Venture Capital DAO: A New Paradigm for Venture Capital in the Web3 Era?

TechFlow Selected TechFlow Selected

Venture Capital DAO: A New Paradigm for Venture Capital in the Web3 Era?

In the future, will there be more successful venture capital DAOs?

Y Combinator and BVP have both established their own DAOs. So what exactly is a venture capital DAO? And if we look at the industry’s history, are there still new structural and model possibilities for the future of venture capital?

What is YC's Orange DAO? Could hybrid models (DAO + traditional) of venture capital firms emerge in the future? Will DAOs one day replace traditional venture capital firms altogether? These are the questions this article seeks to explore.

Key Takeaways

The U.S. Small Business Investment Act of 1958 formally allowed financing and management of small entrepreneurial businesses in the United States, which helped catalyze the rise of early private equity firms on a macro level.

With technological advancements, starting from Kleiner Perkins and Sequoia Capital in 1972, venture capital gradually began investing in semiconductor and early computer companies.

In 1974, the U.S. stock market crashed, causing a temporary downturn in the venture capital industry. The broader market remained cautious about this new investment structure.

The success of DEC and Apple in the late 1970s and early 1980s revealed profit opportunities, fueling further growth in venture capital. While only dozens of VC firms existed in the early 20th century, by the late 1980s, the number exceeded 650.

The emergence of the World Wide Web (Web 1.0) in the early 1990s revitalized the venture capital landscape. Investors recognized that many high-potential companies were emerging during this wave. Netscape and Amazon were founded in 1994, Yahoo in 1995—each received venture funding.

Although legacy VC giants often claim their capital is superior, solo GPs can unite other top-tier GPs into a “super team.” Such energetic organizations increase startups’ odds of success.

The core goal of a DAO is to provide future enterprises with a new decentralized business model through programmable incentives distributed among token holders—essentially forming a new type of (online) organization.

Investment DAOs are typically managed and operated via smart contracts. Given the involvement of investments, they also adopt legal structures offering liability protection. Due to differing regulatory frameworks across U.S. states, DAO registration varies by jurisdiction.

Venture-focused DAOs targeting crypto have become a new model for sourcing deals and connecting with founders—an activity once dominated by star investors and traditional VCs.

DAO power may grow over time. However, some VCs argue that DAO-based models still lag behind traditional firms in operational capability and efficiency.

Investment DAOs also carry crypto-related risks such as regulatory scrutiny, poor treasury management, or untested technical vulnerabilities. Individual DAO performance records matter and help distinguish mature DAOs from the crowd.

History of Venture Capital

Before WWII

Early investment behaviors resembling modern venture capital originated with financial dynasties like J.P. Morgan, the Wallenbergs, Whitneys, Rockefellers, and Warburgs. These families invested heavily in various companies. A notable example is the Wallenberg family founding Investor AB in Sweden in 1916, becoming an early backer of firms like ABB and Ericsson in the first half of the 20th century.

After 1945

True venture capital institutions emerged after World War II. In 1946, Georges Doriot—the "father of venture capital"—alongside Ralph Flanders and MIT’s former president Karl Taylor Compton, founded American Research and Development Corporation (ARDC). Its main purpose was to encourage private-sector investment in businesses run by returning WWII veterans. Around the same time, J.H. Whitney & Company was also established.

ARDC broke the mold of family-led investment. Notably, its 1957 investment in Digital Equipment Corporation (DEC) paid off massively—when DEC went public in 1968, it was valued at over $355 million, more than 1,200 times ARDC’s initial stake.

Later, early employees from ARDC spun out to found several prominent VC firms, including Greylock Partners and Fidelity Ventures.

Macro Support and the Growth of Venture Capital

Beyond individual initiatives, macro-level policies also accelerated the industry. The 1958 U.S. Small Business Investment Act officially enabled financing and oversight of small startups, significantly boosting the rise of early private equity firms.

During the 1960s and 1970s, VC firms focused on launching and scaling companies. But beginning in the 1960s, the prototype of today’s private equity fund began to take shape. What did it look like?

Specifically: Private firms increasingly organized investments through limited partnerships, where general partners (GPs) manage operations and limited partners (LPs) provide capital—the primary source of fundraising.

Venture Capital and Technology Waves

As technology advanced, starting in 1972 with Kleiner Perkins and Sequoia Capital, venture capital began actively investing in semiconductor and early computing companies.

In 1973, as the number of new VC firms grew, the National Venture Capital Association (NVCA) was formed.

However, no industry grows without turbulence.

In 1974, the U.S. stock market collapsed, leading to a brief slump in venture capital. The market approached this novel investment model with caution.

The success of DEC and Apple in the late 1970s and early 1980s showed clear profit potential, accelerating VC expansion—from just dozens of firms in the early 20th century to over 650 by the late 1980s. At that point, nearly every firm was hunting for the next big winner.

Yet, the IPO market cooled in the mid-1980s, culminating in the 1987 crash. By the late 1980s, oversupply of IPOs and inexperienced investment managers led to constrained growth throughout the 1980s and early 1990s.

The emergence of the World Wide Web (Web 1.0) in the early 1990s reignited the venture capital sector. Investors realized a wave of highly promising companies was forming. Netscape and Amazon launched in 1994; Yahoo in 1995—all backed by venture capital.

Success stories like AOL, UUNet, Spyglass, Netscape; later Lycos, Excite, Yahoo, CompuServe, Infoseek, C/NET, E*Trade, Amazon, ONSALE, Go2Net, N2K, NextLink, and SportsLine became legends of the era.

These iconic companies delivered massive returns to VCs. High returns and strong IPO performances triggered a boom in new venture fund formation.

From around 40 VC firms in 1991, the number surged to over 400 by 2000.

Still, the industry faced setbacks. In 2000, the dot-com bubble burst—many VC firms collapsed, and tech startup valuations plummeted. Over the next two years, numerous venture firms were forced to shut down.

Cycles continued. By 2010, the industry began recovering. In 2020, total VC funding reached $80 billion, with investment focus gradually shifting toward what we now call the Web3 era.

Dynamics of Change in Venture Capital

Having reviewed the history of venture capital, let’s now examine recent industry shifts.

Amid the pandemic, global remote collaboration has become the norm. During this period, new characteristics of the venture capital industry have emerged across the internet and the world.

We can abstract these trends as follows:

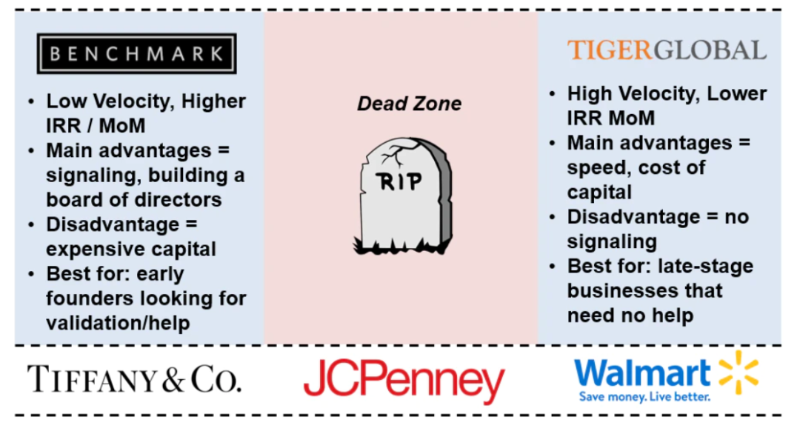

Rise of Solo GPs: On how VCs succeed in the industry, Everett Randle in his essay “Playing Different Games” offered insights: a VC firm can choose to become a marquee firm (like Benchmark) or a low-cost capital provider (like Tiger Global), but being stuck in the middle can be problematic, as shown below:

Image source: Not Boring

To some extent, this holds true for large funds managing hundreds of millions of dollars.

However, another category exists—one that plays by entirely different rules and performs well: solo GPs. Although the value provided by VCs has become commoditized, their cost structure doesn’t always support sustainable operations.

Specifically, the capital (“ammunition”) held by VCs is essentially a commodity subject to dynamic equilibrium. Firms must compete fiercely for deals. Large VC funds unable to secure positions amid intense competition for hundreds of millions in allocations risk missing key opportunities.

Meanwhile, firms pursuing extreme differentiation—whether through strong branding or low capital costs—can find their niche.

Like individual creators, solo GPs, micro-fund managers, or self-funded investors have distinct advantages. For instance, with a $5M fund, investing $100K in a startup that later achieves a 250x valuation means even if the other $4.9M fails, the fund still generates a 5x return—enough to satisfy LPs.

Such solo GPs often possess strong individual energy, laying the foundation for collaborative venture models:

Legacy VC firms often tout the superiority of their capital, but solo GPs can assemble other top-tier GPs into a “super team.” This energetic collective increases a startup’s likelihood of success.

While a16z won’t refer deals to Benchmark, solo GPs and angel investors frequently introduce outstanding founders to peers. Leveraging this energetic collaboration, some solo GPs raise larger funds and attract other high-energy individuals, making them more appealing to founders.

Individual collaboration is faster than institutional competition. We may see more high-performing solo GPs form dynamic super teams, competing to lead rounds and offering concentrated value as a competitive edge.

We already know collaboration improves efficiency—this could define the future of venture capital. But how does this relate to decentralized autonomous organizations (DAOs)?

Decentralized Autonomous Organizations (DAOs)

Before diving deeper, let’s clarify what a DAO is:

A DAO is a blockchain-based, decentralized organization governed by smart contracts. Unlike traditional centralized companies with hierarchical management, DAOs are typically governed by native tokens (yes, the same tokens discussed in that Token Economics article).

Through software programs and smart contracts, DAOs automate functions traditionally performed by humans, enabling members with shared goals to share risks and rewards equally.

The core goal of a DAO is to offer future enterprises a new decentralized business model, using programmable incentives distributable among token holders—essentially creating a new type of (online) organization.

Core Features of DAOs (Partial List):

Clear Structure and Roadmap: Organizational vision is co-defined by members who control and shape the DAO’s future.

Equal Voting Rights: All members vote on major decisions.

Rules Codified Upfront: Automated decision-making reduces human error, insider manipulation, etc. DAO rules are transparently encoded in software.

Open-Source Code: DAO code is publicly accessible.

Token-Based Governance: In many DAOs, holding the DAO’s token grants voting rights.

Note: Bitcoin might be considered the first fully functional DAO, with programmable rules and autonomous operation via consensus; miners and nodes signal votes through participation.

Venture Capital DAOs Are Emerging

We observe that venture capital DAOs are rapidly emerging. Could this new organizational model evolve into something transformative?

Consider this data point: according to DeepDAO, DAOs exploded in 2021. From just 13,000 users across all DAOs in January 2021, membership surpassed 1.6 million by December—over a 130x increase year-over-year.

Moreover, crypto-focused investment DAOs have become a new paradigm for deal sourcing, founder engagement, and closing investments.

Note: These activities were previously exclusive to star investors and traditional VCs.

Investment DAOs

As DAOs evolve, they now serve diverse communities and business needs. Investment DAOs and venture DAOs have become a new organizational form and a method for early-stage investing.

What Are the Characteristics of Investment DAOs?

Investment DAOs are typically managed and operated via smart contracts. Since investments are involved, they also establish legal structures to protect members from liability. Given varying U.S. state regulations, DAO registration depends on local laws.

However, the investment process in a VC DAO differs from traditional funds: each member can act as a lead investor and propose deals. Investment decisions are made via DAO-wide voting rather than through an Investment Committee (IC).

Depending on the DAO’s smart contract, members may have the right to “exit” or withdraw at any time—though traditional VC funds usually require investors to stay committed for a set duration.

For example, Joyce Yang, founder of Global Coin Research, believes her DAO aims to disrupt traditional VC by democratizing crypto investments and opening access to those previously excluded. Yet, as a nascent model, DAOs haven’t yet proven themselves across market cycles. Their current popularity stems largely from market enthusiasm and top-tier VCs' bullish stance on crypto and Web3 ventures.

How Do They Source Deals and Connect with Top Founders?

A "venture DAO" is a collective of individuals interested in crypto, pooling personal or group capital into early-stage crypto startups.

Typically, members of investment-focused DAOs must:

① Purchase the DAO’s governance token in advance

② Gain access to gated channels—such as invite-only Discord servers, Telegram groups, or private events—where deal sourcing and negotiations occur.

Take Global Coin Research (GCR) members as an example: they’ve collectively invested in over 30 startups, deploying more than $25 million into projects like Aurora (a cross-chain interoperability protocol) and Coinvise (a Web3 management platform).

(To participate in deals, individual DAO members must be accredited investors—typically defined as individuals legally authorized to purchase unregistered securities.)

A Result: As of December 2021, GCR estimated average returns exceeding 40x across its portfolio projects that had launched or become market-traded.

Michael Steinberg, founder of Reciprocal Ventures, argues: Crypto enables smaller VC firms to thrive because crypto project returns can reach hundreds or even thousands of times initial investment.

Steinberg believes VC DAOs are reshaping angel investing. As a passive investor, accessing founders directly is difficult.

With a DAO, there’s no gatekeeping intermediary—you’re part of a battle-ready squad.

Community Support

What benefits can founders gain from engaging with a DAO?

First, for early-stage crypto startups, acquiring users and achieving product-market fit remains a fundamental challenge.

Jenil Thakker, founder of Coinvise, shared his experience collaborating with GCR and another VC DAO, “The LAO”: “By co-hosting events with GCR, new members joined Coinvise’s community, accelerating our growth. More broadly, VC DAOs offer access to wider networks, enabling rapid feedback on projects.”

For Coinvise—a DAO infrastructure provider—GCR helped test its product, including launching GCR’s governance token on the Coinvise platform.

“Today, having a community is increasingly critical when raising funds. Founders want not only a crypto-native team to validate their product but also a feedback loop.” According to Thakker, most VC DAOs even offer media, recruitment, and legal support to portfolio companies.

"Often, traditional VCs charge high fees for these services."

YC: Orange DAO

Now let’s discuss Orange DAO, founded by YC alumni:

Image source: Near

Y Combinator: a renowned startup accelerator and investment platform for internet-based companies in the U.S.

Founded in fall 2021 by several YC alumni, Orange DAO aims to build a VC organization supporting crypto startups. It has since attracted over a thousand YC alumni.

According to Orange DAO’s official charter: "Orange DAO helps crypto startups apply to venture funding, supports founders in joining Y Combinator, enhances leadership skills, and provides hiring and operational guidance."

Currently, over a thousand founders in Orange DAO’s Discord channel are YC alumni. Y Combinator has backed over 3,300 companies. The initiative is co-led by Ben Huh, an entrepreneur who led YC’s New Cities program in 2016.

The Orange DAO (nicknamed by the author) verifies identity by linking wallet addresses to HackerNews profiles associated with YC. Each member mints a unique, non-transferable NFT to confirm alumni status and gain participation rights.

Orange DAO isn’t the first attempt to leverage YC’s vast alumni network. Back in 2017, hundreds of YC alumni launched Pioneer Fund—a more traditional VC effort aimed at leveraging past YC founders’ expertise for deal flow.

Ultimately, DAOs represent collective power rather than individual strength. Some believe DAOs are the next evolution of companies, abstracting visions and rules into code.

Syndicate, a DAO startup, helps these groups launch and navigate complex regulatory issues. Papper assisted the ConstitutionDAO team with complexities in the Sotheby’s auction bid and guided Huh’s early efforts around Orange DAO. Orange DAO’s structure is somewhat unconventional—an effort to balance innovation with compliance under securities law.

The actual fund supporting startups, Orange Fund, is a separate legal entity managed by Huh and several other GPs. It has closed its initial fund and invested in about 30 startups, including DeFi firm Goldfinch.

“We’ve found a way to combine the investment entity with the DAO structure—they remain independent but work together,” said Huh. “Our direction is clear: strictly follow what the smart contracts dictate.”

The DAO itself operates via committees—organizing over 1,000 members into smaller working groups. A core principle, according to Huh, is rewarding members who contribute more to individual deals with internal governance tokens. However, concerns have been raised (per TechCrunch) about transparency regarding how fund performance translates into DAO member returns. Still, the Orange Fund GPs state they will contribute carried interest back into the Orange DAO ecosystem.

Initially named “YC Crypto DAO,” the group rebranded to reflect broader ambitions, adopting a new name and mascot—a pixelated orange wearing glasses, nicknamed “abundant returns.”

DAO + Non-DAO: The Hybrid Future

After reviewing these cases, we must ask: Will DAOs eventually replace traditional venture capital firms?

As crypto’s market cap has grown to $3 trillion, investors and VC capital have poured into this booming sector chasing extraordinary returns. Different investment-driven DAOs have developed distinct identities—such as Komorebi Collective and FlamingoDAO, both focusing on female-founded startups.

Some argue crypto VC is a full-time job. Traditional VC firms are deeply involved, dedicating significant time and resources to portfolio companies.

Perhaps DAO influence will grow over time. Yet, others maintain that DAO-based VC models still lag in operational efficiency compared to traditional firms. “From what I see, projects value individual DAO members’ strengths and collaboration, but most still prefer traditional funds to lead rounds.”

However, as DAOs gain increasing equity stakes in startups, a hybrid model appears to be emerging—one that combines the community-driven spirit of DAOs with the deep pockets and operational expertise of traditional VCs.

Investment DAOs also face crypto-specific risks: regulatory scrutiny, poor treasury management, or untested technical flaws. Individual DAO track records are crucial, helping mature DAOs stand out.

But in bull markets, remember: ultimately, startup founders hold the power in choosing investors.

"As Kaczmarczyk of Third Prime says: 'Founders should pick investors whose vision aligns best with theirs and who give them the highest chance of success. If DAOs can do that, great.'"

Conclusion

DAOs are a recent innovation in the crypto community, and venture DAOs represent a unique use case. They’ve shifted fund operations onto blockchains, introducing greater transparency to traditionally opaque processes.

However, regulations have yet to catch up with the boundary between DAOs and legal entities—this remains a key risk and explains why many DAOs adopt hybrid models combining traditional legal structures with on-chain governance. Despite challenges, the success of MetaCartel Ventures and The LAO shows venture DAOs have carved out a legitimate space within the crypto ecosystem.

Advantages of Venture Capital DAOs:

Enables broader participation in early-stage investing

Provides strategic capital to new projects

Offers financial diversification

Strengthens network effects within blockchain protocols

Democratizes investment decisions and expands deal sourcing

Disadvantages of Venture Capital DAOs:

Regulatory uncertainty: legal, securities, and tax considerations remain major hurdles

Risks and limitations of smart contracts: hacks, immutability, bugs

Limited retail investor participation depending on jurisdictional rules

Do you think we’ll see more successful venture capital DAOs in the future?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News