MetaFi: The Rise of Metaverse Finance

TechFlow Selected TechFlow Selected

MetaFi: The Rise of Metaverse Finance

The Metaverse can be understood as an interface layer between the physical world and the virtual world, encompassing an innovative combination of hardware and software, but most importantly, it is an economic system that runs parallel to the traditional financial system.

Author: Outlier Ventures

Translation: TechFlow

Note: What happens when the Metaverse meets DeFi?

This is Outlier Ventures’ comprehensive analysis and interpretation of the new concept "MetaFi", translated by the TechFlow Friends volunteer community at TechFlow.

Since 2018, decentralized finance (DeFi) has gained increasing momentum within the cryptocurrency community. While DeFi has attracted significant attention in the crypto space, its adoption rate remains relatively low—less than 5% of all cryptocurrency assets are currently used as collateral.

This article argues that the future growth of DeFi will not be driven by CeFi, but rather through a model we call "MetaFi"—decentralized financial tools for the metaverse.

What exactly is the Metaverse? What value does it hold? How can DeFi combine with ongoing innovations in cryptocurrency to enable large-scale development of MetaFi?

In short, the Metaverse can be understood as an interface layer between the physical and virtual worlds, combining innovations in hardware and software. Most importantly, it is an economic system parallel to traditional fiat-based financial systems. In this context, we must consider it from the perspective of financial inclusion.

The Metaverse Needs Crypto

As mentioned above, the Metaverse is first and foremost an economic system—an “Meta-Economy”—that transcends any single digital economy, virtual world, or game. These should be seen as individual instances or sub-universes (Verses) within the broader Metaverse.

Over sufficient time, when the aggregated GDP of the Meta-Economy surpasses that of nation-states, it may even gain greater prominence compared to fiat-based economies. We believe that at least the open Metaverse—a version of an open, permissionless meta-economy—can be realized through what we collectively refer to as Crypto. And given there is currently no other meta-economy, our argument is: the Metaverse needs Crypto; Crypto *is* the Metaverse.

Within our definition of the Metaverse, people can understand it through two main concepts:

1. Interface Layer. End users experience the Metaverse via various hardware and software technologies such as desktop browsers, mobile apps, or extended reality (XR), virtual reality (VR), and augmented reality (AR).

2. Financial Computation Layer. This is where Metaverse computation occurs—an environment capable of establishing a decentralized, transparent, and democratic foundation that governs how end users exchange goods, services, and currencies based on economic logic. Developers build upon this layer. Ethereum serves as a prime example: a protocol developers use to create smart contracts for decentralized applications, and also functions as a ledger recording transactions among Metaverse users.

In the context of the first point above, early interface layers will likely take many forms and evolve over time. It's important to maintain an open mindset as we advance technologically and conceptually. Thus, when referring to the beginning of Metaverse development, we typically mean current experiences such as games and virtual worlds—whether browser-based 2D environments or more immersive VR/AR experiences.

The financial computation layer refers to the foundational technology supporting the Metaverse. As described in our Open Metaverse OS paper, we believe the core (or foundation) of the financial computation layer will be built on technologies categorized under Web3.

We further argue that any digital domain within the Metaverse must be based on Web3 to provide fundamental property rights, interoperability, and permissionless value transfer across different domains (or verticals) of the Metaverse. These technologies empower the development of diverse applications and instances on top of Web3.

Through this approach, the Metaverse provides a parallel economic system composed of decentralized ledgers—global, transparent, and natively cryptographic. It forms the basis for a new kind of digital-first economy, whose early signs we've already observed through NFTs (Non-Fungible Tokens) and gaming economies like Axie Infinity’s Play-to-Earn model.

Due to its decentralized and permissionless nature, innovation here is unmatched—traditional systems struggle to keep pace.

Therefore, especially in the context of DeFi, the Metaverse has the potential to thrive outside—or at least ahead of—the jurisdiction of national regulators.

Additionally, as observed over the past 12 months in 2021, DeFi began attracting criticism and scrutiny from regulatory bodies across numerous jurisdictions. While regulation may bring some positive market effects, poorly implemented regulations often stifle innovation while benefiting incumbent financial institutions. In the case of DeFi, many of its products resemble traditional financial assets.

Moreover, we view the Metaverse as representing an informal economy, where products are typically digital goods traded in digital markets—some appearing in traditional markets, others not. Just as one cannot regulate every aspect of global economic activity, the same applies to the Metaverse. Given the potential for exponential economic growth within VR, AR, and XR environments, the scope for potential regulation becomes even more challenging—not to mention enforcing such regulations over time within the Metaverse.

We firmly believe that the DeFi components driving Metaverse growth will achieve unprecedented levels of financial inclusion globally. Furthermore, we believe economic activities within the Metaverse will facilitate intergenerational wealth transfer, benefiting future generations and including digital natives, digital creatives, digital workers, gamers, musicians, and others whose digital value is unrecognized by traditional financial systems.

Current State of the Digital Economy

Today, tens of billions of dollars in value are trapped within proprietary network platforms such as social media (Facebook, Instagram, TikTok) or games (Fortnite, Roblox).

Web2, as we know it, was intentionally designed to build “moats” that capture funds and users for as long as possible, maximizing “lifetime value” extraction for shareholder benefit.

Typically, Web2 companies operate under shareholder primacy—even or especially at the expense of user interests. On social media or free-to-play games, this value is monetized primarily through advertising, with profits rarely shared directly with users themselves. Even Roblox, which promotes creators' ability to monetize UGC (user-generated content), pays out only about 25% to its users—similar to music streaming models and YouTube programming.

The global digital economy is currently estimated to be worth $11.5 trillion—equivalent to 15.5% of global GDP. Over the past 15 years, it has grown 2.5 times faster than global GDP, nearly doubling in size since 2000, with an increasing portion of the population relying on the internet for livelihoods.

Focusing on a subset of the digital economy—the digital creator economy—we see it is still only a small fraction of the mainstream digital economy, yet its core areas are growing. It includes publishing, gaming (skin creation), digital art, streaming, music, film, and more.

On the supply side, the sector includes up to 50 million content creators, mostly amateurs (~46.7 million) and around 2 million professionals. In the digital creator economy, professionals can easily earn $100,000 per month. However, most earn far less, income is irregular, and payments may take months to process. Today, much of the digital creator economy cannot be considered part of the Metaverse because value cannot freely trade across platforms—it remains locked into platform-specific equity value.

We further break down the limitations of Web2 digital platforms:

Limited Inclusivity: Most creators, traditionally defined, are economically excluded within today’s digital creator economy because their created value is ignored if outside Web2 platform control, and their earnings are irregular. Simply put, unlike those employed by centralized firms receiving fiat salaries, existing financial systems cannot assess lending risks associated with digital economy wealth holders.

Dynamic Terms & Conditions: Participants in the traditional digital creator economy cannot trust highly centralized services to be credibly neutral, exposing both types of content creators to demonetization or deplatforming risks. For example, when OnlyFans suddenly banned adult content creators, or when platforms like Facebook and Twitter regularly revoke developer access and APIs. In practice, rules governing participation are unclear, inconsistently applied, un-auditable, and subject to arbitrary changes—unlike code-based smart contracts.

Siloed Design: As previously noted, platforms make it difficult or impossible for users to directly transfer value outside their ecosystem or cash out, exiting their closed digital economy. This leads to monopolistic conditions—over time, even if users could leave, they have no viable alternatives.

Web3, NFTs, and the Metaverse

By contrast, the Web3 world—built on cryptocurrency, DeFi, and NFTs—revolves entirely around users and their sovereignty: identity, data, and wealth.

In Web3, data itself can become a form of digital wealth and income. While platforms may still assist in creation, discovery, or curation, users retain full control over their output and can freely transfer value across platforms—reselling, borrowing, or lending in fully permissionless ways. In short, transferability is a fundamental “property right.”

Unsurprisingly, early successes in Web3 show that when moats are removed and transferability enabled, people spend more time and money on preferred platforms—such as blockchain game Axie Infinity. We’ve discussed this in prior papers. Long-term, the Metaverse and its platforms—including most of Web2—will adopt Web3 technologies and principles, not necessarily because it's philosophically correct, but because it makes good business sense.

TikTok’s recent launch of NFTs validates this prediction. But better news is that this could happen without explicit permission or adoption from closed platforms. Instead, NFT derivatives could theoretically be represented and freely traded on permissionless Web3 markets—parallel to closed platforms—through innovations in decentralized commerce infrastructure like Boson Protocol.

Defining MetaFi

For us, MetaFi is an umbrella term referring to protocols, products, and/or services that enable complex financial interactions involving non-fungible and fungible tokens (and their derivatives). For instance, via MetaFi, individuals today can use fractional parts of an NFT as collateral on a DeFi lending platform.

To understand MetaFi, we must first highlight two core principles enabling DeFi: 1) Censorship resistance (inaccessibility), and 2) Composability. Together, these serve as “money legos” for developers, forming a highly innovative parallel financial system.

Developers worldwide can openly participate and compete to offer the highest yields, ruthlessly eliminating inefficiencies. Equally important, regulators can only restrict how fiat-based systems interact with DeFi—but not necessarily what happens within DeFi itself—as long as projects and teams remain sufficiently decentralized.

MetaFi extends these DeFi principles into the broader Metaverse using a hybrid of non-fungible and fungible tokens combined with novel community governance models like Decentralized Autonomous Organizations (DAOs). The convergence of these different crypto primitives enables a mature parallel economy, potentially bringing hundreds of millions—or even billions—of users to the crypto ecosystem over the next decade. We believe four key trends will accelerate this process:

1. Development of Financial Tools: Previously, the DeFi stack was technically complex, accessible only to a small segment of the crypto developer community. Now, through NFT platforms, creators and communities can more easily set economic terms for creative exchanges—from perpetual royalties to issuing their own community tokens. Fans and communities can directly share in the economic success of their favorite products and cultural projects.

2. Financialization of Everything: Many dismiss crypto’s speculative nature, unaware it’s a feature, not a bug. With MetaFi technology, the value and movement of anything can be captured via digital assets, allowing open free markets to price long-tail values. Real-time price discovery unlocks latent value not yet realized on the internet.

3. Improved DAO Stacks: A mature DAO stack enables collective governance of purely on-chain digital and financial services without reliance on corporations or centralized intermediaries (e.g., banks). A key characteristic of DAO members is the ability to seamlessly join and exit under clear terms.

4. Interacting with Risk: History shows traditional financial institutions often fail to assess risk in emerging markets—be it basic banking or insurance. This leads communities to mutualize risk, as seen historically in agricultural communities and shipping industries. Traditionally, cooperatives served this purpose. DeFi already offers users community-based insurance tools, especially when combined with DAO stacks.

5. Gamification of Finance: Generation Z is more interested in becoming financially literate than previous generations. Many neobanks now offer fun, engaging ways to manage personal finances and educational platforms to learn finance easily. This makes younger generations more willing—and likely—to engage with financial products. Additionally, the line between memes and financial instruments is blurring—e.g., Dogecoin or various “meme stocks” offered via Robinhood—making investment and trading within internet culture increasingly natural.

NFTs as Collateral: A Deep Dive

To truly understand whether digital representations can serve as real financial assets for lending, it's essential to examine the viability of NFTs as a form of collateral in DeFi. As we emphasized at the end of 2020, NFTs—typically less liquid than fungible tokens—are increasingly being used within DeFi protocols.

Keep in mind this was before the NFT art explosion of early 2021—the emergence of blue-chip NFTs like CryptoPunks and Bored Apes—and before blockchain gaming categories like Play-to-Earn (led by Axie Infinity) achieved breakout success. This predicted convergence of DeFi and NFTs is now beginning to manifest in everyday MetaFi applications.

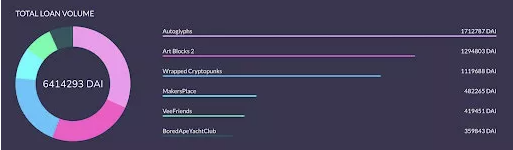

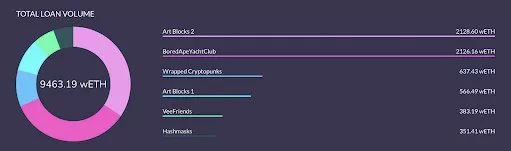

Total wETH loans on NFTfi as of December 13, 2021

Total DAI loans on NFTfi as of December 13, 2021

Additionally, it’s increasingly fascinating how the interaction between fungible and non-fungible social tokens—created by and for creators—has significantly reduced their dependence on intermediaries. People can now gain shares in creator or community franchises and future value they generate. Social tokens now have a total value of approximately $1.1 billion—and growing.

The MetaFi Framework

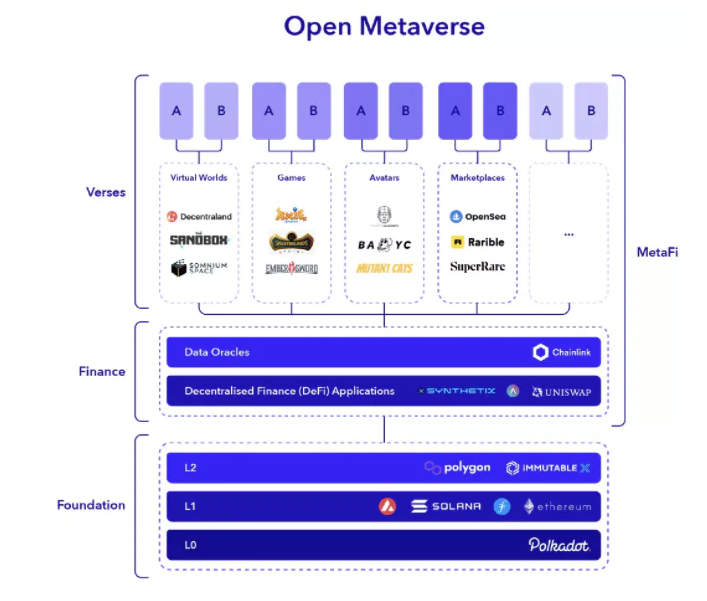

To understand MetaFi within the Metaverse, let’s first visualize the Metaverse’s main components (represented graphically). We use our previous Open Metaverse OS framework, which examines layers of the Web3 stack applicable to the Metaverse.

The Metaverse (see diagram below) consists primarily of three parts: 1) Layers 0, 1, and 2 as the foundation; 2) DeFi; and 3) Verses (applications).

1) Foundation

This section comprises core frameworks (or protocols) labeled Layer 0, 1, and 2—such as Polkadot, Ethereum, and Polygon.

These core frameworks allow application development atop them due to shared application logic and security. They also include a unified communication layer (via execution and consensus, including bridges and cross-chain technologies), enabling horizontal value transfer. The horizontal axis labeled “Open Metaverse” and its related components should be included in applications aiming to deliver internal Metaverse experiences. If an application doesn’t integrate with this core layer, it becomes isolated—its economic and creative value stagnates and eventually disappears, rendering it financially non-inclusive.

We see similar patterns in the traditional world: services failing to integrate into broader ecosystems gradually disappear due to lack of competitiveness for end users.

2) DeFi

This section consists of small financial applications usable on the aforementioned core protocols—often called “money legos.” These are unstoppable applications that leverage smart contracts to enable complex financial dynamics.

3) Verses

This section consists of a set of domains or parallel universes that together constitute the overall Metaverse. Verticals like virtual worlds must connect to the base layer based on compatibility and free value transfer.

MetaFi in the Metaverse emerges at the intersection of vertical and horizontal segments. It’s where domain-specific assets (primarily NFTs) interact with fungible components (infrastructure and finance). The Metaverse hosts numerous and diverse verticals; definitions may be subjective and require debate. At its core, MetaFi is a phenomenon occurring at the convergence of the fungible and non-fungible.

Foundation Enabling Horizontal Growth

As described above, foundational building blocks include core frameworks (or protocols) labeled Layer 0, 1, and 2 (e.g., Polkadot, Ethereum, Polygon). Here, protocols often support modularity—meaning each component (L0, L1, L2) serves the others in some way.

A direct, well-known example is Ethereum—a Layer 1 framework offering smart contract functionality. This means the framework provides customizable logic to create various computer programs, running in a decentralized manner—similar to Bitcoin’s decentralization, but going further by providing what we call smart money or programmable currency via smart contracts.

For simplicity, we focus on Layer 1. Because Ethereum provides a unified layer for developing diverse applications via smart contracts and smart money, it has proven revolutionary for the financial world—as demonstrated by DeFi.

This concept of unification means any smart contract on the Ethereum network can interact with another if programmed accordingly—catalyzing incredible interoperability between services and games built on Ethereum.

The horizontal axis in the diagram remains the broad Metaverse’s factor for horizontal growth. This means Layers 0, 1, and 2 will continue serving as the foundation for all verticals (or parallel universes) constituting the Metaverse. DeFi applications primarily revolve around this horizontal layer, supporting complex financial applications that enable individuals to lend, borrow, and trade within the crypto ecosystem.

MetaFi Activity Clusters

Regarding the illustration above, the number of verticals and their respective definitions will continue evolving with the Metaverse. However, we aim to define some emerging core activity clusters as follows:

Virtual Worlds: Virtual worlds are digital spaces designed for socializing, commerce, or gaming—possibly mimicking or abstracting real-world physics. When mimicking reality, they often include rare elements represented as NFTs—freely purchasable, tradable, and buildable. Notable examples include Sandbox and Decentraland.

As NFT components, virtual land is closely tied to in-game currencies and/or governance tokens of virtual worlds—enabling users to purchase assets and vote on improvement proposals using tokens.

Adoption of virtual worlds has made significant progress—from just a dozen daily interactions at the start of 2021. In the past 30 days, 65,000 unique addresses interacted with smart contracts of Somnium Space, Decentraland, Sandbox, and Crypto Voxels—a fourfold increase since early November. Sandbox contributed most significantly, both in monthly active users (~4,100) and total land sales value to date (112,000 ETH or $450 million).

Gaming: Games can be defined as digital activities primarily for entertainment. Metaverse games differ by incorporating play-to-earn mechanics—users or players receive token rewards for contributing to the game. This creates entire in-game economies where capital and labor combine to produce value.

Axie Infinity is perhaps the most famous Metaverse game and a pioneer in the category—by metrics of users (~2 million monthly active users) and protocol revenue ($2.5 billion annualized). Blockchain games have gained widespread acceptance since the beginning of this year. Nearly half of active blockchain wallets are now linked to games, with the top 10 blockchain games collectively hosting 4 million monthly active users.

Avatars: Avatars are uniquely designed digital identities for users—including 3D avatars interoperable across various Metaverse spaces—often mass-produced as generative PFP (Profile Picture) projects.

PFPs function like famous social clubs, enhancing NFTs with fungible tokens within their projects—often including governance rights or other benefits. Popular projects like CyberKongz and SupDucks distribute native tokens to holders of certain NFT classes. In the CyberKongz project, holding a genesis kong earns 10 Banana tokens every 24 hours. These can be sold on Sushiswap or spent in the “Banana Store” to upgrade, rename, buy gear, or breed new kongs (costing 600 Banana tokens).

Equipment: Equipment refers to digital items displayed in the Metaverse—currently most valuable in games, but expected to expand to other Metaverse categories soon. Increasingly, designer brands are leveraging NFTs to reach the global market of 2.7 billion gamers. Players can now own unique skins designed by top fashion houses and showcase their taste to millions online. For example, Balenciaga partnered with Fortnite to design four virtual outfits; Burberry collaborated with Mythical Games to launch fashion pieces represented as NFTs.

Markets: Markets are digital venues matching supply and demand, enabling better NFT discovery and price discovery. Platforms like OpenSea, SuperRare, and Rarible allow users to freely trade and directly issue NFTs—effectively turning NFTs into financial assets. Fractionalization allows high-value NFTs to gain liquidity by splitting into fungible tokens for proportional ownership. Combining fractionalization with bundling is particularly popular—creating index fund-like solutions for specific NFT categories, such as NFTX or Beeple’s B20 index. The NFT boom has driven explosive market volume: OpenSea’s 30-day trading volume rose from $1 million in January 2021 to over $200 million in November 2021.

Yield-Generating NFTs: NFTs can generate yield in two ways: indirectly or directly. Indirect yield generation includes using NFTs as collateral for loans, then reinvesting borrowed funds at higher rates. NFTfi enables using NFTs as loan collateral.

Additionally, a persistent trend over recent months involves NFT-first projects introducing native tokens—adding another yield-generating dimension to their NFTs. EtherCards is launching its Dust token, distributed based on the rarity of each existing EtherCard. Dust tokens can enter raffles to win blue-chip NFTs. This overlaps with avatars—CyberKongz and SupDucks can also be viewed as yield-generating NFTs.

Access Tokens: Can be either fungible or non-fungible tokens granting holders various forms of value—access to communities, specific individuals, or future mints. A strong example is The Bored Ape Yacht Club—a collective of 10,000 ape NFTs. Ownership grants entry to a Discord community and allows speculation/trading on the club’s future value.

Notably, the above categories do not operate in isolation—they often overlap. For example, successful mechanisms now allow play-to-earn 2.0 projects like Axie Infinity to hold yield-generating NFTs transferable to other NFT use cases. Similarly, established crypto protocols (centered on fungible tokens) have launched NFTs as additional engagement tools—e.g., Gitcoin selling NFTs to fund digital public goods. We expect to see more unusual combinations of these categories—and entirely new MetaFi categories—in the near future.

Current Limitations

Much work remains before MetaFi realizes its full potential. More specifically, the current state of MetaFi faces several limitations that must be overcome for widespread adoption:

1. NFT Valuation: To buy, sell, or borrow against an NFT, owners need to know its value. NFTfi addresses this: users list NFTs as collateral on NFTfi, and lenders offer loans based on their assessment of the NFT’s value. Valuation is essentially performed by lenders—not neutral third parties.

2. Legal and Governance Issues Around Fragmentation: If you split an NFT into 100 parts and distribute them to different people—especially when the NFT carries voting or revenue rights—it's unclear who can do what, when, and how these rights are managed.

3. Cross-Blockchain Standards: The Metaverse is no longer built solely on Ethereum—it spans multiple Layer 1 or Layer 0 blockchains that still lack 100% interoperability. This means value fragmentation is unavoidable in the short term.

To fully unlock DeFi’s value for the Metaverse, NFTs must be easily integrated into DeFi protocols—capable of being traded, borrowed, lent, re-lent. While today’s DeFi works only with fungible tokens, we expect new methods connecting NFTs and DeFi:

1. NFT Fractionalization: Dividing a non-fungible token into many fungible tokens. Fractional parts can be seen as equity stakes in NFT ownership. For example, meme creators can use asset creation platforms to mint memes, fractionalize them into highly fungible tokens, and trade them on DeFi DEXs like Uniswap. Notable NFT fractionalization projects include Fractional and DAOfi.

2. NFT-Enabled DeFi: Upgrading DeFi protocols to accept NFTs as collateral. For instance, creators can build assets in virtual worlds and use them as collateral to borrow on platforms like Centrifuge or Pragmafy.

3. NFTs as Derivatives: Creating a series of liquid digital assets whose value depends on off-chain assets, in-game items, social capital, etc.—represented as NFTs and possibly linked to data feeds determining their behavior. For example, a digital artist can create artwork, mint an NFT derivative, and use it as collateral on Synthetix to mint synthetic assets like stablecoins, synthetic gold, or stocks.

MetaFi Outlook for 2022

In summary, MetaFi—Metaverse Finance—is an umbrella term referring to protocols, products, and/or services enabling complex financial interactions among non-fungible and fungible tokens (and their derivatives). It encompasses foundational components of the blockchain space (Layer 0, 1, 2), the DeFi stack, and various Verses.

MetaFi inherits two core features of DeFi protocols: censorship resistance and composability. Its development is driven by key trends including risk mutualization, gamification of finance, financial tool development, and improved DAO stacks.

We hope we’ve clarified that MetaFi, in its current form, remains in its infancy. Though some of its capabilities seem unimaginable today, we’re only beginning to grasp its medium- to long-term potential. Based on current market observations and detailed analysis of catalytic factors, we anticipate the following developments in the short to medium term:

1. Combinations of different MetaFi categories and the creation of entirely new ones—e.g., users building games within virtual worlds that have their own economies or generate non-fungible assets like equipment or avatars.

2. Improved user experience/user interface for financial MetaFi projects, possibly incorporating VR elements. For MetaFi to succeed broadly, it must become more accessible and intuitive to the general public.

3. Further innovations from DeFi 2.0 migrating to MetaFi—similar to those seen in Olympus DAO and Alchemix. Better solutions are needed for NFT fractionalization—particularly regarding legal and governance issues—and for integrating NFTs into DeFi.

4. Improvements in foundational technologies (e.g., Layer 1), reducing transaction fees, increasing user capacity, enabling scalability, and making blockchain-based applications easier to access overall.

Original Report Download Link:

https://outlierventures.io/wp-content/uploads/2021/12/OV_MetaFi_Thesis_V1B.pdf

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News