A Guide to the Cryptocurrency Asset Management Sector: The Digital Asset Management Market is Thriving

TechFlow Selected TechFlow Selected

A Guide to the Cryptocurrency Asset Management Sector: The Digital Asset Management Market is Thriving

The demand for asset management will not disappear: as the cryptocurrency market continues to expand, it will even continue to grow.

Written by: King Tuts, lingchenjaneliu, and 0xPhillan

Translated by: TechFlow intern

The sharp decline in cryptocurrency prices has devastated many crypto asset management firms. However, the demand for asset management will not disappear—in fact, it will continue to grow as the crypto market expands. We firmly believe that existing companies still possess immense potential and will become great in the future.

1. Market Size

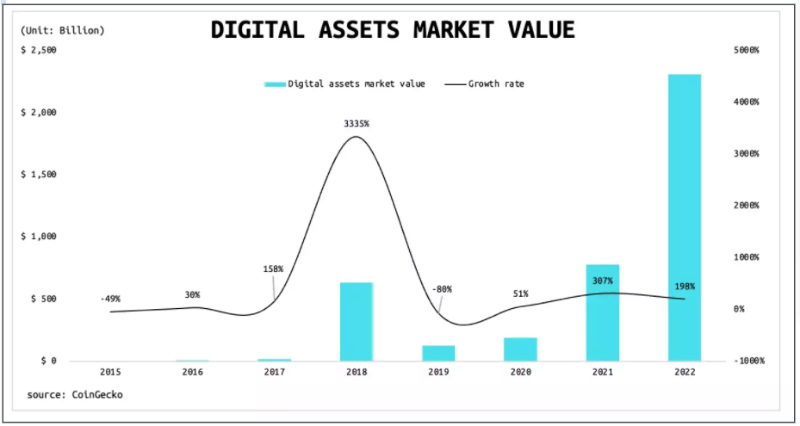

Digital assets are among the fastest-growing asset classes globally over the past decade. According to CoinGecko, the market value of digital assets was around $10 billion in 2014 but surged to approximately $2.3 trillion by early 2022—an astonishing 216-fold increase, with a compound annual growth rate of about 96% over the past eight years.

An increasing number of individuals and institutions recognize the rise of crypto assets as an unstoppable trend. According to VettaFi, since the launch of the first U.S. Bitcoin ETF in October 2021, the combined market capitalization of the top 10 Bitcoin-related ETFs in the United States has grown to approximately $2.27 billion. Morgan Stanley became the first major U.S. bank to offer a Bitcoin fund to its wealthy clients in March 2021, while Goldman Sachs provided its first Bitcoin-backed lending instrument in April 2022. Many other large corporations are also engaging with the cryptocurrency industry in various ways.

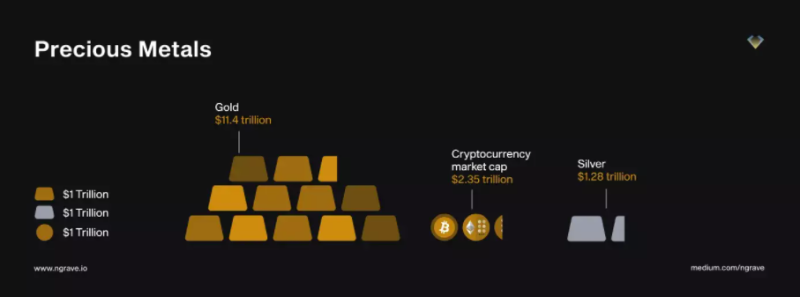

Although the cryptocurrency market has grown significantly over the past decade, we must emphasize that it still holds substantial growth potential. As of January this year, the market cap of cryptocurrencies stood at $2.35 trillion, compared to $11.4 trillion for gold—4.85 times larger than crypto.

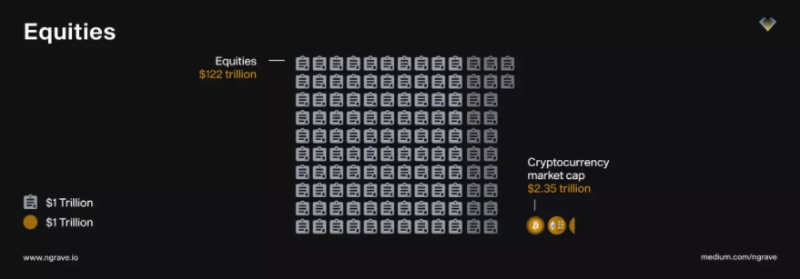

The stock market has a market cap of $122 trillion—52 times that of cryptocurrencies.

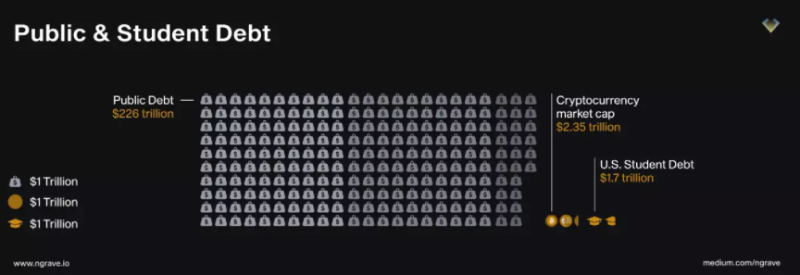

The bond market has a market cap of $226 trillion—96 times that of cryptocurrencies.

To date, Bitcoin still dominates 40.6% of the entire crypto asset market, down from 88% dominance in early 2014. In the long term, Bitcoin’s share within the crypto market may continue to decline, revealing the growth potential of many emerging crypto assets.

2. Overview of the Digital Asset Management Market

Asset management is a broad concept—much like banks in traditional finance, digital asset management firms offer their clients a variety of products and services.

2.1 Savings Accounts and Lending Services

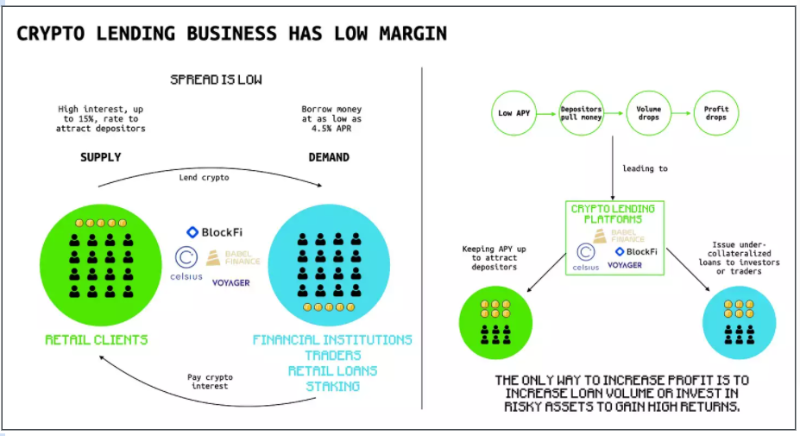

Savings accounts are one of the most fundamental offerings of asset management firms. Similar to traditional banks, customers deposit their digital assets into savings accounts and earn interest. Most often, these firms lend out the deposited assets to generate returns, profiting from the spread. However, digital asset management (digital AM) differs significantly from traditional banking:

Traditional banks typically support one or a few currencies, whereas digital asset managers support many different crypto assets.

Traditional banks cannot access collateral before default, but crypto lenders can re-lend collateralized assets at any time to generate additional profits.

Borrowers of crypto assets are usually limited to a small number of top-tier institutions across the industry, making asset management revenue highly dependent on just a few clients—creating high risk.

The transparent and highly volatile crypto market makes liquidations more likely, which can harm both customers and the firm.

Most digital asset management firms offer these services. These characteristics grant lenders greater operational flexibility but also introduce greater risks. For example, Babel, Voyager, and BlockFi—the most prominent crypto asset management services recently—have faced severe liquidity risks, which, if unmanaged, could trigger financial panic across the market.

2.2 Market Making

Market making is a critical and highly specialized service offered by asset management firms—not directly available to retail clients—but essential and indispensable to the digital asset management industry.

When providing services to clients, asset managers rely on support from crypto exchanges—including custody infrastructure and low fees. They also enjoy higher borrowing limits due to the volume of business they bring. However, exchanges often provide such support only in exchange for strong market-making services. The greater the trading volume and depth a company provides, the more support it receives from exchanges—and thus, the better services it can offer to its clients.

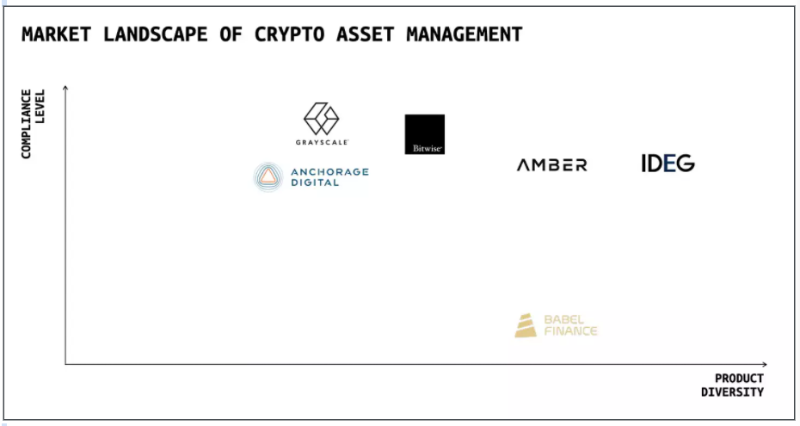

Jump Trading, GSR, Alameda Research, and IDEG are leaders in this space. IDEG is a fully regulated asset management firm headquartered in Singapore. Its trading team has built professional high-frequency trading systems, providing liquidity across multiple digital exchanges. As a result, IDEG enjoys the best fee structures and lowest latency on most exchanges. With these advantages, the company can serve its clients more effectively.

2.3 Trading Desks

Trading desks are another common form of asset management service. Like brokerage services in traditional finance, clients can buy or sell specified assets through the desk based on their preferences. The capabilities of the firm's trading team determine the types of services offered. While most trading desks only provide basic spot trading, others offer diverse strategies including arbitrage, CTA, and options strategies.

Genesis Trading, Amber Group, OSL, and IDEG excel in trading operations. Leveraging robust internal high-frequency trading systems, IDEG has developed multiple trading strategies for clients. Quantitative arbitrage strategies offer clients products similar to fixed-income instruments—denominated not only in USD but also in BTC, ETH, or other cryptocurrencies. Algorithmic trading strategies help clients buy or sell crypto assets at better prices. Finally, hedging strategies protect clients against specific risks.

2.4 Custody

Custody is a crucial service in finance, effectively eliminating operational risk by introducing one or more approvers. In the crypto industry, there are three types of custody services:

Standard custody, similar to traditional services, such as Bitgo and Copper.

Exchange-based custody, useful when underlying assets are frequently traded on exchanges. Both Binance and Coinbase support this model.

Self-custody, a more native crypto approach, typically used by DAOs and protocols, where clients manage assets via multi-party computation solutions. Fireblocks and Gnosis Safe offer such services.

Asset management firms are primary users of custody services to ensure the security of digital assets. Custody should align with corresponding products to truly enhance security.

For instance, when designing trust products, IDEG selects Binance and Coinbase as custodians for exchange-traded products, while using Gnosis Safe for its DeFi products.

2.5 Trusts

Asset management firms typically issue financial products to manage client assets. In the crypto industry, most financial products are issued as funds. However, some regulated firms can raise capital through trusts. Trust products offer several advantages:

With a corporate trustee, limited liability may be possible;

This structure offers greater privacy than a corporate entity;

Distributions among beneficiaries can be highly flexible;

Trust income is typically taxed as personal income.

Trackers

Tracker products actively follow either a single digital asset or a basket of digital assets, aiming for enhanced returns. In single-asset trackers, IDEG’s trading team employs quantitative arbitrage strategies to boost yields. The firm charges a spread based on enhanced returns rather than total returns—highly beneficial for clients bullish on the crypto market.

In basket products, IDEG’s professional investment team selects optimal underlying assets based on fundamental and market analysis. Additionally, the team actively manages positions to improve returns.

Yield Products

Yield products offer clients stable or fixed returns. Unlike many competitors that pay interest from loan business profits, IDEG generates income for its yield products through quantitative arbitrage trading—carrying significantly lower risk.

Mining

IDEG’s Bitcoin mining products offer high returns. Its sister company, Atlas Technology, is one of the world’s largest Bitcoin mining firms. Through refined management, Atlas Technology achieves above-industry-average returns, making IDEG’s mining products highly competitive.

Emerging Opportunities

The crypto market remains at the forefront of technological innovation, vastly different from traditional markets. This demands cutting-edge multidimensional risk strategies to adapt to new innovations and uncover hidden profit opportunities. IDEG’s years of professional research help clients select protocols, time unique opportunities, monitor performance, rebalance risk allocations, and hedge against appropriate market and counterparty risks.

Structured Products

IDEG customizes products for diverse risk appetites. For example, Bitcoin miners’ income closely correlates with Bitcoin’s price, exposing them to significant risk. IDEG uses derivatives structures to smooth miners’ income and eliminate such risks.

3. Challenges in Crypto Asset Management

Extremely high growth rates have attracted numerous speculators into the crypto market, and lending services amplify their leverage. The crypto industry lacks a credit system, allowing large institutions to easily obtain loans from multiple lenders without disclosing their positions or leverage. When the market declines and liquidations are triggered, a chain reaction ensues, causing financial panic. Recently, Three Arrows Capital, Celsius, Voyager, and Babel all suffered severe liquidity crises, severely harming both clients and themselves.

Crypto lending boomed during the pandemic, as retail investors speculated wildly, driving up prices. From early 2020 to early 2022, Voyager’s user base grew from 120,000 to 3.5 million.

3.1 Low Profit Margins

Like traditional banks, savings and lending businesses operate on thin margins. According to Gurufocus, most traditional banks have an ROA of only around 1%. Although crypto asset managers’ AUM is relatively smaller than banks’, their fixed costs remain similar. This renders most digital asset management firms unprofitable, forcing some to take on additional risks to seek extra profits.

3.2 Lack of Regulation

Unregulated underground credit operates at scale, with many CeFi institutions conducting massive unsecured lending among each other. While somewhat normal—similar to interbank lending in traditional finance, which helps optimize capital and risk allocation—it differs in that the crypto industry lacks standardized, transparent, and supervised credit markets.

Credit lending between CeFi entities occurs in an unregulated manner, without peer oversight or disclosure. We can only consider these loans as underground transactions, preventing positive market mechanisms from functioning. For example, Three Arrows Capital once held $18 billion in assets and, after losing hundreds of millions in the LUNA collapse, borrowed billions in unsecured credit from over twenty CeFi institutions.

These lenders were unaware of Three Arrows’ actual asset condition, the intended use of funds, or how much else it had borrowed from other institutions. As a result, after Three Arrows’ bankruptcy, several lenders—including Voyager and Celsius—were dragged into a cascade of bankruptcies and restructurings. This case illustrates how dangerous non-market-driven underground credit transactions can be.

3.3 Poor Risk Management

CeFi institutions often come from trading backgrounds and frequently engage in leveraged trading themselves. During bull cycles, institutions that aggressively leverage tend to stand out and achieve explosive growth in asset size. Thus, in a CeFi world accustomed to judging success by asset size and growth rate, winners are often those who boldly increase leverage and expand exposure. This risk appetite and management style is undoubtedly a root cause of the recent wave of defaults.

4. Solutions

Despite these challenges, we believe centralized asset management firms still play a vital role in the crypto industry. Below are some potential solutions we consider useful:

4.1 Diversified Business Models

Savings and lending businesses have low margins and are heavily dependent on asset management. However, loan demand is constrained by market size. Firms can diversify their operations to increase profitability.

4.2 Regulation

Many CeFi institutions engage in high-risk speculative activities such as derivatives and leveraged trading. While there’s nothing inherently wrong with speculation using their own funds, the lack of disclosure and oversight often leads them to use funds raised for other purposes to speculate, crowding out liquidity that should go to productive sectors.

In traditional finance, proprietary trading is strictly regulated. Proprietary trading ("prop trading") refers to banks or firms trading stocks, derivatives, bonds, commodities, or other financial instruments on their own accounts using their own capital, not client funds.

During the 2008 financial crisis, prop traders and hedge funds were among the entities scrutinized for contributing to the crisis. The Volcker Rule was introduced to strictly limit proprietary trading, regulating how prop traders operate and how much risk financial institutions can take. A key goal is to prevent conflicts of interest between firms and their clients.

4.3 Risk Management

Risk exposure can take many forms. CeFi institutions need to establish disclosure and risk assessment mechanisms across dimensions such as scale, duration, directional bias, volatility, liquidity, and concentration. Furthermore, assets and liabilities must be matched within portfolios to mitigate liquidity risk and avoid maturity mismatches in borrowing and lending. Given rapid market changes, risk exposure must also adjust quickly, requiring daily risk management practices and adjustments.

A healthy and well-functioning funding market plays a critical role in economic sustainability, and well-designed risk management frameworks are essential for driving industry growth.

4.4 Institutional Custody of Assets

Knowing your counterparties and their risk frameworks is crucial. You should also ask your brokers, market makers, exchanges, and prime brokers about their default protection measures, where they hold your assets, and what procedures are required to transfer your assets.

In traditional finance, custody requirements for registered funds are governed by the Investment Company Act of 1940 (commonly referred to as the "40 Act"), which mandates that third-party entities securely hold investors' assets to minimize risks of theft or loss. This is the primary purpose of custody.

Coinbase and Binance have launched custodial sub-account services. With this product, withdrawals are fully controlled by clients, while fund managers can trade directly using the sub-account without transferring client assets to other accounts.

5. Conclusion

In summary, we believe the most important aspects of crypto asset management are product diversification and regulation. Most firms in the asset management industry are moving toward these two directions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News