Delphi Labs: A New Token Issuance Mechanism, Locking + Liquidity Bootstrapping Auction

TechFlow Selected TechFlow Selected

Delphi Labs: A New Token Issuance Mechanism, Locking + Liquidity Bootstrapping Auction

The goal of the token distribution mechanism is to distribute tokens to the protocol's users and community.

Author: Delphi Labs

Translation: MIM

Introduction

Delphi has spent considerable time analyzing and designing token distribution mechanisms. Overall, token issuance has come a long way since the fixed-price ICO sales, but we still believe there is significant room for improvement.

We recently incubated two projects—Mars and Astroport—but while planning their token distributions, we found that none of the existing structures fully met all our design objectives. To achieve a truly "tailor-made" solution, we rethought the token distribution mechanism from first principles. The result is “Lockdrop + Liquidity Bootstrap Auction,” which will be trialed on Astroport in December and later on Mars.

This article explains in detail the design goals we aim to optimize and why we believe this new structure represents the best possible token issuance mechanism.

Design Considerations

Current Token Distribution Mechanisms

Broadly speaking, the goal of any token distribution mechanism is to allocate tokens to protocol users and the community. Currently, most projects use one of two primary approaches:

(1) Distributing tokens to users—Users earn tokens through past or ongoing actions. This includes airdrops and all forms of continuous incentives (staking rewards, liquidity mining, trading competitions, etc.).

(2) Public token sales—Users receive tokens in exchange for capital investment. This includes fixed-price sales, auctions, LBPs, Pylon-style yield underwriting, and more.

Both mechanisms have multiple shortcomings.

-

Distributing Tokens to Users

Protocols distributing tokens to users typically rely on two methods: airdrops and ongoing liquidity incentives.

Airdrops aim to allocate tokens based on users’ past behavior—either because they previously used the protocol or were high-value users of other protocols. This may seem like a good idea, but airdrops reward past actions rather than future commitment, so they do not guarantee alignment with the protocol’s long-term success. In fact, our research shows that most airdropped tokens are eventually abandoned.

Ongoing liquidity incentives aim to reward continued engagement with the protocol and have become the default distribution method for most projects. However, relying solely on this approach has drawbacks. First, continuous incentives can only reward usage that is measurable on-chain—such as providing liquidity, supplying collateral, or completing trades. This favors whales with more capital who gain disproportionately higher rewards, while excluding other stakeholders who contribute value in different ways, such as community contributors, third-party integrators, or teams building atop the protocol. For these participants, buying tokens on the open market may be their only path to alignment.

Second, simply disbursing tokens to suppliers creates additional issues such as low initial float, lack of price discovery, and poor liquidity—especially in the earliest stages. This harms non-suppliers who wish to buy tokens on the open market; they either cannot accumulate meaningful positions or face severe slippage due to illiquidity (e.g., ANC launch), or endure continuous selling pressure from low-floating token emissions (e.g., MIR)—or both.

-

Public Token Sales

To avoid the above problems, some projects opt for public sales to facilitate price discovery, but public sales come with their own drawbacks. First and foremost, all public sale models expose projects to greater regulatory risk. Transactions involving clear “capital investment” in early-stage protocols are most likely to meet the “Howey Test” criteria—relying on the entrepreneurial efforts of a small group. Combined with other factors, this makes public token sales far more likely than other distribution methods to be classified as unregistered securities offerings.

Second, while public sales solve price discovery, they don’t necessarily address low initial liquidity. Projects could bootstrap liquidity themselves, but this requires substantial capital and increases regulatory exposure, as effectively setting a price via self-funded market-making resembles conducting an offering. As a result, many tokens exhibit extreme volatility in the days and weeks after launch—volatility that particularly harms enthusiastic early adopters who may lack sophisticated trading skills.

Third, most sale and auction structures are vulnerable to bot front-running (e.g., ANC, VKR), leading to supply concentration among a few technically capable and well-capitalized whales who dominate the entire sale.

Summary: Design Goals and Constraints

In summary, we aim to design a token distribution mechanism that achieves the following objectives:

Distribution: We want to ensure tokens are fairly distributed across a broad base of stakeholders. Most importantly, the launch mechanism should not be exploitable by bots or whales. Ideally, smaller holders should have an opportunity to earn more tokens by demonstrating genuine commitment to the protocol.

Price Discovery: We want a fair, decentralized, bottom-up mechanism to establish the token price prior to trading.

Sufficient Float: We want enough initial supply to meet demand and support legitimate price discovery. Recently, many projects launched with extremely low floats (less than 5% of total supply), resulting in highly inflated fully diluted valuations (due to inelastic demand with insufficient supply). From there, continuous token emissions and unlocks cause chronic price “bleeding,” leading to community dissatisfaction and declining morale. We firmly believe the only way to build a successful protocol is to involve the community from day one—to grow and succeed together. Therefore, ensuring a sufficiently large initial float is critical for enabling fair and credible price discovery.

Liquidity: Once the price is set, we want immediate and deep liquidity at that price.

Decentralization: The consortium behind Mars and Astroport does not want to set prices, conduct public sales, launch AMMs/LBPs, accept “venture capital” investments, or otherwise act as sellers, authorities, market makers, or brokers.

Therefore, it is essential that Astroport users themselves provide all liquidity and price discovery in a decentralized manner.

Lockdrop + Liquidity Bootstrap Auction

We believe the “Lockdrop + Liquidity Bootstrap Auction” can achieve all these goals. At a high level, it is a two-phase process operating as follows:

Phase One (Lockdrop): Distribution phase. A time window is opened during which anyone can pre-commit to becoming a user of the protocol for a certain duration (details in the “Phase One: Lockdrop” section below).

At the end of the window, participants receive a pro-rata share of the total tokens being distributed, based on the size and duration of their commitment. These tokens remain locked until the end of Phase Two.

Phase Two (Liquidity Bootstrap Auction): Price discovery phase. Another time window opens where participants from Phase One can choose to commit part or all of their ASTRO into one side of a stablecoin liquidity pool (i.e., ASTRO-UST). Other users can then join by depositing UST on the other side, effectively purchasing ASTRO from the locked participants. At the end of this phase:

1. Native tokens and stablecoins are deposited into the liquidity pool. The ratio between native tokens and stablecoins determines the final token price.

2. Auction participants receive LP shares proportional to their deposits. These LP shares are locked and linearly vested over three months. Assuming sufficient participation in Phase Two, this ensures deep and immediate liquidity at the market price.

3. All tokens issued in Phase One that were not committed to the liquidity auction in Phase Two are unlocked and freely tradable.

Note: Airdrops can also be used in Phase One to distribute tokens to users (either as an alternative or complement to the lockdrop).

To illustrate how this mechanism works in practice, we will examine it within the context of “Astroport’s token distribution event”:

Phase One: Lockdrop

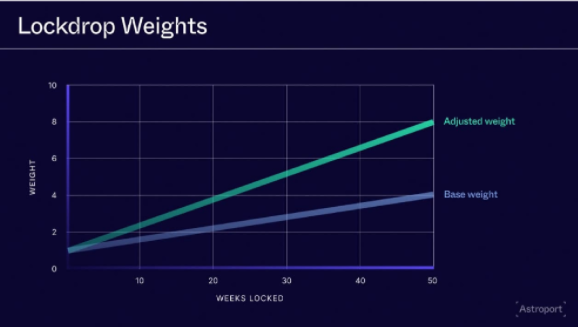

Phase One is the distribution phase, aiming to place tokens directly into the hands of Astroport users. Ideally, the number of tokens a user receives should be proportional to the “value” they bring to the protocol. Different distribution mechanisms capture different forms of value. For example, airdrops identify value brought by historical users of the target protocol or synergistic protocols. A lockdrop is similar to an airdrop, but instead of rewarding past actions, it rewards a forward-looking commitment to use the protocol—akin to the discount you receive when signing a one-year contract with your mobile or broadband provider.

For Astroport, these long-term customers are liquidity providers who help bootstrap liquidity for key trading pairs. During the lockdrop, users can commit to depositing liquidity in the form of Terraswap LP tokens into Astroport for pre-selected trading pairs. Crucially, users can further signal their commitment by locking their LP tokens for longer durations—the longer the lockup, the greater the reward, up to a maximum of one year. 7.5% of the total ASTRO supply will be allocated to users who lock liquidity in Phase One, hence the name “lockdrop.”

Overall, an individual user’s lockdrop allocation will be determined by two factors:

1. The total amount of ASTRO allocated to the trading pair the user contributes liquidity to (to be announced before Phase One begins).

2. The user’s weight-adjusted share of liquidity in the pool. Rather than measuring raw liquidity provided, a weighting factor based on the duration the user locks their LP tokens is applied. Thus, the numerator is the user’s weighted liquidity, and the denominator is the total weighted liquidity supplied by all users in that pair.

The ASTRO share a user receives for contributing LP to a given trading pair is calculated as follows:

A = Ap * (wLu/wLp)

A = ASTRO received by the user

Ap = Total ASTRO allocated to the user’s chosen trading pair

wLu = Weight-adjusted liquidity provided by the user

wLp = Total weight-adjusted liquidity in the pool

B = Bonus multiplier based on lock duration

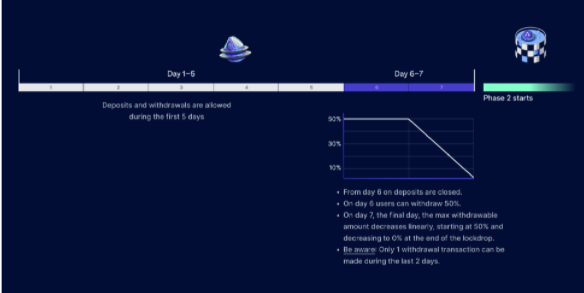

During the first 5 days, users can freely deposit and withdraw, encouraging broad participation and allowing them to commit their desired amount of liquidity. In the final 2 days, only withdrawals are allowed, giving users the option to reduce their liquidity if they feel the ASTRO rewards are less than the opportunity cost of their capital.

At the end of Phase One, liquidity will migrate from Terraswap to Astroport—users’ Terraswap LP tokens will be burned and replaced with locked Astroport LP tokens.

Importantly, in addition to the one-time lockdrop reward, LPs will also earn trading fees plus emission rewards from their respective pools (same as other liquidity providers).

In addition to the 7.5% ASTRO distributed via lockdrop, another 2.5% will be airdropped to LUNA stakers and Terraswap users. This provides a 10% floating supply available for Phase Two.

Phase Two: Liquidity Bootstrapping Auction

Phase Two is the price discovery phase, aiming to establish a fair price and deep liquidity around it. To those familiar with markets, a liquidity bootstrapping auction resembles recent auctions like Mango Markets, but with several key differences:

1. Users sell tokens, not the protocol;

2. Auction participants receive locked LP shares, not unlocked tokens;

3. Withdrawals are gradually restricted in the final two days to prevent whale manipulation (explained in detail below).

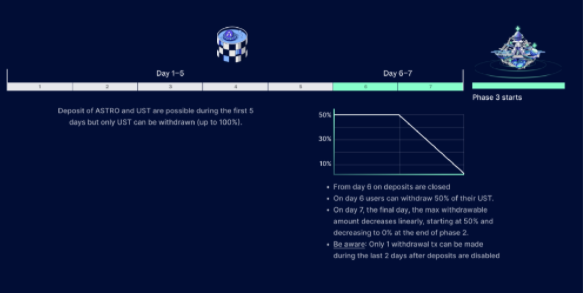

In Phase Two, users who participated in the lockdrop or received tokens via airdrop can choose to deposit part or all of their locked ASTRO into the ASTRO-UST liquidity pool. Then, any user can join by depositing UST on the other side, effectively purchasing ASTRO from the locked participants.

The ASTRO price is determined by the amounts of UST and ASTRO added to the pool—specifically, the final UST-to-ASTRO ratio. If 100 ASTRO and 100 UST are deposited, the implied ASTRO price is $1; if another 100 UST is added, the implied price jumps to $2. Crucially, this price is meaningful because participants commit to initializing and locking their tokens in the pool at this price for three months (i.e., they effectively buy ASTRO below the price and sell above it over three months)—this is the typical impermanent loss risk faced when providing AMM liquidity, i.e., inability to exit spontaneously based on market movements.

Per the schedule, during the first 5 days of Phase Two, users can deposit any amount of ASTRO and UST, but can only withdraw UST. This encourages participation and bidding up to their maximum willingness to pay. In the final 2 days, only UST withdrawals are allowed. As UST is removed, the implied ASTRO price drops. This enables price discovery, as users will continue withdrawing UST until the ASTRO:UST ratio reflects a price they find acceptable.

What happens in the final two days deserves deeper analysis, as other similar designs are vulnerable to manipulation at this stage. On Day 6, withdrawal limits are capped at 50% of deposited amount. On Day 7, the limit linearly decreases from 50% to 0% over 24 hours. These restrictions are necessary—without them, whales could over-deposit (i.e., deposit far more than they intend to keep), pushing the price far above their true willingness to pay, thereby deterring others. Then, just before closing, they withdraw the excess, securing a much lower effective price. This type of manipulation occurred in Mango Markets, severely distorting token issuance and price discovery. Withdrawal caps limit the effectiveness of such attacks, and the linear taper adds increasing stability as closure approaches.

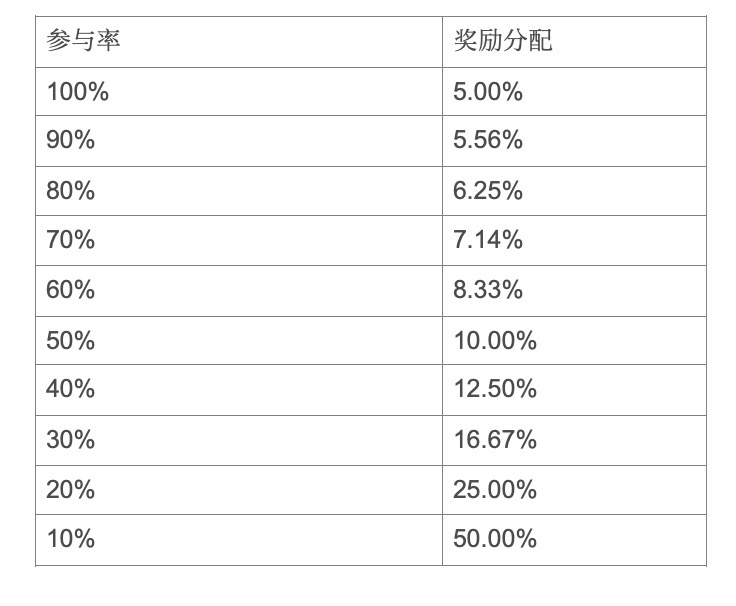

By now, the mechanics of the final days of Phase Two should be clear. Next, we must explain why users would broadly participate in Phase Two. Whether they prefer to sell their rewards or use them as LP, they could do both without participating in Phase Two, retaining full optionality. The reason it's called “optionality” is that participants’ LP shares are locked for three months upon joining Phase Two. To incentivize participation, we offer a bonus: an additional 1% of the ASTRO supply (10 million ASTRO). This 1% is split between ASTRO and UST depositors—effectively a seller premium and buyer discount. The fixed 1% bonus means that if participation is low, the per-participant reward increases. This helps generate secondary market liquidity and ensures the level of participation we deem necessary. The table below illustrates the bonus distribution scheme based on overall participation rates:

While the table covers all scenarios, we obviously don’t expect participation near 100%. Below is an illustrative example with round numbers.

Example: 25% of Phase One token holders decide to participate in Phase Two (25,000,000 ASTRO), and 25,000,000 UST are also deposited. This results in a $1 price per ASTRO. These participants will receive an additional 10,000,000 ASTRO (5 million each) proportional to their deposits.

Suppose you hold 1% of the deposited ASTRO—you are entitled to 1% of 5% of the ASTRO-side bonus. This means your 250,000 ASTRO deposit now represents an LP position of 125,000 ASTRO and 125,000 UST, and you receive an extra 50,000 ASTRO—equivalent to a 20% bonus.

After Phase Two ends, auction participants receive LP shares proportional to their contributed liquidity. These LP shares are locked and linearly vest over three months.

At this point, the circulating supply of ASTRO reaches 11%.

Advantages

Having detailed the new mechanism, let us now examine how it achieves the goals outlined in the “Design Considerations” section.

Distribution: ASTRO is allocated to users who pre-commit to using the protocol. Small investors can increase their ASTRO share by voluntarily committing to longer lockups. Non-users can obtain tokens in a way that resists whale and bot exploitation, while users retain some control over the price they pay.

Price Discovery: Phase Two enables a bottom-up, LP-based auction mechanism where buyers (users depositing UST into the LP) and sellers (Astroport users depositing ASTRO) jointly determine a fair ASTRO price.

Sufficient Float: By the end of Phase Two, 110,000,000 ASTRO will be in circulation, equivalent to 11% of total supply.

Liquidity: Phase Two ensures liquidity by auctioning locked ASTRO-UST LP shares—not ASTRO tokens themselves. The pool is automatically funded at the end of Phase Two, guaranteeing immediate and deep liquidity.

Decentralization: Neither the project team nor the DAO sells tokens to the public. Instead, protocol users are granted tokens (primarily for user-driven governance, not as “investment”), and may optionally sell portions via the auction. Moreover, the large initial float dilutes the potential influence of pre-launch builders on post-launch, token-based governance, accelerating the decentralization of governance compared to traditional models.

Conclusion

We believe both “Lockdrop” and “Liquidity Bootstrap Auction” represent new primitives in token issuance, and we are excited to see the broader crypto community adapt and build upon them. While we chose to combine them here, they are independent mechanisms and can be used separately.

“Lockdrop” can be seen as a new method of distributing tokens to users, rewarding future commitment rather than past or ongoing actions. It can apply to any protocol involving “usage” and capital commitment that can be tokenized and locked. The “Liquidity Bootstrap Auction” we propose in this article doesn’t fit neatly into traditional categories of token distribution or public sale—it arguably represents a new class of token issuance: peer-to-peer auction. That said, for teams comfortable with regulatory risk, “Liquidity Bootstrap Auction” can serve purely as an exceptional price discovery and liquidity mechanism—one funded by project treasury rather than user-held tokens.

We have open-sourced the code for both the “Lockdrop” and “Liquidity Bootstrap Auction.” We’ve already spoken with several projects interested in adopting these mechanisms and will work closely with them to tailor the designs to their specific goals. If you’re interested in using these mechanisms for your own project, please reach out—we’d be happy to help you think through implementation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News