What are the similarities and differences between the Three Arrows Capital crisis and the Lehman Brothers collapse?

TechFlow Selected TechFlow Selected

What are the similarities and differences between the Three Arrows Capital crisis and the Lehman Brothers collapse?

What awaits the crypto world?

Author: yikiiiii.eth

Recently, both Chinese and international media have likened the liquidation of Three Arrows Capital (3AC) to the "Lehman Moment" of the crypto industry. However, there has been little in-depth discussion about how exactly these two events are similar or different.

I reviewed the origins and progression of the 2008 financial crisis and broke it down for comparison with the Three Arrows crisis, hoping to draw lessons from traditional finance that could offer insights into risk management and regulatory foresight within crypto.

It is evident that the triggers and transmission mechanisms of the two financial crises are highly similar. Yet because they occurred in very different financial ecosystems—banks & real estate versus hedge funds & digital assets—their systemic impacts differ greatly, as does the willingness of governments to intervene through bailouts and regulation.

Below is a brief recap of the 2008 Lehman crisis and a side-by-side comparison with 3AC:

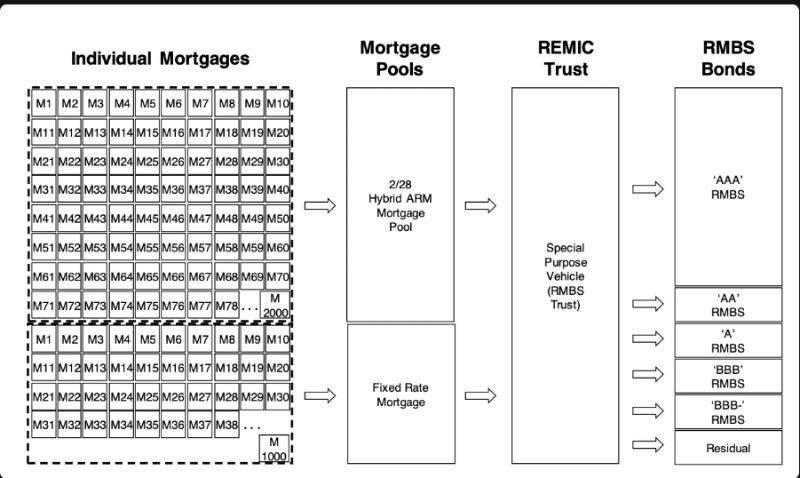

The 2008 subprime mortgage crisis originated when securitized banks packaged residential mortgage loans into bonds for sale. These home loans varied widely in risk rating, but we all know how the story ended: many borrowers had no jobs or income and were completely unable to repay.

However, by bundling them together, subprime loans achieved theoretical risk diversification, resulting in higher credit ratings and smooth sales. Thus, illiquid mortgage-backed bonds became Mortgage-Backed Securities (MBS), which generated cash flow for banks.

This practice of selling securities by securitization banks differs significantly from traditional banking activities like taking deposits and making loans. High leverage risks emerged here. Traditional banks operate under central bank-regulated reserve requirements, with strict oversight on lending volumes, and the central bank acts as lender of last resort. In contrast, securitized banks sell securities whose prices are determined entirely by the market—meaning their effective collateral ratios are market-driven, without any government backstop or central bank support.

But then why would anyone be foolish enough to buy these "junk bonds" lent to unemployed individuals?

The answer lies in the expectation of rising housing prices. As long as property values increased over one or two years, even those unable to repay could offset debt with home equity appreciation.

In times of economic euphoria, people often fail to see looming dangers.

The fragility of MBS lies in this: once home prices stagnate or fall, consensus breaks, triggering a domino effect of runs and death spirals. When mortgage defaults begin, MBS collateral quality deteriorates, causing market-priced MBS values to drop. This reduces real estate credit availability, further fueling market concerns about repayment capacity. This self-fulfilling and self-reinforcing cycle leads to bank runs—banks are forced to sell MBS collateral assets. Due to short-term liquidity shortages, fire sales drive down housing prices further, pushing MBS prices lower again, restarting the downward spiral.

Similarly, the collapse of Three Arrows Capital in 2022 followed a nearly identical logic.

Three Arrows Capital was a hedge fund investing across primary and secondary crypto markets. At its peak, it managed over $10 billion in assets and ranked among the most active investment firms in the cryptocurrency space. It was also considered one of the largest borrowers, with ties to Celsius, BlockFi, Genesis, and others. Like securitized banks, this exposure laid the groundwork for its debt risk.

Based on public information, 3AC’s liquidity crisis began amid a broader crypto market downturn, linked to LUNA's collapse, Celsius' insolvency, and failed BTC investments.

●Market misjudgment leading to GBTC discount. Leveraged purchases of BTC led to margin calls as BTC continued to decline.

● Previously invested heavily in Luna (now LUNC), which lost hundreds of billions in value. 3AC suffered near-total losses—up to 99.9%—on its multi-hundred-million-dollar investment in Luna.

● The Celsius meltdown triggered liquidations, forcing 3AC as a borrower to repay debts, leading to continuous stETH sales (for ETH) to cover obligations, causing stETH to depeg and amplifying market panic and price declines.

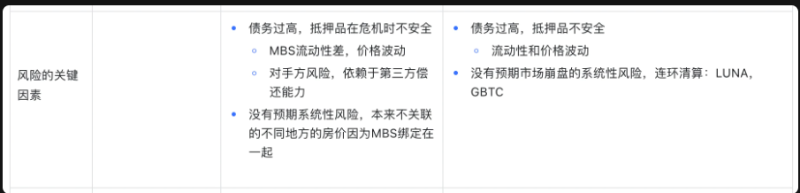

The key risk factors behind Lehman and Three Arrows are strikingly similar: excessive leverage, unstable collateral, and misjudgment of systemic risk explain their extreme vulnerability during market downturns.

● First, excessive debt and unstable collateral.

Under liquidation or extreme conditions, both Lehman’s MBS and 3AC’s stETH revealed poor short-term liquidity, leading to massive price volatility. Moreover, unlike government bonds, MBS also depend on third-party repayment ability, exposing them to counterparty default risk.

● Second, underestimation of systemic risk.

For example, MBS risk models assumed low correlation between housing markets in different regions—say, New York and Illinois—so bundling them appeared to spread risk. But in reality, the act of packaging itself created interdependence, introducing systemic risk. Similarly, 3AC underestimated correlations among crypto assets—from LUNA to Celsius to BTC—where systemic risks become glaringly apparent during crashes.

However, due to the high level of systemic risk posed by the subprime crisis, the U.S. government eventually stepped in as mediator and backstop. Measures included facilitating bankruptcies and acquisitions, partial nationalization of failing institutions, providing emergency loans to insolvent banks, and cutting interest rates to stimulate the economy.

● In contrast, there is no government backstop in crypto.

In traditional finance, governments facilitate takeovers; after 3AC’s collapse, however, large institutions resorted to mutual liquidations. When 3AC sought loans from other entities, such requests likely fell far outside standard risk controls and were mostly rejected. Only stronger players like FTX attempted to play the role of central bank, intervening to stabilize markets—but compared to the U.S. government’s aggressive actions in 2008, their efforts appear woefully inadequate.

History repeats itself. Perhaps the new regulations introduced by the U.S. after 2008 can serve as reference points for the future of crypto regulation.

After 2008, the U.S. significantly strengthened financial oversight. To reduce systemic risk, new rules limited the size of financial institutions and separated commercial and investment banking.

By comparison, crypto market turmoil poses nowhere near the systemic threat of the 2008 crisis. While it may prompt some regulatory attention, governments are unlikely to step in to rescue the market. On June 22, Federal Reserve Chair Jerome Powell stated that cryptocurrencies require better regulation, but so far, their sharp declines have not produced significant macroeconomic effects.

If future crypto regulation tightens—restricting borrowing and leverage—it’s conceivable that measures might include requiring CeFi platforms to improve transparency and report fund usage, or demanding large-cap DeFi protocols to disclose sources of bond issuance and APY yields.

Finally, after 2008, the U.S. and indeed the global economy entered a real recession: credit contracted sharply, consumption, employment, and output plummeted, with investment only returning to pre-crisis levels by 2013.

What awaits the crypto world?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News