Bitget UEX Daily | Waller: AI Pushes Up Prices But Not Necessarily Inflation; Anthropic to Launch IPO as Early as October; Jensen Huang Promotes AI and Robotics Collaboration in Tokyo

TechFlow Selected TechFlow Selected

Bitget UEX Daily | Waller: AI Pushes Up Prices But Not Necessarily Inflation; Anthropic to Launch IPO as Early as October; Jensen Huang Promotes AI and Robotics Collaboration in Tokyo

Overall, institutional consensus leans towards "data-driven cautious optimism," recommending a focus on subsequent retail sales and employment data for revisions to rate cut expectations, as well as the actual impact of evolving AI infrastructure regulatory policies on the industry chain. In a diverging market, stock selection and thematic allocation are more critical.

I. Hot News

Fed Dynamics

Trump Pressures New York AI Infrastructure Policy; Fed Chair Reaffirms Independence

- Trump fiercely criticized New York Governor Kathy Hochul's executive order suspending environmental permit approvals for large data centers on social media Wednesday, calling it a "terrible decision," and emphasized that the taxes and jobs brought by data centers are a huge victory like "liquid gold" for states, demanding New York State change its stance immediately.

- The New York Governor responded that communities providing computing power for AI should share the results, and countered that if data centers are truly "liquid gold," should New Yorkers only get "leftovers." Previously, New York announced a suspension of environmental permits for new large data centers for up to one year to formulate a regulatory framework to prevent rising electricity bills and impacts on water resources.

- Fed Chair Kevin Warsh reaffirmed the Federal Reserve's decision-making independence at the semi-annual monetary policy hearing in the Senate, denied Trump's attempt to intervene in the Fed, and clearly pointed out that price increases brought by AI infrastructure construction do not necessarily constitute inflation and should be distinguished from supply shock-driven price increases.

Market Impact: Confirmation of policy independence helps stabilize market expectations for the consistency of Fed decisions, reduces concerns about political intervention, and boosts confidence in risk assets; however, tightening AI infrastructure regulation may increase compliance costs, affect the investment rhythm of related industrial chains, and in the short term, attention needs to be paid to the transmission effects of policy games between states on the electricity and data center supply chains.

International Commodities

Trump Expects Oil Prices to Fall to $55; Spot Gold and Silver Oscillate at High Levels

- Trump said in an interview that oil prices will fluctuate for a while, and may fall to the level of $55/barrel after the Iran situation stabilizes; currently affected by Middle East geopolitical tensions and global refining capacity shortages, oil prices remain firm in the short term.

- Spot gold briefly rose after the June CPI cooling data but subsequently faced profit-taking pressure, trading near $4050/ounce; silver followed gold's range fluctuations.

- Driving factors include a slight decline in the US Dollar Index, changes in real interest rates, and support for energy commodities from long-term electricity demand for AI data centers, but the New York regulatory suspension order highlights that policy uncertainty may inhibit some infrastructure investment.

Market Impact: Oil prices have significant geopolitical premiums in the short term, but Trump's long-term bearish view may limit continuous upward space; precious metals maintain high-level oscillations against the backdrop of clarified Fed policy and improved risk appetite, focusing on the regulatory effect of inflation data and geopolitical events on safe-haven demand.

Macroeconomic Policy

Fed Beige Book Shows Moderate Economic Growth; AI Regulation and Inflation Outlook Divergence Coexist

- The Fed Beige Book pointed out that US economic activity achieved moderate to moderate growth from late May to June, with 11 out of 12 Fed districts recording expansion; the labor market is robust, employment grew slightly, but skilled worker shortages pushed up wages; inflation is overall moderate, but there are significant differences in inflation outlook forecasts across jurisdictions, with energy price uncertainty becoming the biggest variable.

- Fed Governor Cook warned that the AI investment boom coupled with supply shocks from tariffs and Middle East conflicts is making inflation risks surpass employment risks; action will be taken if inflation does not cool down.

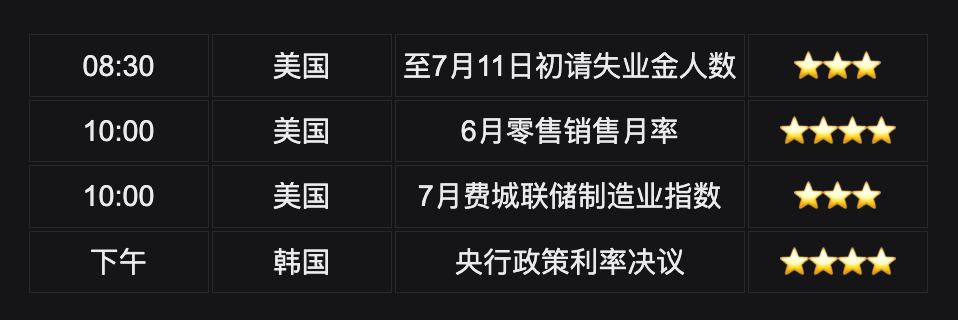

- Today's market focus is on US Initial Jobless Claims for the week ending July 11, June Retail Sales MoM, July Philly Fed Manufacturing Index, and the Bank of Korea policy rate decision (possibly the first rate hike since 2021).

Market Impact: Economic data is robust but inflation stickiness remains; tightening AI infrastructure regulation may increase compliance costs and affect investment rhythm; policy divergence intensifies market vigilance against structural inflation, data releases will further verify consumption and employment resilience, and form corrections to rate cut expectations.

II. Market Review

Commodities & Forex Performance (Real-time Update)

- Spot Gold: $4043/ounce, -0.4%

- Spot Silver: $57.30/ounce, -0.85%

- WTI Crude Oil: $79.80/barrel, +0.8%

- Brent Crude Oil: $85.50/barrel, +0.64%

- US Dollar Index (DXY): 100.466, -0.05%

Driving Factor Analysis: June CPI data cooling exceeded expectations (month-on-month decline for the first time in six years), alleviating concerns about inflation out of control, the US Dollar Index fell slightly, providing support for commodities. Trump's statement about oil prices falling to $55 in the long term reflects optimistic expectations for easing Middle East tensions, but current geopolitical tensions and refining capacity shortages (about 10% of global capacity offline) still push up short-term oil price premiums. Gold at high levels (fell from January highs but still in high range) faces profit-taking pressure, while long-term demand for electricity and energy from AI data centers is good for related commodities, but the New York regulatory suspension order highlights that policy uncertainty may inhibit some investment. Silver follows gold's oscillation. Asset linkage shows improved risk appetite putting pressure on the US dollar, while supply-side factors dominate oil prices. Institutional consensus believes the macro environment favors risk assets, but geopolitical and regulatory risks cannot be ignored, short-term precious metals may maintain range oscillations, and oil prices need to be wary of volatility brought by expectation gaps.

Cryptocurrency Performance

- BTC: $64637, -0.17%

- ETH: $1917, +2.23%

- Total Cryptocurrency Market Cap: About $2.31 trillion, -0.2%

- Market Liquidation Situation: 24h Total Liquidations $300 million, Short Liquidations $184 million

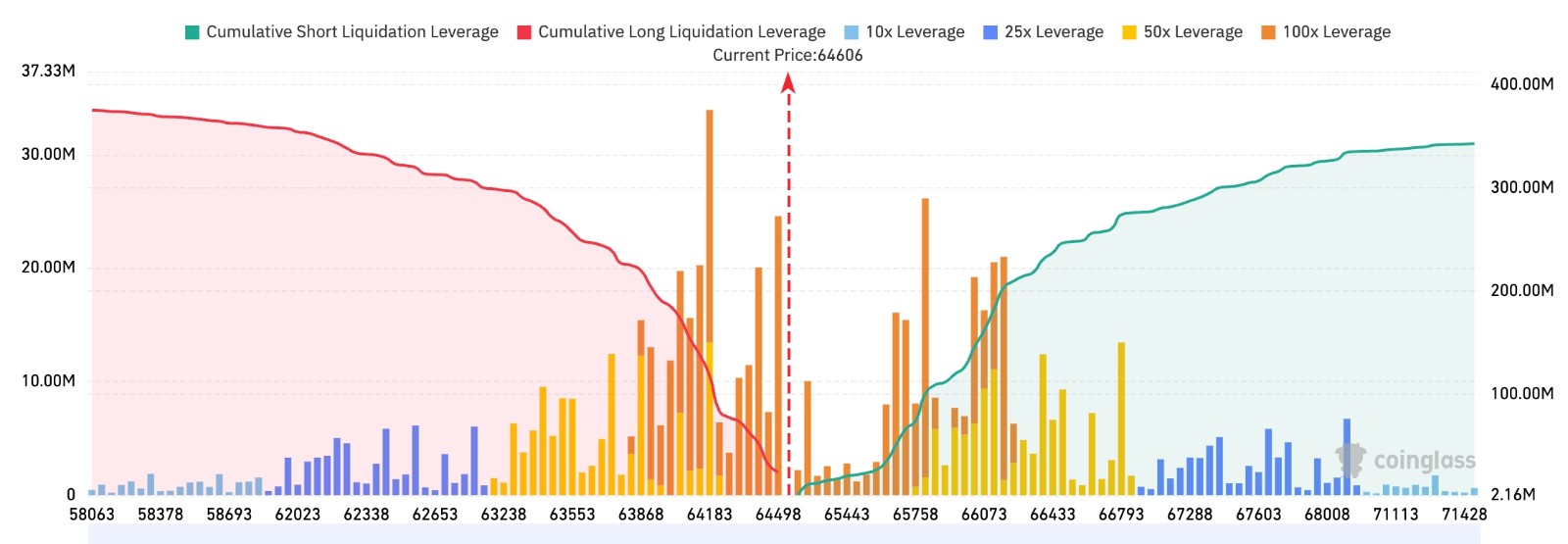

- Bitget BTC/USDT Liquidation Map: Current BTC price is about $64,606, the area above $65,700–$66,100 accumulates more short liquidation pressure, if this range is broken, it may trigger concentrated short covering and push prices to explore further upwards. There is a more obvious long liquidation zone near $63,800–$64,200 below, but the overall scale is lower than the short liquidity above, the short-term market still leans towards testing the upper liquidation band

- Spot ETF Net Inflow/Outflow: BTC Spot ETF net inflow yesterday was $181 million, current 24h dynamic net inflow is $26.9 million.

Driving Factor Analysis: June inflation data significantly cooling boosted market risk appetite, BTC quickly rebounded breaking the key psychological barrier of $65,000 and the 200-week moving average, leveraged long covering and ETF fund inflows formed a合力。ETH followed the rise but the gain was relatively moderate, showing market differentiation led by BTC. BlackRock and other institutional ETFs continuing net inflows reflect traditional capital's warming willingness to allocate crypto assets. At the macro level, the Fed Chair reaffirming independence reduces concerns about political intervention, Trump's rate cut expectations further ease tightening pressure, benefiting risk assets. Leveraged market 24h liquidations exceeding $300 million show volatility remains high, high proportion of short liquidations reflects some profit-taking or reversal signals. Technically, BTC short-term trend is bullish but need to be wary of profit-taking and inflation expectation changes transmitted from geopolitical events. Institutional views generally believe that in a soft data environment the crypto market rebound foundation is relatively stable, but the high leverage environment requires cautious position management.

US Stock Index Performance

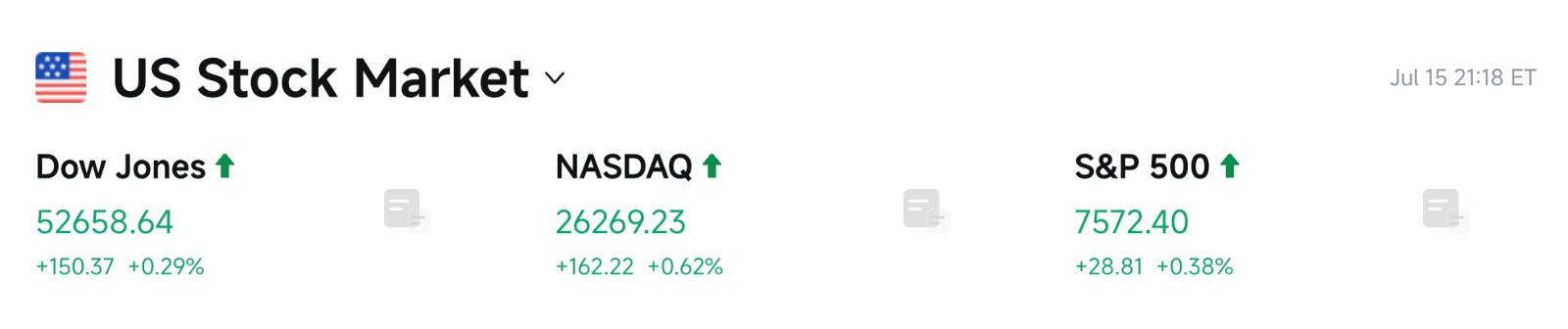

- Dow: 52658.64 (+0.29%), continuous small gains, investor risk appetite回升

- S&P 500: 7572.40 (+0.38%), stood firm on key technical levels, trading volume moderately amplified

- Nasdaq: 26269.23 (+0.62%), tech growth and AI-related sectors drove the lead

Tech Giants Dynamics

- NVDA: 212.50 (+0.33%)

- AAPL: 327.50 (+4.01%)

- MSFT: 395.63 (+2.78%)

- GOOGL: 370.92 (+3.17%)

- AMZN: 254.96 (+3.02%)

- META: 681.31 (+3.07%)

- TSLA: 394.46 (-0.43%)

Performance Summary and Driving Analysis: US stock tech giants overall followed the Nasdaq stronger, boosted by June inflation cooling and strong start to Q2 earnings season risk appetite. Apple, Google, Meta, Amazon, Microsoft generally rose, mainly driven by AI integration progress, cloud business expectations or consumer electronics recovery; NVIDIA small rise shows AI chip demand is robust but may face short-term profit-taking. Tesla small pullback may be affected by specific news. Storage-related stocks (such as MU) fell sharply more than 8%, highlighting sector differentiation—AI data center long-term demand is strong, but short-term supply chain adjustments, regulatory uncertainty (New York suspension order) or capacity concerns led to rotation selling pressure. Overall trend is bullish but individual stock differentiation is obvious, avoid one-size-fits-all, focus on fundamentals and capital flow differences.

Sector Movement Observation

Memory Chip Sector Fell about 8%

- Representative Stocks: Micron Technology (MU) -8%, Western Digital (WDC) -8.7%, SanDisk related stocks -8.12%, SK Hynix -9%

- Driving Factors: Market observed memory concept stocks plummeted, specific reasons may include sector rotation and profit-taking, simultaneously coinciding with AI infrastructure policy discussions (New York suspension approval), may trigger short-term concerns about electricity and infrastructure investment rhythm. Institutions mostly believe pullback provides potential layout window, but need to continuously track demand fundamentals to confirm support strength.

III. In-depth Analysis of US Stocks

1. NVIDIA (NVDA) - Jensen Huang Tokyo Trip Promotes AI and Robotics Collaboration

Event Overview: NVIDIA CEO Jensen Huang recently appeared in Tokyo, actively promoting deep integration of AI technology and the robotics industry. Japan as a global robotics and precision manufacturing powerhouse, this move is seen by the market as NVIDIA's key layout for expanding AI ecosystem in Asia, aiming to extend GPU computing power advantages to robot control systems, autonomous driving, industrial intelligent manufacturing and edge computing 等领域。Background lies in the global AI investment boom continuing to explode, computing demand growing exponentially, while the Japanese government and enterprises are accelerating promotion of "Society 5.0" digital transformation, urgently needing high-performance computing infrastructure support. Notably, this Tokyo trip coincides with the sensitive moment when New York State announced suspension of large data center environmental permit approvals, Trump publicly criticized the decision as "terrible" and called data centers bring "liquid gold" like taxes and jobs, highlighting NVIDIA's importance in dispersing regulatory risks globally and seeking diversified cooperation.

Market Interpretation: Institutional analysts generally believe Huang's Tokyo trip reinforced NVIDIA's irreplaceable core position in the global AI supply chain, helps consolidate long-term demand expectations for its GPU in robotics and intelligent manufacturing scenarios. Although short-term memory chip sector (MU, SK Hynix ADR etc.) appeared obvious pullback due to New York regulatory signals, showing AI infrastructure supply chain exists short-term differentiation pressure, but NVIDIA as AI infrastructure key supplier fundamentals resilience is strong. Market interprets this trip as "ecosystem expansion + global hedging" dual signal, rather than purely earnings-driven event. Combined with Trump and Fed Chair Warsh's statement about AI price increases not necessarily constituting inflation, institutions believe long-term AI capital expenditure cycle remains intact, regulatory noise is more state-level gaming, difficult to block overall trend.

Investment Implications: NVIDIA in AI full stack (chip + software + ecosystem) layout continues to deepen, Tokyo cooperation may become its global diversification strategy new pivot; suggest focusing on tracking order landing situations in robotics and edge AI fields, as long-term core allocation asset, short-term can focus on data center policy evolution impact on valuation volatility.

2. Apple (AAPL) - Accelerating AI Server Chip Autonomous Layout

Event Overview: Market rumors Apple is actively seeking to acquire chip design or related semiconductor companies to accelerate promotion of AI server and self-developed chips in data center and terminal vertical layout. This move core goal is to reduce dependence on external suppliers, improve AI capability integration efficiency and supply chain security, especially under the background of Apple Intelligence (Apple Intelligence) large-scale promotion, terminal and cloud collaboration demand explosion appears particularly urgent. Background highly related to New York State suspension of large data center approval regulatory action—Trump criticized this decision will lead to investment and job loss, and Apple as heavily computing power dependent tech giant, is internalizing chip capabilities to hedge potential infrastructure approval delays and electricity cost rise risks.

Market Interpretation: Wall Street institutional views overall positive, believe Apple this move fits its long-term "hardware + service + AI" strategic closed loop, expected to significantly enhance ecosystem barriers, improve gross margin space and pricing power. Yesterday Apple stock price rose more than 4%, interpreted by market as confidence warming signal for AI transformation story. Although current valuation still at relatively high level, but growth expectations and vertical integration potential provide support. Institutions also pointed out, forming echo with NVIDIA global expansion, Apple's autonomous layout helps reduce exposure to single supply chain, especially under the background of state AI data center regulatory policy differentiation intensifying has more strategic significance.

Investment Implications: Apple AI server and terminal collaboration progress worth continuously tracking, if acquisition lands may become important catalyst; short-term suggest focusing on earnings season management guidance on AI capital expenditure and server deployment, policy uncertainty may bring phased volatility opportunities.

3. Micron Technology (MU) - Memory Sector Large Pullback

Event Overview: Micron Technology and other memory chip stocks fell more than 8% in latest trading day, dragging down entire memory concept sector performance. Background directly related to New York Governor Kathy Hochul announced suspension of new large data center environmental permits for up to one year, Trump publicly blasted this decision as "terrible" and emphasized data centers are "liquid gold", and hedge fund billionaire Dan Loeb fiercely criticized this move as "stupidest decision since Amazon second headquarters project aborted". AI data centers high bandwidth memory (HBM) and DRAM旺盛 demand is memory sector long-term core driving force, while New York regulatory suspension signal may affect short-term US domestic data center construction rhythm and electricity supply expectations, coupled with sector previous gains relatively large, triggered profit-taking and short-term sentiment volatility.

Market Interpretation: Analysts pointed out, memory demand long-term still driven by AI training and inference, fundamentals unchanged, but short-term volatility stems from supply chain dynamics, inventory cycles and policy uncertainty transmission. Institutions generally believe this pullback provides potential buy window—if subsequent demand data continues strong (especially HBM orders), will support valuation repair. Contrasting with NVIDIA, Apple global/AI server layout, Micron etc. US memory enterprises more directly exposed to domestic regulatory policy risks, but also therefore after policy clarification elasticity larger. Market interprets as "short-term noise, long-term logic unchanged".

Investment Implications: In sector differentiation market, select fundamentals robust, HBM capacity layout leading memory individual stocks; focus on New York and other states AI infrastructure regulatory policy actual landing situations, pullback may provide good entry point for medium-long term allocation.

4. SPCX (SpaceX) - Stock Price Continuous Fall and AI Infrastructure Correlation

Event Overview: SpaceX (SPCX) stock price recently fell for fourth consecutive trading day, intraday once broke below $135 issue price, far lower than previous highs. Company AI business segment operates vertical integration platform, covering frontier large language model Grok, AI solutions for consumers and enterprise clients, and AI computing infrastructure, deeply bound with xAI ecosystem. This round of adjustment occurred in New York State suspension of large data center approval, Trump and Fed discussing AI price increase nature same window period, market focuses on SpaceX/AI computing demand potential dependence on data center and electricity infrastructure, and overall tech sector profit-taking pressure.

Market Interpretation: Institutions believe, SPCX stock price fall more reflects listing initial valuation digestion and market rotation, rather than fundamentals deterioration. Its AI computing infrastructure layout and NVIDIA GPU demand, memory HBM orders form industrial chain closed loop, long-term benefits from global AI computing power expansion. Although New York regulatory signal may delay some US domestic data center projects, but SpaceX global satellite + AI strategy possesses certain hedging attributes. Analysts interpret this as "growth tech stocks facing normal volatility at high levels", same as memory sector pullback belongs to short-term sentiment release, rather than trend reversal.

Investment Implications: SPCX as AI + aerospace dual-wheel drive target, suggest focusing on its AI computing infrastructure orders and Grok ecosystem progress; short-term volatility provides observation window, medium-long term AI demand expansion still core logic, need to be wary of volatility risks under high valuation.

5. SK Hynix (SKHY ADR) - Global HBM Leader Memory Sector Large Pullback

Event Overview: SK Hynix (via US stock ADR SKHY) as global high bandwidth memory (HBM) absolute leader and NVIDIA AI GPU core supplier, in latest trading day followed memory concept stocks fell nearly 9%. This round of adjustment highly coincides with New York State suspension of large data center environmental permit approvals—Trump criticized this decision will lead to billions of dollars investment and thousands of jobs loss to other states, and data centers are exactly HBM and advanced storage largest demand source. SK Hynix previously through large-scale ADR issuance landed US stock market, stock performance directly reflects global AI memory supply chain sensitivity to US domestic infrastructure policy changes.

Market Interpretation: Institutional analysts emphasize, SK Hynix HBM capacity and technical barriers in AI era have scarcity, long-term demand certainty extremely high; short-term pullback mainly stems from market concerns New York regulatory suspension may delay US data center construction rhythm, and sector previous gains too large after profit-taking. Contrasting with Micron Technology forming US stock memory dual heroes, SK Hynix through global supply chain (including US clients) still deeply bound AI capital expenditure big cycle. Market interprets as "policy noise under phased adjustment", rather than demand fundamentals turning, Dan Loeb etc. institutional investors fierce criticism of New York decision instead highlights data centers strategic value for economic growth.

Investment Implications: SK Hynix as AI memory core target, after pullback allocation value improves; focus on tracking HBM order fulfillment situations and global data center capital expenditure data, New York and other states policy clarification may become important catalyst, suggest combining Micron etc. US stock memory stocks for industrial chain allocation.

IV. Market & Project Dynamics

1. Cathie Wood's Ark Invest bought about $16.6 million worth of SpaceX stock Wednesday, SPCX fell 0.60% to $135.27 that day. Ark simultaneously sold about $3.9 million worth of Robinhood stock, HOOD rose 1.84% to $115.54 that day.

2. Arthur Hayes疑似 through OTC accumulation ETH. First batch sent 1.25 million USDC to Galaxy Digital, received 646.33 ETH (about $1.24 million); second batch completed through FalconX, received 646.93 ETH (about $1.24 million). Two batches total about 1,293 ETH, total value about $2.48 million.

3. MicroStrategy President and CEO Phong Le in an interview with Bloomberg Television said, the company will not stop buying Bitcoin, "in the foreseeable future goal is to become the largest Bitcoin buyer". He said only when Bitcoin falls to about $8,000-$10,000 need to consider debt risks, currently "very reassured" about balance sheet.

4. Fed Governor Cook said, there is reason to believe inflation will continue to cool, but tariffs, Middle East conflicts and artificial intelligence investment may lead to price pressure continuing; waiting for inflation to slow further for a period is wise, if recent no see inflation cooling, prepare to take action.

5. Wall Street Journal reported, US officials said, after holding brief meetings with several senior aides for several days, US President Trump is leaning towards expanding US military action against Iran. Potential options include strengthening air strike intensity, dispatching ground troops to seize Iranian islands near Strait of Hormuz, and bombing a fortified site possibly used for secret nuclear work.

6. July 15 news, market news: Anthropic plans to hold IPO investor meetings in coming weeks.

7. According to people familiar with Apple work, Apple is looking to acquire chip companies to strengthen its efforts to build server chips used for running artificial intelligence. In recent months, the iPhone manufacturer has communicated with bankers about possible deals. Sources said, it also contacted semiconductor startups, understanding if they intend to sell themselves. Apple seeking chip acquisition action coincides with company internal AI server performance problems.

V. Today's Market Calendar

Data Release Schedule

Important Event Preview

- Event: Bank of Korea Rate Decision - Focus on whether to start first rate hike since 2021, affecting Asian currency and risk asset sentiment

- Event: US Data Release - Retail Sales and Initial Claims data will further verify labor market and consumption resilience

Institutional Views:

According to past 24 hours US stocks, precious metals, crude oil, forex and cryptocurrency trends, Wall Street mainstream investment bank analysts generally believe, June inflation data cooling provided Fed policy with larger flexibility space, Chair Warsh reaffirming independence further stabilized market expectations for policy consistency, benefiting risk assets including US stock tech sector and cryptocurrency rebound. Gold at high levels faces certain profit-taking but long-term safe-haven attributes remain; oil prices short-term supported by geopolitical factors, but Trump long-term bearish view may limit continuous upward momentum. Crypto market under ETF inflows and leveraged covering push shows strong resilience, but high volatility and liquidation risks remind investors to note positions. Overall, institutional consensus leans towards "data-driven cautious optimism", suggest focusing on subsequent retail sales and employment data corrections to rate cut expectations, and AI infrastructure regulatory policy evolution actual impact on industrial chain. Differentiation market, selecting individual stocks and theme allocation more critical.

Disclaimer: Above content organized by AI search, artificial only verification publication, not as any investment advice. Data in text inevitably exists deviations, please refer to market instant data为准。

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News