Daily trading volume exceeds $100 million: How has Uniswap become the dominant DEX?

TechFlow Selected TechFlow Selected

Daily trading volume exceeds $100 million: How has Uniswap become the dominant DEX?

Uniswap's daily trading volume exceeds $100 million

Author: Haseeb Qureshi, Managing Partner at Dragonfly Capital

Imagine your college friend comes up to you and says: "Hey, I have a business idea. I'm going to run a market-making bot. Whenever someone asks for a quote, I'll instantly provide one. I’ll use x * y = k as the pricing algorithm. That’s pretty much it. Want to invest?"

You’d probably run away immediately.

In fact, that's exactly what Uniswap is.

Unisamp is the world’s simplest automated market maker (AMM). Last year, this humble market maker saw explosive growth in trading volume and became the largest decentralized exchange by volume globally.

Since Uniswap’s rise, innovation in the AMM space has surged. A wave of uniquely designed AMM projects has emerged.

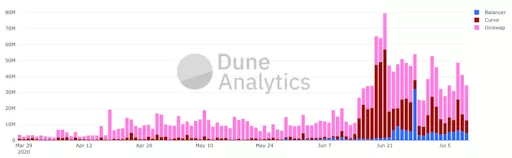

Figure | Trading volumes of Uniswap, Balancer, and Curve (Source: Dune Analytics)

While these projects inherit Uniswap’s core design, each features its own unique pricing function.

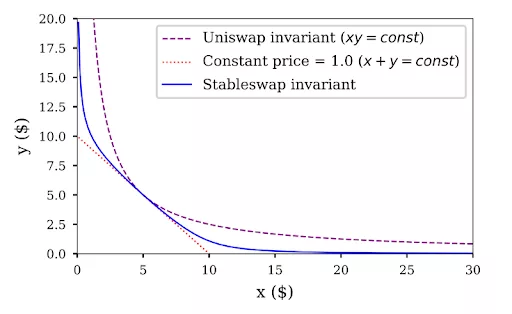

Take Curve and Balancer as examples. The former uses a hybrid pricing function combining constant product and constant sum models, while the latter employs a multi-dimensional, multi-asset pricing function. Some even feature curves capable of draining liquidity—such as Foundation, which uses such a curve to sell limited-edition items.

Figure | The Stableswap curve used by Curve (blue line) (Source: Curve)

Given the rapid growth in the number of AMMs, it's easy to assume that AMMs are destined to dominate all on-chain trading in DeFi and that their success is inevitable.

But I don’t think so.

In fact, the massive success of AMMs stems from some very specific and contingent factors.

Don't forget—there were already many decentralized exchanges before Uniswap existed! Yet Uniswap managed to beat order-book-based DEXs like IDEX and 0x. Why?

From Order Books to Automated Market Makers

I believe there are four reasons why Uniswap outcompeted order-book exchanges:

- First, Uniswap’s implementation is extremely simple. This means low complexity, minimal attack surface, and low integration costs—especially low gas costs! For anyone executing transactions on Ethereum, this is crucial. It’s not a minor issue. I believe that once next-generation high-throughput blockchains emerge, order-book exchanges will eventually dominate, just as they do in traditional finance. But can order-book exchanges dominate on Ethereum 1.0? Ethereum 1.0 has so many constraints precisely to maintain simplicity. If you can’t do complex things, you must excel at doing simple ones. Uniswap is a beautifully simple protocol.

- Second, Uniswap has a small regulatory footprint [Bram Cohen argues Bittorrent succeeded for similar reasons]. Uniswap is highly decentralized and requires no off-chain inputs. Compared to cautious decentralized order-book exchanges, Uniswap operates as a pure financial infrastructure, enabling greater freedom to innovate.

- Third, providing liquidity on Uniswap is incredibly easy. Compared to becoming an active market maker on an order-book exchange, Uniswap offers a one-click liquidity provision experience—especially valuable before the surge in DeFi trading volume. This was critical because most of Uniswap’s liquidity came from small token holders. These users are less sensitive to yield, so minimizing friction through a seamless UX made a big difference. Cryptoeconomic designers often ignore psychological transaction costs, assuming participants are highly diligent. Uniswap minimized the effort required to provide liquidity—and it paid off.

- The final reason for Uniswap’s success is the low barrier to creating incentive pools. Creators of these pools airdrop tokens to liquidity providers, offering returns above Uniswap’s standard fees. This practice is known as “liquidity mining.” Some of the largest incentive pools on Uniswap have distributed airdrops—for example, AMPL, sETH, and JRT. Balancer and Curve now use their native tokens to incentivize liquidity.

Traditional market makers earn money in three ways—one of which involves designated market maker agreements where asset issuers pay fees. In a sense, incentive pools are exactly that: asset issuers pay AMMs via airdrops to those providing liquidity.

However, incentive pools do more than just facilitate market making. They also serve as tools for marketing and distributing new tokens. Through incentive pools, AMMs can distribute tokens in a Sybil-resistant way to speculators seeking exposure, while simultaneously bootstrapping a liquid market.

Moreover, with incentive pools, token buyers don’t need to flip tokens to profit—they can deposit them into the pool and earn yield instead! You might call this “poor man’s staking.”

These factors deeply explain Uniswap’s current success (this article doesn’t cover “initial DeFi offerings,” which I’ll discuss elsewhere).

Nevertheless, I don’t believe Uniswap’s dominance will last forever.

If the limitations of Ethereum 1.0 enabled today’s AMM dominance, then Ethereum 2.0 and Layer 2 solutions will foster the growth of more sophisticated markets.

Additionally, DeFi is rapidly rising. As user counts and trading volumes grow, market makers will multiply accordingly.

I expect Uniswap’s market share to gradually shrink.

What role will AMMs play in DeFi five years from now?

I believe that by 2025, AMMs won’t be the primary way people trade, as they are today. Throughout tech history, such transitions are common.

In the early days of the internet, web portals like Yahoo were among the first to succeed. Given the constraints of early networks, manually curated directories were the best way to organize information. As mainstream users came online, countless portals emerged! But we now understand that portals were merely stepping stones in the evolution of web information architecture.

What, then, are AMMs a stepping stone toward? Will they be replaced, or evolve alongside DeFi? I’ll explore these questions in future writings.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News