Bitget UEX Daily Report | Escalating U.S.-Iran tensions heighten oil price risks; U.S. May CPI, TSMC’s May revenue, and Oracle’s earnings report due

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Escalating U.S.-Iran tensions heighten oil price risks; U.S. May CPI, TSMC’s May revenue, and Oracle’s earnings report due

Overall, volatility has increased, but the medium- to long-term growth narratives—such as AI and stablecoin innovation—remain resilient. We recommend focusing on data-driven opportunities and risk management.

I. Top News

Federal Reserve Updates: Fed Officials Maintain Cautious, Wait-and-See Stance

- Markets await the release of U.S. May CPI data to assess inflation trends and the outlook for rate cuts.

- Recent geopolitical tensions have not significantly altered the Fed’s baseline economic assessment.

- Analysis: A moderate CPI print could strengthen expectations for rate cuts this year; however, upside risks from oil-driven imported inflation may complicate decision-making—providing near-term support for the U.S. dollar while weighing on risk assets.

Global Commodities: Renewed U.S.-Iran Tensions Raise Risks of Global Oil Supply Disruption

- Iran launched missiles and drones targeting U.S. military facilities in the region; the U.S. responded with a second round of self-defense strikes against Iranian air defense and radar systems.

- The U.S. Department of Energy warned that global oil inventories are rapidly declining to multi-year lows.

- Trump signaled potential involvement in Iran’s post-conflict reconstruction—but conditioned it on sharing access to oil resources.

- Analysis: Geopolitical conflict directly lifts crude oil’s risk premium; combined with low inventories, this provides near-term price support. Longer-term direction hinges on escalation intensity and diplomatic progress.

II. Market Recap

Commodities & FX Performance (Real-Time Updates)

- Spot Gold: ~$4,233/oz, down ~1.3% over 24h.

- Spot Silver: ~$65/oz, down ~1.15% over 24h.

- WTI Crude: ~$90/bbl, up 1.79% over 24h.

- Brent Crude: $93.13/bbl, up ~1.84% over 24h.

- U.S. Dollar Index (DXY): ~100.007, nearly flat over 24h with minor fluctuations.

Key Drivers: Escalating U.S.-Iran tensions stoked concerns about Middle Eastern oil supply disruption, while the DOE’s inventory warning amplified the geopolitical risk premium—pushing oil prices higher. The relatively stable DXY reflects investors’ risk-averse positioning without extreme flight-to-quality behavior. Gold and silver were pressured by a strong dollar and shifting risk sentiment. In the near term, oil price momentum, U.S. CPI data, and evolving Fed expectations will drive cross-asset correlations: rising oil prices may rekindle inflationary pressure, constraining room for monetary easing, while gold’s performance—as a traditional safe-haven asset—will hinge on dollar strength and real yields. Consensus among institutions is that geopolitical uncertainty supports energy equities, though any de-escalation or negotiation breakthrough could trigger sharp pullbacks.

Cryptocurrency Performance

- BTC: ~$61,180, down ~1.34% over 24h.

- ETH: ~$1,640, down ~1.42% over 24h.

- Total Crypto Market Cap: ~$2.21 trillion, down ~1% over 24h.

- Liquidations: ~$424 million liquidated over 24h, including $324 million in long positions.

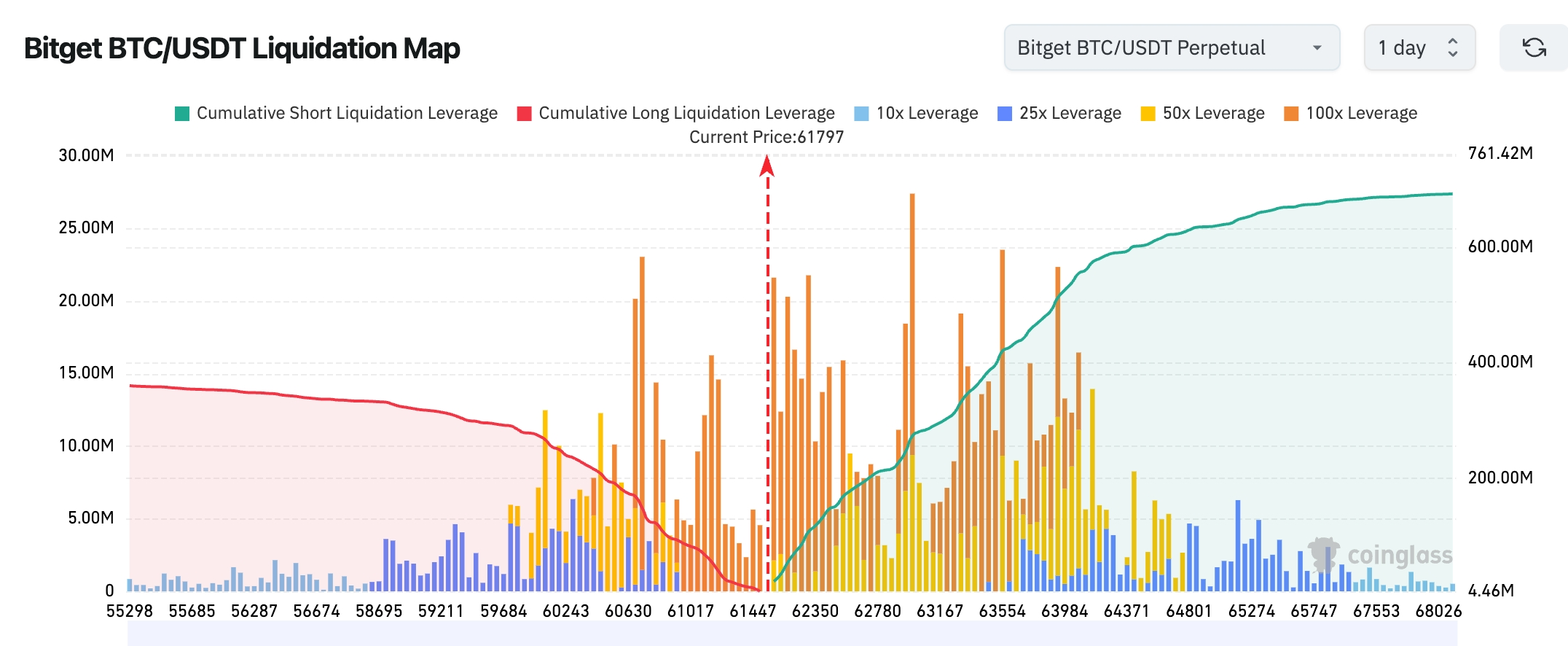

- Bitget BTC/USDT Liquidation Heatmap: Current BTC price ~$61,800. Major long liquidation zones have clustered near $60,500–$61,500, suggesting most highly leveraged longs have been cleared—releasing near-term downside momentum. However, market sentiment remains cautious. Notably, cumulative short liquidations above $63,500–$64,500 exceed $600 million—significantly surpassing downside long exposure. If BTC regains and sustains levels above $63,000 and breaks higher, a large-scale short squeeze could accelerate price gains toward the $64,000–$65,000 range.

- Spot ETF Net Flows: BTC spot ETFs recorded $94.1 million net outflow yesterday.

Key Drivers: Geopolitical tensions and broad-based tech sector weakness in U.S. equities converged to suppress risk appetite. SemiAnalysis reported delays in NVIDIA’s 800VDC power architecture and co-packaged optics (CPO) mass production timelines—directly undermining AI infrastructure growth expectations, triggering sector-wide selloffs that spilled over into crypto markets. Leveraged liquidations amplified volatility, with BTC and ETH moving in tandem but showing limited divergence. ETF flows turned cautious, reflecting mixed macro signals: stable dollar strength alongside rising oil prices. Technically, price action shows consolidation near key support levels. Institutional views suggest near-term digestion of event-driven shocks remains necessary; medium-term direction will depend on Fed policy signals and ETF flow dynamics. Overall posture remains defensive—watch for rebound potential amid geopolitical de-escalation or positive data surprises.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Closed ~50,872 (+0.17%), continuing modest stabilization.

- S&P 500: Closed ~7,387 (−0.26%), with pronounced sector divergence.

- Nasdaq Composite: Closed ~25,679 (−0.97%), weighed heavily by tech underperformance.

Tech Giants’ Performance

- NVDA: ~$208.19, −0.22%.

- AAPL: ~$290.55, −3.64%.

- MSFT: ~$403, −2.02%.

- GOOGL: ~$364.26, +0.26%.

- AMZN: ~$244.19, −0.42%.

- META: ~$584.59, −0.14%.

- TSLA: ~$396.68, −3.00%.

Summary & Driver Analysis: Broad index divergence emerged: the Dow proved relatively resilient, while the Nasdaq suffered under tech-led weakness. Delayed AI infrastructure rollout—particularly in optical and electrical components—hit “light” and “power” subsectors hardest. Apple’s Siri AI launch failed to meet expectations, further deepening sector splits, whereas some defensive or non-AI tech names held up better. Stock-specific drivers varied widely: NVDA was pressured by supply-chain concerns, GOOGL benefited from Gemini progress, and AAPL faced mounting competitive headwinds. Overall, the tech sector remains under pressure from macro uncertainty and event-driven shocks. Near-term valuation corrections may present opportunities—but geopolitical spillovers warrant caution.

Crypto Stock Futures Trading Data

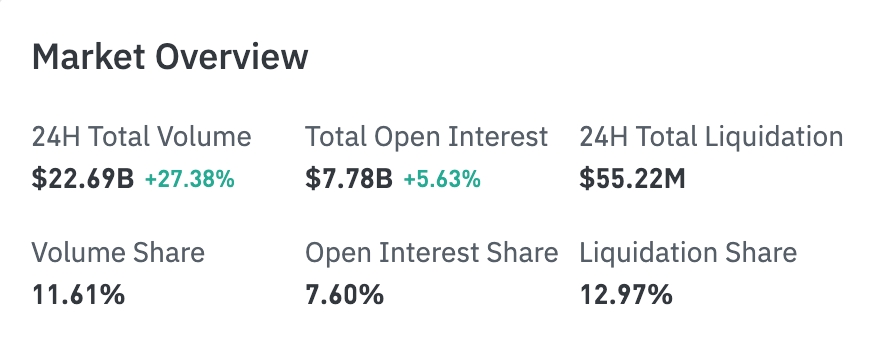

- 24H Total Turnover: $22.69 billion (+27.38%), indicating markedly improved trading activity.

- Open Interest (OI): $7.78 billion (+5.63%), signaling continued inflow of new capital.

- 24H Total Liquidations: $55.22 million.

- Turnover Share: 11.61%.

- OI Share: 7.60%.

- Liquidation Share: 12.97%.

Top Sector OI Rankings

- Technology: $1.14 billion (Rank #1)

- Financials: $147 million

- Consumer Discretionary: $66.65 million

- Biotech: $20.09 million

- Industrials: $17.24 million

Heatmap Capital Allocation (by OI)

Commodities (Highest Concentration)

- Gold (GOLD): $3.31 billion (largest single-position OI)

- Silver (SILVER): $747 million

- WTI Crude: $592 million

- Brent Crude (BRENT): $422 million

Technology Stocks

- NVIDIA (NVDA): $232 million

- Marvell Technology (MRVL): $191 million

- Google (GOOGL): $101 million

- Circle (CRCL): $97.6 million

- Intel (INTC): $94.65 million

- Tesla (TSLA): $79.8 million

- SanDisk (SNDK): Active position

Sector-Specific Observations

Semiconductor / Optical Communications: Sharp Declines

- Representative stocks:

- AAOI (Applied Optoelectronics): Down ~17.17% (close ~$162.88).

- COHR (Coherent Corp.): Down ~11.44% (close ~$355.94).

- MRVL (Marvell Technology): Down ~7.61% (volatile recent session).

- Others: Lumentum (LITE) and peers broadly fell 5–10%+.

- Drivers: SemiAnalysis reported further delays—now pushing NVIDIA’s next-gen architecture and CPO mass production to ~2028—due to yield, ASIC integration, and packaging bottlenecks (e.g., TSMC’s CoWoS). This dented near-term high-growth expectations for the AI optical module supply chain, triggering profit-taking and sector-wide contagion. Optical stocks had surged earlier on AI datacenter demand (some YTD gains >400%); this correction is typical event-driven pullback. Short-term valuations face pressure, yet long-term AI infrastructure demand narratives remain intact.

Cruise / Aviation Services: Relative Outperformance

- Representative stocks:

- CCL (Carnival): Up 3–8% recently (varies by session, influenced by oil prices and geopolitical developments).

- RCL (Royal Caribbean), NCLH (Norwegian Cruise Line): Broadly posted positive returns or demonstrated resilience.

- Aviation-related service providers (e.g., airlines benefiting from oil price swings) also saw rotational gains.

- Drivers: Amid U.S.-Iran tensions, defensive capital rotated from high-valuation tech/semiconductors into consumer services. Simultaneously, oil price volatility and potential de-escalation hopes eased fuel cost concerns for cruise and aviation operators. Strong underlying demand and improving booking volumes had already supported the sector; its relative strength now highlights market-style rotation amid uncertainty.

III. Deep Dive: U.S. Equity Highlights

1. Super Micro Computer (SMCI) – Equity Financing to Support AI Business

Overview: SMCI announced a $7 billion equity and convertible bond financing plan—including a $5 billion underwritten offering and a $2 billion at-the-market (ATM) program—to procure components and fulfill surging AI server orders. Market Interpretation: Institutions are monitoring dilution impact but affirm SMCI’s strategic role in AI server demand. Investment Takeaway: Near-term share price pressure likely; longer-term value depends on order execution and capital structure optimization.

2. Nuvalent (NUVL) – Acquisition by GSK

Overview: GlaxoSmithKline (GSK) agreed to acquire Nuvalent for $10.6 billion in cash ($124/share), representing a 40% premium to prior closing price, focused on targeted cancer therapies. Market Interpretation: Transaction well-received, underscoring big pharma’s commitment to innovative pipelines. Investment Takeaway: Similar deals may lift biotech valuations; monitor regulatory approval progress closely.

3. Samsung & SK Hynix – Korean Investment Plans

Overview: Both firms may soon announce expanded domestic investments—including advanced packaging facilities or wafer fabs—with Korea’s President set to discuss regional strategies with major conglomerates. Market Interpretation: Reinforces supply chain localization to mitigate global geopolitical and trade risks. Investment Takeaway: Positive for Korea’s semiconductor ecosystem; consider related supply chain investment opportunities.

4. SpaceX – IPO & AI Compute Progress

Overview: SpaceX accelerated orbital AI compute testing to 2027; its IPO has drawn several times oversubscription. Market Interpretation: Highlights long-term growth runway and attracts interest from major institutional investors. Investment Takeaway: Imminent listing offers a timely entry point—but valuation must align with execution capability.

IV. Crypto Project Updates

1. Carlos Domingo, CEO of Securitize, stated that tokenized equities could expand the RWA (real-world asset) market from its current ~$30 billion to $5 trillion. He noted that global equities and ETFs total ~$150 trillion; even just 2–3% tokenization would approach $5 trillion. Domingo believes tokenized equities—not private credit or sovereign debt products—will be the primary catalyst for this growth.

2. The U.S. House Ways and Means Committee held hearings on multiple crypto tax bills. Bipartisan lawmakers raised concerns over draft details, and no consensus has yet emerged. Proposed measures aim to reduce taxpayer compliance burdens—including exemptions for small-value transactions and elimination of double taxation on mining and staking rewards (i.e., taxation upon receipt and again upon sale).

3. On-chain analysts disclosed on X that a purported “private key leak” enabled attackers to continuously mint and dump tokens on BSC, issuing ~300 million new tokens and selling ~450 million total—netting ~$34 million in ETH and BNB.

4. CryptoQuant analyst MorenoDV noted Bitcoin demand has entered one of its most extreme contraction phases since 2019. Combined 30-day demand growth across spot and perpetual futures has fallen to ~−650,000 BTC—a threshold previously observed only three times historically. Concurrent contraction across both spot and derivatives demand signals broad-based weakness—not limited to leveraged speculation—but extending to institutional buying and derivative exposure. This implies fewer marginal buyers and diminished capacity to absorb sell-side pressure. Historically, the −650,000 BTC level has marked the onset of highly unstable market conditions—not an immediate bottom.

Analysts view the current environment less as a confirmed reversal and more as the opening phase of a final cleansing process. The most probable path involves initial volatility expansion, followed by a “numbing” price phase: weak momentum, compressed activity, and prolonged sideways consolidation. Psychologically, this phase may prove more damaging than the selloff itself.

V. Market Calendar

June 10 (Wednesday)

- U.S. May CPI Release: Key input for assessing inflation trajectory and Fed policy implications. ★★★★★

- Major U.S. Earnings: Oracle (ORCL) reports after market close (focus: AI cloud growth and guidance). ★★★★★

- TSMC (TSM) May Sales Report: Watchpoint for semiconductor supply chain health.

June 11 (Thursday)

- SpaceX IPO Final Pricing: One of history’s largest IPOs ($135/share, ~$75 billion expected proceeds, ~$1.77 trillion market cap)—a powerful catalyst for space/tech equities. ★★★★★ (plus major investor events)

- U.S. May PPI Release: Critical gauge of inflationary pressures (consensus expects notable increase).

- U.S. Earnings: Adobe (ADBE) reports after market close (AI software demand focus).

- FIFA World Cup USA-Mexico-Canada Opening (June 11–July 19): Related U.S. sports industry equities may draw attention.

June 12 (Friday)

- SpaceX Official NASDAQ Listing (Ticker: SPCX): Historic IPO debut—first day of trading, significant sentiment boost. ★★★★★

- U.S. Economic Data: June University of Michigan Consumer Sentiment (prelim.), June 1-Year Inflation Expectations (prelim.).

*This Week’s Core U.S. Equity Themes: “Super Event Week”: SpaceX IPO + Apple WWDC + Key Inflation Data (CPI/PPI) + Oracle/Adobe Earnings—set to dominate tech and macro sentiment. Focus on AI, tech infrastructure, and space-themed equities.

Institutional Views: Leading investment banks emphasize cautious optimism. Geopolitical tensions lifted energy prices, yet U.S. equity divergence reflects defensive capital rotation. Concerns over AI rollout delays weighed on tech valuations, while crypto markets oscillated amid macro uncertainty and leverage dynamics. Most institutions believe clarity on CPI data will help re-establish the Fed’s rate-cut path—supporting risk-asset rebounds. Energy and defensive sectors attract near-term preference, while tech stocks digest supply-chain news. Overall, volatility is rising—but long-term growth narratives (AI, stablecoin innovation) retain resilience. Prioritize data-driven opportunities and robust risk management.

Disclaimer: The above content was compiled via AI-powered search and verified manually prior to publication. It does not constitute investment advice. Data presented herein may contain unavoidable discrepancies; always refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News