Bitget UEX Daily Report | U.S. and Iran Reach Agreement to Reopen the Strait of Hormuz; SpaceX Surges 19% on First Trading Day, Market Cap Exceeds $2 Trillion; Asia-Pacific Equities Rally, Japan and South Korea Lead Gains

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S. and Iran Reach Agreement to Reopen the Strait of Hormuz; SpaceX Surges 19% on First Trading Day, Market Cap Exceeds $2 Trillion; Asia-Pacific Equities Rally, Japan and South Korea Lead Gains

The overall market has entered an observation period. Focus on guidance from the G7 and economic data regarding liquidity, and consider inter-asset correlations and valuation divergence.

I. Top News

Federal Reserve Updates

Fed Monitors U.S. Treasury Yield Pressure and Policy Path

- Goldman Sachs’ head of trading noted that if the 10-year U.S. Treasury yield reaches 5%, it could materially pressure U.S. equity valuations; while this threshold has not yet been breached, bond market volatility is intensifying.

- Investors are closely watching the upcoming FOMC meeting, with rate expectations facing repricing.

- Market impact: Amid AI-driven strength in equities, rising Treasury yields may dampen risk assets; near-term focus should be on potential drag from bond markets on equity valuations.

Global Commodities

U.S.-Iran Deal Eases Geopolitical Tensions, Weighing on Oil Prices

- Trump announced the Strait of Hormuz would be opened for free navigation and lifted its blockade; the U.S. and Iran signed a ceasefire memorandum of understanding, with an official ceremony scheduled for June 19 in Switzerland.

- An Israeli airstrike prompted criticism from Trump, yet the broader agreement reduces escalation risks.

- Market impact: The deal eases supply concerns, driving oil prices lower—supportive for risk assets but potentially negative for energy stocks.

Macroeconomic Policy

G7 Summit Opens Amid Focus on Economic Data

- The 52nd G7 Summit is underway in France, centered on global economic coordination.

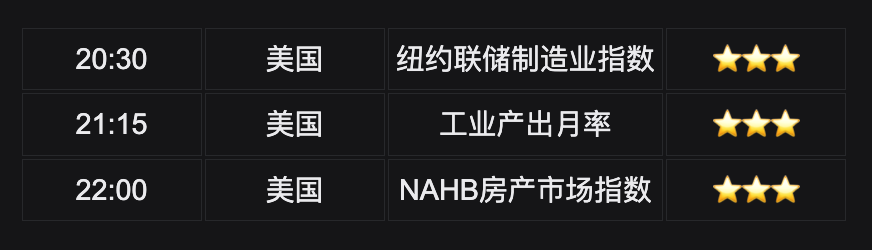

- Today’s key U.S. data releases include the New York Fed Manufacturing Index, Industrial Production, and the NAHB Housing Market Index.

- Market impact: These data points and summit outcomes will influence Fed expectations and risk sentiment; current geopolitical easing provides a relatively stable backdrop for policy discussions.

II. Market Recap

Commodities & FX Performance

- Spot Gold: ~$4,300/oz, +2%.

- Spot Silver: ~$70/oz, +2.8%.

- WTI Crude: ~$80/bbl, -4.24%.

- Brent Crude: ~$84/bbl, -3.74%.

- U.S. Dollar Index (DXY): ~99.57, -0.23%.

Drivers Analysis: The U.S.-Iran ceasefire agreement significantly eased geopolitical risk, and expectations of opening the Strait of Hormuz weakened concerns over crude supply disruptions—causing oil prices to fall sharply. Gold and silver benefited from improved risk sentiment and relative dollar stability, posting rebounds. The DXY traded in a narrow range, reflecting market caution awaiting Fed policy cues amid geopolitical easing. Overall, asset correlations were pronounced: reduced geopolitical risk boosted equities and crypto, but pressured energy prices; gold, as a safe-haven asset, faced short-term pressure yet retained support from industrial and investment demand. Consensus among institutions is that macro data and G7 outcomes will dominate near-term price action; if inflation remains on a moderate path, precious metals may retain resilience, while oil supply-demand rebalancing hinges on implementation of the agreement.

Cryptocurrency Performance

- BTC: ~$65,500, +1.2%.

- ETH: ~$1,720, +1.9%.

- Total Crypto Market Cap: ~$2.32 trillion, +1.3%.

- Liquidations: ~$324 million in 24h, with ~$230 million in short liquidations.

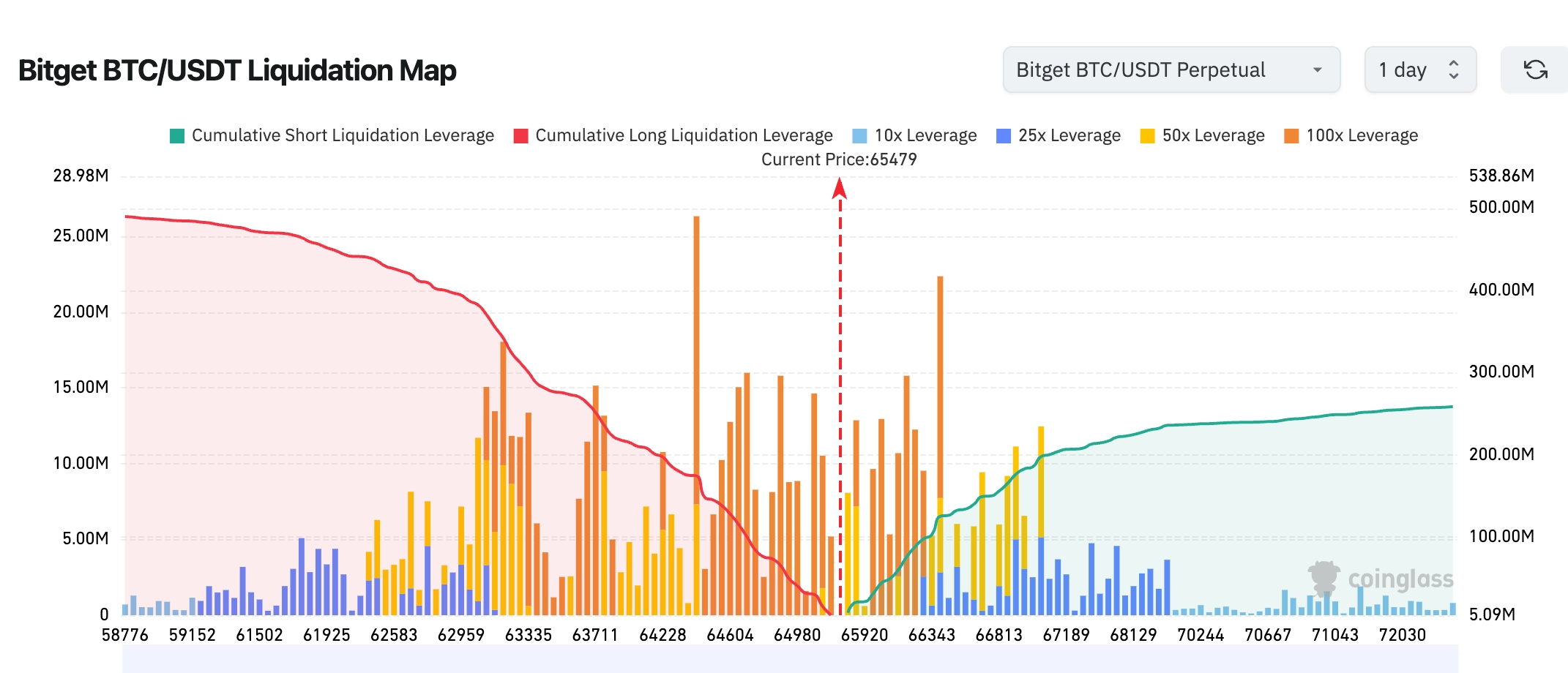

- Bitget BTC/USDT Liquidation Map: BTC currently trades at ~$65,479; the long liquidation zone between $64,500–$65,000 has largely been cleared, markedly reducing near-term downside leverage pressure. A substantial short liquidation cluster sits above $66,300–$67,200; if BTC continues upward and breaks above $66,000, short covering may accelerate price gains toward $67,000+.

- Spot ETF Net Flows: As of last Friday, BTC spot ETFs recorded ~$86 million in daily net inflows.

Drivers Analysis: The U.S.-Iran agreement boosted risk appetite, and SpaceX’s successful IPO provided positive spillover effects, catalyzing crypto markets. Both BTC and ETH rebounded, total market cap stabilized, and ETF flows turned modestly positive—relieving prior outflow pressure. Liquidations were predominantly short positions, indicating forced covering pushed prices higher. Technically, BTC has formed a base above $60,000; institutional views hold that improving macro conditions and capital inflows support the near-term trend—but ETH performance diverges, influenced by AI and Layer 2 narratives. Overall, market sentiment shifted from prior panic to cautious optimism, with attention now on Fed policy and upcoming macro data’s implications for liquidity.

U.S. Equity Index Performance

- Dow Jones: Closed at ~51,202, +0.7%, extending its upward trend.

- S&P 500: Closed at ~7,431, +0.50%, exhibiting steady performance.

- Nasdaq: Closed at ~25,889, +0.31%, driven by technology and semiconductor stocks.

Tech Giants’ Updates

- NVDA: ~$205.19, +0.16%.

- AAPL: ~$291.13, -1.52%.

- MSFT: ~$390.74, +0.10%.

- GOOGL: ~$359.68, +0.53%.

- AMZN: ~$238.55, -1.23%.

- META: ~$566.98, -0.26%.

- TSLA: ~$406.43, +1.82%.

Summary & Drivers: Tech giants broadly followed the broader market higher. SpaceX’s first-day IPO surge (+19%) and market cap exceeding $2.1 trillion bolstered investor confidence; semiconductors mostly rose (NVDA edged up slightly). However, stock-level divergence emerged: TSLA outperformed on positive catalysts, while AAPL and AMZN posted modest pullbacks. AI-related names gained on valuation expansion, whereas some consumer-tech stocks faced valuation pressure or internal adjustments. As highlighted in Futu Morning Brief, space and AI enthusiasm persists—but rising yields pose a potential headwind for high-valuation stocks.

Crypto Stock Derivatives Overview

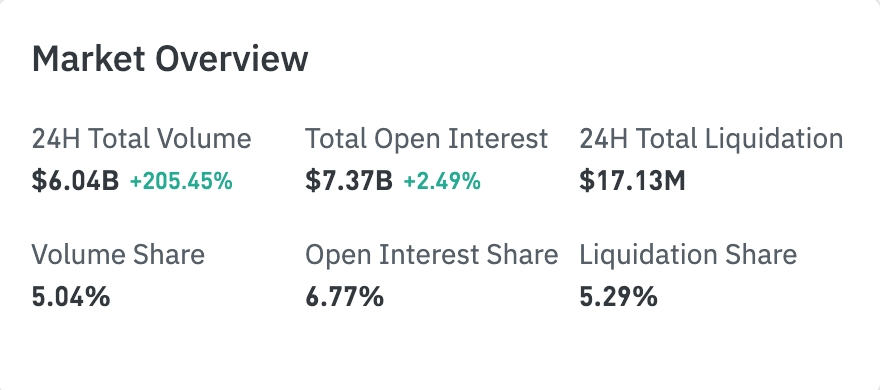

- Stock derivatives market activity surged notably, with 24-hour total volume reaching $6.033 billion—a 204.94% increase.

- Total open interest rose to $7.358 billion (+2.39%), signaling continued capital inflow.

- 24-hour total liquidations amounted to $17.13 million—modest relative to the sharp volume expansion.

Sectoral Open Interest Breakdown

- Technology sector open interest: $1.342 billion—far exceeding other sectors and remaining the core trading theme.

- Financials: $160 million—second-largest.

- Consumer discretionary: $67.64 million—significantly ahead of Industrials and Biotech.

- Industrials ($24.96 million) and Biotech ($13.07 million) attracted comparatively less attention.

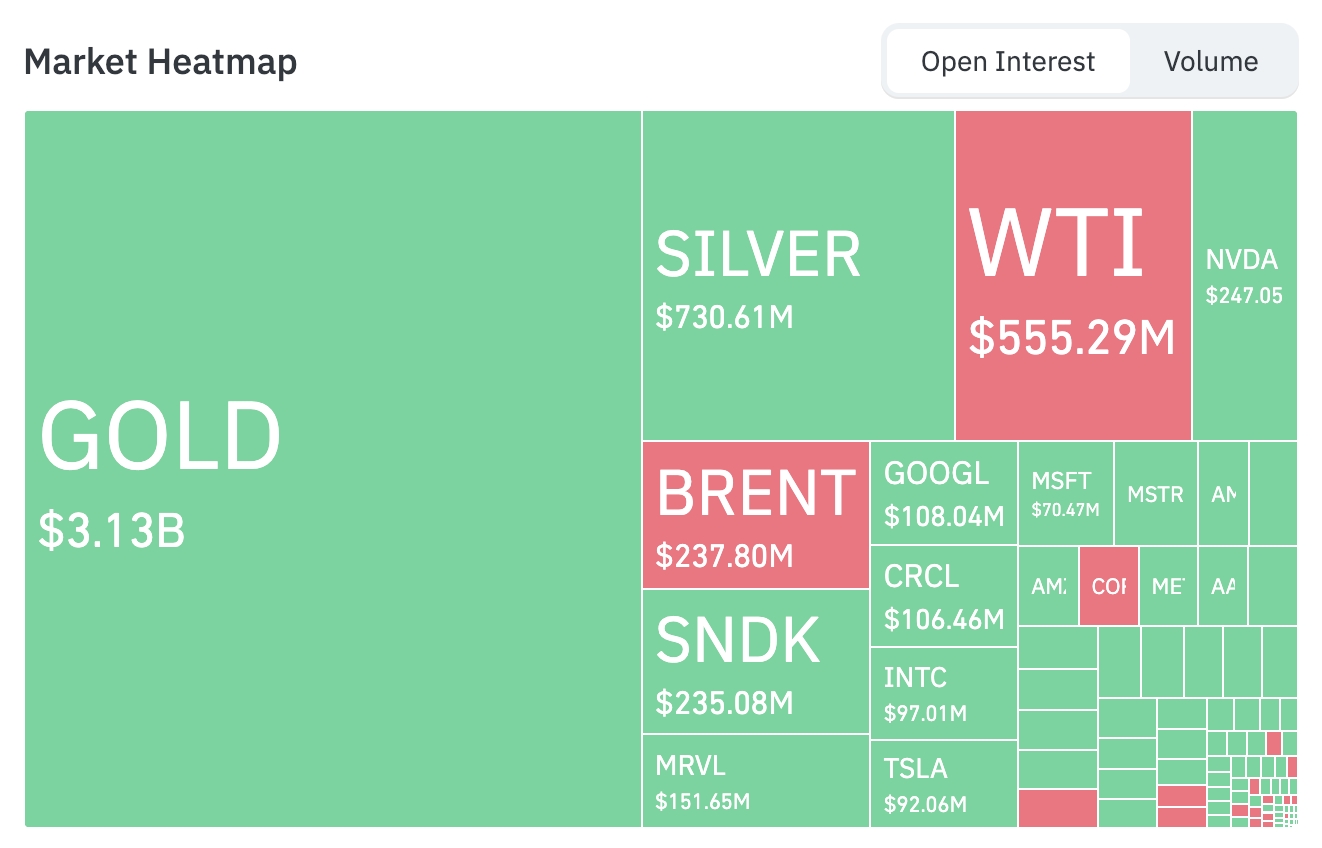

Heatmap Capital Allocation (by Open Interest)

Commodities

- Gold (GOLD): ¥3.125 billion—the largest position, reflecting strong ongoing safe-haven demand.

- Silver (SILVER): ¥728 million—second-largest.

- WTI Crude (¥556 million), Brent Crude (¥238 million)—substantial but well below precious metals.

Tech Stocks

- NVIDIA (NVDA): ¥247 million—top tech stock holding.

- SanDisk (SNDK): ¥235 million; Marvell Technology (MRVL): ¥152 million—highlighting continued bets on AI memory and semiconductor supply chains.

- Google (GOOGL): ¥108 million; Circle (CRCL): ¥106 million—both exceeding ¥100 million.

- Intel (INTC): ¥97.12 million; Tesla (TSLA): ¥92.07 million—maintaining elevated interest.

Sectoral Volatility Observations

Semiconductor Sector Mostly Up, Yet Stock-Level Divergence Notable

- Key movers: ARM +11%+, Seagate +7%+, Intel and Western Digital +6%+, SanDisk +5%+, AMD and Qualcomm +4%+; Micron down ~1.4%.

- Drivers: Sustained AI memory and chip demand underpins sector-wide strength, yet fundamentals vary across stocks—impacted by supply chain developments, valuation adjustments, and company-specific news.

Media/Consumer-Tech Sector Volatility

- Roku Inc. (ROKU): +~20%, its largest single-day gain since November 2023.

- Drivers: Rumors of potential sale negotiations, combined with broad risk sentiment improvement, fueled strong rebound.

Aerospace/Emerging-Tech Sector Surge

- SpaceX (SPCX): First-day IPO gain of +19%, ~$80 billion in trading volume, market cap surpassing $2.1 trillion.

- Drivers: As the aerospace leader, its successful IPO—not only breaking records but also boosting investor confidence in high-growth tech themes—was further amplified by ARK Invest’s large-scale buying.

Software Sector Pullback

- Adobe (ADBE): -6.7%, its worst single-day performance recently.

- Drivers: Dragged by internal developments or market concerns about software stocks’ growth sustainability, underscoring intra-sector divergence.

III. In-Depth Stock Analysis

1. SpaceX (SPCX) – IPO Debut

Event Summary: SpaceX officially debuted on Nasdaq, opening above its $135 IPO price and trading relatively steadily before closing ~19% higher near $161, pushing its market cap past $2.1 trillion—making it the sixth-largest U.S. company. Trading volume exceeded 500 million shares, with ~$80 billion in turnover, setting multiple IPO records. Cathie Wood’s ARK Invest acquired ~3.29 million shares via private placement, totaling ~$443 million—making SpaceX its Venture Fund’s top holding. Options trading launches next week, enhancing market liquidity and hedging tools. Its pre-IPO valuation (~$2 trillion) and massive fundraising (~$7.5 billion) expanded further post-IPO, reflecting robust investor conviction in the long-term space economy. Market Interpretation: Wall Street widely views SpaceX as a technological and commercial leader in space exploration and satellite internet, with its monopoly-like advantages in Starlink and Starship seen as long-term growth engines—even at premium valuations. Its smooth listing also eased concerns about liquidity strain from a wave of mega-IPOs. Investment Implications: SpaceX sets a benchmark for emerging tech, with short-term spillover likely into related supply chains; however, profit-taking pressure warrants caution given lofty valuations. Monitor upcoming earnings, contract execution, and options market development for entry timing.

2. Adobe (ADBE) – Sharp Price Decline

Event Summary: Adobe fell 6.7%—its worst one-day performance since March—with elevated trading volume. This move links to recent corporate developments and broader software sector valuation reassessment, though no single catalyst dominated; rather, it reflects weaker defensive positioning within the broader tech rotation. Market Interpretation: Analysts argue that AI-fueled enthusiasm has lifted traditional software giants’ valuations beyond fundamentals, prompting questions about growth sustainability and capital return efficiency. As a creative-software leader, Adobe continues investing in AI features, yet near-term cost pressures and intensifying competition have tempered sentiment. Investment Implications: Short-term volatility offers a window for observation; prioritize tracking next quarter’s AI product monetization metrics and management guidance—if fundamentals stabilize, this may present a medium-term accumulation opportunity.

3. Roku (ROKU) – Strong Rebound

Event Summary: Roku surged ~20%, its largest single-day gain since November 2023, accompanied by sharply higher volume. Market rumors suggest the company may be engaged in potential sale or strategic transaction talks, and improved risk sentiment helped lift shares off recent lows. Market Interpretation: Institutions view Roku as a critical infrastructure provider in streaming—its moat in advertising and content distribution remains attractive, especially amid consumption recovery expectations; potential acquisition premiums serve as a key catalyst. Investment Implications: Event-driven momentum suits short-term trading, but beware of rumor falsification risk; watch for official announcements and industry consolidation progress.

4. Sivers Semiconductors (SIVE) – AI Optical Collaboration

Event Summary: Sivers Semiconductors deepened its silicon photonics partnership with GlobalFoundries to develop co-packaged and pluggable optical solutions for AI data centers, and secured an ~$8.2 million Ka-band beamforming IC production order from All.Space. Though Q1 revenue declined year-on-year and operating losses widened amid cash burn, order pipeline and strategic alliances lifted sentiment, triggering notable price volatility and a partial rebound. Market Interpretation: Analysts recognize its technical expertise in optical interconnects for AI infrastructure; capacity expansion and CHIPS Act-related support—if realized—could meaningfully improve its long-term growth trajectory, though near-term execution risks and valuation swings remain concerns. Investment Implications: Suitable for AI supply-chain thematic allocation; assess holdings based on order execution progress, and monitor potential dual-listing developments for enhanced liquidity.

5. AXT Inc. (AXTI) – Indium Phosphide Shortage & AI Demand

Event Summary: AXT Inc.’s share price saw sharp fluctuations, driven by reports of potential indium phosphide export restrictions and surging AI data center material demand. Analysts repeatedly raised price targets. The company is expanding capacity actively; Q1 results showed improved gross margin and a backlog of $100 million. Despite governance matters and financing activities, AI-driven demand remains the core catalyst. Market Interpretation: Institutions see AXT’s dominant position in semiconductor substrate materials—especially indium phosphide—as directly benefiting from data center and 5G/6G expansion, though geopolitical export risks represent the main uncertainty. Investment Implications: Medium-term bullish on AI materials theme; track capacity rollout milestones and geopolitical policy developments, and manage position sizing to mitigate high volatility.

IV. Views & Updates

1. Brian Armstrong posted on X: “My conviction in Bitcoin remains unchanged—I continue holding a long-term bullish position. Things are never quite as good—or as bad—as they appear.”

2. Serenity wrote on X: “Technical analysis (TA) is more like astrology for traders—a blend of confirmation bias and market psychology used to gauge sentiment, not a primary price driver. Major rallies in stocks aren’t chart-based—they’re rooted in fundamentals and expectations. For example, $SIVE’s ~1900% surge stems from market repricing of future revenue tied to $JBL and $GFS partnerships; $AXTI’s ~8000% rise reflects industry logic around indium phosphide substrates, photonics demand, and export controls.”

Serenity added: “TA mainly reflects participants’ psychological expectations—for instance, chart-based predictions around $IREN cannot offset structural supply pressure from large-scale funding events (ATM). Real price drivers include sectoral theme linkages, earnings expectation shifts, macro environment, financial reporting, and float structure.”

“TA may help identify entry timing—but long-term upside must rest on fundamentals and capital structure, not ‘chart faith.’”

3. Tokenized Pokémon cards are seeing rapidly growing trading volumes on crypto platforms. Powered by gacha mechanics, physical cards are mapped to NFTs or digital certificates—creating a ‘pack-opening’ or ‘card-drawing’ experience. Per Messari data, trading volume across seven blockchains—including Solana, Polygon, Base, and BNB—reached ~$230 million in May, up ~10x YoY.

4. Pakistani Prime Minister Shehbaz Sharif announced Sunday that the U.S. and Iran have declared hostilities terminated. A formal signing ceremony is expected this Friday (June 19) in Switzerland, followed by detailed nuclear negotiations. Sharif posted on X: “A peace agreement between the United States of America and the Islamic Republic of Iran has been reached. Both sides have declared an immediate and permanent cessation of military operations on all fronts—including within Lebanon.” He added, “This agreement is now in effect.” Trump confirmed the news and stated he is lifting U.S. sanctions, expecting Iran to open the Strait of Hormuz. Iran responded affirmatively.

5. According to Xinhua News Agency, the UK, France, Germany, and Italy jointly issued a statement saying that, following the U.S.-Iran war-ending agreement, parties are prepared to lift sanctions on Iran in exchange for concrete steps on its nuclear program.

6. Analyst Darkfost posted on X: “On-chain behavior of Bitcoin long-term holders (LTHs)—those holding for over six months—still shows ‘phased high-intensity selling,’ typically marked by daily inflows to exchanges far exceeding annual averages (up to 5x or more).”

“Short-term, LTHs continue transferring BTC to exchanges—indicating persistent near-term selling pressure, often translating into actual sales. Long-term, however, the annual average LTH inflow to exchanges is trending downward, suggesting greater holding discipline—and gradually smoothing overall market sell-side pressure.”

“Data shows a slight uptick recently—from ~630 BTC/day in early May to over 800 BTC/day—yet still within the lowest historical range since 2015. This shift may reflect rising ETF and institutional participation altering LTH composition, but overall, LTHs’ systemic sell pressure on mid-to-long-term markets is diminishing.”

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

- G7 Summit: June 15–17—Global economic policy coordination.

Institutional Views:

Top-tier investment banks broadly agree that the U.S.-Iran agreement has meaningfully improved risk sentiment—boosting equities and crypto—but falling oil prices highlight ongoing supply-demand rebalancing. SpaceX’s successful IPO reinforced tech confidence, while Goldman warns that approaching the 5% Treasury yield threshold could pose pressure. In crypto, modest ETF inflows and leveraged liquidations support near-term rallies; institutions see BTC consolidating within its current range, but stress that Fed policy and macro data will dictate H2 direction. Markets have entered an observation phase—watch G7 outcomes and economic data for liquidity signals, and remain attentive to cross-asset correlations and valuation dispersion.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain unavoidable discrepancies; always refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News