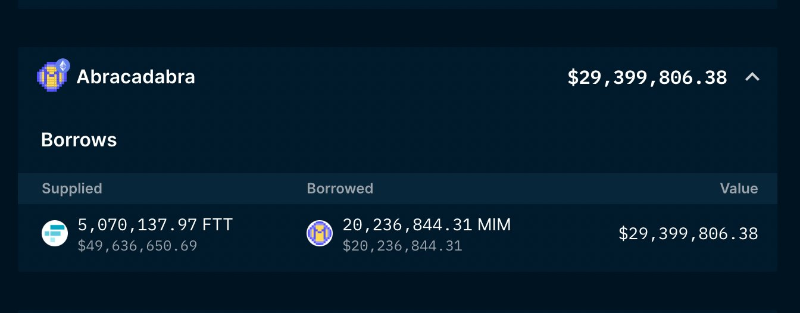

Before CeFi collapsed, Alameda Research held an outstanding loan of 20 million MIM (Abracadabra’s stablecoin), secured by 5 million FTT—the exchange token of FTX. But regardless of your views on Alameda (or Dan Sestagno), amid market turmoil, the debt was fully repaid on November 9.

Why did they repay?

Alameda didn’t repay out of goodwill. They paid because in the EVM world, there’s no option to file for bankruptcy protection. Had Alameda defaulted, their FTT collateral would have been immediately liquidated and sold off by liquidators at whatever price prevailed—in this case around $17.

Repaying the loan and reclaiming their FTT was clearly in their own best interest.

In short, it was DeFi that forced them to repay.

What about the stablecoin segment of the DeFi world?

The benchmark for a stablecoin is whether it maintains its peg to the dollar—especially under market stress.

Yet Maker’s DAI performed well during last week’s test.

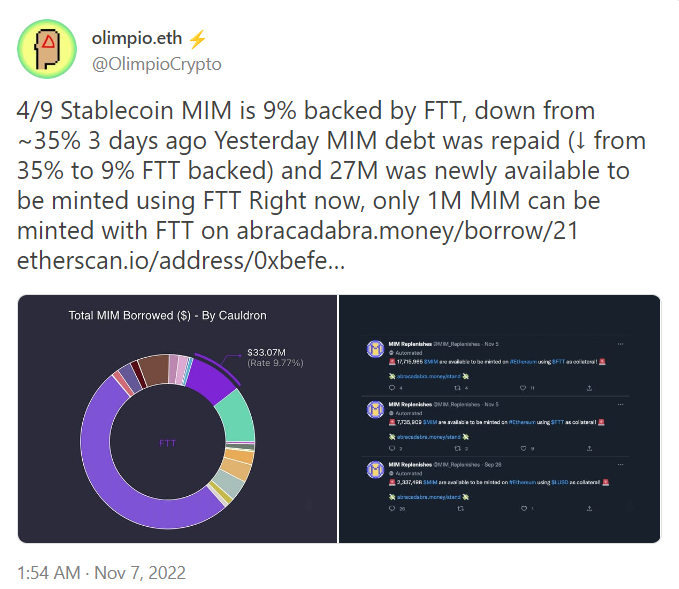

Even MIM, despite having 35% of its backing in FTT, held up well.

After briefly dipping to $0.974 on November 9, MIM quickly re-pegged.

DeFi Failed at the Social Layer

Therefore, when crypto skeptics assign the blame of “failure” to DeFi, those within the space should rightly push back.

Did DeFi trading and lending protocols function as intended?

Yes, they did.

Did decentralized stablecoins devalue and collapse?

No, they did not.

Ultimately, skeptics seem to miss this point. Yet in a sense, DeFi did fail.

-

DeFi failed because its community grew complacent. We should have implemented proof-of-reserves long ago.

-

DeFi failed because we didn’t anticipate SBF’s intentions—we should have been more skeptical.

-

DeFi failed because we accepted centralized intermediaries for convenience. Self-custody is hard, but trusting FTX left too many in the industry exposed to risk.

The failure lies not with the DeFi system itself, but with the crypto community, which compromised far too much on the values of decentralized finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News